Budget 2016-17 has been presented in Parliament. The Finance Minister has kept the Personal Income Tax slab rates unchanged for the Financial Year 2016-17 (Assessment Year 2017-2018).

Let us understand all the important sections and new proposals with respect to Income Tax Deductions FY 2016-17. This list can help you in planning your taxes.

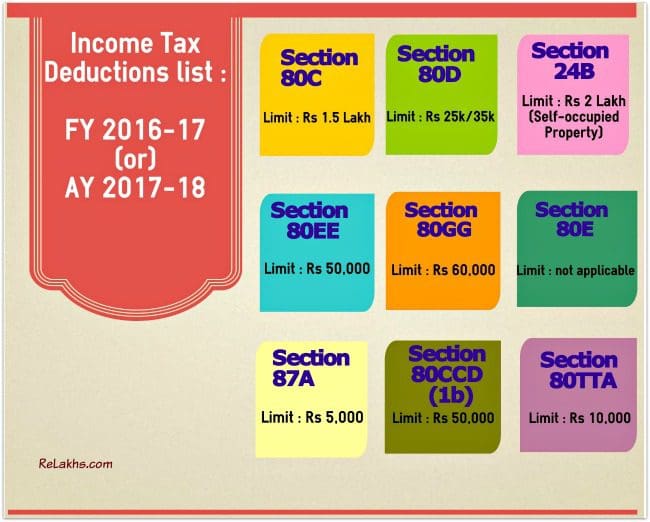

Income Tax Deductions FY 2016-17

Section 80c

The maximum tax exemption limit under Section 80C has been retained as Rs 1.5 Lakh only. The various investment avenues or expenses that can be claimed as tax deductions under section 80c are as below;

- PPF (Public Provident Fund)

- EPF (Employees’ Provident Fund)

- Five year Bank or Post office Tax saving Deposits

- NSC (National Savings Certificates)

- ELSS Mutual Funds (Equity Linked Saving Schemes)

- Kid’s Tuition Fees

- SCSS (Post office Senior Citizen Savings Scheme)

- Principal repayment of Home Loan

- NPS (National Pension System)

- Life Insurance Premium

- Sukanya Samriddhi Account Deposit Scheme

Section 80CCC

Contribution to annuity plan of LIC (Life Insurance Corporation of India) or any other Life Insurance Company for receiving pension from the fund is considered for tax benefit. The maximum allowable Tax deduction under this section is Rs 1.5 Lakh.

Section 80CCD

Employee can contribute to Government notified Pension Schemes (like National Pension Scheme – NPS). The contributions can be upto 10% of the salary (or) Gross Income and Rs 50,000 additional tax benefit u/s 80CCD (1b) was proposed in Budget 2015.

To claim this deduction, the employee has to contribute to Govt recognized Pension schemes like NPS. The 10% of salary limit is applicable for salaried individuals and Gross income is applicable for non-salaried. The definition of Salary is only ‘Dearness Allowance.’ If your employer also contributes to Pension Scheme, the whole contribution amount (10% of salary) can be claimed as tax deduction under Section 80CCD (2).

Kindly note that the Total Deduction under section 80C, 80CCC and 80CCD(1) together cannot exceed Rs 1,50,000 for the financial year 2016-17. The additional tax deduction of Rs 50,000 u/s 80CCD (1b) is over and above this Rs 1.5 Lakh limit.

Section 80D

Deduction u/s 80D on health insurance premium is Rs 25,000. For Senior Citizens it is Rs 30,000. For very senior citizen above the age of 80 years who are not eligible to take health insurance, deduction is allowed for Rs 30,000 toward medical expenditure.

Preventive health checkup (Medical checkups) expenses to the extent of Rs 5,000/- per family can be claimed as tax deductions. Remember, this is not over and above the individual limits as explained above. (Family includes: Self, spouse, dependent children and parents).

Section 80DD

You can claim up to Rs 75,000 for spending on medical treatments of your dependents (spouse, parents, kids or siblings) who have 40% disability. The tax deduction limit of upto Rs 1.25 lakh in case of severe disability can be availed.

To claim this deduction, you have to submit Form no 10-IA.

Section 80DDB

An individual (less than 60 years of age) can claim upto Rs 40,000 for the treatment of specified critical ailments. This can also be claimed on behalf of the dependents. The tax deduction limit under this section for Senior Citizens is Rs 60,000 and for very Senior Citizens (above 80 years) the limit is Rs 80,000.

