Agriculture is the main occupation in India. Two-third of India’s population is dependent on agriculture either directly or indirectly. Agricultural income is exempt under the Income Tax Act. But, is this provision holds good even if you have other sources of income? Let’s discuss..

In this post let us understand – What is an Agricultural Land? What is considered as Agricultural Income? What are the scenarios where Agricultural income is exempted from income tax? What are the scenarios where income from Agriculture is considered for calculating your tax liability? How to calculate income tax on Agricultural income for Tax Year (FY) 2026-27? What are the tax implications on sale of agriculture land? How to save capital gain taxes on sale of Agricultural land under Section 54?

What is an Agricultural land?

Any land used for agricultural purpose shall be treated as agricultural land. It can be situated in rural area or urban area.

What is considered as Agricultural Income?

To be classified as an Agricultural income, the following two conditions must be satisfied;

- The income should be derived from land situated in India (urban or rural area) and

- The land should be used for agricultural purposes only.

Agriculture income can be in the form of

- Income derived from agricultural land through cultivation or agriculture.

- Any rent or revenue received from tenant or sub-tenants of agricultural land.

- Income received from sale of agricultural produce.

- Income derived from saplings or seedlings grown in a nursery.

- Income from Farmhouse subject to certain conditions. Income from Farmhouse can be treated as Agricultural income if ;

- The farmhouse is occupied by the cultivator or receiver of rent from land.

- The farmhouse is located in the immediate vicinity (near) of the agricultural land.

- The farmhouse is used as storehouse or out-house or dwelling house. But, if the income from farmhouse is through letting out for residential purposes or for any business purposes, such income is not an agricultural income.

Is Agricultural Income exempted from Income Tax for FY 2026-27?

As we are clear about what is an agricultural income, let’s now understand the scenarios where income from agriculture is totally tax-exempt;

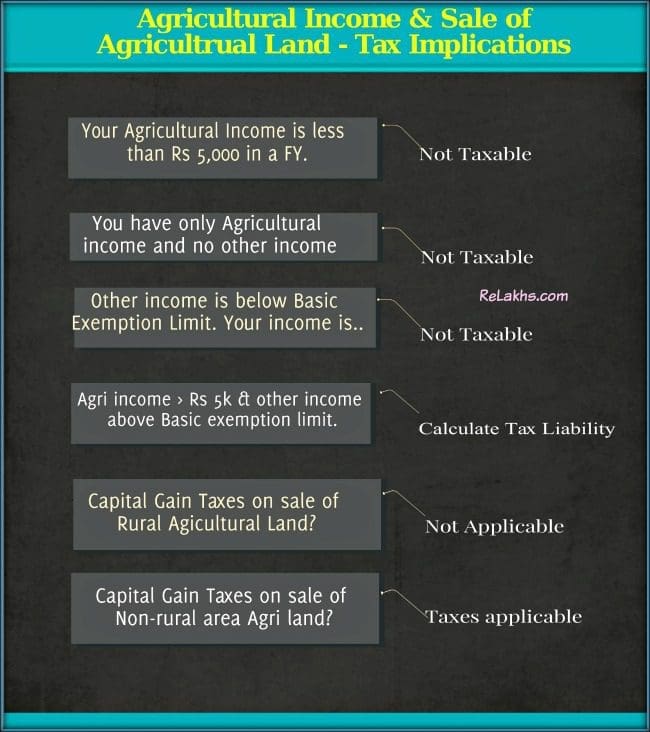

- If your agricultural income is less than Rs 5,000 in a Financial Year, it is tax free.

- If agriculture is your only source of income, such income is tax exempt.

- If you have agricultural income and also have other income from salary/business , and the total income excluding agricultural income is less than basic income exemption limit then there will be no tax liability.

For the Tax Year 2026-27, the basic exemption limit under the old tax regime is Rs 2.5 lakh (Rs 3 lakh for Sr. Citizens) and for the new tax regime it is Rs 4 Lakhs.

How to calculate Income Tax on Agriculture Income Tax Year 2026-27?

