ELSS or Equity Linked Savings Scheme of Mutual Funds are one of the best tax saving cum long-term wealth creation investment tools. Your investments in ELSS schemes are eligible for income tax deduction under Section 80c.

Tax saving is one of the most important investment objectives of many investors. In the next few days, the current Financial Year (2017-18) is going to end and the new one (FY 2018-19) will begin. So, when is the right time to start planning your taxes? Is it good to wait till next IT declaration season or March (2019) for tax planning?

You may kick-start your tax planning from this April itself. Don’t wait till March 2019!

And, which is the best available investment option for tax saving cum long-term wealth accumulation in Equity products?

I believe that ELSS (Equity Linked Savings Scheme) is one of the best tax saving options that we currently have in the financial market.

Why ELSS Funds?

- ELSS Tax saving mutual funds come with a lock-in period of three years; the lowest among all the tax saving options that are available under Section 80C. (PPF’s lock-in period is 15 years, Tax saving Bank Fixed Deposit’s is 5 years, National Saving Certificate’s is 5 years etc.,)

- There is no upper limit for investment in ELSS but the maximum tax benefit is limited to Rs 1.5 lakh under Section 80C.

- Investing in ELSS funds can give you a better chance to get better inflation adjusted returns (of course higher returns may generally associate with higher risk profile).

Top 5 Best ELSS Mutual Fund Schemes for FY 2018-19

As you may be aware that we have been witnessing a few major changes in the mutual fund industry namely : SEBI’s re-categorization’ norms, 10% LTCG tax on Equity mutual funds, changes in Expense ratios of mutual fund schemes etc.,

All these years, SEBI/AMFI have been allowing multiple funds under same fund categories from same AMCs, in order to bring the desired uniformity across mutual funds and to standardize the various MF scheme categories, the SEBI through Mutual Fund Advisory Committee has issued new guidelines on ‘new Categorization of Mutual Fund Schemes.’

As per these new norms, only one scheme per category would be permitted. ELSS Tax saving funds are one of the 11 categories (under Equity Funds) proposed by the SEBI. The mutual fund houses have already started implementing these re-categorization rules. (Related Article : ‘Mutual Fund Schemes Categorization and Rationalization – Types of MF Schemes | SEBI’s Latest Guidelines‘)

To meet these new guidelines all the mutual fund houses may have to merge, modify or close their available schemes. This is the main reason for not publishing the ‘Best Equity Mutual Funds 2018’ article.

As per my last year’s analysis, below are the top performing Tax saving mutual funds for FY 2017-18 ;

- DSP Blackrock Tax Saver Fund

- Birla Sunlife Tax Plan

- Birla Sun life Tax Relief ’96

- Franklin India Taxshield Fund

- Axis Long Term Equity Fund

Due to SEB’s new norms, we can expect Birla Sulife Tax Plan to be merged into Birla Tax Relief ’96 Fund. Hence, I am replacing this fund with TATA India Tax Savings Fund in this year’s best ELSS Funds list.

Below are the top performing & Best Tax saving mutual funds for 2018 – 2019 and their lump sum investment Returns; (Returns are for Regular plans and Growth option)

- Birla Sun life Tax Relief ’96

- DSP Blackrock Tax Saver Fund

- Axis Long Term Equity Fund

- TATA India Tax Savings Fund

- Franklin India Taxshield Fund

Below are the best ELSS Funds and their monthly SIP Returns ;

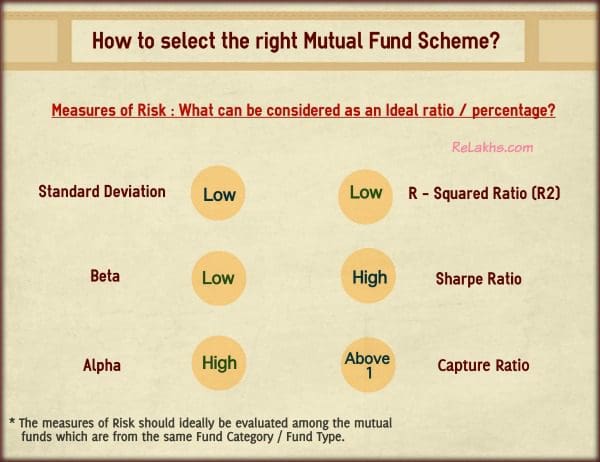

Best ELSS Mutual Fund Schemes & Risk Statistics

Above data gives us information mainly on past Returns that were generated by these top performing ELSS mutual funds. Besides investment returns, it is equally important that we need to look at the Risk Stats of these Funds.

