Capital asset typically refers to anything that you own for personal or investment purposes. It includes all kinds of property; movable or immovable, tangible or intangible, fixed or circulating.

Examples include a house, land, household furnishings, stocks, bonds or mutual funds held as investments etc.,

When you sell a capital asset, the difference between the purchase price of the asset and the amount you sell it for is a capital gain or a capital loss. Capital gains and losses are classified as long-term or short-term.

If Land or house property is held for 36 months or less 24 months or less (w.e.f. FY 2017-18) then that Asset is treated as Short Term Capital Asset. You as an investor will make either Short Term Capital Gain (STCG) or Short Term Capital Loss (STCL) on that investment.

If Land or house property is held for more than 36 months more than 24 months (w.e.f FY 2017-18 / AY 2018-19) then that Asset is treated as Long Term Capital Asset. You will make either Long Term Capital Gain (LTCG) or Long Term Capital Loss (LTCL) on that investment.

You may have to pay Capital Gains Tax on STCG / LTCG.

In this post let us understand – How to calculate Short Term capital gains on sale of land or property? How to calculate Long Term Capital Gains on sale of land or house? What are the applicable capital gain tax rates on sale of land / house property? How to avoid / save / minimize capital gains tax on sale of land or flat?

Latest Article : Capital Gains Tax Exemption Options on Sale of House or Plot | Latest Rules 2023-24

How to calculate Capital Gains on sale of Land or House property?

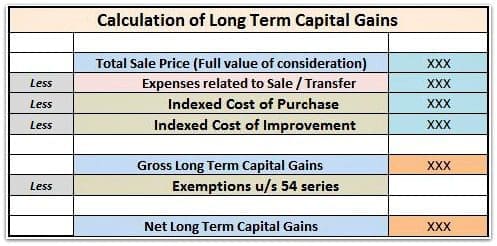

Short Term Capital Gains Calculation is calculated as below:

STCG = Total Sale Price – Cost of acquisition – expenses directly related to sale – cost of improvements.

Long Term Capital Gains Calculation;

The LTCG calculation is similar to STCG. The only differences are, you are allowed to deduct Indexed Cost of Acquisition/Indexed Cost of Improvements from the sale price and also claim certain exemptions to save capital gains tax.

With effective from Financial Year 2017-18, the base year for calculation of Indexation is going to be 2001.

(Indexation is done by applying CII – cost inflation index. This increases your cost base ie purchase price and lowers your gains. Your purchase price is adjusted for the impact of inflation.

How do you calculate the indexed cost of purchase? The indexed cost is calculated with the help of a table of cost inflation index.

Divide the cost at which you purchased the Property by the index as on the date of the purchase. Multiply this by the index as on the date of sale.

For Example : If purchase year is 2011 and year of sale is in Financial Year 2015. Then indexed cost of purchase would be –

Indexed cost of purchase = (Purchase price / 184) * 254.)

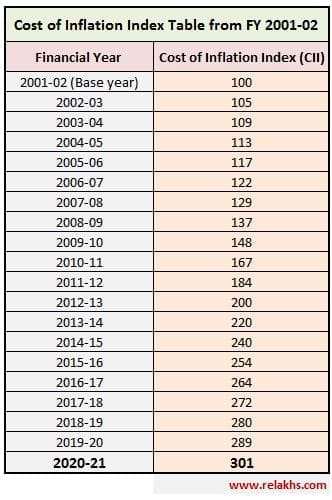

Below is the Cost Inflation Index Table from 2001-02 to FY 2020-21 for your reference. Cost Inflation Index (CII) for FY 2020-21/ AY 2021-22 Notified by CBDT at 280.

What are the applicable Capital Gains Tax Rates on Sale of Property AY 2021-22?

- Short Term Capital Gains are included in your taxable income and taxed at applicable income tax slab rates.

- Long Term Capital Gains are taxed at 20%.

How do I save Capital Gains Tax from sale of Property?

Capital gains tax on Short term gains is unavoidable and no exemptions are available to minimize your tax liability. However, you can claim deductions to lower the tax liability on long-term gains.

