Retirement is one of the most important stages of your life for which you work and should save for. With the break-up of the joint family system in India, increase in longevity (life expectancy) due to advanced medical innovations, shorter work-span and lower job security; ‘Retirement Planning’ assumes greater importance.

If you are creating an Investment Plan, your top most priority should be to save and invest for your retirement. Do not think that it’s too early to start planning for retirement. It is very important that you start early for your retirement.

In this post, let us understand – How to calculate the retirement corpus? How to do Retirement Planning? How much do you need to save for your retirement goal? How to calculate the required retirement fund in 3 simple steps using MS Excel?

First, let’s understand the stages of Retirement planning.

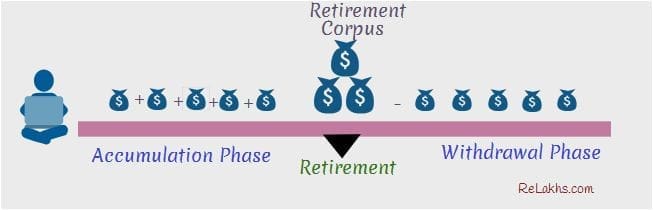

Stages / Phases of Retirement planning

- Accumulation phase – During this phase, you save and invest for your retirement. This is the stage where you invest to generate a decent corpus which is assumed to take care of you / your family during retirement. The earlier the accumulation period is in your life, the more advantages you will have (like the power of compounding).

- Transition to Retirement – This is an individual’s transition from work into retirement.

- Withdrawal phase / Wealth Consumption– In this phase, the retiree withdraws the income from the accumulated fund (Retirement fund / corpus) and enjoys the retired life.

Retirement Planning in 3 Simple Steps

Let’s now calculate the retirement corpus and the required amount of savings to achieve your retirement goal. You can do this in 3 simple steps as below. I have also provided a “Basic Retirement Planning Calculator.” Do try that.

Example : Mr Rahul G (35 years) wants to plan for his retirement. His current annual living expenses are around Rs 3.6 Lakh. He wants to retire at 60 years and expects his life expectancy to be 80 years. He would like to know the projected / required retirement corpus and what is the required savings to meet his retirement goal amount??

So, Rahul has 25 working years (65-35 years) and would like to enjoy 20 years (80-60 years) of retirement life.

Step 1 – Project your Expenses

We are all aware that the living expenses may not remain the same. They keep increasing. So, we need to first project the expenses by assuming a certain rate of Inflation (let’s assume it as 7%).

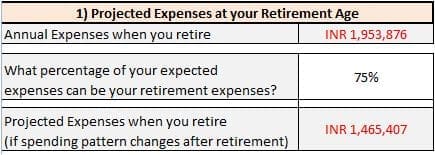

The current expenses of Rs 3.6 Lakh p.a. will be projected to be at Rs 19.53 Lakhs, in the first year of Rahul’s retirement (at 60 years of age). He needs Rs 19.63 Lakh to continue with the same spending pattern in the first year of his retirement.

However, he assumes that some of the current expenses may not be relevant when he retires. So, he assumes the projected expenses to be Rs 14.65 Lakh only (75% of 19.63 Lakh).

Rahul expects to earn 8% from his investments after the retirement. So, we now need to calculate the required retirement corpus. At 8% ROI and 7% inflation rate, the real rate of return (inflation adjusted) is 0.9346% (Real rate of return is generally used in ‘withdrawal phase’ of the investments).

To withdraw inflation adjusted expenses of Rs 14.65 Lakh for 20 years (retirement life) at 0.9346% real rate of return, the required Retirement Fund is Rs 2.66 crore. Step 3 – Calculate required savings per year / month to accumulate your retirement corpus

Step 3 – Calculate required savings per year / month to accumulate your retirement corpus

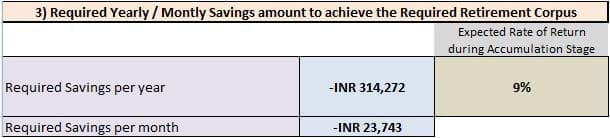

In this step, let us calculate the required savings amount to achieve the retirement goal amount (Rs 2.66 cr).

Rahul wants to invest in safe fixed income securities only, and expects 9% rate of interest from his investments. To accumulate Rs 2.66 cr in 25 years (work-span), at 9% ROI, Rahul has to save and invest Rs 3.14 Lakh per year (or) Rs 23,743 per month.

You may try these calculations using the below Retirement corpus calculator.

Download Simple & Basic Retirement Goal Planning Calculator.

We often hear about the celebrities and famous personalities struggling to make ends meet during their retirement. Kindly go through the below links to understand the importance of having a realistic and good Retirement Plan;

So, to become wealthy and to stay wealthy, it is very important to MANAGE your money properly.

You can get a HOME LOAN to buy a property. You can get a PERSONAL LOAN to meet your short-term financial goals. You can get an EDUCATION LOAN to fund your higher education (or) to fund your Kid’s higher Education. But, you don’t get a loan to fund your RETIREMENT (hmmm..by any chance, are you now thinking about Reverse Mortgage?).

Make your retirement years more comfortable and secure. Plan your retirement now! Remember, retirement planning is not a one-time event, but a continuous process of making sure you are staying in line with the goal you set for yourself. Do share your views and comments. Cheers!

Continue reading :

- Lump sum Investment options for Retirees/Senior Citizens | Where to invest my Retiral benefits to get Regular Income?

- List of Best Investment Options in India

- Is NPS a good investment choice?

- My 6 Core Personal Financial Planning principles!

- How much Term Life Insurance Cover do I need? | Online Insurance coverage Calculator

- Top 15 Best Mutual Funds to invest in 2020 & beyond | Top Performing Equity Funds

(Image courtesy of mapichai at FreeDigitalPhotos.net)

Join our channels

Very informative article explaining retirement planning in a simple 3-step structure. Many people underestimate the impact of inflation on future expenses, and this calculator clearly shows how important it is to start early. Having clarity on the retirement corpus requirement helps individuals make better investment decisions today. Along with such calculators, using Personal Financial Planning Software can further simplify goal tracking, scenario analysis, and long-term financial projections. Combining the right tools with disciplined investing can significantly improve retirement readiness.

Thanks for sharing such practical insights!

Thank you so much for your thoughtful feedback 😊

Glad you found the 3-step approach and the calculator useful — you’re absolutely right, inflation is often underestimated, and that’s where early planning makes a big difference.

Also agree with your point on using financial planning tools — they can definitely help in tracking goals and making more informed decisions over the long term.

Appreciate you taking the time to share your insights 🙏

Hey Srikanth

According to calculator, my retirement corpus will not sustain if my spouse is younger to me.

I do not understand why spouse age is not considered in the calculations. Retirement corpus should be for both to survive, not the single person.

Correct me if I am wrong.

Dear Ritz,

Kindly note that one can consider living expenses of his/her entire family and can project the required retirement corpus.

Hi,

What is your views on tata retirement savings fund? Do you have any article on it?

Dear Chandra,

It is a decent fund with two options – Moderate (Balanced) and Progressive options.

Unlike regular Equity funds, retirement oriented funds have certain certain & conditions for investments and redemptions. So, personally I prefer to invest in general equity funds.

You may kindly go through below articles related to similar retirement oriented funds;

* Reliance Retirement Fund – Equity Oriented Pension Scheme- Features & Review

* HDFC Retirement Savings Fund – Tax Saving cum Pension Scheme – Details & Review