Tax planning is an important part of a financial plan. Whether you are a salaried individual, a professional or a businessman, you can save taxes to certain extent through proper tax planning.

The Indian Income Tax act allows for certain Tax Deductions / Tax Exemptions which can be claimed to save tax. You can subtract tax deductions from your Gross Income and your taxable income gets reduced to that extent.

A new income tax regime was proposed in Budget 2020. Budget 2020 has sparked a new debate on which income tax slab rates are beneficial for tax assessees (New Tax Regime Vs old one). A taxpayer can opt for it by forgoing 70 income tax exemptions.

Latest Articles (02-Feb-2021) :

- Budget 2021 | Latest Income Tax Slab Rates FY 2021-22 & Key Highlights

- 15 Important Budget 2021 Proposals related to your Personal Finance

Latest Income Tax Slab Rates FY 2020-21 / AY 2021-22

Offering an optional lower rate of income tax to individuals, Finance Minister Nirmala Sitharaman in the Budget 2020-21 proposed new income tax slabs of 15% and 25% in addition to the 10%, 20% and 30% slab rates.

In case, you wish to claim your IT deductions and exemptions then your income will be subject to tax as per the old FY 2019-20 income tax slab rates only (as below);

Related Article : New Income Tax Slab Rates Vs Old Tax Regime | Which one is better AY 2021-22?

Income Tax Deductions under New Tax Regime FY 2020-21

Individuals opting to pay tax under the new proposed lower personal income tax regime will have to forgo almost all tax breaks that you have been claiming in the old tax structure.

Below is the list of the main tax exemptions and deductions that are not available for the tax payers if you opt for the new regime;

- The most commonly claimed deductions under section 80C will go.

- Section 80C deductions claimed for provident fund contributions, life insurance premium, school tuition fee for children and various specified investments such as ELSS, NPS, PPF can not be availed.

- House rent allowance

- Leave Travel Allowance

- Standard Deduction of Rs 50,000

- Deduction available under section 80TTA (Deduction in respect of Interest on deposits in savings account) and 80TTB (Deduction in respect of Interest on deposits to senior citizens).

- Interest paid on housing loan taken (Section 24).

- Under the new tax regime, set-off of loss under Income from House Property is not allowed. However, you can still use it to nullify rental income from a let-out property.

- The deduction claimed for medical insurance premium under section 80D will also not be claimable.

- Tax break on interest paid on education loan will not be claimable-section 80E.

- Tax break on donations to charitable institutions available under section 80G will not be available

So, all deductions under chapter VIA (like section 80C, 80CCC, 80CCD, 80D, 80DD, 80DDB, 80E, 80EE, 80EEA, 80EEB, 80G, 80GG, 80GGA, 80GGC, 80IA, 80-IAB, 80-IAC, 80-IB, 80-IBA, etc) will not be claimable by those opting for the new tax regime.

The above are part a total of 70 deductions and tax exemptions that will not be available in the new tax regime.

Income Tax Deductions & Exemptions allowed under New Tax Regime AY 2021-22

Section 80CCD(2)

Employer contribution on account of employee in notified pension schemes like EPF, NPS and/or Super Annuation Account can be claimed up to Rs 7.5 lakh limit.

An employer can contribute an amount equal to 12% of the employee’s basic monthly salary to his/her EPF account. Similarly, an employer can contribute an amount equal to 10% of the employee’s basic salary to the Tier-I account of NPS. In a superannuation account, an employer can contribute maximum of Rs 1.5 lakh exempted from tax in a financial year.

The budget has restricted the tax-exempt superannuation, NPS and EPF account contribution by the employer to maximum of Rs 7.5 lakh in a financial year. Further, the budget states that any interest or gains earned from the excess contribution will also be taxable in the hands of an employee.

Interest received on Post office Account

Interest received on post office savings account balance is exempted up to Rs 3,500 under section 10(15)(i) of the Income-tax Act. (Exemption of up to Rs 7,000 for joint savings account).

Gratuity & Other retiral benefits

Gratuity is tax-exempt up to Rs 20 lakh in a lifetime for non-government employees. For government employees, all gratuity received is tax-exempt, irrespective of the amount received by them.

Below benefits up to certain threshold limits (if any) are allowed under new tax regime as well;

- Commutation of pension

- leave encashment on retirement

- retrenchment compensation

- VRS benefits

- NPS withdrawal benefits

- Education scholarships

- Payments of awards instituted in public interest

Interest on EPF Account

The interest received from EPF account continues to be exempted from tax in the new tax regime as well, provided it does not exceed 9.5%.

