Reliance Retirement Fund is one of the New Fund Offers which is open for subscription now. Reliance Mutual Fund has launched this open ended ‘Tax Savings’ cum ‘Pension Scheme’ on 22nd January 2015. The NFO is open from 22nd Jan to 5th of February 2015.

‘Reliance’ – ‘Pension scheme’ – ‘Retirement Fund’ – ‘Notified Tax saving scheme’..these words/features are enough to catch many investors’ attention. Moreover, many investors do their tax planning during January to March period (which is not correct, tax planning should be done and implemented throughout the financial year).

I generally do not prefer to write reviews on individual mutual fund schemes. As mentioned above, this fund is grabbing the attention of many investors during its NFO period. I have received few queries like – Is Reliance retirement fund a good plan? Should I invest in Reliance pension fund to save tax?

Hence, I thought to write about the features, review and pros/cons of Reliance Retirement Fund.

Features of Reliance Retirement Fund (RRF):

- RRF is an open ended scheme (An open-ended fund or scheme is one that is available for subscription and repurchase on a continuous basis. These schemes do not have a fixed maturity period.)

- Reliance MF claims that this is the first Notified Retirement Fund having Equity oriented scheme. (The fund has received permission from the central govt and has been notified as a pension fund under Section 80C(2)(xiv) of the Income Tax Act.)

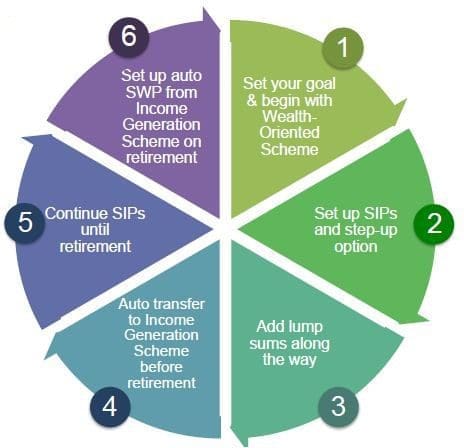

- Reliance Retirement Fund offers two schemes with distinct investment portfolios.

- Wealth Creation Scheme – This is equity oriented plan. In this plan, 65% to 100 % of the funds are invested Equity & Equity related instruments. The remaining 0 – 35% in debt and money market securities.

- Income Generation Scheme – This is Debt oriented plan. 70 to 95% of the scheme’s funds are invested in debt and money market securities and 5 – 30% in equity/equity related instruments.

- Wealth Creation scheme is for Accumulation phase. (The phase in an investor’s life when he/she builds up his/her savings. )

- Income generation option is for the investors who are nearing their retirement (who cannot afford to take risk).

- The investors can switch between these two schemes without any limitation.

- Reliance Retirement Fund has a lock-in period of Five years.

- Exit load of 1% is applicable on redemption (sale of units) before the age of 60 years.

- The fund provides ‘Auto Transfer’ facility wherein investors’ entire investment (Lump sum/SIP) shall be switched automatically from Wealth Creation Plan to Income Generation Plan (with nil exit load) at any date as specified by the investor (which is within or after the lock-in period) or upon completion of 50 years of age.

- Lump sum, Systematic Investment Plan and Step-up modes are available. (Step-up option -A facility wherein an investor who has enrolled for SIP, has an option to increase the amount of the SIP Installment by a fixed amount at pre-defined intervals.)

- Systematic Withdrawal (manual or automatic) option is available to withdraw money during the investor’s retirement phase. (Auto SWP : This optional facility aims to provide a regular inflow of money to investors (monthly/quarterly/annual) by automatic redemption of units on or after 60 years of age.)

- Investments in Reliance Retirement Fund are eligible for tax deductions up-to Rs 1.5 Lakh in a Financial Year, as per Section 80C of the Income Tax Act 1961.

- One interesting feature about this fund is, employers can sign up for this scheme. They can invest in Reliance Retirement Fund systematically by deducting the SIP amount from the employees salary.

- This mutual fund scheme has two plan – Growth & Dividend pay out options. Growth plan has again two sub-plans : i) Growth & ii) Bonus oriented.

