Sukanya Samriddhi Account (SSA) along with ‘Beti Bachao-Beti Padhao’ (BBB) will be officially launched on 22nd January, 2015. These schemes will be introduced by our honorable Prime Minister Narendra Modi.

Sukanya Samriddhi Account/Yojana is a Small Savings Special deposit Scheme for girl child. This scheme is specially designed for girl’s higher education or marriage needs.

Finance Minister Arun Jaitley had announced this scheme in his budget speech in July. The gazette on this scheme was released on 2nd December, 2014. On 21st January, 2015 the finance ministry released a notification with respect to the applicable interest rate on Sukanya Samriddhi Account.

Let us understand the features and benefits of Sukanya Samriddhi Account Special Savings deposit scheme.

Features of Sukanya Samriddhi Account (SSA):

- Who can open the account? – Sukanya Samriddhi a/c (or Khata) can be opened on a girl child’s name by her natural (biological) parents or legal guardian.

- What is the Age limit? – SSA can be opened in the name of a girl child from the birth of the girl child till she attains the age of ten years. (Girl child who is born on or after 02-12-2003 can open SSA/SSY account).

- How many accounts can be opened? – A depositor may open and operate only one account in the name of same girl child under this scheme. The depositor (or) guardian can open only two SSA accounts. There is one exception to this rule. The natural or legal guardian can open two or three accounts if twin girls are born as second birth or triplets are born in the first birth itself.

- How to open a SSA account (Sukanya Savings Account opening procedure)? Accounts in name of the girl child can be opened in post offices or in any branch of a commercial bank that is authorized by the Central Government to open an account under this scheme rules. As of now, the list is not drawn and many government owned banks are still in the process of completing formalities to open the Sukanya Samriddhi Yojana (SSY) Account, you may visit any of the government banks for the purpose of opening the account. (Some of these banks include – State Bank of India (SBI), SBH, Bank of Baroda, Punjab National Bank, Bank of India, Canara Bank, Andhra Bank, UCO Bank, Allahabad Bank, Corporation Bank etc.,)

- What is the minimum deposit to open the account? –

The account may be opened with an initial deposit of one thousand rupees. The minimum contribution in any financial year is Rs 1000. Thereafter the contributions can in multiples of one hundred rupees.- SSA Account may be opened with a minimum initial deposit of two hundred and fifty rupees and thereafter any amount in multiples of two hundred and fifty rupees may be deposited in an Account subject to the condition that a minimum of two hundred and fifty rupees shall be made as deposit in a financial year in one Account. (Latest update : 15-July-2018)

- What is the maximum deposit amount? – a minimum of

one thousand rupeesRs 250 shall be deposited in a financial year but the total money deposited in an account on a single occasion or on multiple occasions shall not exceed Rs 1.5 Lakh in a financial year. - Deposits/contributions in an account may be made for fourteen years from the date of opening of the account.

- Is there any penalty? – If minimum (Rs 1000 pa) amount is not deposited, the account will be treated as an irregular account. This can be regularized/renewed on payment of Rs 50 per year as penalty. Along with this, the minimum specified subscription for the year (s) of default should be paid.

- What is the mode of deposit? – The deposits in Sukanya Samruddhi scheme can be made in the form of Cash or Demand Draft or Cheque. Where deposit is made by cheque or demand draft, the date of encashment of the cheque or demand draft shall be the date of credit to the account. The cheque or DD should be drawn in favour of the postmaster of the concerned post office or the Manager of the concerned bank.The depositor (parents or guardian) has to write the account holder’s name (child’s name) and the account number on the backside of the instrument.

- What is the Rate of Interest on Sukanya Samriddhi Account? – The applicable rate of interest on SSA for the financial year 2014-2015 is 9.1%. This is one of the highest rates of interest offered by Government on small savings scheme. (Latest News (18-March-2016): The Govt has cut rate of interest of Sukanya Samriddhi Scheme. The interest rate on Sukanya Samriddhi Account (SSA) for 1st Quarter of Financial Year (FY) 2016-17 would be 8.6%. For complete details on revised interest rates, click here..)

