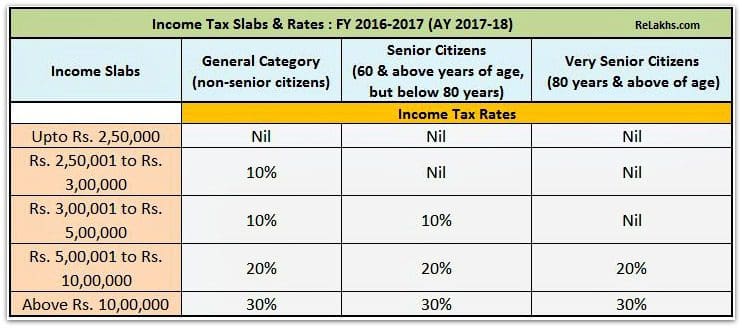

Indian Finance Minister, Shri Arun Jaitley has tabled today, the Union General Budget 2016-17 in the Parliament. No changes have been made to the existing Income Tax slabs & rates. Below are the Income Tax Slab Rates for FY 2016-17 or AY 2017 -18.

(FY is Financial Year. AY is Assessment Year)

Latest Income Tax Slab Rates for FY 2016-17

The income tax slabs & rates are categorized as below;

- Individual resident aged below 60 years.

- Senior Citizen (Individual resident who is of the age of 60 years or more but below the age of 80 years at any time during the previous year).

- Super Senior Citizen (Individual resident who is of the age of 80 years or more at any time during the previous year).

Budget 2016-17 & Important Tax Proposals

- Deduction amount under 80GG increased from Rs 24,000 per annum to Rs 60,000 per annum. Section 80GG is applicable for all the individuals who do not own a residential house & do not get HRA (House Rent Allowance).

- Section 87A Rebate : Benefit of Rs 5,000 upto the income of Rs 5,00,000. If you are earning below Rs 5 lakh, you can save an additional Rs 3,000 in taxes. Tax rebate under Section 87A has been raised from Rs 2,000 to Rs 5,000. Effectively, this means now the basic exemption is of Rs 3 lakh.

- 15 % Surcharge on income of more than 1 crore rupees yearly has been proposed, earlier it was 10 %.

- National Pension System : 40% of corpus withdrawal at the time of retirement will be tax exempted.

- As per the Budget 2016 proposal, at the time of retirement, 40% of the EPF (Employees Provident Fund) lump sum withdrawal is tax-exempted, 60% of the corpus is taxable as per the applicable Income Tax Slab. To avoid this, the EPF member has to invest this 60% balance in an Annuity life insurance product. The Annuity income will be Tax-free. (Read : Latest EPF withdrawal rules 2016)

- Section 80EE – First time Home Buyers can claim an additional Tax deduction of up to Rs 50,000 on home loan interest payments u/s 80EE.

- The home loan should have been sanctioned in FY 2016-17

- Loan amount should be less than Rs 35 Lakh

- The value of house should not be more than Rs 50 Lakh

- Budget 2016 proposes to levy 10% Dividend Distribution Tax (DDT) in the hands of the investor who receives dividend of Rs 10 Lakh or more in a financial year.

- Cash purchases of goods & services which are worth more than Rs 2 Lakh & purchases of car worth more than Rs 10 Lakh will be subject to TCS (Tax collection at Source). Tax at source of 1% on purchase of luxury cars would be levied.

- Budget 2016 has proposed to provide a limited period ‘Tax Compliance Window‘ for domestic taxpayers. This will be created between 1 June to 30th September to declare undisclosed income or income. To clear up their past tax transgressions, the taxpayers will have to pay tax at 30%, and surcharge at 7.5% and penalty at 7.5%. So, the total applicable tax would be at 45% of the undisclosed income. They will have to pay up the taxes within two months of declaration.

- Levy of Infrastructure Cess on purchase of SUVs & Diesel cars.

- Krishi Kalyan cess at 0.5% on all taxable services effective from 1st June, 2016.

- Income tax department will expand e-sahyog project to assist small taxpayers.

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net)

You may like reading below posts;

- List of Income Tax deductions & limits for FY 2016-17 (or) AY 2017-18

- Income Tax Declaration & Investment Proofs to be submitted to your employer

- Latest TDS rates chart for Financial Year (FY) 2016-17 (or) AY 2017-18

Join our channels

Dear Sir,

Please tell us we have received a salary of Rs. 42,000/- per month without any deduction, Ist salary received to may 2016, so, how to calculate salary with deduction. and how many pay the amount in TDS Department.

