Today is March 31st, the final day of the Financial Year 2015-16. Financial year starts from 1st April and ends on 31st March. There are many new amendments or changes that have been proposed for the next Financial Year (2016-17).

In this article, let’s discuss some of the major Personal Finance changes that you need to know. Some of these new proposals might affect most of our personal finances.

FY 2016-17 & Personal Finance Changes

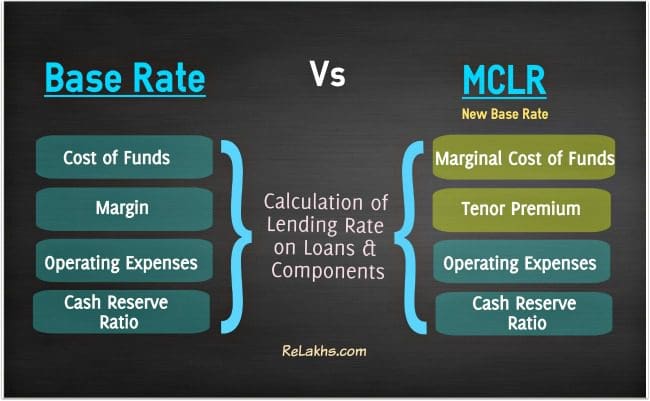

- Home Loans : The Reserve Bank of India has issued new guidelines for setting lending rate (on loans) by commercial banks under the name Marginal Cost of Funds based Lending Rate (MCLR). It will replace the existing base rate system from 1st April, 2016 onwards. As per the RBI’s new guidelines, it is mandatory for the banks to consider the repo rate while calculating MCLR with effective from 1st April, 2016. (Read : MCLR, new Lending Rate – Details & Review)

- Taxation Proposals :

- Service tax will be increased from the existing 14.5% to 15%.

- Budget 2016 proposes to levy 10% Dividend Distribution Tax (DDT) in the hands of the investor who receives dividend of Rs 10 Lakh or more in a financial year.

- Cash purchases of goods & services which are worth more than Rs 2 Lakh & purchases of luxury cars worth more than Rs 10 Lakh will be subject to Tax Collection at Source (TCS).

- Central Board of Direct Taxes (CBDT) has informed that the interest income earned on deposits should be shown in the return of income even in cases where Form 15G/15H has been filed. The interest income has to be shown in ITR if the earning is not exempt under Section 10 of the Income-tax Act and the total income of the person exceeds the maximum amount not chargeable to tax.

- According to the Budget 2016 proposals, sovereign gold bonds will be exempted from capital gains (LTCG) tax at the time of redemption. So, if you hold the gold bonds till the maturity date and if you make any long term capital gains when redeeming your gold bonds, there will not be any capital gain taxes on the profit you make.

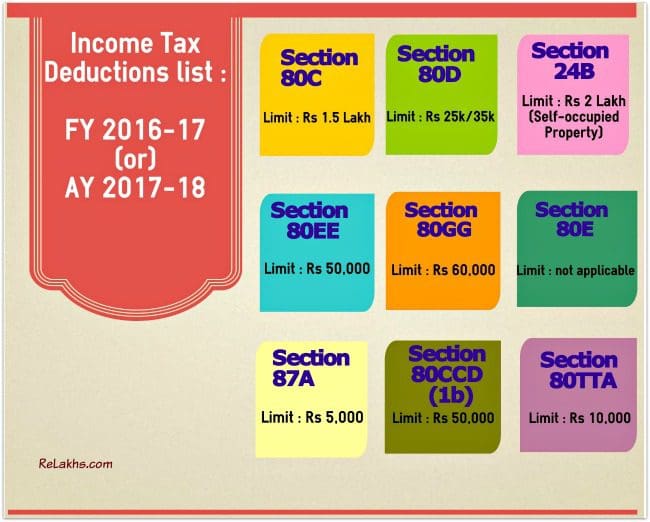

- For complete List of Income tax deductions for FY 2016-17 (or) AY 2017-18, click here..

- For detailed List of TDS rates for FY 2016-17, click here..