- Is interest rate fixed or variable? – The rate of interest is not fixed and will be notified by the central government on a yearly basis.

- The account can be transferred anywhere in India if the girl shifts to a place other than the city or locality where the account stands.

- Is Premature withdrawal allowed? – 50 % (half of the fund) of the accumulated amount in SSA can be withdrawn for girl’s higher education and marriage after she attains 18 years of age. The account’s balance at the end of preceding financial year is used for the calculation.

- Can the girl child operate the account? On attaining age of ten years, the account holder that is the girl child may herself operate the account, however, deposit in the account may be made by the guardian or parents.

- Is premature closure allowed? In the event of death of the account holder, the account shall be closed immediately on production of death certificate. the balance at the credit of the account shall be paid along with interest till the month preceding the month of premature closure of the account , to the guardian of the account holder.

- The scheme would mature on completion of 21 years from the date of opening of the account, with an option of keeping the account till marriage. So, the maturity of the account is 21 years from the date of opening of account or if the girl gets married before completion of such 21 years (whichever is earlier).

- Can the girl child continue the account after her marriage? – The operation of the account shall not be permitted beyond the date of the girl’s marriage.

- What are the required documents to open Sukanya Samriddhi Account? – Birth certificate of the girl child has to be produced. The depositor (parents or guardian) has to submit his/her identity and address proofs.

- Download Sukanya Samriddhi Account/Yojana (SSA/SSY) Application form. (This SSA applicaiton form that can be submitted at Post office. Download the file by clicking on the below image and go to ‘Form 1’ Post office Savings Bank page and you can take print out of the same)

- On opening an account, the depositor shall be given a pass book. It will have date of birth of the girl child, date of opening of account, account number, name and address of the account holder and the initial amount deposited. The depositor has to present the passbook to the post office or bank at the time of depositing/receiving the interest/on maturity.

Income Tax Benefits on Sukanya Samriddhi Account Scheme – Section 80c

The amount that is deposited under Sukanya Samriddhi Account will be eligible for income tax exemption under Section 80C of Income Tax Act, 1961.

(Issue of making interest income exempt from taxation can be done by Department of Revenue (DoR) through legislative amendments. The matter is under examination of DoR)

Latest News : As per Budget 2015, all the payments under Sukanya Samriddhi Account / Yojana Deposit Scheme are exempted from Income Tax. So, Deposits made under SSA Khata / account are exempted under Section 80C. The interest amount and maturity amount (withdrawals) are also exempted from Income Tax. So, investments in SSA falls under Exempt – Exempt – Exempt (EEE) tax category.

PPF Account (Public Provident Fund) Vs Sukanya Samriddhi Account

PPF (Public Provident Fund) has E-E-E tax rule. As per this rule – contributions, accumulation (interest amount) and withdrawal are all exempted from income tax. There is a high chance that Sukanya Samruddhi Account may be brought under E-E-E catergory(As of now there is no official confirmation on this. Let us wait for more information).

For the fiscal year 2014-2015 the rate of interest on PPF account is 8.70% (upto March 2015). On Sukanya Samruddhi Account this is 9.10%. So, comparatively SSA has higher rate of interest. The interest on SSA will be calculated just like the way it is done on PPF a/c.

Sukanya Samridhi Account – Interest Amount & Maturity Amount Calculation:

You may have few questions like : How is the interest amount calculated on Sukanya Samridhi Savings scheme? – What could be the total maturity amount on SSA Savings account? What is the total interest amount that I can earn on SSA?

Before proceeding with the calculations, below are the main points/assumptions with respect to interest and maturity amount calculations:

- The contributions are allowed upto 14 years from SSA account opening date.

- The SSA savings account can be operated till the completion of 21 years from the account opening date.

- The current applicable interest rate on SSA scheme is 9.1% (this rate of interest will vary in future, as per the Central Government’s future notifications.)

- The interest on SSA will be calculated just like the way it is done on PPF a/c. (PPF interest is calculated monthly on the lowest balance between the end of the 5th day and last day of month, however the total interest in the year is added back to PPF only at the year-end.)

- I have assumed the investments are done at the beginning of every month/year and calender year as April-March.

