What is a Risk? – Risk implies uncertainty. It is the potential of gaining or losing something of value. In financial language, it is the chance an investment’s actual return can differ from the expected rate of return.

When we talk about an investment option, we have to analyze both Risk and Return. This applies to mutual fund investments too.

“ Mutual Fund investments are subject to Market Risks, read all scheme related documents carefully before investing! “

I am sure most of us might have come across above disclosure when we are watching TV, reading a news paper, or while investing in mutual funds.

What is this disclosure all about? – This is a regulatory requirement. Any mutual fund company has to include this disclosure as part of their marketing communication.

So, when a mutual fund company runs Ad campaigns for their mutual fund schemes, they have to mandatorily display this disclosure in their marketing material. This is as per SEBI’s (Securities Exchange Board of India) guidelines.

For example, in the below advertisement campaign by HDFC AMC, you can find the disclosure about the market risks.

AMFI has been aggressively promoting mutual funds as an investment/savings option (Saving ka naya Tareeka) in the last couple of years. At the end of these Videos (Commercials) you can notice the disclosure being displayed.

In this post let us understand – What are these Market Risks? What are Mutual fund Scheme related documents? Are mutual funds investments only subject to risks?

What are Market Risks?

Theoretically, risks can be classified as ‘Systematic Risk’ and ‘Unsystematic Risk’. Systematic Risk is also referred to as Market Risk or Un-Diversifiable Risk or Volatility. Whereas, Unsystematic risk is diversifiable risk or Specific risk.

For example : If there is a prolonged strike by Employees union of a particular company, then the shares of that company can be exposed to risk, which is UNSYSTEMATIC. This risk can be reduced through diversification. Systematic risk affects the entire market. It underlies all other investment risks. If there is a war or recession or a bad monsoon, it can affect the entire market and can not be avoided through diversification. At best, you can invest in such stocks which can withstand the impact in a better way.

What are Mutual Fund scheme related documents?

The the latter part of the disclosure – ‘Please read the scheme related document carefully before investing’ – is easier said than done. The reason being, these scheme related offer documents can run into tens of pages and have legal/financial terms, which may not be understood by a layman or retail investor.

The documents we are talking about are;

- Scheme Information Document (SID) : This document provides complete information about the scheme. It also has list of all other mutual fund schemes offered by the concerned fund house.

- Statement of Additional Information (SAI) : SAI contains all statutory information of the Mutual Fund house. It provides more detailed information about fund policies & operations.

- Key Information Memorandum (KIM) – Abridged document of SID & SAI

- Fund Factsheet : Analysis of returns with graphs and charts. If you have already invested in a fund, you can check the scheme’s progress and performance in the Fund’s Factsheet. Until Oct 2015, there was no standardized format. But from Oct 2015, the new factsheet format has been made effective and all AMCs have to provide the factsheets in the same format so that it is easy for the investors to go through them.

(These documents are available on respective fund house websites for each and every Mutual fund scheme they offer.)

Which document has detailed information on MARKET RISKs and various types of Risks? – SID has the information on various types of risks.

For example : Click here to download SID of Franklin Templeton Prima Plus Fund and kindly visit page numbers 4 to 7 to understand about Market Risks & unsystematic risks.

- Standard Risk Factors

- Scheme Specific Risk Factors

- Risks Associated with Equity investments

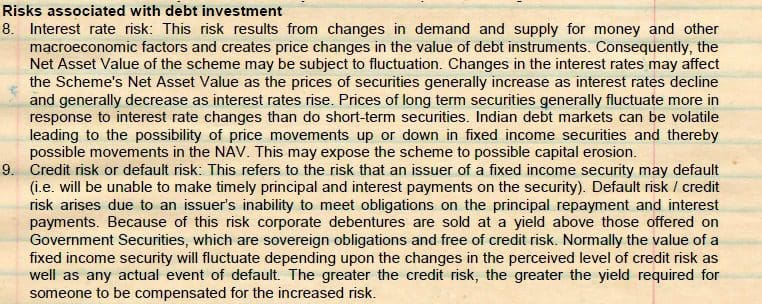

- Risks associated with Debt investments or securities and so on..