The volatility of returns generated by a mutual fund scheme can be measured by some important risk ratios like;

- Standard Deviation

- Beta

- Alpha

- Sharpe Ratio

- R-Squared Ratio

- Upside & Downside Ratios

Below info-graph gives us an idea about ideal ratio/percentage that can be considered while selecting a mutual fund scheme;

I have shortlisted the above listed best ELSS Funds based on these measures of volatility as well;

(Source : Valueresearchonline.com)

Best ELSS Funds & Analysis :

- Birla Sun life Tax Relief ’96 : This fund is one of the oldest ELSS Funds and has been a consistent performer for the last few years. We can consider this fund as a typical Multi-cap one with a higher allocation to Mid-cap stocks. The fund’s portfolio has stocks from these top 3 sectors – Auto, Banking & Pharmaceuticals. The current portfolio has an allocation of around 52% to Mid & Small cap stocks and around 40% in large-cap stocks. The fund management team has remained very stable since 2006. The winning investment strategy of this fund has been its ability to pick quality mid-caps for the long haul. The returns generated by this fund during last 5 & 10 years are 22% and 12% respectively.

- DSP Blackrock Tax Saver Fund : This fund has outperformed its benchmark (Nifty 500) in eight out of nine years since launch and its peers in seven of those years. DSP Tax saver fund does not follow any particular investment style as such but sticks to ‘blended’ model. The fund has been a large-cap oriented in the last five years with an allocation of around 69% to large cap stocks and around 24% to mid-cap stocks. The top sectors chosen by this ELSS fund are Banking, Oil & gas and Auto. The fund has seen a change in fund manager during 2015-16 and since then the management team has been bettering more on Large cap stocks. We need to keep a close watch on this fund’s performance for the next couple of years. The returns generated by this fund during last 5 & 10 years are 20% and 14% respectively.

- Axis Long Term Equity Fund : This is one of the largest Equity Funds (AUM wise) in India. The fund’s portfolio typically invests in 50 to 70% in large cap stocks with the remaining portion of portfolio invested in small & mid-cap stocks. The current allocation to large caps is around 63%. The top three sectors that have been invested in are – Banking, Auto & Chemicals. It witnessed a slowdown in performance in 2016 but has recovered in 2017. This can be a good example as to why one should not churn his/her MF portfolio frequently and advisable to give enough time for the consistent performers before dropping them from their investment list. The returns generated by this fund during last 5 are around 23%. But, let’s not forget the fact that this fund is yet to be tested in a severe market meltdown, being a ‘late entrant’ (year of launch – 2009).

- TATA India Tax Savings Fund : This fund follows a typical Multi-cap approach. The current portfolio allocation is around 57% in Large cap stocks, 32% in mid-cap stocks and 10% in Small cap stocks. The top three sectors that have been invested in are – Banking, Cement & Oil/Gas. Historically, this fund has been good at containing losses during bear phases such as 2001, 2008 and 2011. It has also performed well during the current bull phase of the market. This fund can be considered by the investors with good risk appetite. The returns generated by this fund during last 5 & 10 years are 21% and 13% respectively.

- Franklin India Taxshield Fund : I believe that this ELSS fund is a right choice for a ‘conservative’ investor. It has been maintaining a large-cap bias amid different market phases. Its ‘ability to contain downside‘ and ‘consistency‘ of returns are its main features. Advisable not to expect abnormal returns from this fund even during a bull phase. There has been a change in fund manager during 2016-17. The returns from this fund has been low compared to its benchmark and category for the last couple of years. We need to keep a track of its performance for the next couple of years. The top three sectors that have been invested in are – Banking, Auto & Oil/Gas. The returns generated by this fund during last 5 & 10 years are 18% and 14% respectively.