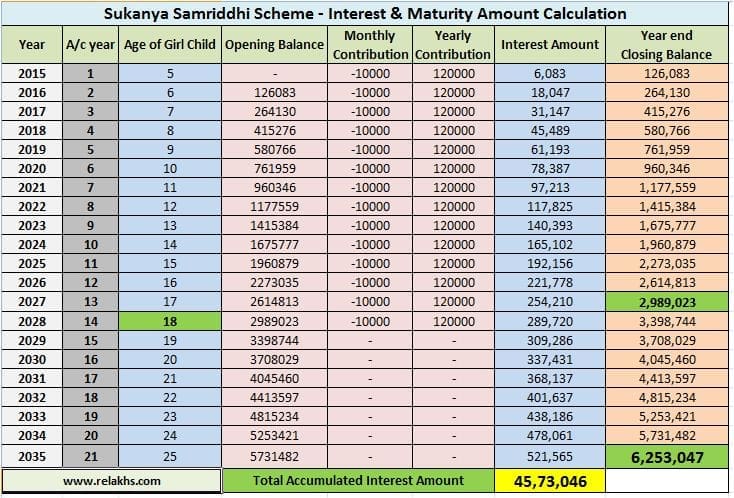

Sukanya Samriddhi Account/Yojna – Interest & Maturity amount calculation – Scenario 1-Monthly Deposit

Example 1 – Mr Aravind Swamy wants to open the Sukanya Samridhi Savings account in the name of his girl’s child (5 years old) in April 2015. He wants to contribute Rs 10,000 every month for 14 years. He also wants to keep this account active till 21 years from the account opening date (or till Child’s age of 25 years). He wants to know, what could be the total approximate interest amount and total maturity amount that he would accumulate under SSA?

As per above calculations, Mr Aravind Swamy can accumulate total interest amount to the tune of Rs 45.73 Lakh. The total maturity amount on his SSA savings account can be Rs 62.53 Lakh. He also has the option to withdraw 50% of Rs29.89 Lakh when his child turns 18 years. (If he withdraws, the total maturity amount will not be as shown above.)

The present value (PV) of Rs 62.53 Lakh (maturity amount ) is Rs 8.45 Lakh, assuming 10% as Education inflation (the rate at which education/marriage expenses may increase). Kindly think from this angle too.

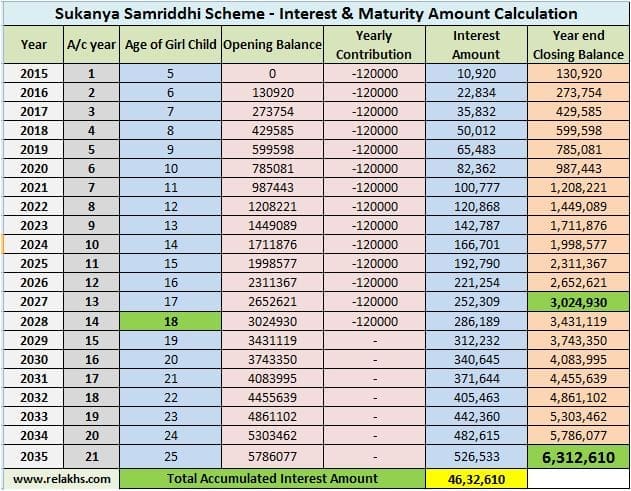

Sukanya Samriddhi Account/Yojna – Interest & Maturity amount calculation – Scenario 2 – Yearly Deposit

Example 2 – Mr Madhavan wants to open the Sukanya Samridhi Savings account in the name of his girl’s child (5 years old) in April 2015. He wants to contribute Rs 1,20,000 every year for 14 years. He also wants to keep this account active till 21 years from the account opening date (or till Child’s age of 25 years). He wants to know, what could be the total approximate interest amount and total maturity amount that he would accumulate under SSA?

As per the above calculations, Mr Madhavan can accumulate total interest amount to the tune of Rs 46.32 Lakh. The total maturity amount on his SSA savings account can be Rs 63.12 Lakh. He also has the option to withdraw 50% of Rs 30.24 Lakh when his child turns 18 years. (If he withdraws, the total maturity amount will not be as shown above.)

