Capital asset typically refers to anything that you own for personal or investment purposes. It includes all kinds of property; movable or immovable, tangible or intangible, fixed or circulating.

Capital assets are further classified as Financial Assets and Non-Financial Assets. Financial assets are intangible and represent the monetary value of a physical item.

Stocks (Shares) and mutual funds are the best examples of Financial Assets.

The profit (if any) that you make on your mutual fund investments when you redeem or sell the MF units is referred to as Capital Gains. It can be a Short Term Capital Gain (STCG) or a Long Term Capital Gain (LTCG) depending upon the ‘Period of Holding’. The tax that is applicable on these profits is known as ‘Capital Gains Tax’.

In this post let us understand: What are the factors that determine the tax status of mutual funds? What are the tax implications on mutual fund investments? What are the Budget 2018-19 proposals related to Mutual Funds Taxation? – Mutual funds taxation & capital gains tax rates on mutual funds for Financial year 2018-2019 (Assessment year 2019-2020).

Factors determining the tax status of mutual funds

The capital gains tax on mutual fund withdrawals is based on the factors as below;

- Residential Status

- Fund Type (whether the fund is an Equity-oriented fund (or) a Non-Equity Oriented Fund)

- Holding Period (Duration of your investment)

1. Residential Status & Mutual Funds Taxation

The capital gains tax rates are determined based on the residential status of an individual / investor. Residential status can be either ‘Resident Indian’ or ‘Non-Resident India” (NRI). (Related article : ‘Residential Status online calculator.’)

2. Type of Funds & Mutual Funds Taxation

What are Equity-oriented Mutual Funds? – MF schemes that invest at least 65% of its fund corpus into equity and equity related instruments are known as equity mutual funds. Examples are : Large cap, ELSS tax saving funds, Mid-cap, Balanced funds (equity oriented), Sector funds etc.,

What are Non-Equity Mutual Funds? – MF schemes that hold less than 65% of their portfolio in equities and equity related instruments are known as Non-Equity Funds / Debt funds. Examples are : Liquid Mutual funds, Money Market funds, Gold funds, Infrastructure debt funds, MIPs, FMPs, Hybrid funds (Debt oriented) etc.,

3. Period of Holding & Capital Gains on Mutual Funds

Capital gains on Mutual funds could be either long term capital gains or short term capital gains, depending on your investment horizon.

- Long Term Capital Gains

- If you make a gain / profit on your investment in a Equity Mutual Fund scheme that you have held for over 1 year, it will be classified as Long Term Capital Gain.

- If you make a gain / profit on your investment in a Non-Equity Mutual Fund scheme (or in a Debt Fund) that you have held for over 3 years, it will be classified as Long Term Capital Gain.

- Short Term Capital Gains

- If your holding in a Equity mutual fund scheme is less than 1 year i.e. if you withdraw your mutual fund units before 1 year, after making a profit, then the profit will be considered as Short Term Capital Gain.

- If you make a gain / profit on your Debt fund (or other than equity oriented schemes) that you have held for less than 36 months (3 years), it will be treated as Short Term Capital Gain.

Budget 2018-19 & Mutual Fund Taxation

- The Budget 2018-19 has proposed to introduce tax on Long Term Capital Gains on sale of stocks and equity mutual fund units from FY 2018-19 (or) AY 2019-20 onwards.

- LTCG tax at 10% on gains of above Rs 1 lakh from Equities & Equity mutual funds.

- No change has been proposed to STT tax rate structure.

- No change has been proposed to holding period to arrive at LTCG/STCG.

- STCG will continue to be taxed at 15%.

- Equity Oriented Mutual Funds will now have to pay a dividend distribution tax (DDT) of 10%. (Read : ‘10% LTCG Tax on sale of Stocks/Equity Mutual Funds | How are Capital Gains calculated on Investments made before 01-Feb-2018?’)