Mutual Funds are subject to Market Risks – My Opinion

I currently live in a small town in Andhra Pradesh. Last week, all the families in my apartment had a get-together party. During dinner time, I casually asked two of my neighbors – ‘what is your opinion on mutual funds?’. Both of them replied that they have not invested in mutual fund schemes till date.

One of them who is a doctor says that he has seen an MF ad and at the end of the commercial they say it is risky to invest in mutual funds. When they themselves are saying it is risky then why should we invest in mutual funds? He also said that it is like a Pharma company giving an Advertisement for a Tablet and highlighting the impact of SIDE-AFFECT prominently. This is the reply I got for my question.

Are mutual funds only subject to MARKET RISKS? What about other investments, are they free of risks? – in my opinion all investments carry certain amount of risk. Unfortunately, most of us equate RISK with ‘losses’ directly. We forget the fact that it is only a probability of losing and not actually losing.

Investing in a Land has its own set of risks. Even investing in Bank Deposits can be a risky affair, if bank goes bankrupt.

Saying ‘mutual fund investments are subject to market risks’ is way too generic. This sentence can scare a new or small-time investor to invest in a mutual fund scheme. This can create a negative perception about mutual fund products as a whole.

All mutual fund schemes are not one and the same. All mutual fund schemes do not necessarily carry same amount of risk. Many of us do believe that all mutual fund schemes invest in Shares only. It is a misconception. There are different types of mutual fund schemes – Equity, debt, balanced/hybrid, arbitrage etc.,

So, it is not the mutual funds that carry risk it is the underlying assets/investments that carry the risk. The mutual funds try their best to mitigate the risk (especially the un-systematic risks can be taken of by the fund manager).

In my opinion! The biggest risk is not taking risk at all.

So, instead of quoting ‘mutual funds are subject to market risks’, may be it’s wiser just to say ‘investments are subject to risks’, understand and manage them.

As Mark Zuckerberg (Co-founder of Facebook) says – ‘The biggest risk is not taking any risk… In a world that changing really quickly, the only strategy that is guaranteed to fail is not taking risks.’

(Read : ‘How to compare & select the right Mutual Fund scheme based on Risk Ratios?‘)

Kindly note that this post is for information purposes only. ReLakhs.com is not associated with any of the companies mentioned in the above article. (Image courtesy of bplanet at FreeDigitalPhotos.net) (Post published on : 16-September-2016) (References: moneycontrol.com & Video Courtesy :AMFI)

Join our channels

What is your investment plan sir shrikant reddy?

Dear RANJEET ..Are you referring to my investments in Mutual funds?? You may go through this article..

sir,

How is motilal oswal mutual fund

one of my friend suggest me not to purchase any mutual fund through banks as it deduct charges,better to purchase from direct company.

In my case, i am using axis bank. is it a wise solution.

Dear RANJEET .. Your friend is referring to Direct plans of Mutual fund schemes. Suggest you to go through below articles ;

What are Direct Plans of MF schemes?

Direct plans Vs Regular Plans – Returns

MF Utility online platform for Direct plans

Dear sree,

Can you guide us what factores need to be consider while selecting a mutual fund, like expese ratio etc and theie ideal values…… also how is rebalacing done…please

Dear Abhee,

Kindly read: How to select the right mutual fund scheme?

You have to identify your ideal Asset allocation and check your current allocation.

To meet your expected allocation ratio, you may have to sell/buy the securities/units accordingly.

Thanks Sree!!!

I read the above article its Really Good. I just wanted to know the IS THIS THE ONLY METHOD TO SELECT THE MUTUAL FUND? ASLO CAN I CHOOSE MUTUAL FUND FOR MYSELF BASED ON THESE FACTOR?

Also if i wanted to take a mutual fund for 30 year expecting 12 % CAGR, do i need to rebalace it in that time frame?

Dear Abhee,

The points mentioned in the suggested article are ‘major risk stats’ that one can consider when shortlisting a mutual fund. You may follow your analysis.