Let’s also keep an eye on L&T Tax Advantage Fund, IDFC Tax Advantage (ELSS) Fund & Principal Tax Savings Fund

My Investments in ELSS Funds :

Personally, I have been investing in Axis Long Term Equity fund and my spouse invests in Birla Tax Relief ’96 Fund.

FAQs on ELSS Funds

- My Section 80C bucket is full, should I still invest in an ELSS Fund? – You may consider investing in other mutual fund categories based on your investment objectives and time-frame. (Read : ‘Best Equity Mutual Fund Schemes – 2017‘)

- What is the best way to invest in ELSS – Lump sum or SIP mode? – There is no right or wrong answer. For the sake of convenience, I prefer 2 to 4 lump sum installments in a FY instead of monthly SIPs. Let’s understand the fact that timing the market is next to impossible. If you do not have the time to track the markets, it is perfectly ok to create a SIP in an ELSS fund. But, do note that units allotted under each SIP are locked for 3 years. (Read : SIP Vs Lump sum investment!)

- Dividend or Growth option, which is better for ELSS investment? – It is advisable to make investments in ELSS Schemes for long-term goals, so Growth option is better than dividend for long-term wealth accumulation.

- Direct Plan or Regular plan? – There is no doubt that the direct plans of ELSS MF Schemes outperform their respective Regular plans. Hence, you may consider investing in Direct plans, in case you have the required expertise, skills and time to pick the right ELSS fund for your long-term goals.

- Are ELSS funds also Multi-cap funds? – We need to look at Funds’ Portfolio allocations to consider them as Large cap or mid-cap or multi-cap oriented funds. As mentioned in the above analysis, funds like Birla Tax Relief, Axis LTE or TATA Tax savings Scheme typically follow multi-cap approach. (Do note that Portfolio allocations can change over a period of time depending on the market cycles / Fund’s investment strategy.)

- Should I invest in Multiple ELSS Funds? – If you have already made investments in an ELSS fund, you may continue making additional investments in the same fund. But, do track its performance at least once in a year.

- Is Lock-in period for ELSS Investments applicable on unfortunate demise of the Investor? –

- ELSS mutual funds have a lock-in period of 3 years. In the event of death of the investor, the nominee or the legal heir can withdraw the amount, only 1 year after the date of allotment of units to the deceased (original investor / unit-holder).

- For example : If the investor dies eight months after purchasing the units, the nominee has to wait for at least four more months to be able to sell the units (if he/she wants to redeem..).

- Kindly note that nominee can get the units transferred to him/her much earlier but can’t sell those until 1 year is over. Essentially, the lock-in period goes down from 3 years to 1 year in the event of demise of the original investor. This information can be found in any of the ELSS funds ‘scheme information documents’.

- Can I invest in Joint names? – Yes, investments in ELSS funds can be held in joint-names. But, the first account holder (primary) can only claim tax benefits u/s 80c.

- ULIPs Vs ELSS, which is a better investment option? – You may kindly go through my article on this topic @ ‘Mutual Funds Vs ULIPs – Which is better? | Post Budget (2018) LTCG Tax proposal on Equity Mutual Funds & Shares.’

Kindly note that ‘Tax saving’ is just one aspect of ELSS investments. Wealth creation should also be an equally important objective. The key to equity investment is to remain invested for a sufficiently long time horizon of at least 5-10 years.

Have you invested in any of the above Best ELSS mutual funds? Do you also believe that ‘Mutual Fund ELSS’ is a good tax saving instrument? Kindly share your views and comments.

Continue reading :

- Budget 2018 LTCG Tax on Equity Mutual Funds & Important Implications

- Mutual Fund Capital Gains Taxation rules for FY 2018-19 / AY 2019-20

- Is Lock-in period for Investments applicable on unfortunate demise of the Investor?

- List of important Tax Deductions for FY 2018-19 | How to save tax for AY 2019-20?