What if your agricultural income is more than Rs 5,000 and if you also have income from salary / business / profession which is above the basic exemption limit?

In this scenario, your agricultural income has to be added (included) to the total income while calculating the tax liability for the given Tax Year (FY).

Below is the procedure to calculate the tax liability by taking Agricultural income into account;

- Step 1 – Add Agricultural income and other sources of income.

- Step 2 – Compute income tax (A) on the above aggregate income as per the applicable income tax rates.

- Step 3 – Add Agricultural income to the applicable basic exemption limit.

- Step 4 – Compute income tax (B) on the above aggregate income at the income tax rates prescribed.

- Step 5 – Income tax liability is A – B.

Let’s understand this with a simple example. Mr Reddy (35 years) is having Business income of Rs 4,00,000 and net agricultural income of Rs 90,000/-. What is the income tax liability of Mr Reddy for TY 2026-27, under old tax regime.

In the above scenario, the agricultural income is above Rs 5,000 and the other income is above the basic exemption limit. So, we need to include agricultural income to total income when computing tax liability.

- Add Agricultural income and other sources of income. Aggregate income = Rs 4,00,000 + Rs 90,000 = Rs 4,90,000.

- Compute income tax (A) on the above aggregate income as per the applicable income tax rates. Income tax liability on Rs 4.9 Lakh is Rs 12,000. (Up to Rs 2.5 Lakh no tax and tax @ 5% on the remaining Rs 2.4 Lakh. Education cess ignored.)

- Add Agricultural income to the applicable basic exemption limit. Aggregate income = Rs 90,000 + Rs 2.5 Lakh = Rs 3,40,000.

- Compute income tax (B) on the above aggregate income as per the applicable income tax rates. Income tax on Rs 3.4 Lakh is Rs 4,500. (Up to Rs 2.5 Lakh no tax and tax @ 5% on the remaining Rs 90,000. Education cess ignored.)

- Mr Reddy’s income tax liability is Rs 12,000 – Rs 4,500 = Rs 7,500.

- Please note that Rebate u/s 87A, surcharge, Cess will be applicable in addition to the tax calculated. Standard deduction is applicable for salaried individuals.

So, it is clear that even though agricultural income is exempted under IT act, in actual practice it is not the case. Also, if you are in say 20% tax bracket, addition of agricultural income may take you to 30% tax slab rate. So, agricultural income is considered for determining the applicable income tax slab rate.

Income tax implications on Sale of Agricultural Land 2026-27

Land is a capital asset. Capital asset typically refers to anything that you own for personal or investment purposes. It includes all kinds of property; movable or immovable, tangible or intangible, fixed or circulating.

When you sell a capital asset, the difference between the purchase price of the asset and the amount you sell it for is a capital gain or a capital loss. Capital gains and losses are classified as long-term or short-term.

So is Agricultural land a Capital Asset? Do you need to pay income tax on sale of your agricultural land?

If your agricultural land is in rural area, such land is not treated as Capital asset and hence no capital gain taxes are levied. Agricultural land in Rural Area India is not considered a capital asset. Therefore any gains from its sale are not taxable under the head Capital Gains.

Definition of Rural Area as per Income Tax Act – Any area which is outside the jurisdiction of a municipality or cantonment board having a population of 10,000 or more is considered Rural Area, if it does not fall within distance (to be measured aerially) given below;

- 2 kms from local limit of municipality or cantonment board and If the population of the municipality/cantonment board is more than 10,000 but not more than 1 lakh.

- 6 kms from local limit of municipality or cantonment board and If the population of the municipality/cantonment board is more than 1 lakh but not more than 10 lakh

- 8 kms from local limit of municipality or cantonment board and If the population of the municipality/cantonment board is more than 10 lakh.

So, if your agricultural land falls in Urban Area (non-rural area) then Capital Gain Tax is applicable.

Capital Gain Tax on Sale of Urban Agricultural Land (non-rural area)

If Agricultural Land is held for 24 months or less then that Asset is treated as Short Term Capital Asset. You, as an investor will make either Short Term Capital Gain (STCG) or Short Term Capital Loss (STCL) on that investment. Short term capital gains on Agricultural land will be taxed as per applicable income tax slab rate.

