The National Savings Schemes (NSSs) are one of the very popular saving schemes in India. These are regulated by the Ministry of Finance. They offer complete security of investment combined with attractive returns.

These schemes also act as instruments of financial inclusion especially in the geographically inaccessible areas due to their implementation primarily through the Post Offices, which have reach far and wide.

It is estimated that nearly $137 billion or over Rs. 9 lakh crore are tied up in small savings schemes.

Some of the very popular schemes which fall under NSS are as below

- PPF (Public Provident Fund)

- Sukanya Samriddhi Scheme

- Monthly Income Scheme

- Senior Citizen Savings Scheme

- KVP (Kisan Vikas Patra)

- NSC (National Savings Certificate)

- Time Deposits &

- Recurring Deposits

Small Saving Schemes Interest Rates & New norms w.e.f. April 2016

Let’s have a look at what are the changes that have been implemented regarding Small saving Schemes’ interest rates;

- As per the current norms, the interest rates of these small saving schemes are linked to the yield of government bonds of comparable maturity (with a small mark-up) and are revised once a year. Mark-up here refers to ‘Spread’.

For example : The interest rate on PPF has a mark-up of 25 basis points over and above the G-Sec rate (Govt Bonds rate). So, if comparable maturity G-sec rate is say 8.5% then the interest rate on PPF will be determined as 8.75%. (One Basis Point is equivalent to 0.01%)

- The government has decided to revise Small Saving Schemes Interest Rates on a Quarterly basis.

- The saving schemes like Sukanya Samriddhi, Senior Citizen Savings Scheme and Monthly Income Scheme enjoy ‘spreads’ over the G-sec rate of comparable maturity viz., of 75 basis points (0.75%), 100 bps (1%) and 25 bps respectively. These mark-ups / spreads have been left untouched by the Government.

- Similarly the spread of 25 basis pointss that long term instruments, such as the 5 yr Term Deposit, 5 year National Saving Certificates (NSC) and Public Provident Fund (PPF) currently enjoy over G-Sec of comparable maturity, have been left untouched.

- The 25 bps (0.25%) spread that 1 year, 2 year and 3 year Term Deposits, KVPs and 5 yr Recurring Deposits have over comparable tenure Government securities, shall stand removed w.e.f. April 1, 2016 to make them closer in interest rates to the similar instruments offered by the banking sector.

- The interest rates on a 10 year National Saving Certificate (discontinued since 20-12-2015), 5 year National Saving Certificate and Kisan Vikas Patra is compounded on half-yearly basis. This shall be done on an annual basis from 1st April, 2016.

- Premature closure of PPF accounts shall be permitted in genuine cases, such as cases of serious ailment, higher education of children etc,. This shall be permitted with a penalty of 1% reduction in interest payable on the whole deposit and only for the accounts having completed five years from the date of opening. (Read : ‘PPF Account pre-mature closure – latest rules, eligibility & amount calculation‘)