- The minimum investment should be,

- For Lump sum – Rs 5,000

- For Monthly SIPs – Rs 500

- Quarterly SIPs – Rs 1,500

- Annual SIP – Rs 5,000

Should I Invest in Reliance Retirement Fund NFO?

My opinion and some of the important points to ponder over before investing in this retirement fund are as follow:

- We have so many good mutual funds with proven track record which are available for investments. NFO schemes do not have past performance data. Some investors may have a misconception on NFO’s Net Asset Value (NAV). It is a common misconception that an existing fund’s whose NAV is around Rs 100 is more expensive and less profitable than a NFO at Rs 10. This is just a myth.

- The fund charges 1% Exit load on switch-outs and redemptions before the attainment of 60 years of age. The reason could be, the fund manager wants to encourage the investors to stay invested for long term. But, I feel charging 1% on redemptions and that too up to 60 years of age is definitely not a good point.

- I believe this scheme is more like an ULIP (Unit Linked Insurance Plan) minus the risk coverage.

- Though the investments made under this plan has income tax exemptions, we know that Section 80C is already crowded with many investment options. If Government approves these funds for tax exemptions under other Sections (like the one offered to National Pension Scheme under Section 80 CCD, which is over & above Rs 1.5 lakh provided under section 80c), we could see good demand for these kind of pension plans.

- I personally do not believe in ‘Defined package’ ((i.e 65% of the fund’s money in equity and all) or ‘Defined Products’ (like retirement fund or pension fund etc.,). If you are an young investor and planning for your retirement, you are better off investing in normal Equity mutual funds which can invest up-to 100% in equity related instruments. You can even consider investing in good Balanced funds for your retirement planning (if you are a bit conservative investor).

- When you are planning for your long term goals like ‘retirement’, you should have the flexibility and control on the way you chose various asset classes.

- ‘The Income generation option’ is not suitable for young (in terms of age) investors .

- The nearest competitor for Mutual funds’ pension plans is NPS (National Pension Scheme). From taxation point of view, Equity oriented Pension funds outscore NPS. You can withdraw only 60% of the accumulated corpus under NPS, 40% of the remaining fund should be compulsorily invested in Annuity schemes after attaining 60 years. There is no such restriction in case of Equity oriented pension funds. The amount withdrawn (60%) and Annuity income (40%) under NPS are fully taxable. LTCG tax (Long Term Capital Gains) on redemption of equity oriented MF schemes is tax free.

Both Franklin Templeton and UTI’s have already launched pension funds which invest up to 40% into equities and rest in debt and money market securities. But they are not pure equity oriented schemes.

Franklin India Pension Plan has given returns of around 13% (annualized) in last five years. UTI’s Retirement Benefit Pension Fund has generated returns of 10% in last 5 years.

Axis, SBI, HDFC and Pramerica Mutual Fund houses had also filed offer documents with SEBI to launch similar pension funds. So, we may soon see plethora of Retirement or pension oriented NFOs hitting the primary market.

I suggest you not to get carried away by words like ‘pension fund’ or ‘retirement fund.’ With little home work and research, you yourself can build a good portfolio of investments for your retirement. These investment options can be – your EPF (Employee Provident Fund), PPF (Public Provident Fund), Balanced Funds or Equity Mutual Funds with proven past performances. You may also consider investing in Top Equity Linked Savings Scheme offered by various Mutual Fund houses. ELSS funds offer both income tax benefits and generate decent positive returns over the long run.

Most investors (retail investors) move out of equity mutual funds within few years of investment. Staying invested and periodically reviewing your retirement plan has proven to be best ways of creating long term wealth (which can generate inflation protected retirement income.)

Most of us generally think that lot of time is left for retirement planning. Do not think like that. Retirement planning should be your topmost priority. Based on your current expenses, retirement age, life expectancy and future inflation (during retirement/withdrawal phase) calculate your required retirement corpus. Once you know how much you need, work backwards to calculate how much do you need to save periodically till you retire.

Will you consider investing in Mutual fund pension or retirement schemes? Do you have retirement plan in place? Share your views and comments. Cheers!