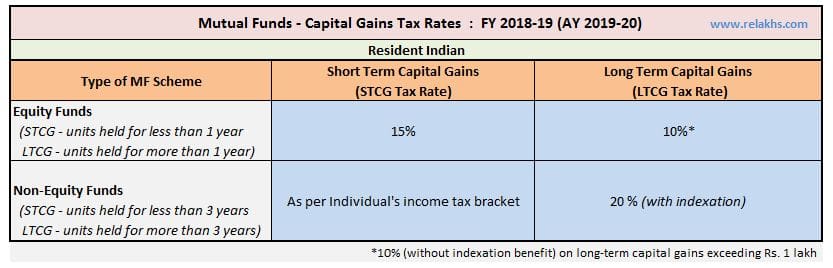

Mutual Funds Capital Gains Taxation Rules FY 2018-19 | Latest Mutual Funds Capital Gains Tax Rates AY 2019-20

Capital Gains Tax Rates on Mutual Fund Investments of a Resident Indian are as below;

- The STCG (Short Term Capital Gains) tax rate on equity funds is 15%.

- The STCG tax rate on Non-Equity funds (or) Debt funds is as per the investor’s income tax slab rate.

- The LTCG (Long Term Capital Gains) tax rate on equity funds is 10% on LTCG exceeding Rs 1 Lakh.

- The LTCG tax rate on non-equity funds is 20% (with Indexation benefit)

Capital Gains Tax Rates on NRI Mutual Fund Investments for the Financial Year 2018-19 (Assessment Year 2019-20) are as below;

- The STCG tax rate on equity funds is 15%.

- In case the short-term capital gains were on account of listed equity shares which were sold on a stock exchange or equity-oriented mutual fund, then the provisions for tax calculations as per section 111A of the Income Tax Act provide that 15% tax is payable by non-residents on a flat basis without getting any benefit of the initial exemption limit of Rs 2,50,000. Unfortunately, the basic exemption limit is available only for resident individuals and HUFs, and not for any other entities. If the short-term capital gains is not on account of either of the two types of sale mentioned above, then the benefit of initial exemption will be available even to non residents.

- The STCG tax rate on Non-Equity funds (or) Debt funds is as per the investor’s income tax slab rate. (Tax Deducted at Source – TDS @ 30% is applicable)

- The LTCG tax rate on equity funds is 10%, on LTCG exceeding Rs 1 Lakh.

- The LTCG tax rate on non-equity funds is 20% (with Indexation) on listed mutual fund units and 10% on unlisted funds.

Base Year & Indexation : As per Budget (2017-18), the base year for calculation of Indexation has been changed to 2001. It has an affect (mostly positive) on investments where indexation benefit is available when calculating Capital gain taxes.

- For example: Suppose you are holding on to your investments made in debt funds (or) Property before 2001, the Fair Market Value (NAV) as on 1 st April, 2001 will be considered as cost of acquisition for calculating capital gains. This will help the investor to reduce the capital gains taxes.

- As of now, the base year is 1981. To calculate the capital gains at the time of selling any Deb fund units / property purchased before 1981, its purchase price is now calculated on the basis of the fair market value of 1981. Calculation at the fair market value of 2001 will increase the cost of acquisition and lower the capital gain.

(How do you calculate the indexed cost of purchase? The indexed cost is calculated with the help of above table of cost inflation index.

Divide the cost at which you purchased the Mutual Fund units by the index as on the date of the purchase. Multiply this by the index as on the date of sale.

For Example : If purchase year is 2011 and year of sale is in Financial Year 2015. Then indexed cost of purchase would be –

Indexed cost of purchase = (Purchase price / 184) * 254.)

Taxation of Mutual Fund Dividends

- Dividends on Equity Mutual Funds : The dividend received in the hands of an unit holder for an equity mutual fund is completely tax free. However, w.e.f. FY 2018-19, the fund houses have to pay 10% Dividend Distribution Tax (DDT) on equity oriented mutual fund schemes. (Effective DDT rate is 11.648% inclusive of 12% surcharge & 4% cess.)