The Interest and maturity amount received on Sukanya Samriddhi account, PPF account are tax-free in both old and new tax regimes.

Tax Rebate of up to Rs 12,500 u/s Section 87A

Individuals having taxable income of up to Rs 5 lakh will be eligible for tax rebate under section 87A up to Rs 12,500, thereby making zero tax payable in the new tax regime.

Related article : Rebate under Section 87A AY 2021-22 | Is Sec 87A Tax Rebate Available under New Tax Regime?

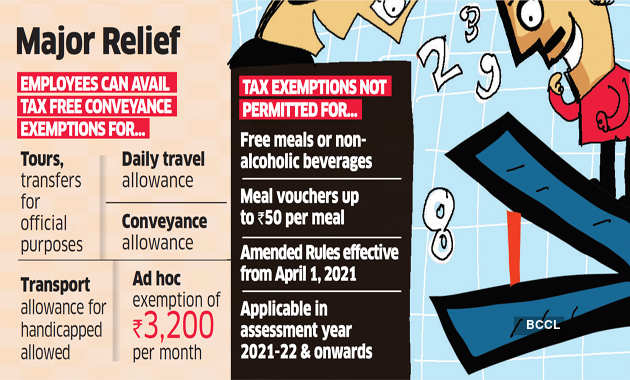

Conveyance Allowance

You can claim income tax exemption for conveyance, travel and other allowances given by your employers under the new tax regime as well.

Income Tax Deductions available under Old Tax Regime for FY 2020-21 / AY 2021-22

Section 80c

The maximum tax exemption limit under Section 80C is Rs 1.5 Lakh only. The various investment avenues or expenses that can be claimed as tax deductions under section 80c are as below;

- PPF (Public Provident Fund)

- EPF (Employees’ Provident Fund)

- Five year Bank or Post office Tax saving Deposits

- NSC (National Savings Certificates)

- ELSS Mutual Funds (Equity Linked Saving Schemes)

- Kid’s Tuition Fees

- SCSS (Post office Senior Citizen Savings Scheme)

- Principal repayment of Home Loan

- NPS (National Pension System)Income Tax benefits are currently available on Tier-1 deposits only (FY 2018-19). The contributions by the government employees (only) under Tier-II of NPS will also be covered under Section 80C for deduction up to Rs 1.5 lakh for the purpose of income tax, with a three-year lock-in period. This is w.e.f April, 2019.

- Life Insurance Premium (Read : ‘Best Term insurance plans‘)

- Sukanya Samriddhi Account Deposit Scheme

Section 80CCC

Contribution to annuity plan of LIC (Life Insurance Corporation of India) or any other Life Insurance Company for receiving pension from the fund is considered for tax benefit. The maximum allowable Tax deduction under this section is Rs 1.5 Lakh.

Section 80CCD

Employee can contribute to Government notified Pension Schemes (like National Pension Scheme – NPS). The contributions can be upto 10% of the salary (salaried individuals) and Rs 50,000 additional tax benefit u/s 80CCD (1b) was proposed in Budget 2015.

As per the Budget 2017-18, the self-employed (individual other than the salaried class) can contribute up to 20% of their gross income and the same can be deducted from the taxable income under Section 80CCD (1) of the Income Tax Act, 1961.

To claim this deduction, the employee has to contribute to Govt recognized Pension schemes like NPS. The 10% of salary limit is applicable for salaried individuals only and Gross income is applicable for non-salaried. The definition of Salary is only ‘Dearness Allowance.’ If your employer also contributes to Pension Scheme, the contribution amount (10% of salary) of up to Rs 7.5 lakh can be claimed as tax deduction under Section 80CCD (2).

The Centre contributes 14% of basic salary to Govt employees’ pension corpus, up from 10%. This is w.e.f April, 2019.

Contributions to ‘Atal Pension Yojana‘ are eligible for Tax Deduction under section 80CCD.

Kindly note that the Total Deduction under section 80C, 80CCC and 80CCD(1) together cannot exceed Rs 1,50,000 for the financial year 2020-21. The additional tax deduction of Rs 50,000 u/s 80CCD (1b) is over and above this Rs 1.5 Lakh limit.

Section 80D

In the union budget 2018, the government of India implemented the below changes with respect to deductions available on Health Insurance and/or towards Medical treatment. The same provisions are applicable for FY 2020-21 as well.

The below limits are applicable for Financial Year 2020-2021 (or) Assessment Year (2021-2022) u/s 80D.

