Kisan Vikas Patra Yojna has been relaunched by Government of India on 18th November,2014. The Kisan Vikas Patra scheme was originally launched in April, 1988 but was discontinued in 2011. This was a very popular financial product among the lower and middle income group.

Main Features of Kisan Vikas Patra are:

- Safe investment scheme for small income group.

- The scheme will give you annual return of 8.67 %. Interest is compounded annually.

- Your investment will be doubled in 100 months or in 8 years 4 months.

- You can purchase this scheme from a post office. Soon this will be made available in Nationalized Banks too.

- The re-launched KVP will be available in the denomination of Rs 1,000, 5,000, 10,000 and 50,000, without an upper ceiling on investment.

- KVP certificates can be bought in single or joint names.

- You can pledge KVP certificates as security to avail loans from banks

- Only individuals can invest in KVP. You can invest on behalf of a minor too. But Companies, NRIs, HUFs etc., can not buy these certificates.

- Nomination facility is available on KVP.

- You can transfer kisan vikas patra certificates from one post office to another one, anywhere in India

- There is a lock-in period of 2 years and 6 months. After 2.5 years and thereafter in any block of six months you can encash the certificates. Redemption will be at pre-determined maturity values

- Interest on KVP will be taxed at 10% TDS ( if you are in different income tax slab then you have to club to your income and file Income tax returns accordingly)

- KYC (Know Your Customer) rules are applicable on your KVP investments. You have to submit required documents while investing in KVP.

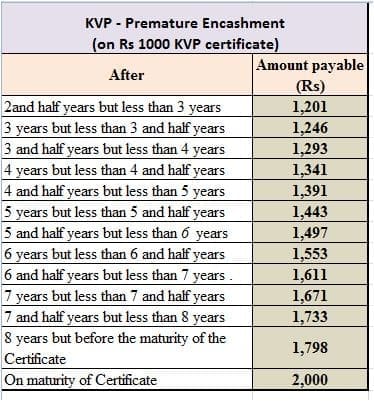

Premature Encashment of KVP & Amount Payable

Premature Encashment or withdrawal of KVP certificates will be at pre-determined maturity values as below. To invest or not to invest in Kisan Vikas Patra? (KVP vs Bank Fixed Depostis)

To invest or not to invest in Kisan Vikas Patra? (KVP vs Bank Fixed Depostis)

- The current interest rates on bank fixed deposits for 8 year term are around 8.5% (around 9% for senior citizens). We can soon expect reduction in interest rates by RBI in the coming quarters. Even if RBI reduces interest rates, the expected annual yield on Kisan Vikas patra which is 8.67% is not a great return on investment. (You may like visiting my post on “information on RBI rates.”)

- Also, investments in KVP are not eligible for any tax benefits under Section 80c. If you really want to invest in a safe investment avenue then you can book a 5 year Bank Fixed deposits and get tax benefits too.

- KVP does not have tax benefits and Lock-in period is applicable.

- Consider investing in Public Provident Fund (15 years lock-in will be there) if safety is your priority.

- You can consider investing in National Savings Certificate (NSC – 5 years) which is available at 8.5% interest rate. Also, it has tax benefits too (under section 80c)

Do not just buy Kisan Vikas Patra as it is a safe investment option and promoted by the Government. Before buying KVP certificates, identify your investment requirements first and then compare KVP scheme with other similar investment avenues like Bank fixed deposits, Post office NSC/PPF etc., (I will try to update this post with more details ..Cheers!)

Government’s Press note on Kisan Vikas Patra . Click here for KVP application form. Click here for Application form for transfer of KVP Cert from Bank to Post office & Vice Versa.

Latest News (28-June-2016) : The sale of Pre-printed NSC (National Savings Certificate) & KVP (Kisan Vikas Patra) Certificates will be discontinued w.e.f 01-July-2016. Henceforth, the certificates shall be recorded in a Passbook. Detailed Procedure for accepting deposits for issue of NSC/KVP in the shape of Passbooks shall be issued shortly by the Ministry of Communication & IT (Dept of Posts).

Latest News (18-March-2016): The Govt has cut rate of interest on Kisan Vikas Patra (KVP). The new interest rate on KVP would be 7.8%. This will be effective from 1st April, 2016 to 30th June, 2016. Your investment will now be doubled in 110 months or in 9 years 2 months. For complete details on revised interest rates of Small Savings Schemes, click here..

Join our channels

I THINK KVP IS BEST FOREVER.

Retire on 31/3/2005&my date of birth is 3march1947 whose policy is better

Pl send best policy as a senior citizen &age is 3/3/47

Dear Sreekanthreddy,

Will you please suggest a better yield with tax benefit plans..

Your opinion on u.t.i retirment plan investing as s. i p .

Dear Dr.Parvathidevi,

Suggest you to invest in Equity Linked Savings Schemes of mutual funds for tax-saving cum long-term wealth creation of wealth.

Kindly read my articles on;

Best ELSS funds

Best equity funds.

Kishan ke liye kya mila lon chhahye

i want to kisan vikas patra9

Thanks for a good analysis of the scheme.

Thank you for your comment.

Hi Sreekanth,

Now Financial Ministry relaunches KVP , they mentioned PAN number is not required, may be they are in- directly offering black money to the indian growth, if pan card is not necessary how TDS will come into picture??, any changes in tax scheme in present KVP??

Hi Pavan – Recently govt has made KYC mandatory for all National Savings Schemes too. Let us wait for more clarity on PAN requirement. I think as per Govt notification PAN is mandatory if investment amount is more than Rs50k. I believe the KVP maturity amount will be credited to Post office savings account (or) Bank account only. No cash payment will be made.

will you pl.compar it with VARISHTHA PENSION BIMA YOJANA/L.I.C. ?

Hi Uday – VPBY is a pension plan. Investor can pay single premium and get periodic pension. There is a ceiling on maximum receivable pension which is Rs 5,000 pm. The expected return on Varishtha plan is 9% p.a. Both the schemes do not have any tax benefits.

Hi Sreekanth,

Thanks for sharing this .

This blog gives very clear and crispy information regarding KVP and what is good / not good with other investments (like PPF) comparison. You are on-par with latest updates in the market .

Thanks for your time !!!

Hi Rajendra – Thank you for the comment.