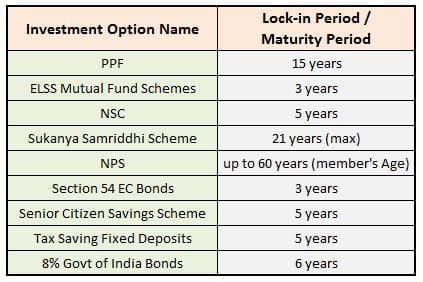

We are aware of the fact that certain Investment (or) Saving schemes have a lock-in period. ‘Lock-in period’ is a common phenomenon especially with popular Tax saving Schemes. These schemes are like PPF, ELSS mutual funds, NSC, 5 year Tax saving Fixed Deposit, Senior citizen Savings Scheme etc.,

What is a Lock-in period? – It is a period during which an investor is restricted from selling a particular investment. For example : An investment in ELSS Mutual fund has a lock-in period of 3 years. The units allotted under these schemes can not be redeemed before 3 years. Similarly, the lock-in period that is applicable on PPF accounts is 15 years…and so on..

Unfortunately, what if an investor of any of the above mentioned schemes / savings options expires (dies) before the lock-in period ends? Can the nominees/legal heirs redeem the money immediately during the lock-in period itself? Is it possible to redeem money if an investor dies before the lock-in period? Let’s discuss..

Latest Article : Lock in Period of various Saving & Investment Options

Can lock-in period apply on death of the Investor / Holder?

Let us now understand the rules & guidelines pertaining to ‘lock-in period’ and whether nominee/legal-heir(s) can withdraw the investments before the lock-in period ends?

Public Provident Fund

- The lock-in period on PPF account is 15 years.

- Premature withdrawal is allowed in case of unfortunate demise of the PF subscriber.

- The legal heirs or nominee can withdraw the entire balance available in PPF account, but have to produce certain documents to make a death claim. So, the nominee(s) can withdraw PPF deposits during the lock-in period.

- The HUF account will not be closed before maturity on the death of the Karta but it will continue by the new Karta appointed by the HUF.

- If the subscriber dies during a year, his executors cannot deposit any sum from the income of the deceased to his PPF account after his death. If they do so, the amount deposited shall neither carry interest nor shall this amount be eligible for tax rebate. This amount will be refunded without interest to the nominee/legal heir, as the case may be, at the time of closure of the account.

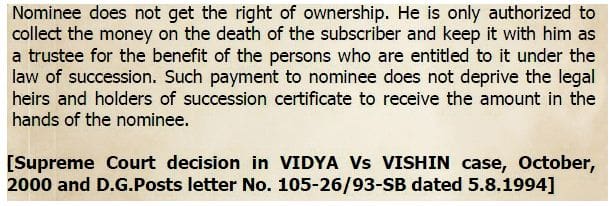

- Kindly do note that the Nominee does not get the right of ownership. He/she is only authorized to collect the money on the death of the subscriber and keep it with him as a trustee for the benefit of the persons who are entitled to it under the law of succession.

National Savings Certificate (NSC)

NSCs have a lock-in period of 5 years. However, premature encashment is permitted under Sec. 16(1) only on the following three contingencies:

- On the death of the holder or any of the holders in the case of joint holders

- On forfeiture by a pledgee being a Gazetted Government Officer when the pledge is in conformity with these rules (or)

- When ordered by a court of law.

In case of the holder’s death, the nominee can encash the NSC before or after the maturity (i.e. 5 years). The amount payable is at a proportionate rate.

5 year Tax Saving Fixed Deposit

Tax saving FDs have a lock-in period of 5 years. However, in case of death of the depositor before the maturity of term deposit, levy of penalty would be exempted and nominee/legal heir will be allowed premature payment even before the lock-in-period.

54EC Tax Saving Bonds

54EC Bonds have a lock-in period of 3 years. To avail the benefit under Section 54EC of the Income Tax Act, 1961, the investment made in the Bonds needs to be held for a period of at least three years from the Deemed Date of Allotment. The Bonds are for tenure of 5 years (wef 2018) and are ‘Non-transferable & Non-negotiable’ and cannot be offered as a security for any loan or advance.

However, Transmission of the Bonds to the legal heirs in case of death of the Bondholder/Beneficiary to the Bonds is allowed. But, they have to be held for the entire 5 years term, interest income is taxable in the hands of nominees/legal heirs. (Related Article : ‘How to save Capital Gains Tax on sale of Property?‘)

ELSS Tax saving Mutual Fund Schemes

ELSS mutual funds have a lock-in period of 3 years. In the event of death of the investor, the nominee or the legal heir can withdraw the amount ,only 1 year after the date of allotment of units to the deceased (original investor / unit-holder).

For example : If the investor dies eight months after purchasing the units, the nominee has to wait for at least four more months to be able to sell the units (if he/she wants to redeem..). (Read : ‘Best ELSS Mutual Fund Tax Saving Schemes for FY 2020‘)

Kindly note that nominee can get the units transferred to him/her much earlier but can’t sell those until 1 year is over. Essentially, the lock-in period goes down from 3 years to 1 year in the event of demise of the original investor. This information can be found in any of the ELSS funds ‘scheme information documents’.

Senior Citizen Savings Scheme

Sr.CSS has a maturity period of 5 years. However, in the unfortunate event of death of the deposit holder, the account can be closed immediately (if no joint ac holder exists) and the nominee can receive the deposit amount as per the rules. Same is the case with Post office Monthly Income Scheme.