Yes, you may rebalance your Portfolio based on your target goal amount, time-frame and allocation ratio.

Thanks

Dear Sreekanth,

What happens to the dividend amount issued by the Stock/Company in which Mutual Fund has invested? Does it goes to AMC directly and shown to the investors as expense ratio or gets added to the NAV of the fund and leads to increase in NAV?

For Eg: If Infosys declares dividend of Rs 2 per share and and ICICI MF (Growth option) holds the shares of Infosys then will the NAV of ICICI MF increases or goes to ICICI AMC as charges?

Based on your option chosen, Re-investment or payout: it will be re-invested in the same MF or paid out respectively. During payout, respective charges are also cut. Unless you are a NRI, the TDS is not cut. However, you will need to show tax during filing,

Dear Mak,

If you look at how NAV is calculate;

Net Asset Value (NAV) = (Assets – Debts) / (Number of Outstanding units)

Here Assets are referred to as : Th total asset value of a fund will include its stocks, cash and bonds at market value. Dividends and interest accrued and liquid assets are also included in total assets.

Thank you Sir, really appreciate the lucidity of your explanation and promptness of response.. Greatful.. Big fan of your articles..

Dear SriKanth,

It’s really great to your website.

I am 38 years old, working professional,married, and having 2 sons, 8 years old and 3 years old.

Having home loan – 35 Lakhs – 52k EMI/month

Educational Loan – 4 lakhs -10k EMI/month

My salary is 80k/month and family expense is 15k per month.

Before plan any savings for further and future expenses, i would like to clear the home loan.

And currently i am having 10lakhs savings amount and wanted to invest in MIP-Aggressive so that i can nearly get 50k month in which i can clear my home loan slowly in another 2 years with other support.

Is that a right option, please advice if you have any other option.

Thank you

Regards.

Vel

Dear Vel,

What is the rate of interest on your home loan?

Are you claiming the interest on education loan as tax deduction u/s 80E?

Have you planned and allocated sufficient savings for your high priority goals like Kids’ education & Retirement planning? If no, you may continue with your home loan and you may invest for these goals instead.

Read:

Kids’ education goal planning & calculator.

Retirement planning calculator.

List of articles on Personal Financial planning!

Thanks for your reply sir.

rate of interest 10.15% and taken the loan in SBI. outstanding loan as on date 35laks.

Yes. i am claiming the educational loan interest paid for tax benefits.

In this situation, is it a good option to invest the 10 lakhs in hand in to Aggressive MIP or any other good plans will you please suggest. I would like to get monthly returns.

Please advice. Thank you.

Dear Vel..If I understand you correctly, would you like to receive monthly income from this Rs 10 Lakh investment? If yes, what would you do with this income? For consumption or re-payment of home loan??

As mentioned in the my previous comment, if you have not planned for your other high priority goals you may use at least some amount for long-term investment and some portion of corpus for repayment of home loan.

Yes sir. you are right. I would like to use the monthly income from this 10 lakhs investment in to repaying home loan as a first priority….then some amount in to other long term goals.

Please advice.

Also, I don’t know which aggressive MIP is performing good….will you please name few of them sir.

Thanks.

Dear Vel,

Suggest you to allocate some money to long-term goals and then if any remaining amount, can be allocated for home loan repayment.

Aggressive MIP fund ex – Birla Sun Life MIP II Wealth 25 Plan.

You are almost hand to mouth – 80K Salary and 75K Outflow. How much is your Education loan effective interest? If it is greater than your savings account, then use the 4 lakhs from your 10 Lakhs savings to clear off the Education Loan. You can use this 10K p.m to increase the Home loan pre-payment to close off your Home loan faster.

Dear Srikanth,

I want to invest 5 L in two MF – ICICI Pru Value Discovery Fund & DSP Micro Cap Fund equally. Could you suggest me good procedure mean whether in Lump sum in one go or can I spread this amount in 12 equal installments into the said funds. Pl. guide me.