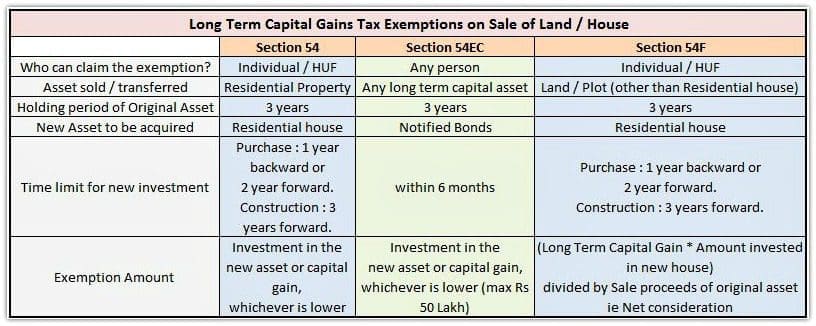

How to save Capital Gains Tax by claiming Exemption u/s Section 54EC? (Applicable to LTCG only, on sale of both land / house property / commercial property)

- Capital gains from sale of any long-term asset can be claimed as tax-exempt under Section 54EC of the Income-Tax Act by investing in notified bonds within six months of the transfer of Asset.

- These bonds are issued by the Rural Electrification Corporation and the National Highways Authority of India.

- The exemption is equal to the investment or the capital gain, whichever is lower. If you transfer or take a loan against these bonds within three years, the capital gain will become taxable.

These are redeemable after 3 years and must not be sold before the lapse of 3 years from the date of sale of the house property.The Bonds issued u/s 54EC for saving of LTCG on sale of property will now have a lock-in period of 5 years instead of 3 years from FY 2018-19.- You are allowed a period of 6 months to invest in these bonds, but before the Income Tax Return filing date (to claim this exemption).

- You can invest a maximum of Rs 50 lakh during a financial year in these bonds as per Budget 2015-16.

How to save Capital Gains Tax by claiming Exemption u/s Section 54? (Applicable to LTCG on sale of house property only)

You can use the entire Long Term Capital Gain proceeds on sale of a residential house to buy another house property (residential property) to save Capital Gains tax. Below conditions need to be satisfied though;

- The new house has to be bought one year before (under-construction property) the transfer of the first house or within two years after the sale. (For an Under construction property or flat , the construction has to be completed within three years of the transfer of the first property.)

- The deduction allowed is equal to the actual investment or the capital gain, whichever is lower.

- If you plan to use the gain to build a house, it has to be done within three years of the sale of the property. Do note that ‘cost of land’ can be included in the construction cost.

How to save Capital Gains Tax u/s 54F? (Conditions applicable to LTCG on sale of Land or Commercial Property)

Below conditions need to be satisfied in case you sell land and are planning to buy a residential home.

- You can use the entire sale proceeds (received by selling a plot / land) to buy a new house or to build a new residential house.

- If you use a part of the money, the deduction will be proportion of the invested amount to the sale price.

- The time-frame for investment is the same as that for capital gains from residential property.

- You should not own more than one residential house prior to this investment.

- The deducted capital gain (from sale of land) becomes taxable if you buy another house (other than the new one) within two years of the transfer of the original asset or construct a new one within three years.

- If the new house is sold within three years, the deduction claimed will become taxable as a long-term gain.

- This new house purchased or constructed must be situated in India.

- The proceeds should not be invested in a commercial property or in another vacant plot.

How to Save Long Term Capital Gains Tax without buying another House Property?

If you are unable to invest the sale proceeds in any of the above options before the date of income tax returns filing , you can deposit the CAPITAL GAINS (not entire sale proceeds) amount in a public sector bank or other banks as per the Capital Gains Account Scheme- CGAS, 1988.

- The capital gain (full amount or utilized amount) can be deposited in CGAS account.

- This is only a stop-gap arrangement, as the funds have to be used to buy or build a house within the period specified.

- The deposited money can be used only to buy or construct a residential house within the prescribed time frame.

- If you withdraw funds from this account, they have to be used within 60 days.

- If you do not utilize the amount within three years of the sale of the first property, such un-utilized amount will be treated as LTCG this will lead to taxation of the unutilized amount as long-term capital gain after three years of the sale of the first / original property.