If Land is held for more than 24 months (w.e.f. FY 2017-18 / AY 2018-19) then that Asset is treated as Long Term Capital Asset. You will make either Long Term Capital Gain (LTCG) or Long Term Capital Loss (LTCL) on that investment. (Read : ‘How to calculate Capital Gains on sale of Land?‘)

| Land Type | Tax Status & Rate | Indexation Benefit | Tax Saving Options? (Sec 54B, 54F, 54EC) |

| Rural Agricultural Land | Exempt (Zero Tax) | Not Applicable | Not Required |

| Urban Agricultural Land (Held > 2 Years) | 12.5% Tax | No (Removed) | Yes (Can reduce tax to zero) |

How do I save Capital Gains tax on sale of Urban Agricultural Land 2026-27?

You can claim below deductions to lower the tax liability on capital gains of sale of Agricultural land;

- Deduction Under Section 54B

- If you sell an agricultural land and make capital gains, you can re-invest such gains in acquiring another agricultural land. You have to buy another agricultural land within 2 years.

- This deduction is available only if you/your parents have been using the agricultural land for a period of two years prior to date of transfer (sale). (Exemption U/s. 54B on Sale of agricultural land available even if land is cultivated for a part of year during two immediately preceding years.)

- The new agricultural land that is acquired should be held by you for atleast 3 years from the date of purchase.

- Deduction under section 54F

- With effect from Assessment Year 2024-25, the Finance Act 2023 has restricted the maximum exemption to be allowed under Section 54F. In case the cost of the new property (capital asset) exceeds Rs. 10 crores, the excess amount shall be ignored for computing the exemption under Section 54. Up to FY 2022-23, there was no tax exemption ceiling limit u/s 54F.

- If you sell land and make long-term capital gains, you can re-invest the sale proceeds to purchase a residential house within 1 year before or 2 years after from the date of sale of land or you should construct the residential house within 3 years from the date of sale.

- You should not own more than one residential house on the date of transfer of land.

- Deduction under section 54EC

- If you sell agricultural land and make long-term capital gains, you can re-invest Capital Gain amount to purchase NHAI or REC bonds within 6 months from the date of transfer.

- The maximum allowed investment is Rs 50 Lakh.

- The bonds should not be sold/transferred for 3 years.

- The capital gains can also be deposited in Capital Gains Account Scheme of any designated banks. With effective from 1st April , 2023 (i.e. A.Y. 2024-25), Capital gain of upto to Rs. 10 Crore can be deposited in CGAS.

Important Points & FAQs on Agricultural Income & Sale of Agricultural Land

- The Central Government can’t impose or levy tax on agricultural income. The exemption clause is mentioned under Section 10 (1) of the Income Tax Act of India. However, state governments can impose tax on Agricultural income.

- Under Section 10(37) of the Income Tax Act, Capital Gains on compensation received on compulsory acquisition of urban agricultural land is exempt from tax. This exemption is available if the land was used by the taxpayer (or by his parents in the case of an individual) for agricultural purpose for a period of 2 years immediately preceding the date of its transfer.

- Is rebate 87A applicable on agricultural income? – Yes. The resident individuals earning from agricultural income sources are eligible to claim tax rebate under section 87A.

- I have agricultural income as the only source of income, should I file income tax return? – It is not required to file IT returns if agriculture is your only source of income. But filing Income Tax Return has its own advantage so you may consider filing your taxes.

- Is 1% TDS on sale of agricultural land is applicable? – 1% TDS is not applicable on sale of Agricultural land.

- I have Agricultural income of more than Rs 5,000, which ITR form should I file? – Agricultural revenue should be reported in ITR 1 under the Agriculture Income column. However, ITR 1 can only be used if your agricultural income is less than Rs 5,000. If the stated income exceeds this limit, form ITR-2 must be filed.