- Why your Best Mutual Fund Schemes may not remain as ‘the best’? | SEBI’s new re-classification rules

(References : valuereasearchonline, moneycontrol, freefincal & morningstar portals)

( Image courtesy of Stuart Miles at FreeDigitalPhotos.net) (Post published on 27-March-2018)

Join our channels

Thanks Sreekanth for sharing such a detail blog. I have learnt a little bit more about ELSS mutual fund schemes through this.

Keep writing such informative blogs. All the best!

Dear Sreekanth,

I am the regular visitor of your blog and thanks for the service.

I have invested in Principal Cash Management fund before IL&FS issue which is currently under loss by 10%.

Shall I keep invested or exit? Can you advise if it is sensible to stay invested in the fund and expect recovering some of the losses in coming months (with news that govt is taking over IL&FS)? Or better to exit now?

Also I understand that if I exit now, the loans which have been written off are gone for me (due to exit), even if the same are recovered in future? Please help understand how the process works?

Thanks & Best Regards,

Madhavan

Dear Madhavan,

Thank you for being a loyal reader!

“If you have invested in a debt fund that has got affected by IL&FS defaults, should you withdraw? “No,” said Sen. “There’s not much that investors in these affected debt funds can do, now that the NAVs have already fallen post default and downgrades.” Sen said that if a solution is worked out at IL&FS and the companies pay their lenders (mutual funds and insurance companies), then the payment will push up the NAVs of those funds that had to mark them down earlier. “Exiting immediately means booking the loss, rather remaining invested will help recoup through accruals over time,” said Amandeep Chopra, head fixed income, UTI Asset Management Company Limited.

If you are invested in affected FMPs, it’s always better to stay invested till maturity. But even in open-ended funds, it makes sense to stay invested in these funds as IL&FS itself is busy working out a solution.”

(Source : Livemint).

Thanks Sreekanth for your reply…

Respected sir,

I got my first job last month with a monthly take home salary of 20,000. I can save and invest 5,000 per month. My friend told me about your website.

Can you please suggest what mutual funds should I choose? I think I am a mid level risk taker. My age is 23 and I want to build wealth. I want to have 5 crore rupees when I am 60 yrs old.

Can you please help me sir and guide me while choosing right mutual funds?

Best regards,

Vivan Jha

Dear Vivan,

Congratulations!

You may kindly go through below articles and revert to me with more queries (if any) :

* Investment Planning – How to create a solid investment plan?

* Retirement Planning in 3 Easy steps

* Best Mutual Funds 2018-19 | Top Equity Funds post SEBI’s Reclassification

I read your blog and it is always helpful. Your tips on investing are excellent.

I am investing in these 40,000 schemes from 2015. I am 27 yrs. old I want to accumulate wealth when I am 50 and goal is around 2 crore.

I have done a lot of research before investing it. All are direct plans. I just want to evaluate my portfolio and need you help to understand your views.

Kotak Emerging Equity Scheme – Mid Cap – 5,000

Reliance small cap – Small Cap – 5,000

Parag parikh long term equity – multi cap – 5,000

SBI bluechip – large cap – 15,000

Aditya birla sunlife front line equit – large cap – 10,000

Dear Hitesh,

The mentioned list of schemes are decent ones.

However, you may avoid investing in two large-cap funds. Both of them are large cap oriented ones and hence their portfolios may overlap (on the higher side). You may retain any one of them and divert the future SIPs to other funds in your portfolio.

Kindly read :

* Mutual Fund Portfolio Overlap Comparison Tools

* Best Mutual Funds 2018-19 | Top Equity Funds post SEBI’s Reclassification

Hi Sreekanth,

I am investing Axis Long Term Equity Fund and Reliance tax saver (ELSS) fund for last 2 years. I could see the return of reliance fund was very low. Shall i shift to another fund or hold it for sometime, kindly suggest.

Dear Dev,

I believe that Reliance Tax Saver has relatively higher Standard deviation and the returns can be very volatile.