Kindly note the difference in the maturity amounts between the ‘monthly contribution account’ and ‘yearly contribution account.’

My opinion on Sukanya Samriddhi Account Savings Scheme:

I can confidently say that the average rate of education inflation in India is somewhere around 10% to 15%. The rate at which marriage expenses are increasing is also very high.

Given this scenario, the 9.10% rate of interest may not beat the inflation. Unlike Bank fixed deposits, this rate of interest is not fixed.

The better way to create sufficient corpus for a Child’s education is to allocate major portion of savings to equity related instruments (if you have more than 10 years time frame). You can then consider investing small portion of your savings towards this scheme. This scheme can be considered as the DEBT component of your investment portfolio.

Another drawback of SSA is the number of accounts that can be operated. The number of accounts that are allowed to open under this scheme is limited to two accounts only. Parents of more than two girls can not open multiple Sukanya Samriddhi Accounts.

(Download Government’s Gazette & notification on Sukanya Samriddhi Account/yojna savings deposit scheme. Gazette is in HINDI and english versions) (Image courtesy of chubphong at FreeDigitalPhotos.net )

Latest News – Reserve Banks of India (RBI) has issued a notification, authorizing 28 banks to open Sukanya Samriddhi Accounts. These banks include SBI, ICICI Bank, Bank of Baroda, Punjab National Bank (PNB), Allahabad Bank, Canara Bank, Corporation Bank, Andhra Bank etc., For complete list, kindly read my article – “Sukanya Samriddhi Deposit Account – Authorized Banks list for Account opening – Download Sukanya Samriddhi A.c Opening form.”)

Continue reading..

- Latest Interest Rate on Sukanya Samriddhi Deposits

- Comparison of Sukanya Samridhi Yojana Savings Scheme with Public Provident Fund.

- Calculate how much do you need to invest for kid’s education.

- 15 New Amendments to Sukanya Samriddhi Scheme – Revised Rules 2016.

Join our channels

If I pay lum sum 25000 in a particular year, the next year can i deposit more or less means can i deposit greater than or less than in the next financial year

Dear Shaik,

Yes, you can..

The minimum annual contribution to the Sukanya Samriddhi Account is Rs. 250 and the maximum contribution is Rs. 1.5 lakh in a financial year.

Can we closed in middle this shecme ssa.

Dear Ashwin,

You may kindly go through this article @ Sukanya Samriddhi Account Deposit Scheme – New Amendments 2016

This scheme can also be viewed as an initiative on part of the Government, to increase the domestic savings percentage which had reduced from 38% of the GDP in 2008 to 30% in 2013. This scheme is expected to encourage parents/guardians to save for their girl child’s education and future

My Self chetan i have one daughter and i need to pay quarterly or yearly how much amount has to pay.

i want to know how much amt l had to pay and what is the interest rate

Dear Chetananand,

You can deposit monthly, quarterly or yearly as per your choice. The minimum amount you have to deposit is Rs 250 pa and the maximum amount is Rs 1.5 lakh p.a.

Dear sir,If,The parent or guardian unexpected death.any insurance is applicable

Dear CHELLADURAI ..Insurance is provided under this scheme.

Hi

Who can withdraw the money any time if both the account holder and the guardian is not available

Dear Lavanya.. A legal heir can withdraw the funds.

Related article : Nominee Vs Legal Heir : Who will inherit (or) own your Assets? | Importance of WILL

if i withdraw after 14 years would i get maturity amount benefit.? please suggest…

My 1st daughter was born on 15.03.2013 and i want to open SSA in P&N Bank which was operated by my wife she was a house wife,if i attached my name as a 2nd account holder will i be able for Tax benefit u/s 80C.

My second part was if in same bank after some time again,I open SSA for my next child than also can i get tax benefit collectively for both of my daughter collective amounts.

waiting for your reply pls.

Dear Syed ..If your wife is contributing to SSA, only she can claim the tax benefit of up to Rs 1.5 Lakh u/s 80c.

Hi,

The information provided is very useful. Thanks.

I have two questions.

1) If I invest monthly or Annually, how will I be benefited compared to Interest amount calculated ?