- Can I carry forward capital losses? – Yes, capital losses from agricultural operations can be carried forward and set off with agricultural income of next eight assessment years.

- I am a sub-tenant or tenant of agricultural land, is my agricultural income tax-free? – Kindly note that ownership of land is not essential. All tillers of land are considered as agriculturalists and enjoy exemption from tax.

- Income from trees that have been cut and sold as timber is not considered as an agricultural income since there is no active involvement in operations like cultivation and soil treatment.

- Dairy / poultry Farming, income from supply of water for irrigation purpose, income from sale of earth for brick-making, rental income from Farmhouse given for non-agricultural purposes etc., are not considered as an agricultural income.

- Is Agricultural income taxable for an NRI in India? – NRI’s cannot purchase agricultural land, plantation or farm land in India. If an NRI is willing to purchase agricultural land in India, it requires permission from the Reserve Bank of India for doing so. However, NRIs can inherit and hold agricultural land. Any agricultural income derived from such land is tax exempt. (While this type of income is exempt from tax, it is nonetheless included in the total income for arriving at slab rate purposes.)

- Is foreign agricultural income tax exempted? – Foreign agricultural income is not entitled for exemption and it is chargeable to tax under the head ‘income from other sources’.

I have tried my best to provide all tax related matters of Agricultural income & on sale of Agricultural land in a simple and easy to understand manner. Hope this is useful!

Do you believe that agricultural income should not be exempted from income tax? Is agricultural income one of the root causes of generation of domestic black-money? Kindly share your views and comments. Thanks!

Continue reading:

- How Salary + Agricultural Income Affects Your Income Tax (Partial Integration Rule Explained)

- Capital Gains Tax Exemption Options on Sale of House or Plot | Latest Rules

- Income Tax Deductions FY 2026-27: Complete Guide to Old vs New Tax Regime

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net) (Post first published on : 09-June-2016) (Updated on 16-July-2026)

Join our channels

The information provided is in simple terms ,with clear illustrations and a prudent person can have basic information on capital gains and its repercussions. Thanks Mr Sreekanth Reddy and his team on this advisory.

C.Janardhan Reddy

Hyderabad.

Dear Janardhan,

Thank you for your appreciation.

Keep visiting ReLakhs!

Very Nice Explanation Sir Truly Appreciable and no comments on it. Thanks for Sharing.

Thank you for the appreciation dear Suryanarayana.

Keep visiting ReLakhs!

My uncle is having 10 acres of rural agricultural land which is 25 kms., away from the nearest municipal limits. One real estate developer approached my uncle to sell the land for him to sell as plots after getting the layout approved from the authorities. He is proposing to give me certain plots as consideration for the sale of agricultural land. Is it taxable? He is asking me to register the plots to the buyers of the plots.

Dear Siva,

Suggest you to kindly consult a CA/Lawyer in this regard and then take decision..

Sir , my father age is 64 years .He is having 15 Marla agriculture land and selling it … Authorities are saying that for this sale Registery would on commercial basis ….. Will this affect my father’s tax implications …Or captital gain be considered as agricultural one or commercial one …Kindly suggest in detail

Dear Samdip,

May I know, what is Marla agriculture land?

Kindly go through the points given in the article as to what is considered as a rural Agri land.

if your agricultural land falls in Urban Area (non-rural area) then Capital Gain Tax is applicable.

You may kindly consult a local civil lawyer as well..

Sir marla refers to size of plot

There are 160 marlas in one acre of land …

This land comes under rural agriculture land …. but buyer wantes it to have register it as commercial land purchase.

My confusion is that if the registration is done as commercial land ..will it have tax implications on seller (my father) in this case

Dear Sandip,

Suggest your father to sell it as a rural Agri land, if it is so, there won’t be any tax applicable.

You can sell it as rural Agri land and let the buyer convert it to commercial usage based on applicable rules & regulations.

Kindly consult a civil lawyer..