Continue reading :

(Image courtesy of hyena reality at FreeDigitalPhotos.net) (References : Reliance Retirement Fund Scheme Information document)

Join our channels

Dear sree

good morning!

Can u tell me what should be ideal portfolio for retirement. for 30 year old.

or,

what financial products must have in retirement portfolio for anyone.

Thanjs

Dear Abhee,

Options can be many!

But, I believe that Equity oriented funds can be surely considered for long term goal like Retirement.

Kindly read:

Retirement planning goal calculator.

List of best investment options!

PLEASE REPLY

THANKS FOR REPLY SREE

my age 37 i want to immediately pension or months income plan life time

1.Month income Rs 20,000 p/m

2.how do u work ? any idea ?

3.how much investment scheme ?

Dear feroz,

Do you mean to say that you would like to get monthly pension from now? (at age 37 onwards)

Suggested reading: Retirement planning & calculator.

yes today investment lump amount immediately start income

i am not waiting 60 age just now regular income

I agree with Mr.Harish. Indian investors are not mature enough to invest and resist temptation to redeem/ wait till the financial goals are achieved. There are many cases where people have withdrawn EPF at the time of job change.The views of Mr.Srikant Reddy may be appropriate and useful for mature and knowledgeable investors. Not for nascent investing nation like ours.

Mutual fund advisers tell how difficult it is to convince this generation which believes in instant gratification to save for future. Moreover,Reliance retirement fund has started recently and one should give at least 5 years time before comparing its performance with peers in the field. As a fund house,RMF is doing well if not great.

sir, i m very new to to mutual fund schemes. I have started SIP of rupees 10000/- in reliance retirement fund – wealth creation scheme and SIP of rupees 10000 /- in HDFC children gift fund – investment plan just one month before as per advice of a financial adviser.

I want to invest for long term and can take moderate risk . My goals are child higher education ( after 12-13 years) and retirement planning after 25-30 years.

i already have term plan of 1 crore, personal accident policy of 50 lakhs and mediclaim of 5 lakhs rupees.

please suggest whether i should continue with these two plans or discontinue above plans and go with some other funds.

And please also suggest best mutual funds / schemes for me to invest.

Dear akshay,

Nothing wrong as such with both invested funds. But the point is there are better funds considering past returns, ease of operation, flexibility etc.,

Kindly read:

Children’s gift mutual funds review..

Best Equity funds 2016.

Retirement planning calculator

Kid’s education planning calculator.

Best investment options list.

The idea of a 1% load is not such a bad idea. There is big positive side to it as well. Though it can be argued on why invest in a retirement fund instead one could invest in an good equity oriented fund with a retirement objective. Although this is one way of looking at it. The other perspective to it is if you are investing for Retirement and if you are comfortable with age 60 as your retirement age, How does the 1% exit load even matter. One of the MAJOR ideas of the schemes is “FORCED SAVINGS”. Therefore in a way it penalizes you if you redeem your funds before age 60. It makes complete sense for a retirement fund to be designed this way as quick redemptions in a short span is one of the biggest problem any fund house faces today.

More over if you take cue from the funds world over specially in the developed markets. Retirement or Pension funds are historically some of the best funds in terms of performance which is purely due to its long term nature and lower redemption rate.Thereby enabling fund managers to manage it better

Dear Harish,

Forced Savings may not work for majority of investors (esp in India). If someone wants to redeem looking at short-term fluctuations in Equity markets, he/she may redeem irrespective of the load percentage.

But, investing in Retirement funds like these is much better than investing in Pension schemes offered by Life insurance companies or say NPS.

Dear sreekanth,

I agree, the culture of redemption looking at short term fluctuations is by and large the mind set of Indian retail investors.

However,that is precisely why these retirement funds with exit loads will work because it will straight away discourage investors who are not willing to invest systematically for the long term, from entering the fund.

This is good for the Fund manager to take a take a long term perspective to investment and manage the fund better thereby benefiting the long term investors.

For people who redeem at short term fluctuations, be it retirement fund or any other equity fund or any other fund as the case may be, this short term & wavery approach of investing for “RETIREMENT” may not work.