You discontinue your investments in Reliance fund and switch to any other ELSS fund (like Franklin Taxshield) or make additional investments in Axis LTE fund itself.

dear sir,

many thanks for your valuable analysis.

Some experts are of the opinion that ELSS funds are the best among the MFs, as its growth rate is very high.

is it always true? Looking for your early reply.

Dear Kaushiki,

It is not always true.

It is very subjective.

Hi Sreekanth,

I have invested lumpsum in Franklin India Taxshield for last 2 years. Can I stay invested in the same fund for this year ELSS too? or can I invest in some other ELSS funds like DSP BlackRock Tax Saver Fund or L&T Tax Advantage Fund – Direct Plan?

Dear Muhsin,

Franklin Taxshield fund is a conservative fund and can give you stable returns, but may not be as aggressive as some of its other peers (like Birla Tax relief ’96 fund or DSP Tax saver fund etc.,).

Got it, i will go ahead with Franklin tax shield itself.Thank you for the reply Sreekanth.

Sir, have Reliance Value Fund the old name was reliance regular savings (growth equity fund).

I am holding this from last 9 years with 2000 rupees every month. My goal was to create a wealth in 10 years for my kids education. But this fund has not given much return. Can you please help me sir. What should I do, I have 15% profit on this. SHould I stay or move to a new fund? Thank you very much.

Dear sudarshan,

15% is a decent return on an MF investment.

Suggest you to hold on to this fund for next 6 to 12 months, keep a track of its performance and then can take a decision. (I am assuming you have a time-frame of 10 years from now.)

EXISTING – INVESTMENT OBJECTIVE : The primary investment objective of this Option is to seek capital appreciation and/or to generate consistent returns by actively investing in equity/ equity related securities.

PROPOSED – INVESTMENT OBJECTIVE : The primary investment objective of this scheme is to seek capital appreciation and/or to generate consistent returns by actively investing in equity/ equity related securities predominantly into value stocks. However there can be no assurance that the investment objective of the Scheme will be realized.

Related article : Why your Best Mutual Fund Schemes may not remain as ‘the best’? | Categorization & Rationalization of MFs

Thank you Mr. Sreekanth Sir. You are a very good person that you replied back. do you do private consultation on finance and tax? what are your charges sir? thank you very much sir.

Dear sudarshan,

I used to offer one-to-one personal financial planning service, but not now!

I provide suggestions through my blog only.

Respected.sir iam going to retire in 6 years.plz suggest some mutual funds.i want to invest by sip mode of 15000 monthly.

Dear Ramana ji,

May I know your investment objective(s) and time-frame for these investments in MFs??

Hi Sreekanth,

First of all I would like to thank you for valuable information on MF.I am regular investor in Mirae Asset Emerging Bluchip fund for last 2 years and now I am planning to start SIP in ELSS.After going through many reviews, I have come up with 2 funds Aditya Birla Sun Life Tax Relief 96 and Tata India Tax Savings. I need your suggestion to pick one among these 2 funds with a reason for not selecting the other one.Thanks in advance.

Dear Pravin,

Both are decent funds. However, on risk ratio parameters (as of now), Birla tax relief is a better fund.

In case, your investment time-frame is long and looking for a slightly aggressive ELSS fund then Birla fund can be considered, as it has higher allocation to mid-cap stocks.

Kindly go through the changes of fundamental attributes if any for the said funds..

Read : Why your Best Mutual Fund Schemes may not remain as ‘the best’? | Categorization & Rationalization of MFs

Dear Sreekanth,Gud day to U. I’m retiring with terminal benefits of Rs.40,00,000 by nxt month. Plz suggest the best deposit. Further to save under 80C, which is the best ELSS for investment of Rs.1.5 lk for FY 2018-19. Thx..

Dear Kesav ji,

Kindly go through this article @ Lump sum Investment options for Retirees/Senior Citizens | Where to invest my Retiral benefits to get Regular Income?

For best ELSS funds, kindly refer to the above list in the article.