Is there any rule like if the area of sold agriculture land is small (below 34 Marla ) then it will be registered as commercial land ….kindly confirm …..As the person who will prepare registration documents is telling me the above …

Thank you in advance for ur valuable response…

Dear Sandip,

I am not sure if there is any such rule. Do note that the law vary from State to state. Plz consult a civil lawyer and do not entirely believe the Agents/Document writers.

Hi Srikanth, i have bought 20 cent agriculture land with amount of 15Laks and now i converted that land into layout and i paid the conversion charges and land comes under major panchayati limit and i will be planing to sell 2 plots out of 3 plots, each plot cost as 15laks, so is it taxable on 2 plots cost (30 Laks) . Please suggest.

Dear Srinu,

If your holding period is less than 2 years then you have to taxes on Short term capital gains (if any).

if it is more than two years also, do i need to pay tax

Dear Srinu..Yes..

Kindly read : How to save Capital Gains Tax on Sale of Land / House Property?

Hello Sri,

One of my friend sold his agriculture land in rural area for more than government value and he is planning to invest entire amount in the fixed deposit of the bank.

He sold his property for 80 lakhs (market value) but government price was 20 lakhs.

Here I need your assistance for below queries

1. Does he need to pay tax for entire 80 lakhs? Or it is exempted as it is rural agriculture land?

2. After investing in FD’s, does he need to file income tax return for 80 lakhs. And also does he need to file every year.

3. If he need to file income tax return then what link he need to follow to do this.

4. Does he need to pay any other taxes while fixed depositing in bank.

5. What precautions need to be taken before investing entire amount in fixed deposits, if any.

He is not willing to work in bpos due to serious health issues.

Thank you in advance.

Regards,

Prabhakar.

Dear Prabhakar,

1 – Is the Sale Deed done for Rs 80 lakhs or Rs 20 lakhs? It is a tax-exempt income. But, suggest him to file his Income Tax Return and disclose this exemption income in his ITR (can declare this under Exemption income section of ITR)

2 – The interest income on FDs is a taxable income. So, if his income is above the basic exemption limit then he has to file his ITR.

Related articles :

* Income Tax Slab Rates for FY 2019-20 / AY 2020-21

* Do I need to file my Income Tax Return?

3 – I did not get your query..

4 & 5 – Is the Sale Deed done for Rs 80 lakhs or Rs 20 lakhs?

Hi Sri,

Thank you for your answers.

The sale deed consideration done according to government value i.e., for 20 lakhs.

Related to 3rd question, I got answer in your first answer.

I am seeking your advise on 4 and 5 questions. Please help on this.

The sale deed consideration was done for 20lakhs as per government value.

Dear Prabhakar,

If the Registered value is just Rs 20 lakhs then he may have tough time to deposit the remaining amount ie Rs 60 lakh, as it is not a white money.

Even if he deposits, he may get a tax notice from the IT dept inquiring about the Source of these funds..

Related article :

How Income Tax Department tracks the High Value Financial Transactions?

Thank you Sri, I will inform my friend the same.

I am a salaried Govt. Employee and have taxable income. I inherited 3 bighas of Rural Agricultural Land(Falling under Exempt Income category on it’s sale as per land use, character and distance and population from a Municipality etc.) after the decease of my father. Now I intend to sale the land for Rs. 6 Lacs. Is the sale proceeds taxable in my hand?

Dear BIKAS,

It is tax-exempt in your hands.

Does the construction/purchase of residential house in village eligible for deduction under section 54F

Dear Dharmendra,

Are the proceeds used to buy this house property from the sale of Agri land?

If so, yes, its eligible.

Kindly refer to the points given in the article.

Hi..

I have bought agriculture land in rural area at cost Rs. 500000 in july 2018, now i m selling this land in January 2019 at consideration at Rs. 1200000..so i have to pay any tax??

Dear Amit,

Agricultural land in a rural area in India it is not considered a Capital Asset, and therefore no capital gains are applicable on its sale.

Dear Sreekanth, if agriculture land is sold with teak and sandalwood trees in the land, would the taxation be any different for the seller? Thank you.

Dear Ram,

There are no clear rules reg. this.