To claim Tax deductions under Section 80DDB, it is mandatory for an individual to obtain ‘Doctor Certificate’ or ‘Prescription’ from a specialist working in a Govt or Private hospital.

For the purposes of section 80DDB, the following shall be the eligible diseases or ailments:

- Neurological Diseases where the disability level has been certified to be of 40% and above;

(a) Dementia

(b) Dystonia Musculorum Deformans

(c) Motor Neuron Disease

(d) Ataxia

(e) Chorea

(f) Hemiballismus

(g) Aphasia

(h) Parkinson’s Disease

- Malignant Cancers

- Full Blown Acquired Immuno-Deficiency Syndrome (AIDS) ;

- Chronic Renal failure

- Hematological disorders

- Hemophilia

- Thalassaemia

Section 24 (B)

The interest component of home loans is allowed as deduction under Section 24B for up to Rs 2 lakh in case of a self-occupied house. If your property is a let-out one then the entire interest amount can be claimed as tax deduction. (Read: Understanding Tax Implications of Income from house property)

Section 80EE

This is a new proposal which has been made in Budget 2016-17. First time Home Buyers can claim an additional Tax deduction of up to Rs 50,000 on home loan interest payments u/s 80EE. The below criteria has to be met for claiming tax deduction under section 80EE.

- The home loan should have been sanctioned in FY 2016-17.

- Loan amount should be less than Rs 35 Lakh.

- The value of the house should not be more than Rs 50 Lakh &

- The home buyer should not have any other existing residential house in his name.

Section 80U

This is similar to Section 80DD. Tax deduction is allowed for the tax assessee who is physically and mentally challenged.

Section 80GG

As per the budget 2016 proposal, the Tax Deduction amount under 80GG has been increased from Rs 24,000 per annum to Rs 60,000 per annum. Section 80GG is applicable for all those individuals who do not own a residential house & do not receive HRA (House Rent Allowance).

The extent of tax deduction will be limited to the least amount of the following;

- Rent paid minus 10 percent the adjusted total income.

- Rs 5,000 per month.

- 25 % of the total income.

Section 80G

Contributions made to certain relief funds and charitable institutions can be claimed as a deduction under Section 80G of the Income Tax Act. This deduction can only be claimed when the contribution has been made via cheque or draft or in cash. But deduction is not allowed for donations made in cash exceeding Rs 10,000. In-kind contributions such as food material, clothes, medicines etc do not qualify for deduction under section 80G.

Section 80E

If you take any loan for higher studies (after completing Senior Secondary Exam), tax deduction can be claimed under Section 80E for interest that you pay towards your Education Loan. This loan should have been taken for higher education for you, your spouse or your children or for a student for whom you are a legal guardian. Principal Repayment on educational loan cannot be claimed as tax deduction.

There is no limit on the amount of interest you can claim as deduction under section 80E. The deduction is available for a maximum of 8 years or till the interest is paid, whichever is earlier.

Section 87A Rebate

If you are earning below Rs 5 lakh, you can save an additional Rs 3,000 in taxes. Tax rebate under Section 87A has been raised from Rs 2,000 to Rs 5,000 for FY 2016-17 (AY 2017-18).

In case if your tax liability is less than Rs 5,000 for FY 2016-17, the rebate u/s 87A will be restricted up to income tax liability only.

Section 80 TTA

Deduction from gross total income of an individual or HUF, up to a maximum of Rs. 10,000/-, in respect of interest on deposits in savings account with a bank, co-operative society or post office can be claimed under this section. Section 80TTA deduction is not available on interest income from fixed deposits.

Conclusion

It is prudent to avoid last minute tax planning. Do not invest in unwanted life insurance polices or in any other financial products just to save taxes. It is better you plan your taxes based on your financial goals at the beginning of the Financial Year itself. Plan your taxes from April 2016 itself, instead of waiting until late December 2016 (or) January 2017.

It is OK to pay some taxes when you can not save or cannot invest in right financial products. But, do not invest just to save TAXES. The cost of buying wrong financial products may outweigh the cost of taxes. Tax Planning is not a goal but a tool. Remember “Tax Planning alone is not Financial Planning.”

Also, kindly understand the tax treatment of the selected investment products across the different investment stages (i.e., investment, accrual & withdrawal) and then invest.

I believe that the above list is useful for your Tax Planning purposes. The above ‘Income Tax Deductions 2016-17’ are applicable for financial year 2016-2017 (Assessment Year 2017-2018).