- Dividends on Debt Funds : The dividend income received by a debt fund unit holder is also tax free. But, the mutual fund company has to pay a dividend distribution tax (DDT) before distributing this dividend income to its Unit-holders. DDT on Debt Mutual Funds is 29.12% (inclusive of surcharge & cess).

NRI Mutual Fund Investments & TDS Rate

Below are the TDS rate applicable on MF redemptions by NRIs for AY 2019-20.

Hope this post is informative. Do you check your capital gains statement(s) every year? Do you include your capital gains taxes (if any) in Income Tax Returns (ITR). Share your comments.

Continue reading :

- 10% LTCG Tax on sale of Stocks/Equity Mutual Funds | Budget 2018-19 Proposal

- LTCG Tax on Equity Mutual Funds & Important Implications

- Mutual Funds Vs ULIPs – Which is the best Investment option? | Post Budget (2018) LTCG Tax proposal on Equity Mutual Funds & Shares

- Mutual Fund Taxation rules FY 2017-18

- Income Tax Slab Rates for FY 2018-19 / AY 2019-20 (Budget 2018-19)

- Income Tax Deductions List FY 2018-19 | List of important Income Tax Exemptions for AY 2019-20

- Best Mutual Fund Schemes 2018-19

(Assumption – STT (Securities Transaction Tax) is payable) (Featured Image courtesy of Stuart Miles at FreeDigitalPhotos.net) (Post published on 01-March-2018)

Join our channels

Dear Sreekanth,

What is listed and unlisted funds? all open ended debt funds are unlisted funds?

Dear Madhavan,

Closed Ended funds are generally the LISTED ONES. (Investors can invest in the scheme at the time of the initial public issue and thereafter they can buy or sell the units of the scheme on the stock exchanges where the units are listed.)

Non-Equity funds like FMPs (Fixed Maturity Plans Funds) can be listed on Stock exchanges after the initial NFO.

One can find information whether a fund is listed on stock exchanges or not by going through the scheme information documents (you can find them on fund house/AMC websites).

Thanks Sreekanth

Dear Sreekanth

Thanks a lot for sharing valuable comments on above queries.

Could you please suggest something about Aditya Birla Sun Life Insurance Wealth Aspire Plan.

It has got 5 years locking period and claims to give 25% return.

Could you please provide your opinion on this plan for long term investment. Is it a good plan for good gain

Dear Sunil,

Aditya Birla Sun Life Insurance Wealth Aspire is an Unit Linked Insurance plan.

If your investment objective is purely wealth accumulation and not insurance requirement, you may avoid investing in it. Can consider for Mutual fund schemes..

Kindly read : Mutual Funds Vs ULIPs – Which is better? | Post Budget (2018) LTCG Tax proposal on Equity Mutual Funds & Shares

Dear Sreekanth,

How will be the tax calculation done for Debt Funds (FMPs) with maturity period less than 3 years? (For example SBI Debt Fund Series C-31 – 365 Days).

Whether its considered as LTCG or STCG ?

Thanks & Regards

Raj

Dear Raj,

FMPs are Debt Funds, if the holding period is less than 3 years then gains realized (if any) are treated as STCG.

Very informative article and nicely explained. Please attach a tag to save article to own E.Mail ID so that we can refer as and when needed.

Dear Avinash,

You can use ‘Print’ option from the left side Floating Social Media Icons, can attach the print friendly version to your Email Id , or print it or Can save the article in PDF version as well.

Thank you Sreekanth for your quick reply.

Whether Mutual Fund – AMC will provide LTCG & STCG Statements every year for the investor to pay the taxes. Since its very difficult for a us to calculate the taxes on various MF’s

Dear Raj,

Most of the AMCs do provide. You can also download CG statements from respective RTAs (like CAMS/Karvy) portals. If you are investing through intermediaries like ICICI Direct or Fundsindia etc, they too provide you the required statements.