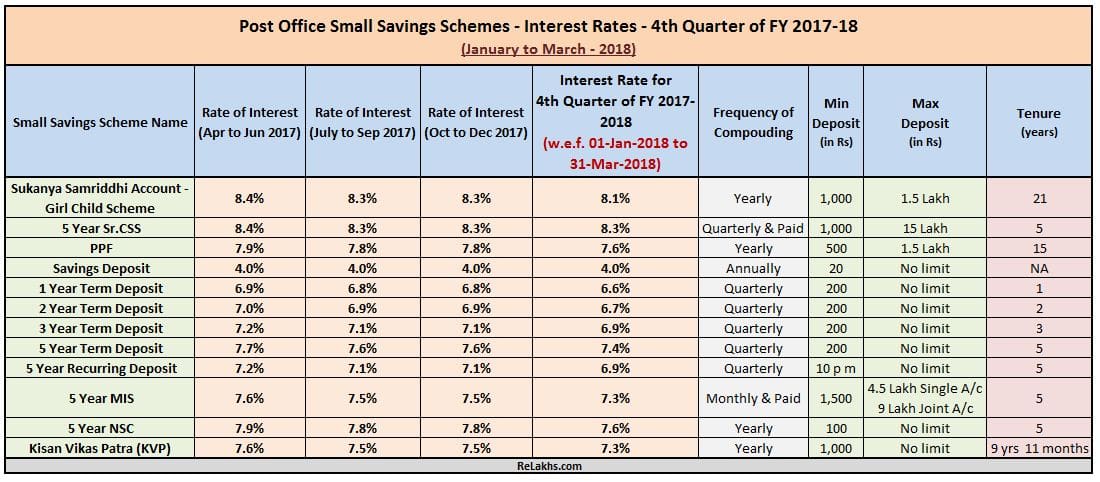

Latest Post office Small Saving Schemes Interest rates FY 2017-18 (January to March 2018)

Kindly note that the Govt of India has reduced the interest rates by 0.2% for 4th Quarter of FY 2017-18 (except for Sr. Citizen Savings Scheme). The rates of interest applicable on various small savings schemes for the quarter from Jan to Mar 2018 effective from 1.01.2018 would be as below;

- The new rate of Interest on Sukanya Samriddhi Scheme (SSA ) is 8.1%.

- The new rate of Interest on PPF (Public Provident Fund) would be 7.6%.

- The interest rate on Senior Citizen Savings Scheme (SCSS) has been retained same at 8.3%.

- New interest rate on Kisan Vikas Patra (KVP) would be 7.3%.

- The rate of interest on 5 year National Savings Certificate (NSC) is 7.6%.

- New interest rate on post office MIS (Monthly Income Scheme) is 7.3%.

- The rate of interest on a 5 year Post Office RD (Recurring Deposit) would be 6.9%.

(Click on the above image to open it in a new browser window)

Latest News (20-10-2017) : Govt allows all Public Sector Banks and three Private Banks (ICICI, HDFC & Axis) to accept deposits under Small Savings Schemes like National Savings Certificate (NSC), Recurring Deposits and Monthly Income Scheme (MIS).

Latest update (07-Oct-2017) : Aadhaar now a must for Post office Deposits, PPF, National Savings Certificate (NSC) and Kisan Vikas Patra (KVP). The Existing investors of these deposits have to submit their Aadhaar numbers by 31 March, 2018. (Read : ‘Important Dates & Deadlines for Aadhaar linking with PAN, Mutual Funds, Insurance Policies & Mobile SIM.’

Continue reading :

- Why you should not invest in Fixed Deposits / RDs for long-term?

- Are you aware of this interesting fact on Bank Fixed Deposits?

- Tax Saving investment options u/s 80c : In whose name can they be invested?

(Source : PTI) (Post first published on 31-March-2017)

Join our channels

(5*)FIVE STAR OUT OF FIVE (5*) RATING AGENCY TO PROVIDE FREE OF COST SERVICE TO CLIENTS/CUSTOMERS.

BEST FINANCIAL ADVISER, HASSLE-FREE SERVICE TO PUBLIC FREE OF COST.

Hi srikanth

Can you give me advice some scheme to deposit money monthly wise in post office for further future plan

Dear Arun,

May I know your investment time-frame & financial goals?

Have you invested in other investment products?

I am retired person. Retired from a PSU organisation. I have no pension. I have only CPF . Please adv. me that where to invest my retirement proceeds with hight interest in monthly/quarterly in government msector.

Dear sujoy ji,

You may kindly go through this article @ Best investment options for retirees..

Hi Sreekant,

Thanks for your suggestions and guidance…..

I have one query…..For senior citizens which Fixed deposit schemes will yield high intrest rates…….pls suggest secured organisation like post office, public sector banks……

Thanks

Dear Karthik,

Kindly go through below articles ;

Investment options for Senior citizens

List of best investment options

Hello Sir , I want to invest 1.00 Lac in MIS for 5 years & re-invest monthly interest amount in RD for 5 years

Plz advise how much maturity amount i will get after 5 years

Regards

Dear Sanjay,

May I know the objective of re-investing the monthly interest income??

