Normally, a person is taxed in respect of income earned by him/her only. However, in certain special cases income of other person is clubbed (i.e. included) in the taxable income of the taxpayer and in such a case he will be liable to pay tax in respect of his income (if any) as well as income of other person too.

The situation in which income of other person is included in the income of the taxpayer is called as ‘Clubbing of income‘. Income Tax Section 60 to 64 contains various provisions relating to clubbing of income.

Example : Income of minor child is clubbed with the income of his/her parent (Section 64(1A) of the Income Tax Act).

In this post let us understand – What are the different situations for clubbing of income? When do provisions of clubbing of income of spouse apply? What are the exceptions?….

Situations for Clubbing of Income & the Exceptions

Below are the main scenarios where clubbing of Income provisions apply;

- Clubbing of Income of Spouse (Transfer to Spouse)

- Clubbing of Income of Son’s Wife (Transfer to Son’s Wife)

- Clubbing of Income of a Minor Child

- Transfer of Income without Transfer of Assets

- Revocable Transfer of Assets

- Transfer of Asset to HUF (Hindu Undivided Family)

Clubbing of Income of Spouse

In the below situations the income of your spouse is included in your income;

1) Remuneration / Salary paid to Spouse

- Salary, Commission, Fees or remuneration paid to Spouse, from a concern / firm in which you have a substantial interest. The spouse of the individual is employed without any technical or professional knowledge or experience (i.e., remuneration is not justifiable).

- An individual shall be deemed to have substantial interest in any concern, if such individual alone or along with his relatives beneficially holds at any time during the previous year 20% or more of the equity shares (in case of a company) or is entitled to 20% of profit (in case of concern other than a company).

- Example : Mr Chandra Babu holds 25% equity shares of Heritage Minerals Pvt. Ltd. His wife – Smt Bhuvaneshwari is employed as Manager (in Sales department) in the same company, at a monthly salary of Rs. 90,000. Bhuvaneshwari is not having any knowledge, experience or qualification in the field of Sales. Will the remuneration (i.e., salary) received by Bhuvaneshwari be clubbed with the income of Mr. Babu?

- In this situation, Mr. Babu is having substantial interest in Heritage Minerals Pvt. Ltd. and remuneration of Bhuvaneshwari is not justifiable (i.e., she is employed without any technical or professional knowledge or experience) and, hence, salary received by her from Heritage Minerals Pvt. Ltd. will be clubbed with the income of Mr. Babu and will be taxed in the hands of Mr. Babu only.

- Exception – Is there any situation in which the clubbing of income provision does not apply even if remuneration is paid to Spouse?

- Clubbing of income is not attracted in case your Spouse possesses technical or professional qualification and remuneration is received in exercise of that knowledge and qualification.

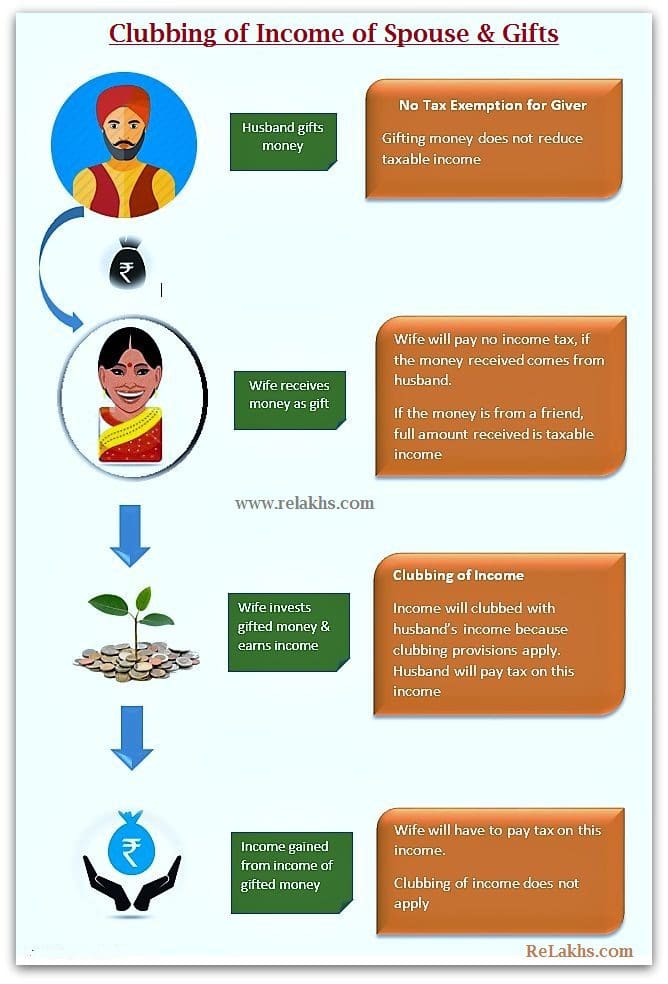

2) Income from Assets transferred to the Spouse (U/S 64 (1) (iv)

As per section 64(1)(iv), if an individual transfers (directly or indirectly) his/her asset (other than house property) to his or her spouse otherwise than for adequate consideration, then income from such asset will be clubbed with the income of the individual (i.e., transferor).