- NPS Withdrawal : 40% of corpus withdrawal at the time of retirement will be tax exempted. 60% of the corpus will be subject to tax if you withdraw it. To avoid taxes, you have to invest this 60% corpus amount in an Annuity product. Death claim (if any) received under NPS scheme is tax exempt. One-time portability from EPF to NPS will be provided and this will not be subject to any taxes.

- Inoperative EPF Accounts : The Employees Provident Fund Org has decided to provide Interest on Inoperative Accounts from 1st April, 2016. This move will benefit over nine crore such account-holders having total deposits of over Rs 32,000 crore.

- Motor Vehicle Insurance : Third party motor insurance premiums to cost more from April as premiums will be hiked by up to 40%. (Read : What is third party insurance?)

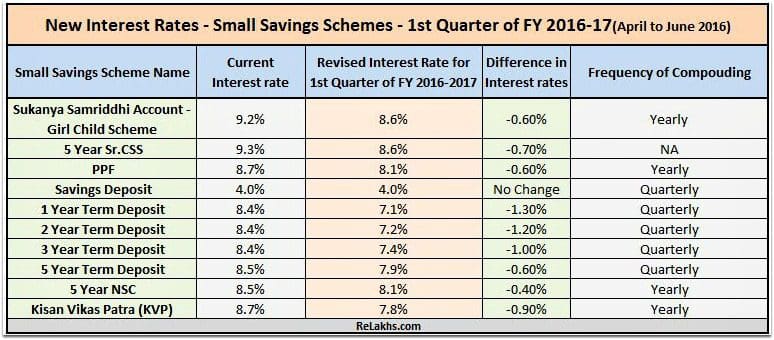

- Post Office Saving Schemes : The government has decided to revise Small Saving Schemes interest rates on a quarterly basis starting from 1st April, 2016.

- High Value Financial Transactions: With an aim to curb black money mess and to track high value cash transactions, the government has decided to implement new reporting guidelines w.e.f 1st April, 2016.

- Immovable Property : The Registrar of properties will have to report purchase & sale of all immovable property exceeding Rs 30 Lakh to the Income Tax authorities.

- Professionals : The Professionals will be required to inform the tax department of receipt of cash payment exceeding Rs 2 lakh for sale of any goods or services.

- Cash Deposits in Banks : Banks will have to report cash deposits aggregating Rs 10 lakh or more in a financial year in one or more accounts of a person.

- Term Deposits in Banks : Banks will have to report cash deposits aggregating Rs 10 lakh or more in a financial year in one or more Time Deposit accounts of a person. These norms will also cover deposits and withdrawal made in Post Office Account.

- Deposits in Current Accounts : Cash deposits or withdrawals aggregating to Rs 50 lakh or more in a financial year in one or more Current Account of a person will have to be reported by the bank to the I-T authorities.

- Any cash payment of Rs 10 lakh or more in a financial year for purchase of bank drafts or pre-paid instrument issued by RBI will also be reported.

- Investments in Financial Securities : A company has to report receipt of Rs 10 lakh or more from a person/an investor in a financial year for acquiring bonds, debentures, shares or mutual funds.

- Bank Savings Account: Reserve Bank of India (RBI) has asked Banks to pay interest on savings banks account on quarterly basis or shorter intervals from next Financial Year. Though the interest rate on Savings account is calculated on a daily basis, at present the interest amount is credited in savings bank account on half-yearly basis (every 6 months) only.

- Real Estate Bill – The real estate bill which has been pending before the parliament since August 2013 has finally received the parliament’s nod. This bill is expected to be beneficial to home buyers and can attract the much needed capital flows into the realty sector. (Read : Real Estate Bill & Benefits)

- ECS (Electronic Clearing Service) will be replaced NACH (National Automated Clearing House) from 1st April, 2016. NACH is a centralized system which will consolidate multiple ECS systems that are currently available in the country. All banks have to switch to this new platform by 1st May, 2016. So, from May 2016 onwards you have to use this facility instead of ECS. This is applicable to all your Utility Bills, Insurance Premium payments, Credit Card Bills, SIP of Mutual Funds, or in fact any payment, which is recurring in nature. Kindly note that your existing ECS mandates will not be affected. But fresh registration of ECS will not be accepted.

Also, the long-pending GST Bill if implemented in the next Financial Year could be one of the major reforms and can be a game-changer for the Indian Economy. (Read : What is GST Bill?)