Thanks,

Harinath

Dear harinath ..May I know your investment time-frame?

It is long term (9+ Years) for my child education. Or could you suggest me other funds / investments. Actually this amount I am getting from sale of village agriculture land. I sold it for 5 L . But govt. market value is 2.8 L only (Registration value). If they transfer 5 L to my account, how can I show in my income tax returns (Means here white is 2.8 L & Black is 2.2 L). Shall I ask purchaser to make bank transfer for 2.8 L & balance 2.2 L in cash. Pl. guide me.

Dear harinath,

You may opt for STP from respective fund house Liquid fund to Equity fund.

If you have sufficient income inflows (through salary or other sources) then you can accommodate this investment. Else, you may request the buyer to pay full amount in White.

Read:

Income from Agricultural land.

Best Liquid funds.

Very useful article for people who think only Mutual Funds are subject to market risks!!!

However, the fact is every “investment” is subject to one or other type of risk attached to it be it Market risk, credit risk or re-investment risk etc.

Sir, I would like to ask a question about joining Mutual Fund as a distributor. Last month, I cleared MF distributor Exam (VA) and have applied for ARN from Amfi.

After getting ARN, do I compulsorily need to apply individual AMC of Mutual Fund for empanelment ? What are the chances of them approving my distributorship if I don’t have a client base?

Or can I join NJ Wealth, FundsIndia etc. as an associate so that I can promote schemes of many Mutual Funds under one roof (without applying as distributor of individual AMC of MF)? Is it possible?

I am confused as to what is the correct approach.

Thanks

Dear Rupali,

It is not compulsory. It is your choice based on your business strategy and interest.

They (AMCs) will be more than happy to approve your application.

If you join service providers like NJ or Fundsindia, the main benefit would be ease of doing business, you can provide multiple investment options to your prospective clients, can scale up your business with low cost but at the cost of lesser commission.

I believe that if you are in metro city, the future is DIRECT plans. So, be careful in planning your career/business. You may provide bouquet of investment options for your clients.

If you would like to charge fees (advisory fee) for providing your service then you may have to give up commissions on the products. One can’t receive both fee and commissions. (I am sure you are aware of SEBI’s Investment Advisor rules).

Thank you sir for your valuable inputs.

However, I still have one doubt.

Is it mandatory to be SEBI registered Investment Advisor? I don’t think so.

Is it not possible to get commission from products sold to clients who are reluctant to pay for financial advice? Since there are many customers who fall in this category. If I don’t get myself registered as RIA, I may charge fees from customers who are ready to pay for advice and commission from customers who are not ready to pay for advise.

Is my understanding correct?

Please reply

Dear Rupali,

Kindly note that tt is mandatory to register with SEBI as an Investment Advisor, if you wish to charge fees to your clients. Once you are a registered IA, you are not supposed to take commissions on products.

You may kindly go through below links on this topic;

Link 1.

Link 2.

Rupali,

My advice will be to go join the service providers as you will get wealth of knowledge and the feel of what customers are taking / needed. Later – I think you can change after 1 or 2 years and take your stance whether you want to be advisor or distributor. FYI, most of the new investors are getting knowledgeable and opting for Direct funds. Even the existing customers who used to maintain REGULAR type (from Banks) are directly contacting the respective AMCs and getting it converted to DIRECT. With what I have seen, AMCs are not charging any penalties if you just change from Regular to Direct.

Continuing from my previous post. This DIRECT switch benefits the investors but if you are a Distributor than your commissions will go away. The best strategy in my opinion is to make friends and establish reputation as an Advisor. This will help you get client who will see you as transparent advisor and may stick with you for long term. They may also suggest their friends family who will also be likely to stick around.

It is very clear that in long run most will know about this DIRECT funds and will shift to it. The difference in some funds is as high as 1.5 % (Birla Sun Life Pure value for example)

thanks both of you for kind advice.