Preventive health checkup (Medical checkups) expenses to the extent of Rs 5,000/- per family can be claimed as tax deductions. Remember, this is not over and above the individual limits as explained above. (Family includes: Self, spouse, parents and dependent children).

NRIs also can claim tax deduction u/s 80D.

Section 80DD

You can claim up to Rs 75,000 for spending on medical treatments of your dependents (spouse, parents, kids or siblings) who have 40% disability. The tax deduction limit of upto Rs 1.25 lakh in case of severe disability can be availed.

To claim this deduction, you have to submit Form no 10-IA.

Section 80DDB

An individual (less than 60 years of age) can claim upto Rs 40,000 for the treatment of specified critical ailments. This can also be claimed on behalf of the dependents. The tax deduction limit under this section for Senior Citizens and very Senior Citizens (above 80 years) has been revised to Rs 1,00,000 w.e.f FY 2018-19.

To claim Tax deductions under Section 80DDB, it is mandatory for an individual to obtain ‘Doctor Certificate’ or ‘Prescription’ from a specialist working in a Govt or Private hospital.

Section 24 (B) (Loss under the head Income from House Property)

- From FY 2017-18, the Tax benefit on loan repayment of second house is restricted to Rs 2 lakh per annum only (even if you have multiple houses the limit is still going to be Rs 2 Lakh only and the ceiling limit is not per house property).

- The unclaimed loss if any will be carried forward to be set off against house property income of subsequent 8 years. In most of the cases, this can be treated as ‘dead loss‘.

- I believe that this is a major blow to the investors who have bought multiple houses on home loan(s) with an intention to save taxes alone.

- Until FY 2016-17, interest paid on your housing loan is eligible for the following tax benefits ; Municipal taxes paid, 30% of the net annual income (standard deduction) and interest paid on the loan taken for that house are allowed as deductions.

- After these deductions, your rental income can be NIL or NEGATIVE and is called ‘loss from house property’ in the latter case.

- Such loss is currently allowed to be set off against other heads of income like Income from Salary or Business etc. which helps you to lower you tax liability substantially.

No tax on notional rent on Second Self-occupied house is available. So, you can hold 2 Self-occupied properties and don’t have to show the rental income from second SoP as notional rent. This is with effective from FY 2019-20.

Section 80E

If you take any loan for higher studies (after completing Senior Secondary Exam), tax deduction can be claimed under Section 80E for interest that you pay towards your Education Loan. This loan should have been taken for higher education for you, your spouse or your children or for a student for whom you are a legal guardian. Principal Repayment on educational loan cannot be claimed as tax deduction.

There is no limit on the amount of interest you can claim as deduction under section 80E. The deduction is available for a maximum of 8 years or till the interest is paid, whichever is earlier.

Section 80E is available to NRIs as well.

Section 80EEA

Besides the tax deductions under Section 80C and 24b, an individual can claim up to Rs 1.5 lakh under Section 80EEA from FY 2019-20. The same is continued for FY 2020-21 or AY 2021-22 as well, subject to below conditions;

- The home loan should have been sanctioned between 1st April, 2019 to 31st March 2020.

- The Stamp duty value of the property should not exceed 45 Lakhs.

- Taxpayer should not own any other residential property on the date of loan sanction.

- This tax benefit will be available from 1st April 2020 (AY 2020-21) and till the end of the home loan tenure (closure).

- The total interest deduction is now Rs. 3.5 lakh (Rs 2 Lakh +

- Rs 1.5 Lakh).

Kindly note that the deduction under Section 80EEA is available for home loans from banks and approved financial institutions only. Under Section 24, even interest paid on home loans from friends and relatives is eligible for tax benefit.

To claim tax benefit under Section 24, you should have received possession of your house (interest paid before possession is eligible for deduction over the next 5 years in 5 equal installments). Section 80EE and 80EEA do not impose any requirement of possession or completion of construction. Therefore, Section 80EEA provides you immediate tax relief even if you have purchased an under-construction property.

Both resident Indians and non-resident Indians (NRIs) can claim the deduction u.s 80EEA.

Section 80EEB

A Tax deduction of up to Rs 1.5 lakh can be claimed on Interest paid on Loans taken to purchase Electronic Vehicles.

Section 80G

Contributions made to certain relief funds and charitable institutions can be claimed as a deduction under Section 80G of the Income Tax Act. This deduction can only be claimed when the contribution has been made via cheque or draft or in cash. In-kind contributions such as food material, clothes, medicines etc do not qualify for deduction under section 80G.