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net)

You may like reading : How Income Tax Dept tracks High Value Financial Transactions?

Join our channels

I was employed for the period April – December 2019 and based on the rent agreement and receipts submitted to the employer, got HRA relief.

For the period Jan – Mar 2020, I worked as a self employed professional.

I paid a rent of Rs. 30,000 by crossed cheque to my landlord for the month of January 2020.

I shifted my residence and paid Rs. 18,000 for the period Feb & Mar 2020 to my landlord via net transfer.

I would like to know if I can claim HRA relief from the employer for the period of employment (April – December 2019) in the ITR 2 Form in Schedule ‘Salary’ and simultaneously claim relief u/s 80GG in Schedule ‘VI A’ by submitting 2 separate 10BA forms for the two residences during Jan – Mar 2020.

Thanking you in anticipation of an early response

With Kind Regards

Vijay Maheshwari

Dear VIJAY,

I believe that You must not have availed any HRA during the entire financial year. If you were employed for 1 month in the financial year (and availed HRA) and were self-employed during the remaining period, you cannot avail tax relief under Section 80GG.

Thanks for sharing this blog

I have three fixed deposit in Central Bank of India. The bank has deducted TDS of Rs. 2589 for the interest of Rs. 25881.15 on the same though it is not matured. While e-filing the return TDS of CBI comes automatically. Now my question is that whether I should show this income of Rs. 25881 in the income details column under head “Income from Other Sources” or not ? Because if I show that amount my refundable amount decreases and if not show refundable amount increases.

Dear Mahendrasinh,

You need to show the interest income under ‘income from other sources’ and also disclose the TDS details in ‘Tax paid’ sheet.

Hello Mr.Sreekanth,

I was searching for useful articles related to income tax exemptions and deductions and come across your article which is quite informational based on your detailed analysis or expertise.

The content of your blog seems very comprehensive and interesting to read.

I would like to draw your attention towards the Delhi-based online income tax filing services website.Kindly check out the link http://www.trutax.in/ .

It is a portal where the taxpayer can upload their form-16 with required documents and file their income tax returns with ease.It is a platform to give the latest updates of taxation and manage client’s taxes as well as their income tax returns.

This Might be a worth mention on your page.

Either way, keep up the awesome work.

Also, I was hoping you would consider us in contributing articles about topics related to taxes, taxing systems in India, etc. so that we can our knowledge and expertise with your audience.

Is this something you would be interested in?

Let me know what you think.

Regards

Harsh(TruTax)

Dear Harsh,

Thank you for your appreciation.

You may reach me through our Contact page. Cheers!

Respected Sir

In fy 2016-17 i invest Rs 150000 u/s 80c, & i invest Rs 20000 In NPS Tier -1 , can i take tax benefit u/s 80ccd(1) ? Or which u/s benefit receivable ?

Dear pravin ..Yes you can claim u/s 80 ccd (1b)

Dear pravin ..Yes you can claim u/s 80 ccd (1b)

Hi

My salary is 19 lakhs PA , I bought an new apartment for 50Lakhs , so I will pay my principle and interest which comes around 50k per month, but I am not occupied in the apartment it will get over by 2018 -19.

Can I claim full interest which I pair or there is maximum limit of 2 lakhs only.

Please clarify me on this .. Also in the section 80 EE there is 50,000..

Dear Ashok ,

As it is an under-construction property, you can not claim tax benefits on it till your take possession of the property.

The maximum loss that you can claim is up to Rs 2 Lakh only.

Rs 50,000 u/s 80EE can be claimed on under-construction property too (if the conditions are met).

Read :

IT deductions list for FY 2017-18.

Under-construction property & Tax implications.

Where to show standard deduction u/s 24A in ITR 1 excel form of ay 2027-18 ?

Dear Bidehjee ..You need include (claim it) in the calculation of ‘income from house property‘.

My father is an paralysis patient. i am salaried professional, can i avail 80dd deductions for my IT returns and if yes then can i claim 75000 rs?

Dear dhiraj ..I believe that Paralysis comes under Section 80U.

Section 80U is similar to Section 80DD. Tax deduction is allowed for the tax assessee who is physically and mentally challenged.

Thanks for the Blog , it has been really helpful.

Dear Naren ..You may go through my latest article on – Important IT exemptions list for FY 2017-18 / AY 2018-19.