I am waiting your positive response asap.

Dear Pramod,

Do you mean to say that your employer is not deducting TDS?

Suggested articles:

Employer & TDS

TDS & Misconceptions

IT declaration & investment proofs

List of IT deductions for FY 2016-17

i have total salary of Gross 22941/- per month before deductions , worling in pvt company deductions of Rs1376 as Pf

own house no rent

It is reported by yo that income tax rebate under section 87A has been raised up to R’s.5000/- for the F/Y 2016-2017.But,in website of Incometax the same is still Rs.2000/-.Please intimate the factual position.

Dear Subhash ..The income tax rebate u/s 87A has been increased from Rs 2,000 to Rs 5,000 in Budget 2016 and would be applicable for Financial Year 2016-17 or AY 2017-18.

Sir Srikanth,

My flat started construction ( taken bank loan also as 37 Lakhs) from Oct’ 2010 and completed / possession taken fro builder in Feb’2016.. later it was vacant for 2 months to get the desired changes made by our selves and we have entered / self occupied in April’2016., till that time we were residing in a rental house outside.

Also my elder son and my self are the co-owners and Flat registered on both of us, and paying EMI also on sharing basis.

when computing the tax for 2015-16, can we show the Rent exemption on HRA and Housing loan interest beyond 2.0 lakhs each + 20% of pre-constructional interest for this year alone. ( practically it comes to Rs3.80 interest+ PCI 20% of 2.80 Lakhs over 5 years).

Our thinking is to each one of us to claim Bank interest as Rs1.90 + 1.40= Rs3.30 , thinking to claim, only in this year., tax returns have delayed submission and now we like to submit returns with in a weeks time.

Because as i understood, in case of self occupied, next year ( 2016-17) on wards, we should neither claim HRA exemption ( because we will not pay rent ) nor house loan beyond 2.0 lakhs, being self occupied.

Most important to us, this year, because practically it is true in our life, and we really paid the rent out side till March’ 2016 and the house was vacant for 2 months from Feb’16 to April’16…. even if we consider Feb;16 onwards if it is self occupied, can we consider balance 10 months for Interest + 20% pre-construction interest.

regards and Thanks,

V.Ravi sarma

Dear Ravi Ji,

If construction has been completed beyond 3 years from the date of loan disbursal, then you can claim tax deduction of up to Rs 30,000 only.

May I know when was the last installment made (loan) to the builder?

my wife is govt teacher who earning 29000 pm ,can see get deduction for my LIC premium & what other deduction are available for govt teacher? she is on contract basis.

Dear BNAIK,

Kindly read: List of income tax deductions ..

How much we can donate to charity under section 80(G)?

Donations paid to specified institutions qualify for tax deduction under section 80G but is subject to certain ceiling limits. Based on limits, we can broadly divide all eligible donations under section 80G into four categories:

a) 100% deduction without any qualifying limit (e.g., Prime Minister’s National Relief Fund).

b) 50% deduction without any qualifying limit (e.g., Indira Gandhi Memorial Trust).

c) 100% deduction subject to qualifying limit (e.g., an approved institution for promoting family planning).

d) 50% deduction subject to qualifying limit (e.g., an approved institution for charitable purpose other than promoting family planning).

The qualifying limits u/s 80G is 10% of the adjusted gross total income. The limit is to be applied to the adjusted gross total income. The ‘adjusted gross total income’ for this purpose is the gross total income (i.e. the sub total of income under various heads) reduced by the following:

Amount deductible under Sections 80CCC to 80U (but not Section 80G)

Exempt income

Long-term capital gains

Income referred to in Sections 115A, 115AB, 115AC, 115AD and 115D, relating to non-residents and foreign companies.

Dear Ehjaz..Thank you for sharing your inputs. Keep visiting!

Kindly clearyfy about section 40(b)regarding salaries &interest to Partners are withdrawn deduction of firms availing benifit of 44AD or for all firms as amended in budget 2016.

Many thanks in advance.

Dear Dharmesh..Kindly consult a CA.

Dharneshji from 1/4/16 income from business for partnership firm claiming deduction u/s 40(b) will be included in 44ad 8 % limit that means remuneration and interest will be deemed to be already allowed while computing profit u/s 44ad

Thanks a lot CA Ehjaz Ji,

This advise means a lot to me &many more

Dear Sreekanth,

•As per the Budget 2016 proposal, at the time of retirement, 40% of the EPF (Employees Provident Fund) lump sum withdrawal is tax-exempted, 60% of the corpus is taxable as per the applicable Income Tax Slab. To avoid this, the EPF member has to invest this 60% balance in an Annuity life insurance product. The Annuity income will be Tax-free.