Sukanya Samriddhi Account

The maturity period under this scheme is 21 years from the date of account opening. The account can be prematurely closed, in case of the unfortunate death of the girl child (account holder), the parent or legal guardian can claim for the accumulated amount along with the interest accrued on the account. The balance would be immediately handed over to the nominee of the account. (Read : ‘Sukanya Samriddhi Deposit Scheme – Review‘)

National Pension System (NPS)

The exit age under NPS is 60 years (subscriber’s age). However, in the event of death of the contributor, the entire accumulated pension wealth would be paid to the nominee/legal heir of the subscriber and there would not be any purchase of annuity/monthly pension.

8% GOI bonds

These bonds have a maturity period of 6 years. On the demise of the bond holder, they can be transferred to nominee’s name but payable after maturity period only.

Company Fixed Deposits & NCDs

The maturity period (lock-in period) may vary for different Deposit Schemes/Issues. It may be noted that deposit amount will be payable only on the date of maturity and not earlier on the date of death of the investor. However, the surviving person or the legal heir can request the company for a premature payment of the deposit and this is the prerogative of the company to accept or decline such request. It depends on the specific Issue/Scheme’s terms & conditions.

Death is a certainty. Nobody can escape from it. Advisable to share all your investments details with your family members/well-wishers. Also, kindly make sure you provide nomination details on all your investments (or) the best possible thing that you can do is ‘write a WILL‘.

Continue reading related Articles :

- Nominee Vs Legal heir : Who will inherit your Assets?

- Tax Treatment of various Financial investments?

- Tax Saving Options u/s 80C : In whose name you can invest?

(Image courtesy of Vichaya Kiatying-Angsulee at FreeDigitalPhotos.net) (Post published on : 01-Aug-2017)

Join our channels

This is a very informative blog for me. I very much benefited from reading this blog. Keep sharing.

Hi Sir,

What will happen, In case of demise of person investing in equity MF?

Will exit load applicable where one year of unit holding is not yet complete?

Or need to wait for exit load time completion before redeem?

What and how taxation apply on this case?

Regards,

Anuj

Dear Anuj,

Taxation of Capital gains on Transmission of Mutual fund units :

In case of death of the investor who purchased the mutual fund investment, all the units are transferred to the nominee or the heir at the prevailing rate (NAV) on that day.

On transfer of mutual fund units, the nominee or surviving joint holder don’t have to pay any tax. Capital gains tax is applicable only at the time of redemption of units.

The tax liability will be based on the period of holding, whether short term or long term. The period thus calculated will also include the time period for which the original or previous owner held the units.

Related article : Mutual Fund Units Transmission procedure | How to get Mutual Fund units transferred upon death of a Unitholder?

1.sir,Please let me know if sr citixen husband dies suddenly after opening the scheme jointly with wife aged 60 above now ; she can continue the sr c ss as before till completion of the scheme 5 years .

2 if wife is not at the age 60 after death of subscri;ber . the scheme can continue . please reply with thanks .

3 3rd question HUSBAND CAN OPEN ALONE 15L IN SR CITIZEN SCHEME . IF SO THEN WIFE ALSO CAN OPEN 15 L IN THIS SCHEME ALONE AT ABOBE 60 YEARS. Your reply is solicited .thanks.

Dear NITAI,

1 – Yes can continue with the Sr.c.s.s deposit.

2 – I believe that she can continue. In case of the death of the primary account holder, the spouse can continue the account subject to the condition that his or her total investment in SCSS should not exceed Rs. 15 Lakhs.

3 – Yes, your understanding is correct.

Dear Mr. Sreekanth,

The first holder is a Sr. Citizen and he has deposits in SCSS, Govt. Of India 8% Taxable bonds and Post Office 5 yr. TD. jointly with his wife (not Sr Citizen). Suppose if the first holder expired before the maturity period can she continue the deposit till maturity period and continue to get interest if she desires or it should be closed. Can you pls clarify. Thanks

Dear KRISHNAN,

I believe that the second applicant can continue with the investments..

Sir you have mentioned 5 no’s sector specific funds which have given >50% return per annum on one hand and 10no’s mutual funds which has given >40% retur on other hand. Are these funds safe to invest or is any chance the money is forfeited either due to collapse of fund or due to integrity of the fund manager. Secondly please also advice the difference in investing in a mutual fund with option “DIVIDEND” and “DIRECT DIVIDEND”

Dear Devinder,

Kindly note that Mutual Fund industry in India is a very well regulated one, you may kindly invest in them with no worries!

Kindly read :

What are Direct MF plans?

Direct plans Vs Regular plans

Sir, I want ask one question regarding Atal pension yojana(APY)

1.Before 50 died how do claim a/c close or pension ?

Dear Feroz,

The person’s spouse can continue the contributions (or) can with draw the accumulated corpus amount by closing the account.

Hi Sir,

If a Sr. citizen has invested in SCSS scheme and has a joint account holder. In such case, if the person expires, who gets right of ownership for the money legally – legal heir or the joint account holder? Pl. clarify as per law.

Thanks.

Dear surya,

In the event of a death of first account holder, then second account holder can continue as primary account holder but with the condition that the maximum overall limit of the second holder must not cross Rs.15 lakh.

Sir, I want ask one question regarding NSC interest,

If I purchase NSc in the mth of July,2017 ,first year int shown in itr on 31.3.18, or 31.3.19

Dear Minal ..Kindly refer to our conversation on FB.