The main point that I am trying to drive here is the decision of whether should I invest in an ELSS or other equity funds OR should I invest in a retirement fund for the purpose of “RETIREMENT” cannot be made just on the basis of just comparing the features of the 2 plans like exit load, lock in period. etc.

In my opinion the suggestion to an investor has to go way beyond that in understanding the investor itself and his mindset and attitude towards investment rather than just comparing 2 schemes and saying one is better than the other.

There is definitely no “One size fits all” concept.

I am not trying to say retirement funds are always a better bet than other funds for retirement. But it really depends, what is good for one may not be the best option for another.

Most of the earlier comments and views were completely skewed against retirement funds based on comparing the features of the scheme without keeping the investor in mind.

My idea of posting this comment is to bring about a broader perspective while considering these various options.

Dear Harish,

I do not agree that just because of 1% load factor, majority of the investors stop or postpone redeeming the fund units.

I agree with your views that comparison of financial products can not be just based on few factors.

End of the day it is PERSONAL Finance and as you said ‘no one size fits all’..

Appreciate for sharing your views. Kindly keep visiting 🙂

Sreekanth sir

can you please provide me your email id…as i have a query about my investment in mutual fund

Dear Lekh Raj..I have answered your queries, kindly check your email a/c.

Sir

I invested in ICICI prudential equity linked pension fund with a protector plan and after 6 months switched over to maximiser II plan. This is a 10 years plan and I remain invested & continued paying premium every year. And after completion of 10 years period, with pension period to start, I decided to surrender the policy and have got my amount based on NAV prevailing at that period. I would be grateful if you could please advise me if my gain is to be treated as long term capital gain with equity exposure & attract nil tax or will I have to pay tax on gains and what is the treatment.

Manoj

Dear Manoj,

Kindly share the name of the product. Is it mutual fund or life insurance product?

If it is a pension plan from life insurance company then the premiums that you have claimed as part of deduction under section 80C will be reversed and you will have to pay tax on it. Secondly, the entire surrender value will be added to your income and you will have to pay tax on it according to your tax slab.

Hi Sreekanth,

I am new to Mutual Funds, I have invested in Reliance Retirement Fund and ICICI Pru Tax saver plan,

could you please let me know whether these 2 are good plans or not?

My age is 30 and I want to have 4 crore by the age of 55.

Could you please suggest hoe to invest so that I can have this much ???

Dear Asim,

May I know the reason for investing/selecting these two funds?

Suggest you to go through the below articles and revert to me;

Retirement planning in 3 easy steps

Calculate future value of your investments

Top Equity funds.

Hi Sreekanth,

Thanks for the nice and unbiased review. I am a regular follower of your blogs. I have created my CAN no. after your blog about MF utilities. Now its very convenient to invest in mutual funds.

I have two questions please clarify.

1)Exit load:

Nil in case of Auto SWP/Redemption/Switch out from Reliance Retirement Fund on or after attainment of 60

years of age or after completion of 5 year lock in period, whichever is later

What it means..? what they mean by “whichever is later” If i withdraw it before attaining 60years and after 5 year lockin, then exit load is NIL..?

2) 65% Equtiy and 35% equity is very same as a typical balanced fund. Due to the 5 year lockin ..will it fetch more return than HDFC, ICICI balanced funds? Will the fund manager have any flexibility/advantage to generate better returns?..If we check the portfolio of this and other balanced fund..do you see anything unique in this?

Thanks,

Senthil

Dear Senthil,

1 – To keep it simple – Exit load is applicable if units are redeemed before 60years of age.

2 – It is 65% equity and 35% debt right?? I prefer to invest in a balanced fund (as mentioned by you) rather investing in this type of funds.

sir,can you tell about sbi life retire smart plan benifits

Dear Ramsha,

Did you already invest in this pension plan?

no sir,planning to invest

Dear Ramsha,

Suggest you to invest in equity mutual funds for long term / retirement goal instead of pension plans.