- Example : Mr. Lalu Prasad has Fixed deposits worth Rs 1 crore. He gifted these deposits to his wife. Will the income from these FDs be clubbed with the income of Mr. Lalu?

- In this situation, the bank FDs are transferred to spouse. Transfer is via gift (i.e., without any consideration) and, hence, interest income (taxable income) generated from the transferred asset, i.e., interest on such FDs will be clubbed with the income of Mr. Lalu only.

Income from transfer of house property without adequate consideration (example – Gifting an ownership share in property) will also attract clubbing provisions, however, in such a case clubbing will be done as per section 27 and not under section 64(1)(iv). The provisions of clubbing will apply even if the form of asset is changed by the transferee-spouse.

- Mr. Suresh (transferor) gifts Rs. 1 crore to his wife Swapna (transferee) in FY 2023-24. The said amount is invested by his wife in a house property. Will the rental income (if any) from the house property purchased by Swapna Suresh from gifted money be clubbed with the income of Mr. Suresh for AY 2024-25?

- In this case asset transferred is money and, subsequently, the form of asset is changed to house property, hence, rental income from house property acquired from money gifted by her husband will be clubbed with the income of her husband. Thus, rental income received by Swapna Suresh will be clubbed with the income of Mr. Suresh for AY 2024-25.

- In case, the property is a self-occupied by husband and wife then annual rental value is NIL, so, no part of the income shall be clubbed with the transferror (Suresh).

As per section 64(1)(vii), if an individual transfers (directly or indirectly) his/her asset for inadequate consideration to a person or an association of persons for the immediate or deferred benefit of his/her spouse, then income arising from the asset so transferred will be clubbed with the income of transferor.

Exceptions – Are there any situations in which the clubbing of income provision do not apply even in case of income from Assets transferred to Spouse?

The clubbing provisions of section 64(1)(iv) are not applicable in the following situations:

- If the transfer of asset is for adequate consideration (not a gift).

- If the transfer of asset is in connection with an agreement to live apart.

- If the asset is transferred before marriage, no income will be clubbed even after marriage, since the relation of husband and wife should exist both at the time of transfer of asset and at the time of accrual of income.

- If on the date of accrual of income, transferee is not spouse of the transferor (i.e. the relation of husband and wife does not exist).

- A husband can transfer / purchase a share in the property in exchange for wife’s jewellery or Streedhan. In this case, clubbing of income provisions do not apply.

Clubbing of Income of Son’s Wife (Transfer to Son’s Wife)

As per section 64(1)(vi), if an individual transfers (directly or indirectly) his/her asset to his/ her son’s wife otherwise than for adequate consideration, then income from such asset will be clubbed with the income of the individual (i.e., transferor being father-in-law/mother-in-law).

The provisions of clubbing will apply even if the form of asset is changed by the daughter-in-law (transferee).

If the asset is transferred before marriage of son, no income will be clubbed even after marriage, since the relation of father-in-law/mother-in-law and daughter-in-law should exist both at the time of transfer of asset and at the time of accrual of income.

If on the date of accrual of income, the relation of father-in-law/mother-in-law and daughter-in-law does not exist, then the provisions of clubbing will not apply.

As per section 64(1)(viii), if any individual transfers (directly or indirectly) his/her asset otherwise than for adequate consideration to a person or an association of persons for the immediate or deferred benefit of his/her son’s wife, then income arising from the asset so transferred will also be clubbed with the income of transferor.

Clubbing of Income of Minor Child

As per section 64(1A) , income of minor child is clubbed with the income of his/her parent. In case the income of individual includes income of his/her minor child, such individual can claim an exemption under section 10(32)) of Rs. 1,500 or income of minor so clubbed, whichever is less.

Income of minor will be clubbed with the income of that parent whose income (excluding minor’s income) is higher (if both the parents are earning individuals).

Exceptions :

- Income of minor child earned on account of manual work or any activity involving application of his/her skill, knowledge, talent, experience, etc. will not be clubbed with the income of his/her parent. However, accretion from such income will be clubbed with the income of parent of such minor.

- However, income of a minor suffering from disability specified under section 80U will not be clubbed with the income of his/her parent.

Example :

Mr. Raja has two minor children, viz., Master A and Master B. Master A is a child artist and Master B is suffering from diseases specified under section 80U. Income of A and B are as follows:

- Income of A from Stage shows : Rs. 1,00,000

- Income of A from bank interest : Rs. 6,000

- Income of B from bank interest : Rs. 1,20,000.

Will the income of minor children be clubbed with the income of their parent (Mrs. Raja is not having any income)?

- As per section 64(1A) , income of minor children is clubbed with the income of that parent whose income (excluding minor’s income) is higher. In this case, Mrs. Raja is not having any income and, hence, if any income is to be clubbed then it will be clubbed with the income of Mr. Raja.

- Income of minor child earned on account of manual work or income from the skill, knowledge, talent, experience, etc., of minor child will not be clubbed with the income of his/her parent. Thus, income of A from stage show will not be clubbed with the income of Mr. Raja but income of A from bank interest of Rs. 6,000 will be clubbed with the income of Mr. Raja.