- The interest rates paid on these accounts are the same as those on regular savings and term deposits. Kindly note that interest earned on this account is taxable.

How to Save Long Term Capital Gains Tax under New Section 54GB(5)?

Under Section 54GB(5) of the Income Tax Act, 1961, long term capital gains on the sale of residential property will be exempt if the sale proceeds are invested in a eligible startup, provided such transfer took place prior to March 31, 2019. As per the latest full Budget 2019-20, this has now been extended to March 2021.

Important points on Capital Gains Tax & Sale of Land / Home

- Agricultural land in a rural area in India it is not considered a Capital Asset, and therefore no capital gains are applicable on its sale.

- While calculating capital gains, expenses related to transfer / sale like advertisement expenses, brokerage expense, Stamp duty, Sale deed registration fees, Legal (lawyer) expenses etc., can be deducted from the Purchase price.

- Sale of a property that is inherited or accepted as a gift will also attract capital gain/loss provisions even though you haven’t spent any money to acquire it. In such a case, capital gains will be computed on the basis of the cost to the previous owner, indexed to the year of purchase.

- If the cost of the new residential property is lower than the total sale amount, then the exemption is allowed proportionately.

- The new property must only be bought on the name of the seller and not on anybody else’s name. Joint ownership can be acceptable but exemption can be limited to the share of ownership.

- You must also remember that you are allowed to purchase or construct only one new asset from the capital gain that accrues. This means that you cannot make multiple property acquisitions and thus seek to reduce your tax outgo. However, if you sell more than one property, you can invest the resulting cumulative capital gain amount in a single new property.

- If you use the capital gain amount to clear loans then tax on LTCG cannot be saved. No exemptions can be claimed.

- Capital Gain Tax cannot be saved if the sale proceeds are invested in a commercial property, agricultural land or plot.

- According to the latest amendments in the Income Tax Act, the residential property which is bought by re-investing the long-term capital gains must be situated in India.If you would like to buy a property outside India say in the US, you need to pay tax on the capital gain portion of the sale proceeds.

Latest Article : Capital Gains Tax Exemption Options on Sale of House or Plot | Latest Rules 2023-24

To summarize;

- Categorize your capital gains i.e., Short term or Long term.

- Calculate Short Term Capital Gains (STCG) / Long Term Capital Gains (LTCG).

- If you have STCG, taxes are payable as per your income tax slab rate.

- If you have LTCG, to save capital gains tax ;

- You may invest the gains in another Residential property (or)

- Buy Notified Bonds (or)

- Temporarily invest in Capital Gains Account Schemes.

- Else, you have to pay 20% on your Long Term Capital Gains.

Calculation of Capital Gains Tax on sale of property can be sometimes be a tricky one. It is advisable to exercise caution when claiming Capital Gains Tax Exemptions. When in doubt, kindly consult a tax expert or a Chartered Accountant.

Continue reading :

- Is Income from Agriculture Taxable? How to Compute Income Tax on Agricultural Income?

- How to calculate Holding Period & Capital Gains on sale of an Under-Construction property?

- Can a Mortgaged property be Gifted, Willed or Inherited?

- Sale of Inherited (or) Gifted Property & Tax implications on Capital Gains

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net)

Join our channels

I am selling a residential house. From the capital gain arising out of this sale I want to buy a residential plot from A . Invest the remaining capital gain in a capital gain account and start construction after 6 months through a contractor B. Will complete construction within 10 month from start.

Can I get exemption from capital gain for total amount including cost of land.

I am selling my plot for Rs 30lacs purchased in 1993 for Rs 25000. My expenses for improving etc are rs 1lac . Please caculate LTCG AND TAX?

Dear Pramod,

Total Cost of Acquisition with Indexation is Rs. 87000.

You need to provide the date of incurring cost of improvement for the calculation of indexed cost of improvement.

I purchased BDA plot at Rs. 4.2 L in yr 2003 and now ( Jul/Aug 2023) selling for Rs. 1.31 Cr. Could you pl suggest best Tax saving investment plan.

Regards

Dear Chandra Sekhar,

May I know, if you have any obligations to meet with this Rs 1.31 cr?

Or you would like to re-invest anywhere else?

Did you receive the entire sale proceeds in non-cash mode?