However, Income from trees that have been cut and sold as timber (or sandalwood/teak) may not considered as an agricultural income since there is no active involvement in operations like cultivation and soil treatment.

You may kindly consult a CA.

Kindly go through this article..

Thank you very much Sreekanth. The article you pointed to helps.

Hi,

Good Day.

Would appreciate if you can throw some light on my below Queries. Thanks in advance for your support.

i) Is there any upper cap on exempting the Tax for the Amount received on the sale of Agricultural Land in rural area.

2)Which documents evidences the land as Agricultural category.

3)Can the registration amount/Land cost be more than the actual Government rate in this case.

4)To be specific, I have a land in Mudimyal village( Chevella Mandal, Rangareddy Dist). Is it considered as Rural or Urban area? Also,

Can I have the registration amount as 30 Lakhs, while the actual Govt value(circle rate) of the land is 10 Lakhs.

5)If the said land is not considered as capital gain, I believe the whole 30 Lakh is non taxable. Please advise.

Dear Raj,

1 – No.

2 – The classification of the land can be ascertained from Setwar/RSR, Pahani/Adangal, IB register, Pattadar Pass Book and Title Deed. Can get the details from the concerned Village Revenue office / Panchayat office.

Mutation details should be checked in ‘land revenue records’ as it (mutation) is mandatory for Agricultural lands.

3 – Yes, it can be..

4 – Kindly inquire at local Panchayat office. Plz refer to the pointers given in the above article as well (Definition of Rural area).

5 – Yes, if it is an agri land.

Dear Sreekanth,

Thanks for your feedback.

Any idea if land under G.O 111 will be excluded from this tax exemption?

Dear Raj,

I do not have an idea about GO 111 (which can be State specific). You may kindly consult a civil lawyer..

Mr Reddy,

Thank you for a very detailed but simple explanation. Can you please advise me on the following issue:

I worked in India for 10 years. Out of my savings I bought a piece of AGRICULTURAL LAND while being a resident.

Subsequently I moved abroad for a job. I am an NRI but file my income tax return regularly because I have some source of income in India.

The agricultural land (in RURAL AREA) has been in my name for 5 years. Now I wish to dispose it off. After indexation there may be some gain. Please advise if I have to pay any income tax on capital gain as an NRI which I need not have paid as a resident.

Dear Mr Dahiya,

Agricultural Land in rural area is not a capital asset and no capital gains shall arise on transfer of such land.Such exemption is covered under section 10(37) of the income tax act, 1961.

Hence there will no capital gains on this sale.

Moreover, this is exempt irrespective of the residential status of the owner. Thus, even if you become NRI, the sale would be exempt from taxability.

A certificate under 197 can be availed from the Income tax Department for Not deducting Tax.

Related articles :

* Residential Status – NRI or Resident? & NRI Taxation

* What is Double Taxation Avoidance Agreement (DTAA)? | Is Income earned outside India Taxable?

I am selling my agricultural land in rural area (Nilgiris), i am spending 50 % of the amount to buy an apartment in city (coimbatore) the balance amount of 50 % to be deposited as FD mode for safe monthly/quarterly payout mode of interest, this interest they (Bankers) deduct 10 %.

I am filing income tax hereafter. Is there any other govt rules i have to face in future ?

Dear Bala,

May I know your exact query?

Sir, I am going to sell my Agricultural land (having one unused old stone house) at Nilgiris in a rural area. The amount i am getting from the sale to be used as 50 % in safe Bank FD, the balance 50 % to buy an apartment at Coimbatore city. Since I heard there is no tax on sale of agri land, is there any other tax i have to face ? I would be very grateful to you, if you could answer this, because i am little bit worried. (50 % buying property and balance 50 % deposit in FD, the quarterly payout mode, the interest i am getting as 10 % taxable) Beyond this i need your suggestion. Till date, i am having pan card but no IT filing since i am doing agriculture.

Dear Bala,

Kindly note that the sale proceeds realized from the sale of Agri land is not subject to taxes.

You can buy a Flat.

The interest income earned on FD is a taxable income. You have to file your Income Tax Return.