Sir currently I’m having surplus of 2 Lakh rupees which I want to invest in Equity mutual funds.. But as market is on high do not want to invest now..is my desicion right?? If no then what would I do with this.. Thank you

Dear Rohan ..Kindly refer to our email conversation 🙂

Dear sir,

My age is 27 yrs and I have started investing 2 years back,i am currently investing 50000 pa in ppf for the last two years.recently I have started some sip like

1.dsp black rock midcap(g)-2000 pm,

2.icici value discovery fund-2000pm,

3.hdfc midcap opportunities fund-3000pm,

I want to take my investment in sip pm to 15 k

Q1-I want to get more than 2 crores at the age of 50,which is my retirement age as I want to enjoy with family after that time,currently I am single.

Q2-should I continue in ppf or should I go for less schemes for tax benefits?

Note-i have taken a term plan of 50 lakhs for 30 years which has started just now.

Dear Manish,

Q1 – Kindly use the calculator available in this article : Retirement goal planning made easy!

Q2 – PPF is one of the best tax efficient long-term savings option (in debt category). You can continue it. But the amount of investment in PPF can be dependent on the required amount of savings for your long-term goals like retirement. If you are falling short then you may increase your allocation to equity mutual funds (can consider ELSS for tax saving too).

Sometimes, people also take too little risk. Like all the investments in liquid / ultrashort funds as their friends would have told them that it is the best mutual funds with lowest amount of risk. After few years they realise that their investments are no better than the fixed deposits or worse. I think biggest myth of risk is because people don’t read enough. If they read, they are influenced by so called agents who constantly induce fear about mutual funds and only promote those which are beneficial to them.

No risk no gain is a saying that holds good always. How much more or how much less, only an individual should decide,

Dear Manja,

Valid point!

Investing in a low risk profile products like FDs/Debt funds results in ‘not achieving the desired goal corpus amounts’.If one invests in wrong product without considering the impact of taxes/inflation then the probability of falling short of goal amounts is 100% or very high.

Dear Shreekanth

Invested in HDFC balanced fund lump sum, wants to invest more, whenever possible in the same fund. I will stay invested 10+ years. I have registered online, can I buy online and is it possible to redeem partially whenever need arises?

( I wish only after 10+ years)

Dear Didagur ..Yes you make partial redemptions too. Yes, you can buy online by visiting HDFC AMC website.

Read:

What are Direct Plans of Mutual fund schemes?

Best Balanced funds.

Thanks! for such an article. Really gave more awareness and knowledge about MFs. I have below SIP mutual fund. Please let me know if my portfolio is gud or anything needs to be changed

1)Axis long term equity ELSS 3k per month

2)Franklin long term equity 3k per month

3)DSP Blackrock micro chip 2k per month

4)ICICI pru value discovery 2k per month

5)Birla sunlife frontline equity 2k per month

6)Tata Balanced fund 2k per month

I know 1 & 2 are overlapping after reading your blogs.Please let me know how to improve my portfolio.If anything i need to add or remove from my portfolio.

Dear Rakesh,

If the overlap is on a higher side lets say >50%, then you may keep one fund.

Your portfolio looks fine and stay invested for long-term.

Is DSP Blackrock better than Franklin small cap and mirae asset emerging blue chip ? or shall i change in small cap MF. I need one gud large cap fund and one gud debt MF. Could you pls help me on the same

Dear Rakesh,

Kindly go through below articles;

How to select the right mutual fund scheme based on risk ratios?

Best Equity funds.

Great Shreekanth !!

You are doing a great job by spreading financial awareness.

Suppose I start SIP and then stop and accumulated 100units @ 10rupee face value,I stay invested for say another 5 yrs but without investing(SIP) or redeeming it. After 5 years I want to redeem but NAV is 15 so will I get 15 for my each accumulated unit?

kindly clarify

Dear Didagur..Yes you will get the NAV as applicable on the redemption date.

The biggest risk is not taking any risk…..This statement reminds me of the speech made by the CEO of Nokia in which he said “we didn’t do anything wrong, but somehow, we lost”.

Dear JJ..Nice share. There are plenty of examples like Nokia w.r.t our domestic market too. Ex – Ambassador car makers.