You may visit this link and use the available calculators.

Just to increase maturity value

Dear Sanjay,

If that is the case then you may pick any other alternative to accumulate your wealth instead of investing the money twice??

Suggested readings :

List of best investment options!

i am sevenig money ..in post office ..save the my family..these schemes heal tha poor peoples……..tank to post office…

can i invest under senior citizens savings scheme short term deposit for 6 months. if s what is the interest rate. what is the maximum amount that a senior citizen can invest.

Dear Mr Rao ..There is no maximum limit as such for term deposits..

I think minmum period is 1 year and the current prevailing rate is 6.8%.

Hello Sir,

I have a query. My question is that I have opened RD for 5 years since 2013 at that time rate of interest was must probably 7.8 %, later while checking postal site, its states that rate of interest revised of 7.1%. How much of rate interest shall i get at the time of maturity ?

Thanks & Regards

Shashikanta Prusty

Dear Shashikanta ..The rate that was mentioned at the time of booking of RD is applicable (not the current market rate).

Hi Shreekanth

What invest option in India for fixed monthly highest income for and NRI you can suggest?

Thanks

A. Rangwala

Dear Aftab ..May I know the age of the person & investment time-frame ??

The Age is 60+ and time span can be 3 years.

Dear Aftab..Can consider SWP (Systematic withdrawal option) in Short Term debt fund / MIP (conservative – Growth option) fund.

Kindly read :

Best MIP Funds

Types of Debt funds.

how much i will get back matirity for nsc rs.25000/=

sir i want to invest 20 lakh in tax free for any monthly/ yearly scheme .plz suggest methank you

Dear mukeshkumar ..Do you mean to say that you would like to receive monthly tax-free income from a lump sum investment?

sir i have open atal pension yojna APY in 2015 and continuously 1000/- is deducted per month from my account. after 2 year i feel that APY is not good decision. instead of APY we can invest in some bank saving scheme. please suggest me, it is good or not

Dear Abhishek ..To get inflation adjusted positive return, I believe one can consider other options like shares, equity mutual funds for long term goals like Retirement planning.

Read: List of best investment options!

I opened NPS TIER 1 ON 25 MARCH 2016 WITH AMOUNT 50000/-PLUS A/ C OPENING PRAN CARD ISSUED ME & DISPATCHED ON 30.03.2016 CAN I CLAIM INCOME TAX REBATE OVER ABOVE Rs 150000/- that is 50000/-under sec 80cc(IB) i.e.200000/-

Kindly advice me

Dear VIPAN ..Yes, you may do so.

Read :

List of IT exemptions for FY 2016-17.

List of IT deductions for FY 2017-18.

Dear Sir,

The information provided are very useful.

Thanks & regards,

Nand Kumar Yadav

Mr.Sreekanth thank you very much for this wonderful site which is very helpful to my investments,.i am planning to invest in real estate so is this a right to invest in real estate in chennai, its for a investment purpose and what legal things need to followed while buying a property,how do i find good property i mean how do i choose, what things need to be checked when buying a properties.once again this information are very use full and easy to understand.thanks for it.

Dear priya,

In most of the metro cities, real estate prices have either corrected slightly or have been stable for the last few months/1 year or so.

We may see turn-around in realty sector due to the initiatives taken by the Govt.

May be this Financial year is a good time to own a property.

You have to ask for Mother deed, link Sale deed, Property tax receipt, Mutation record, latest Encumbrance Certificate, Local civic body approval document (if any) etc from your prospective seller.

Are you planning to take home loan?

Please give me advice how I can manage my finances in a better way.

Dear Subrat ..Kindly go through this article and you may revert to me with more queries;

List of important articles on Personal Financial Planning!