Kindly read : How to get Mutual Fund Consolidated Account Statement / Capital Gains Statement Online?

Thanks Sreekanth for the Clarification.

Another Query on LTCG/STCG.

For example if Buy a ABC & XYZ Equity Product. In a short if am gaining 10,000 in ABC and losing 10,000 in XYZ. If I sell both within one year. Whether the STCG on ABC of 10000 with adjusted against the losses?

Same way in a Long term I am gaining 2 Lakhs in ABC and losing 1 Lakh in XYZ. If I sell both after 1 year, Whether the LTCG on ABC of 1 Lakh with adjusted against the losses and become nil tax?

Thanks & Regards

Raj

Dear Raj,

Yes, adjusted, your STCG for that FY would be nil.

Yes, net off of LTCG, if it is more than Rs 1 Lakh then only tax liability comes into picture.

Related articles :

* Budget 2018 LTCG Tax on Equity Mutual Funds & Important Implications

* 10% LTCG Tax on sale of Stocks/Equity Mutual Funds | Budget 2018-19 Proposal

Thanks for your clarification.

One more query in this line. If I reinvest the entire Long term capital gains into the market in the same financial year. Will the capital gains attract tax?

Say my capital gains is 2 Lakh. If i reinvest the whole Capital gain (2 Lakh) again. Whether 1 Lakh is taxable ?

Dear Raj,

If your LTCG in a FY is Rs 2 lakh, the gains >Rs 1 Lakh are taxable. If you reinvest this amount there is no tax exemption available (on reinvestment, as available in Immovable property case..)

Hi Sreekanth,

My query is related to LTCG tax on sale of Equity Mutual Funds. In the last budget there was provision relating to grandparenting of profits till Jan 31st 2018.

So if one has purchased some equity mutual funds in 2010 and sold those on 25th July 2018. Then the profit upto Jan 31, 2018 will not be taxable. And profit from

1st Feb 2018 till 25th July 2018 (sale date) will only be taxable as LTCG (if it exceeds Rs. 1 lakh).

Is that correct ?

Dear Sujata,

Yes, your understanding is correct!

Kindly read :

* Budget 2018 LTCG Tax on Equity Mutual Funds & Important Implications

* 10% LTCG Tax on sale of Stocks/Equity Mutual Funds | Budget 2018-19 Proposal

I am nri and plans to change mutual fund scheme from regular to direct plan.I HD invested 10 lakh and now it’s value is 25 lakh. Since plan change will imply redemption how much long term tax I will have to pay on this switch of mutual fund scheme.I don’t have any other income in india.

Dear Sanjeev,

The LTCG tax rate on equity funds is 10%, on LTCG exceeding Rs 1 Lakh.

The LTCG tax rate on non-equity funds is 20% (with Indexation) on listed mutual fund units and 10% on unlisted funds.

I believe that small lumpsum payments are much beneficial than the SIP. Here is my reasons:

1. Flexibility of time: Flexibility to invest when the markets are down. However, this is possible only when you are watching markets on daily basis – just 15 mins are required. For example, 23 Mar was the best time to invest. 19 Jan was the best time to take profits. I know when looked in past it seemed right days, but how to predict the future, this is when you start developing ideas when you are checking the markets on the daily basis. SIPs remove these abilities to innovate yourself.

2. Flexibility of Amount : When we decide SIP, I have hardly seen people making changes to the SIP when they know that the markets are down and reducing the SIP when the markets are up. One of the reasons is that it is cumbersome to change the SIPs. Lumpsum investment remove all these strings. Yes, there are minimum investment – I think starting 5K. However, you can choose one or 2 funds to invest at one month rather than all 5 – 6 that you have. You need to target covering all funds in a quarter. The beauty is that, when the markets are down, you have the ability to invest more. All you need is a target for a month or a quarter. SIP remove these opportunities. During the time of Jan, there was huge speculation that the LTCG will be introduced, people that are not in SIP had taken out the parital profits for the equity funds that are more than 1 year (especially those DSP BR micro cap, Mirae Emerging) which have done excellent in 2017. And they reserved these monies for Feb / Mar investment. They are already in black now than those who have done SIP and are in red in last quarter.