- Income of a minor suffering from disability specified under section 80U will not be clubbed with the income of his/her parent. Hence, any income of B will not be clubbed with the income of Mr. Raja.

- The taxpayer can claim an exemption under section 10(32)). Thus, in respect of interest income of Rs. 6,000 clubbed in the income of Mr. Raja, he will be entitled to claim exemption of Rs. 1,500 under section 10(32)), hence, net income to be clubbed will be Rs. 4,500 (i.e., Rs. 6,000 – Rs. 1,500).

Transfer of Income without Transfer of Assets

As per section 60, if a person transfers income from an asset owned by him without transferring the asset from which the income is generated, then the income from such an asset is taxed in the hands of the transferor (i.e., person transferring the income).

E.g., Mr. Pawan Kalyan has given a bungalow owned by him on rent. Annual rent of the bungalow is Rs. 10,00,000. He transferred entire rental income to his friend Mr. Trivikram. However, he did not transfer the bungalow. In this situation, rent of Rs. 10,00,000 will be taxed in the hands of Mr. Pawan Kalyan.

Revocable Transfer of Assets

Revocable transfer is generally a transfer in which the transferor directly or indirectly exercises control/right over the asset transferred or over the income from the asset.

As per section 61, if a transfer is held to be a revocable (capable of being revoked or cancelled), then income from the asset covered under revocable transfer is taxed in the hands of the transferor.

Transfer of Asset to HUF (Hindu Undivided Family)

As per section 64(2), when an individual, being a member of HUF, transfers his property to the HUF otherwise than for adequate consideration or converts his property into the property belonging to the HUF then clubbing provisions will apply as follows:

- Before partition of the HUF, entire income from such property will be clubbed with the income of transferor.

- After partition of the HUF, such property is distributed amongst the members of the family. In such a case income derived from such property by the spouse of the transferor will be clubbed with the income of the individual and will be charged to tax in his hands.

Hope you now have complete idea about clubbing of income provisions. I will soon publish a separate article on – ‘How To avoid Clubbing Of Income Provisions? | Some Tax Saving tips!’

Kindly share your views and comments, cheers!

Cotnine reading :

- Got a Gift? Find out, if it is Taxable or Tax-free?

- Income Tax Deductions List FY 2023-24 | Under Old & New Tax Regimes

- What is Streedhan? – Meaning & Constituents | How can Women protect it?

- Life Insurance & Married Women’s Property Act (MWP Act) – Details & Benefits

- Nominee Vs Legal Heir : Who will inherit (or) own your Assets? | Importance of WILL

- Can a Mortgaged property be Gifted, Willed or Inherited?

(Featured Image courtesy of Sira Anamwong at FreeDigitalPhotos.net) (Post first published on : 04-August-2020) (Source / References : incometaxindia.gov.in)

Join our channels

1) IF Gain from Mutual fund is below 1 lac then it needs to show in ITR ??

2) If Yes then at where in ITR ??

3) Which ITR use for above mentioned Gain ??

Dear Mansukh,

1 – Yes, advisable to file ITR

2 & 3 – Kindly go through this article @ AY 2020-21 Income Tax Return Filing Tips | Which ITR Form should you file?

Dear Sreekanth Reddy,

Thanks for your reply

I have read that article about AY 2020-21 Income Tax Return Filing Tips | Which ITR Form should you file?

But yet i have confusion let me just know that i have Salary income , FD Interest Income & Mutual Fund Gain which is near about 60000, then

1) for above three income which ITR i should use ?? Either it should be ITR-1 Or any else ?? because for Salary & FD Interest i know ITR-1 is applicable but for Mutual fund income which is below 1 lac so it’s confusion so please suggest which ITR i should use ??

2) also advice In ITR where that mutual fund income should i report ?? should it report under Exempt income column in ITR ?? or not ??

Dear Mansukh,

Advisable to file ITR-2.

You can disclose it under Capital gains section and as Gains are less than Rs 1 lakh, no tax liability.

My compliments and thanks for taking painstaking effort for this very important, informative and exhaustive article.

I request you to let me know the following:

1. How dividend income from rights issue, renounced offline in favour of Wife and paid from Wife’s account, will be treated. Will it be income of Wife or clubbed with income of Husband.

2. In future if Wife sells shares in point no 1, for taxation purpose, will it be her capital gains or of Husband’s.

3. If company shares are gifted to Wife by Husband by offline transfer without consideration, will dividend income be treated as Wife’s income or clubbed with Husband’s income.

4. When such gifted shares are sold by Wife, for tax purpose will CG be treated as Wife’s or of Husband’s.

5. Do above transfers in 1 and 3, have to be reported in ITR and any tax has to be paid by Wife or Husband.

Will CG be applicable to Husband while making offline transfer.

Kindly clarify any other relevant point.

Mahesh

Dear Mahesh,

Thanks for the appreciation!

1 – I believe that any taxable income is clubbed to the transferor.

2 – Husband’s.

3 – Husband’s.

4 – Husband’s.

5 – Yes, applicable to husband.

Suggest you to kindly consult a CA as well.