Dear Mr. Reddy,

Abv article is too gud in return wise as well ratio wise bifurcation. I have short listed 2 funds under elss. 1. Aditya birla tax saver96 & 2. Axis long term fund. As i am very much confused that return wise axis long term is good compare to all elss fund as well Aditya birla tax saver96. Where if i compare ratio wise comparison then Aditya birla tax saver96 is gud. My purpose is tax saving as well as long term investment in 1 fund like 10-15years. So i very much optimistic return wise & selection of fund wise. So kindly help me out in abv confusion.

Thanks for your article as well as reply of other persons query.

Dear Hesh Soni.. If you have to pick one fund out of these two then you may go ahead with Birla Fund.

Thx for reply but can u guide why i should select Aditya birla tax saver 96 & not axis long term fund?

I am very much curious about my research as well valid reason to avoid any one.

Dear Hesh,

Long proven track record.

You have a very long term view, so may be worth investing in an aggressive fund (comparatively).

Personally, I have invested in Axis LTE and my spouse invests in Birla Tax relife 96 fund.

Ok Thx. Got your point.

Dear Sree Thx a lot..with regds..kesav

Hi Sreekanth

I had invested in L&T Tax advantage a few years back. Though i have not withdrawn the money despite its locking period is over ( and its growing as well). My question is, shall i pull the money considering the future merging of various mutual funds? Is it going to have any major impact on current NAV?

Thanks in advance!

Regards

Amit Gandhi

Dear Amit,

The re-categorization of schemes is definitely a big change.

If you do not need monies now, suggest you to stay invested and keep a track of the changes and its performance for next few years.

Hi Sreekanth,

The AMCs were supposed to take some action on MFs schemes as per new guidelines of SEBI. Do you have any information on it?

Regards,

Nicolas

Dear Nicolas,

Yes, most of the Fund houses have started implementing the re-categorization norms suggested by the SEBI.

For example :

UTI AMC has done below ‘Merger of Schemes’ ;

▷ Merger of UTI Bluechip Flexicap Fund into UTI Equity Fund

▷ Merger of UTI Multi Cap Fund into UTI Opportunities Fund

▷ Merger of UTI Monthly Income Scheme, UTI Smart Woman Savings Plan & UTI Charitable & Religious Trusts & Registered Societies (UTI – C.R.T.S.) into UTI MIS Advantage Plan

However, as of now, I do not have the consolidated info!

Thanks Sreekanth,

Earlier i understood that AMCs need to comply these guidelines by April 1st, 2018. Seems like that was not the case. Anyways is there any date specified from when these changes will be effective.

Dear Nicolas,

I believe that the first deadline was 31 Dec 2017, then 31 Mar 2018 has been proposed and now, I am not very sure on the new deadline.

But, looking at the way fund houses have been implementing the changes, SEBI may soon notify the final deadline date, for all the AMCs to comply with..

Dear Nicolas,

Looks like the new deadline is 2nd May, 2018.

Thanks Sreekanth.

Anyways, Do you have any idea for HDFC AMC?

Dear Nicolas,

HDFC MF website has updated details regarding their Debt schemes (as of now).

Suggest you to keep a track of the updated at this link..

Thanks Sreekanth.

Looks like HDFC has also announced the changes. But i could not find the details for HDFC Balanced fund & HDFC Prudence fund.

Dear Nicolas ..Yes, the above mentioned link has few details regarding some HDFC schemes only, let’s wait for few more days to know about balanced funds.

Hello Sreekant,

To fill my 80C bucket, I wish to start investing in ELSS via SIP – the plan is to stay invested for 5 years.

Can you please confirm if I can claim tax benefits for all the 5 years? Or can I do that only during the lock 3 year in period?

Also can you please advise where I should put my 8000 p.m?

Thanks in advance.

Dear DK,

If you invest say up to Rs 1.5 lakh in ELSS funds per annum, then you can claim tax benefit every year.

If you invest say Rs 1.5 Lakh only in FY 2018-19 then you can claim tax benefit for FY 2018-19/AY 2019-20 only.

Kindly note that units allotted under each SIP have a lock-in period of 3 years..

Kindly refer to the above article for my suggestions..