As per my understanding after completion the age of 60 any investor can withraw maximum 60% of his total accumulated amount and out of that 60% withdrawl amount 40% will be tax free and 20% will be taxable.

Moreover it will be mandatory for the investors to buy immediate annuity plan from any of the insurer with remaining 40% amount and PENSION AMOUNT WILL BE TAXABLE. Please correct me if am wrong.

Dear Vishal..As of now, this amendment has been withdrawn by the govt.

I have given resignation and submitted form on 5th of December 2015.And my company submitted my form on 4th of March 2016. They told company keeping form 2month after that they will send. So I have submitted form to the company before new rules. there is any changes in claim amount. How much I will get in the claim amount.

Dear joseph..Are you currently employed?

Sir ! When this tax rebate U/s 87A should be considered ?

I will be grateful to the person if he can come out with some example table with two different category (one with rebate and teh other without rebate)

Dear Govind,

* Only Individual Assesses earning net income up to Rs.5 lakhs are eligible to enjoy tax rebate u/s 87A. For Example : Suppose your yearly pay comes to Rs.6,00,000 and you claim Rs.1,50,000 u/s 80C. The total net income in your case comes to Rs.4,50,000 which makes you eligible to claim tax rebate maximum of Rs.2,000.

* The amount of tax rebate u/s 87A is restricted to maximum of Rs.5,000. In case the computed tax payable is less than Rs.5,000, say Rs.2,500 the tax rebate shall be limited to that lower amount i.e. Rs.2,500 in our case.

* The Tax Assesse is first required to add all incomes i.e. salary, house income, capital gains, business or profession income and income from other sources and then deduct the eligible tax deduction amounts u/s 80C to 80U and under section 24(b) (Home Loan Interest) to come up with the net taxable income.

* If the above net taxable income happens to be less than Rs.5 lakhs than the tax rebate of Rs.5,000 comes in the picture and should be deducted from the calculated total income tax payable.

Click here to know more about Section 87A.

Dear Mr. Sreekanth Reddy !

Thank you very much for the detailed, complete and quick advice.

Dear Sir,

What about the NPS tax benefits for the FY 2016-17? whether the deduction under 80 CCD-1B ( Additional benefit of Rs. 50K is over and above the benefits under 80C) is existing or Not?

Dear Raj..I believe that tax deductions rules are same u/s 80ccd for AY 2017-18.

I’ve one CAN account with CAMS. Now via mfuonline portal, I can invest/redeem/SIP in mutual funds from the comfort of my home! Now I want to open a demat account for online share trading. How to open it? And what are my options? Suggest me the option which has minimum or no brokerage for opening/maintaining that account, but with more features. Wish to see one full article on that from you in future.

Dear Raju,

For a long-term investor, who wish to buy and hold investments, who does not prefer short-term trading, I believe that any dmat a/c service provider is ok to go with.

I will surely try to write an article on this topic. Thank you for the suggestion!

Dear Mr. Sreekanth,

Can you please clarify if a person retired during the year 2015 and he withdraws the PF amount after April 2016 what will be his tax implications?

Thanks and regards

H. R. Krishnan

Dear KRISHNAN,

As the 60:40 tax rule is applicable only on contributions made after april 2016, this rule is not applicable.

If the person has attained 58 years, he/she can withdraw full PF balance.

Read: Latest PF withdrawal rules 2016.

Dear Sreekanth,

Like EPF, Is there any effect on PPF.

Dear Kumar..No. PPF still falls under the E-E-E tax category.

Thank you for your quick response

Thank you.

I got a home loan sanctioned on 15th Feb 2016, Will I get “Tax deduction of up to Rs 50,000 on home loan interest payments”

Dear Jayakrishnan..No, the home loan should have been sanctioned in FY 2016-17.

What about the section 80C?

Does 150000 limit is same or increased?

It is the same

Hi,

I want to know how to calculate tds per month on salary, if you can help out with excel sheet calculation.

Dear heena..There are lot of excel based tax calculators available on net. You ma kindly google.

You can also visit this link..

Tax rebate U/s 87 A – Rs. 5,000/- should be applied before the Standard Deduction of after ?

Kindly advice

Dear Govind..By standard deduction do you mean regarding ‘income from house property’ (or) Tax deductions like section 80c etc??