3. Flexibility to Shift: Most often when people do SIP, they do now research enough (or do it once or twice a year). It is very difficult to get a pulse of the markets when you are doing it only once or twice. This means that when a person decides on the SIP, it is not likely that they realize whether the fund is doing good or bad. I know a fund should be observed over the years, but the past history does cast some lights on how the future behaviour may be. If you are looking for trends, you will soon know what is the investment strategy of the fund manager this year. Some fund managers take their own decisions, some base their decision majorly on the research done by the young guns (the word fintech was coined by these). So based on this, if you think the trend indicates the past behaviour which is not to your liking, then you can look at the other funds. What I am indicating is that this option give us flexibility to observe other funds and do a back testing to see if they have a better strategy. So you are just start investing into new funds and not bother about stopping any SIPs in the previous ones.

Dear Rakesh,

I do endorse your views and thanks for sharing them!

However, I strongly believe that there is no right or wrong approach to investing.

Some may have time and interest to track the markets on a daily basis and some may not have time or do not like doing it.

Personally, I follow SIP + manual lump sum investing approaches.

Related article : Is creating wealth through Systematic Investment Plan (SIP) a hoax?

Hi Sreekanth,

Thanks for your advise, I’ll go with Large cap: Birla Frontline & Mid / Small Cap : L&T Emerging bluechip…

I have discontinued my Birla vision life income policy and with 1 Lakh loss. Total I paid 1.57 lakh and I’ll surrender amount only 57K. could you pls advise where I can invent this 57K, I don’t have any immediate need so this 57K, I can leave for 5+ years.

Dear Chandresh,

You may invest it in an equity oriented balanced fund like HDFC Balanced fund.

Hi Sreekanth,

I invested lumsum amount 40k in Birla front line. Y’day i got email from Birla that there is some changes in front line mutual fund as per SEBI. i gone thru complete email but could not understand what change is made. Only thing i noticed is Benchmark is chaged from S&P BSE 200 to Nifty 50. I dnt know what this means.

Do you have any advice on this..shall i continue or switch fund?

Dear chandresh,

There are no major changes proposed for this fund.

Earlier, the fund can invest in top 200 companies by market capitalization, now it may have to invest primarily in top 50 funds (bluechips).

In case, your investment objective is to invest in frontline/large-cap stocks, you may continue with this fund.

Related article @ Why your Best Mutual Fund Schemes may not remain as ‘the best’? | Categorization & Rationalization of MFs

Hi Sreekanth,

I’m planning to invest in below 3 MFs to 10 years either for daughter’s higher education or my retirement

Large Cap – IDFC Focused Equity – Direct (G) – 4K/Month

Small & Mid Cap – Reliance Small Cap Fund (G) – 3K/month

Small & Mid Cap – L&T Emerging Businesses Fund-RP (G) – 3k/month

Please advise, can I go for these MFs or you’d suggest different plan. I checked these funds on money control and they are ranked 1 funds by CRISiL.

Dear Chandresh,

The start ratings or rankings are generally given based on short term / recent performances only. Kindly do not give too much importance to them.

We need to analyze the funds’ long term performances and how consistent are they during different market cycles.

My suggestions would be ;

Large cap : SBI Bluechip / ICICI Focused bluechip / Birla Frontline

Small & Midcap : Franklin Smallers cos fund / L&T Emerging bluechip..

Kindly read :

How to select best mutual fund schemes?

Mutual Fund portfolio overlap analysis tools