The donations made to any Political party can be claimed under section 80GGC.

W.e.f FY 2017-18, the limit of deduction under section 80G / 80GGC for donations made in cash is reduced from current Rs 10,000 to Rs 2,000 only.

If you want to donate some fund to a political party of your choice, you can do so in cash of up to Rs 2,000. Beyond that you can not donate the amount in cash mode. It can be done through Electoral Bonds.

Section 80GG

The Tax Deduction amount under 80GG is Rs 60,000 per annum. Section 80GG is applicable for all those individuals who do not own a residential house & do not receive HRA (House Rent Allowance).

The extent of tax deduction will be limited to the least amount of the following;

- Rent paid minus 10 percent the adjusted total income.

- Rs 5,000 per month.

- 25 % of the total income.

Section 87A – Tax Rebate

Individuals having taxable income of up to Rs 5 lakh will be eligible for tax rebate under section 87A up to Rs 12,500, thereby making zero tax payable in the old and new tax regime as well.

Section 80 TTA & new Section 80TTB

For Senior Citizens, the Interest income earned on Fixed Deposits & Recurring Deposits (Banks / Post office schemes) will be exempt till Rs 50,000 (FY 2017-18 limit was up to Rs 10,000). This deduction can be claimed under new Section 80TTB. However, no deductions under existing 80TTA can be claimed if 80TTB tax benefit has been claimed (the limit for FY 2017-18 & FY 2018-19 u/s 80TTA is Rs 10,000).

Section 80TTA of Income Tax Act offers deductions on interest income earned from savings bank deposit of up to Rs 10,000. From FY 2018-19, this benefit will not be available for late Income Tax filers.

- No TDS of up to Rs 40,000 on interest income from Bank / Post office deposits (the FY 2018-19 TDS threshold limit u/s 194A is Rs 10,000). Kindly note that no TDS does not mean no tax liability. Interest income on Deposits (FDs/RDs) is still a taxable income.

Interest income from deposits held with companies will not benefit under this section. This means, senior citizens will not get this benefit for interest income from corporate fixed deposits us/ 80TTB.

Section 80U

This is similar to Section 80DD. Tax deduction is allowed for the tax assessee who is physically and mentally challenged.

Standard Deduction of Rs 50,000

The Standard Deduction of Rs 40,000 for FY 2018-19 was increased to Rs 50,000 for FY 2019-20. The same is applicable for FY 2020-21 as well.

Related article : Treatment of Standard Deduction Rs 50000 under the New Tax Regime (FY 2020-21 / AY 2021-22)

Conclusion:

It is prudent to avoid last minute tax planning. Do not invest in low-yielding life insurance polices or in any other financial products just to save taxes. It is better you plan your taxes based on your financial goals at the beginning of the Financial Year itself. Plan your taxes now itself, instead of waiting until late December 2020 (or) January 2021.

As discussed, under the new tax regime, the individuals can opt to pay tax at the reduced rates without claiming the various tax exemptions and deductions.

So, you will have to work out your tax liability under the old and new tax regime before deciding which one is more beneficial. While the new regime seems simple on account of no exemptions, if you have already made commitment in recurring tax savings instruments, you may still want to avail exemptions and get taxed under the old tax regime.

You may this ‘compare Tax under old and new regime’ using this official online tax calculator provided by the IT dept e-Filing portal.

Kindly keep in mind – It is OK to pay some taxes when you can not save or cannot invest in right financial products. But, do not invest just to save TAXES. The cost of buying wrong financial products may outweigh the cost of taxes. Tax Planning is not a goal but a tool. Remember “Tax Planning alone is not Financial Planning.”

I believe that the above list is useful for your Tax Planning purposes. Kindly note that these Income Tax Exemptions are applicable for financial year 2020-2021 (or Assessment Year 2021-2022).

Continue reading:

- NPS Income Tax Benefits FY 2020-21 | Under Old & New Tax Regimes

- NRI Residential Status & Taxation (new) rules FY 2020-21 | Budget 2020

- Income Tax Exemption Vs Tax Deduction Vs Tax Rebate Vs TDS | Key Differences

- How Income Tax Department tracks the High Value Financial Transactions?

Join our channels

hello sir, very useful information is provided in the website.

I would like to know whether “remuneration paid for election duty” to govt employee is exempted from tax. If so please provide section details.

ITS BEST ARTICLE PLACE I FULL SATISFIED THANKS FOR THE ARTICLES I TOTALLY UNDERSTAND

An informative piece When should file 80c documents as employer ask in the beginiñg of FY BKDave