Hi,

I have received my Apr,May,June month salary from the company, but after that the company was not paying salary to us and after three month it got closed without paying any salary and reimbursements. Management is fighting in court for their dues. I have lost my three month salary and also the reimbursements. How should i show this loss of income in my ITR. I have also not received the Form 16 from previous employer as the company was closed. whatever i have earned in three month salary almost i have lost the same amount in form of reimbursements. Kindly advise.

Dear Dheeraj ..I believe that these are not loses but dues have not been paid.

You need to file your ITR based on the income that you have received in FY 2016-17.

Hi

My father is 62 and dependent on me. In June 2016 he had pacemaker implantation which cost around 2.36 lakh. out of which I got 1.55 lakh from insurence claim. Can I claim 40k under section 80DDB amount for tax deduction.

Dear Sushil ..Kindly note that Sec 80DDB is applicable for the above listed Medical treatments only.

sir,

my father is having 80% disability certificate which clearly states that no further reassessment is required. regarding 80DD my query is i am getting all the claims for his expenses incurred from health insurance provided by my employer.Should this claim amounts credited in my account by the insurance company be also shown as my income to claim 80dd.

Dear sharath ..I believe that same expenses can not be claimed twice..

my salaried income is 445200 and investment under 80c is 51500 i have also pay 60000 as annual house rent

what will be the exemption under 80gg

kindly help

Dear Saninder,

Under Section 80GG, you can claim the least of the below applicable amounts:

Rs. 60,000 annually (Rs. 5,000 monthly)

The amount that is equal to the total rent paid minus 10% of the total income

25% of annual salary

Provided , you do not get HRA benefits in your salary.

My wife undergone Kidney transplant in Feb 2016. But I did not claim any tax deduction.. Now our expense is atleast Rs. 10000 a day.. Can I claim tax deduction under 80DDB?

Dear Vikas,

I have provided the eligible list of diseases / ailments in the above article.

If your spouse’s medical treatment is for any of the above ailments, you can claim tax deduction u/s 80DDB.

For FY 2016-17, I have already invested in ELSS for Rs.150000/- I have also made a donation to a registered Charitable Institution (IT Dept accepted) for Rs.15000. How much deduction I can claim in the return.

Dear Narasimhan,

Your investment of Rs 1.5 Lakh can be claimed u/s 80c.

50% of donation made to charitable institution can be claimed u/s 80G.

hi, srikant,

iam a retired psu employee. now ihave income from interests on bank fds and cpaital gains on mutual funds and shares. which IT form to be filled. pl., let me know.

can i personally contact u for future investment plans pl provode your mob no:

Dear sudhakar Ji,

Kindly go through this article : Which ITR form to fill? (This is as per AY 216-17)

How to calculate the i.tax for individual & pvt comp & its director , M.D for f.y-2016-17/ A.y-2017-18

Dear chittaranjan ..Kindly consult a CA.

Although the Research fellowships, grants received from govt. universities are all tax-exempted, is it necessary to show the income(from fellowship) while filing the return.

or how one can show the income for his loan EMI’s if he is getting fellowship.

Dear Ankit,

I believe that one can disclose it under Exempt Income section of ITR.

Can show the bank statements (if accepted & considered by the lending insti) which reflect the income.

thanks sir

this will help me a lot for my home loan EMI’s

One more query is about HRA, apart from my income under scholarship i am also getting an amount of Rs 76500/- pa as HRA, so where this HRA is to be declared, I think It should be declared under the head “Income from salaries” may I right?

if is it so what exemptions are applicable over this HRA received under section 10(13a) since the income under the head salary is zero

Dear Ankit,

As the entire income is tax-exempt, need not worry about HRA exemption as it is also a part of your income.

thanks

i am kishor, i need the details for house rent how much possible to get income tax deduction for me, because iam staying in my own house. i can possible to get house rent deduction for my income tax deduction for the year 2016-17.

Sir,

My mother is 84 years of age and suffering from hypertension, vertigo and cardiac disease. She has been hospitalized twice in this financial year. My query is can I claim rebate for the hospital bill under 80DD or 80DDB as only some specified diseases are given from which we can claim rebate. She does not have mediclaim.

Dear Velarian,

The tax claim under sections 80DD or 80DDB are limited to certain conditions only, as given in the above article.

I believe that you can claim up to Rs 30,000. For very senior citizen above the age of 80 years, not eligible to take health insurance, deduction is allowed for Rs 30,000 toward medical expenditure u/s 80D.

Kindly read : Section 80D & tax benefits.