The government has also proposed to launch ‘Start-up India’ mobile APP & online portal in the month of April 2016. Registration of a startup company can be done in a single day through Startup India Mobile app / portal.

The much awaited online EPF withdrawal facility might be launched by the EPFO during the next FY.

I hope you find this post informative and useful. Kindly share your comments and also, please bring out any other important personal finance changes that I might have missed. Happy New Financial Year 🙂

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net) (Post published Date : 31-March-2016)

Join our channels

Dear sir,

I am sudhakar working in a public sector bank I have been a avid reader of your blog I like the analysis very much. I request you to kinldly advice me on stocks purchase as I have a trading account in sbi kindly suggest me best stocks I can afford 20k for long term investment on stock purchase

regards

Dear sudhakar..Kindly note that I do not provide suggestions on direct equity (stocks).

fantastic Article..Good Finacial Year start for everyone with this article. Thank you very much for sharing with all of us.

Hi

Have been reading all the wonderful info u provide.

Can u also make a few suggestions for NRI ‘s on how to plan their investments.

Thanks

Dear Deepti,

Thank you for following my blogs.

Whether NRI or Resident Indian, the starting point would be Financial Goals and then we can identify the right products based on the investment objectives/time-frame.

So, if you are an NRI and would like to ask any specific queries related to NRI investments, do leave your queries and I will surely try my best to reply to them at the earliest.

Thank you so much for ur reply.

Well, I’m a 33yr old and gulf based with savings of 30lakh p.a. since 2 yrs. I have a

1. LIC Jeevan bhima yojna of 80k p.a

2. Rest in fixed deposits in senior citizen names or nri account

4. 25k/month in mutual funds.

Should I invest in property or stock markets or increase the mutual funds?

Will I be taxed if the benefits of the mutual funds increase by more than 2.5lk p.a?

Wat are the best ways to avoid taxes?

Thank you for your patience and time.

Dear Deepti,

1 – Kindly share details of LIC policy (plan name, commencement date, tenure).

2 – Kindly read: Why one should avoid investing in FDs for longer period?. Are these investments towards any specific goal(s)?

3 – May I know your investment horizon & goals? If ok, share your MF portfolio details.

Read:

The 6 most common personal finance mistakes..

Financial planning pyramid.

List of best investment options.

Hi Shrikanth

Good article, informative keep it up. Thanks

Thank you dear Srikanth sir for stopping by and leaving your comment! Keep visiting 🙂

Informative article.

Investment in financial securities need some clarification. Earlier 2 lakh and above in MF, 5 lakh and above in bond/debentures, 1 lakh and above in shares etc. were reported through AIR.

Now article states that a company has to report receipt of Rs 10 lakh or more from a person/an investor in a financial year for acquiring bonds, debentures, shares or mutual funds.

Does this mean that limits set earlier in AIR have been revised upward to Rs 10 lakh and above?

Kindly elaborate.

Thanks

Dear Mahesh..Yes these are the new limits and effective from 1st April, 2016.

Dear Sreekanth,

Since I am affecting a switch more than the present limit, I talked to my MF customer service and they say the limit for AIR reporting remains at Rs 2 lakh only.

Can you please help me with relevant rules, sections of recent budget which can be shown to them.

Thanks.

Dear Mahesh..As of now I couldn’t trace out the relevant notification, but I believe that the new limit is Rs 10 Lakh.

Thanks a lot for the information. Have a doubt.With the introduction of MCLR , as a simple home loan EMI payer, how is it going to affect me??

Dear Shrikant,

Suggest you to kindly go through this article and revert to me if you need more info : MCLR – Details, components & Review.

Thanks a sir for the above info…Keep it up ..

Thank you dear Jitendra ..Keep visiting!

Thnx for providing such h a valuable info at one place.Keep it up dear.

Thank you dear Rakesh..do share the article with your friends 🙂

Thanks Sreekanth for consolidated everything and sharing.

It really helps everyone!

Keep up the good work as always!

Regards,

Shravan

Dear Shravan ..Thank you! Kindly share the article with your friends.

Awesome article. Thanks for such a nice info in one go!

Thank you Deepak. Keep visiting 🙂