As you mentioned Birla Sunlife Tax Plan to be merged into Birla Tax Relief ’96 Fund,

I was planning to start an SIP with Birla Tax Relief ’96 fund,is there anything i need to be concerned about because of this merging?

Does this mean it will be a new MF with a new name ? If so, as a new fund, it doesnt have a track record.

Can we expect change in allocation style, Fund size, etc.

Dear Vishnu,

The Assets under management of Birla Tax plan are lesser than of Birla Tax Relief Scheme, hence I am assuming that the former may be merged into the later one.

Change of name, allocation of investment strategy etc., – The AMC may confirm the same very soon.

The fund size of the merged scheme (if any) will surely change.

The same set of changes may happen with the schemes offered by other Fund houses as well. All we can do is to keep investing for now and wait for more clarity on the said changes..

Great article. The data provided helped me to analyze and finalize my investments.

keep doing the great work!!!

Hi Sreekanth ,

Your site is too good and too informative. Keep up the good work 🙂

I need your suggestion on the below :

My husband wants to start with the mutual funds now with monthly investment of 5000/- as of now .

I have the following MFs :

1. Axis LTE (Tax Saver)

2. HDFC Balanced Fund

3. SBI Blue Chip

Now , my husband is planning to start the MFs for 2 Years from today for the accumulation of downpayment of Home. And keeping in mind the Tax Saving .

We are planning to start off with the below :

1. DSP BR Tax Saver (1500)

Please suggest two more funds for 1000/ each a month.

Thanks in Advance 🙂

Dear Pooja,

Thank you for your appreciation!

Is your investment time-frame for the above three funds 2 years? Or Is it for investments to be made by your husband? Are you guys highly dependent on this corpus accumulation for making the required down-payment?

Kindly note that units allotted under each SIP of ELSS fund have a lock-in period of 3 years.

Hi there ,

For my huband investment we were planning it for 2-3 years .

We will be saving some ion our accounts , FDs , RDs and MFs as of today for the down payment .

But to begin with Please suggest few MFs .

Is it good practice to have different MFs for both of us ?

Thanks,

Pooja

Dear Pooja,

Investing in Equity funds with a time-frame of around 2 years can be a very risky affair!

Suggest you not to consider equity funds for the said time-frame.

Thanks for the suggestion . I would still invest in the same but on ur suggestion would increase the time-frame to 5 years .

For down Payment would look for other options (Please suggest few ).

Also for 5 Years do suggest me few MFs with good returns

Dear Pooja,

For 2 to 3 years, you may consider Short term debt funds like Franklin Duration Fund.

Kindly read : Types of Debt Funds

For a 5 year time-frame – you may consider a Large Cap/Diversified fund & an Equity oriented Balance Fund.

Ex :

HDFC Balanced / ICICI Balanced fund

Birla Equity / Franklin High Growth Cos Fund

SBI Bluechip / Birla Frontline Equity Fund

Investing in two different portfolios is fine, but advisable to maintain low overlap.

Kindly read :

MF Portfolio overlap analysis tools

How to pick right mutual fund schemes?

Best Balanced Funds

Mutual Fund Schemes Categorization and Rationalization – Types of MF Schemes | SEBI’s Latest Guidelines

Thanks a lot . Really appreciate

Thanks

Hi Sreekanth, AXIS long term eq fund money control rating is saying 2 star by crisil? Should we need to worry about?

Dear Shas,

The star ratings are given based on the recent or very short term performances of the Funds (last 1 to 2 years). So, you may ignore the ratings for now for this fund.

Kindly note no Fund will remain as Five Star rated fund forever…!

Hi Sreekanth,

Please provide your views on “Motilal Oswal Long Term Equity Fund – Direct Plan (G)” in comparison to your above suggested ELSS funds. I see it has given decent returns and has handled the recent dip comparatively better.

Dear Vineet,

There is no doubt that this fund has out-performed its peers for the last 1 – 3 year period.

But this is relatively a new fund, launched in 2015, I prefer to invest in a fund with a long-track record.

However, nothing wrong in investing in this fund, if one believes that this fund can continue its good performance in the future as well.