Kindly go through my articles;

Top Equity funds

Top Balanced funds

I am 64 yrs. I wish to invest Rs 5000 for ten years in two schemes. Which mutual equity fund gives best return. What minimum and maximum returns I escape in such a scheme?

Dear Mr Nath,

Consider investing in a balanced fund & a Large cap Fund.

Kindly read my articles : “Top Equity Funds” & “Top Balanced Funds“.

HI sir,

I am rajamouli 31 years old. If I am invested 1000 per month in reliance retirement wealth creation fund.

How much I will get approximately at the time of retirement?

please give me reply

Dear Rajamouli,

You have invested in an equity oriented scheme, the maturity amount can not be predicted.

Hello Mr. Shreekanth,

Thanks for your valuable and honest review on Reliance Retirement Fund.

Personally I feel for availing Tax benefit in Mutual fund, I would prefer to investing money in ELSS which gives us an option of redeeming after 3 years than this Reliance Retirement Fund which has 1% exit load (if redeemed before the age of 60). Moreover when both Funds (ELSS and this Retirement Fund wealth creation) object is to invest in Equity market directly, i still feel that ELSS has an edge over Retirement Fund as in ELSS we can withdraw after 3 years.

Regards,

Udaya Poojary

Dear Udaya,

Thank you for sharing your views. Agree with your points. But, one needs to invest in ELSS with a long term view (i m sure you agree with me).

All debt funds are charged in long term@20% after indexation.. Is reliance retirement plan also charged? At the age of 60 or during swp is each payment received charged?

Dear Pavitra,

Reliance Mutual Fund’s Retirement plan is an Equity Oriented Scheme. So, the Long term capital gains are exempted from taxes (after holding the units for more than one year).

Thanks Sreekanth. But is the fund not invest in debt?

Dear Pavitra,

My previous reply was related to Reliance Retirement fund – Wealth creation option. (In this option the scheme can invest in 65% to 100% of its funds in Equity related securities).

In case of Income generation scheme, this fund is treated as a Debt oriented product (70 to 95% of the scheme’s funds are invested in debt and money market securities) and you are right about the 20% LTCG taxes.

Kindly note that there is a 5 year lock-in period.

Just another confusion. The pitch was that the customer can make switches between the income annd wealth plan. In that case what will be tax treatment?

Dear Pavitra,

I was expecting this query 🙂

The tax treatment will depend on the time-frame only. (How many days/months the units are in Equity scheme/Debt scheme)

Thanks for prompt replies to queries. Making a mental note to come back to your blog regularly. 🙂

Dear Pavitra,

My pleasure & Thank you. Keep visiting!

Hello Sir,

I am 42 years old. I am new to mutual funds. I do not want to invest in any pension fund, Instead I would like to create my own portfolio for my retirement exclusively. Currently, I am having one SIP investment into HDFC Balance fund (on my friend’s suggestion) of 5,000. I am a long term (2o years) investor (can take moderate risk). I want to extend my portfolio by adding two more funds (with SIP of 4,000 each). My goal is to get handsome corpus at my retirement age of 60. Can you please suggest any two funds to add to my RETIREMENT PORTFOLIO ?

Thanks,

Narasimha

Dear Narasimha,

Good to know that you are very clear about your financial goal and investment requirements.

Since you have 20 years as investment time-frame, you can consider investing in 1 Large-cap and one Equity diversified funds. You may continue these SIPs, may be for next 15 years and slowly move the accumulated corpus (15th year to 20th year period) to safe/debt oriented financial securitieds (like Debt mutual funds/FDs/Post office schemes).

Read my article on “Top Equity Mutual Funds.” Let me know if you need more info.

Hi, what are the management charges for this fund. Can u throw some light on it.

Dear Teja,

The expense ratio for Wealth Creation scheme is upto 2.5% and for Income generation scheme it is upto 2.25%.

Dear Sreekanth ,

Thank you so much for the review. I was looking for information about how the retirement corpus is dealt with. Is it compulsory to have annuity or full amount is redeemable and tax treatment of the same. You have explained it better than the scheme information doc. Appreciate that. Thanks,

Sachin

Dear Sachin,

Thank you and nice to know that you could find the required information here. Keep visiting!