2) If I pay 2,500 inr/ monthly as a Standing Instruction in SBI, annually it would be around 30,000. Say, by year end I had some surplus amount 20,000. Can i deposit this amount in SSA as well and avail the benifits ?

Dear Sharath,

If you invest say lump sum amount in the beginning of the year, the interest is payable for the entire year.

This is not the case with monthly deposits. It is calculated monthly on the lowest balance between the end of the 5th day and last day of month,

2 – Yes, you may do so.

Thanks a lot for the info.

sir my daughter was 14 years old. please tell best savings scheme for her.

I already opened SSA account in my daughter name and i am investing 1.5 Lakh per financial year .Now i would like to knwow who can claim this ( Father or Mother )while filing income tax. How do Income Tax Department verify these.

I am an NRI and i want to include this investment in my income tax filing to avoid tax against the income earn from India.

My wife is housewife and she doesnt have to file income tax.

Baby

Dear Manoj,

The depositor (mentioned in the passbook) has to claim the tax benefit.

Kindly read: SSA scheme & new amendments.

Dear Sir, My daughter’s D.O.B. was 07/04/2003. I was ppf account on her name from 14/02/2005. i want to open SSA account on her name. Is that possible? And one more thing , Is it possible to migrate PPF account in SSA account. I am waiting for your kind reply.

Dear Shyam,

Transfer of funds from PPF A/c to SSA is not possible.

If you girl child is aged more than 10 years, you can not open SSA account in her name.

Read:

Kid’s education goal planning.

List of best investment options.

Dear Sir,

My daughter’s DOB is 07/04/2003. I have PPF account in state bank of india from last 5 years. and i want to migrate my ppf account in SSA. Is that possible? I want to open SSA account for my daughter how and if any other investment government scheme are available? Please guide me for investment.

Dear Sir,

My daughter is born on th April 2006 Pune, confirm if the SSA scheme applicable for her, if yes confirm the last date to submitt the scheme form in the bank.

If not, kindly help any other government scheme feasible me to apply the same for future prospective.

Thanks

Dear Rajesh ..Age limit is 10 years, so it’s not possible to open SSA.

Kindly read:

List of best investment options!

Kid’s education goal planning & Calculations.

Dear Sir,

if i deposite 1000 every year then how much i will earn after 21 years, kindly send calculation in excel format

Thanking you

Reply

Sir my child was born on 23/08/2007, if I will be able to open this ssa a/c. I will deposit 1000 rs per month,then kindly send how much I will get after 21 yrs.

Thanking you.

Dear Roopa & Srinivas..Kindly download the SSA calculator…

Dear Sir,

I have opened Sukanya Samridhi Account for my girl child on 11/01/2017. I am planning to deposit INR 1,50,000 annually.

I have made 1st deposit of INR 1,50,000 on 11/01/2017.

Now my question is ….

When should I deposit my 2nd installment ?

case – 1 : at the start of financial year 2017-18 i.e on 01/04/2017

case – 2 : at the opening date of next year i.e 11/01/2018

case – 3 : anywhere in the middle of financial year 2017-18 i.e, say 01/08/2017

which of the above case would be idle and will benefit me maximum….

Thanks in advance

Dinesh Ramakrishna

9730490933

Dear Dinesh,

Investing every month before 10th (or) in case of lump sum investment before 10th of April every year, you can get slightly better returns to a certain extent.

Dear Sreekanth,

I wish to open next week for my daughter, kindly clarify the following

1. Is possible to open Post office and SBI (two account for one name)?

2. I wish to deposit lump sump now, is there is possible to change the mode of payment either lump sump/monthly?

3. what is the maximum and minimum amount per year deposit?

Dear shanmugam,

1 – No.

2 – Yes.

3 – Rs 1000 & Rs 1.5 Lakh.

Hi Sir,

My daughter 2 years old. If i start deposit 1000 per month, how much child will be getting while reaching 18th years. Calculator link which you mentioned below doesn’t work. Please provide alternate link or can you calculate and let me know.

Thank you.

Dear Ameen / Sam,

Kindly use the calculator available in this article….click here.