Related articles :

* Do I need to file my Income Tax Return?

* Recurring Deposit Taxes & Fixed Deposit Taxes – How do they work? (RD & FD)

Sir, I’m planning to buy a rural agricultural land, & deal is undergoing below circle rate. It is clear from your blog that capital gain will NOT attract to seller being rural agricultural land. Can you please give guidance on buyer’s perspective for below circle rate registration, will the difference be taken as income from other sources or it will not attract being rural agricultural land ??

Dear Ashish,

If the property is a rural agri land, it will not attract any taxes..

I am a teacher my own agricultural land is in rural areas. I want to sale it now.

Please tell me if it is necessary to file the tax. I have only one acre

Dear Nitin,

If your agricultural land is in rural area, such land is not treated as Capital asset and hence no capital gain taxes are levied. Agricultural land in Rural Area India is not considered a capital asset. Therefore any gains from its sale are not taxable under the head Capital Gains.

However, you can just file your Income tax return disclosing this exempted income, so that you can avoid any tax notices.

I am purchasing an agriculture land at a price lower (~5 lacs) than the guideline price, in a village which is 15 KM away from the nearest municipal corporation. Kindly advice if I have to pay income tax on the difference amount under Income from Other Source.

Dear Mr Singh.. Income tax (if any) is payable only when you sell any asset and not while buying..

Are you referring to Stamp duty and registration fees? If so, then you need to pay them as per the guideline values only though your ‘Consideration’ is less..

Dear Mr.Srikanth,

I am a salaried class employee. I received compensation from Government (District Collector for National High Way project) for my agricultural land situated in my native village.

I would like to know which ITR form to use for filing my returns for AY2017-18 and showing this Agri land compensation from Govt.

Please let me know which ITR form i have to use and also please clarify under which head this income falls (which is completely tax exempted).

Thanks in advance

Dear Pandu,

As this compensation is tax-exempt, you can disclose it under ‘Exempt income’ section of an ITR.

Which ITR form? – It depends on your sources of income.

Suggest you to check with a CA too.

Kindly read : Which ITR form to file FY 2016-17?

Dear Sir,

My Friend Sold a Rural Agricultural Land (Agriculture land as per sec 2(14) it is not capital asset) to NRI and received money Rs.40,00,000/- (40 Lakhs) trough Bank Account from NRI Account. Please tell me am I need to show it as Capital gain or agricultural income.

Dear Ramesh,

For you, it is a tax-exempt transaction.Agricultural land in Rural Area India is not considered a capital asset. Therefore any gains from its sale are not taxable under the head Capital Gains.

Dear sir,

Some where I saw (In RBI website) that NRI cannot buy Indian agriculture land. If NRI wants to buy Indian agricultural Land They have take prior permission from RBI. In the above situation NRI did not taken any such permission. So, what will be the tax or what we have to do. Kindly help.

Dear Ramesh,

Under the exchange control law, an NRI is permitted to purchase immovable property in India other than agricultural land or plantation property.

To acquire agricultural land/plantation property/farm house in India, they have to get approval from the RBI and the government.

Suggest you to kindly take advice from a lawyer / Chartered Accountant who deals with NRI taxation matters.

hi sir , i have agriculture land and i want to sale it and want to use that money in other investment like buying a flat and car or non-agriculture land ..so is my other investment are taxable….

Dear Kiran,

If your agricultural land is in rural area, such land is not treated as Capital asset and hence no capital gain taxes are levied. Agricultural land in Rural Area India is not considered a capital asset. Therefore any gains from its sale are not taxable under the head Capital Gains.

If your agricultural land falls in Urban Area (non-rural area) then Capital Gain Tax is applicable.

You may refer the points given in the above article under the title ‘How do I save Capital Gains tax on sale of Urban Agricultural Land?’

My land in very close to munis-left limit, although I have to pay capital gain tax. How I CAN SAVE CAPITAL GAIN TAX ON SALE OF AGRICULTURE LAND

Dear Kishan ..Kindly go through above article.