Financial planning is about developing strategies to help you manage your financial affairs and meet your life goals.Most of us spend too much time concentrating on only one aspect of Financial Planning i.e., Investment Planning (we can call it as Wealth Accumulation). We tend to invest our time and energy in identifying Investments that can generate High returns. In the process, we neglect or ignore other important aspects of Financial Planning. Let us understand about the other important aspects of a solid Financial Plan.

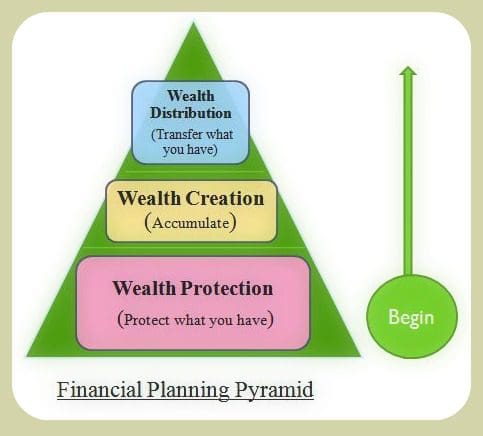

Blocks of Financial Planning Pyramid

I have created a Financial Planning Pyramid with three pyramid blocks as below. All these blocks are equally important. Let us understand these..

1. Wealth Protection :

Ideally you have to start creating your financial plan with Protection Planning. You need to first protect ‘What you have‘. It can be your Life, Health, Property, Vehicles etc., Plan for sufficient insurance coverage and buy right products to cover the risks associated with all these. Another important point is to ‘create and maintain an Emergency Fund.’ This can be to the extent of 3 to 6 months of your monthly living expenses. But, do not invest this fund in risky investment products. The main objective of maintaining this fund is to have ready cash to meet any unforeseen emergencies. Besides these two points, you can concentrate on maintaining a monthly Budget. Track monthly cash inflows and cash outflows.You can plug any leaks by doing this exercise.

2. Wealth Accumulation :

Most of us concentrate more on ‘how to create wealth.’ Undoubtedly this is an important aspect of your financial plan. But, accumulation without having a proper protection plan may prove costly when you have to face bad times.

Once you have developed good Protection Plan then go ahead and create list of realistic Financial Goals. Examples of accumulation goals can be ‘creating corpus for your Retirement’, Kid’s education goal, ‘purchasing a Property’ etc.,

Select suitable investment products based on the time-frame of your goals. Do not hesitate to invest in risk-oriented products like equity mutual funds or shares for your long term goals. Once your have allocated your savings towards each goal then continuously monitor your portfolio. If required change your asset allocation (Debt vs Equity) .

(You may visit my post on “How to create a Solid Investment Plan?“)

3. Wealth Distribution :

This is also known as Estate Planning. It is the most neglected aspects of Financial Planning. Let us assume you have created a good protection plan and good wealth accumulation strategies. But, what is the use of building assets and buying insurance policies if you have not mentioned proper nominations on your investments.

If the head of the family dies without leaving a Will (Intestate) or without mentioning the nominee names then it is an upheaval task for the legal heirs to access the investments/assets. We have lot of high profile examples for this, like Dhirubhai Ambani, Abraham Lincoln, Picasso, Agatha Christie, who died without writing a Will.

Estate Planning is the process of making a plan in advance and naming whom you want to receive the things you own after you die.It is very easy to write a Will. You can now create Wills through online Will drafting websites like LegalDesk.com, Ezeewill.com etc.,

(You may visit my post on “Now, write your WILL online.“)

In the below image I have included the action items /tasks in the blocks of Financial Planning Pyramid. You may find Tax planning in the below image. Tax planning is a tool but not a Goal in itself. You can create a good tax plan so that it helps you in identifying tax efficient investment options. But, remember it should not be the sole criteria to invest in a financial product.

Financial Planning is a dynamic process. It is not a one time activity. Have you created a sound Financial Plan incorporating all the above blocks of Financial Planning Pyramid? Share your thoughts.

Continue reading :

- List of Articles on the key Components of Personal Financial Planning

- The importance of numeracy in becoming Financially Literate!

- Checklist For Attaining Lifelong Financial Fitness

(Image courtesy of Stuart Miles / FreeDigitalPhotos.net)

Join our channels

I wish to use ITR2 to show STCG. However, sheet ‘CG’ the various items are confusing. Kindly guide me againsr which item number in CG should I show the following STCGs:

1) STCG on sale of TAX FREE BONDS.

2) STCG on sale of Equity Shares.

3) LTCG on sale of EQUITY ORIENTED MF. (should this be under EI sheet (Exempt Income)?)

Dear S.K.

Suggest you to kindly take help of a CA.

My wife’s brother has gifted her Rs 1.25L from his NRE Account. Is it compulsory to show this amount in ITR? Should this he shown under ‘EXEMPT’ income? Worried that her RGESS INVESTMENT benefit would be nullified if this amount is added to her GROSS overall income from ALL SOURCES whuch amounts to around Rs.11.7L. Please advise a solution.

Dear S.K.

1 – Yes, you can show it under EI schedule.

2 – This is only for reporting purpose and I believe that there is no need to add to her gross income.

Sir, Thank you for responding. Total GROSS INCOME without deductions should be less than 12L to qualify for RGESS deduction. My wife’s total GROSS Income is already 11.7L If I add the GIFT if 1.25L even under EXEMPT INCOME the GROSS Income will total upto 12.95L, hence I will exceed the RGESS Limit of 12L. Please clarify/advise & oblige.

Hii

I am 25 yrs old.

Below are my investments:

HDFC Pro Growth Plus ULIP (Balanced Fund) : Rs 4166 pm. Period:10 yrs

HDFC Click 2 invest ULIP(Opportunities Fund) : Rs 3000 pm. Period: 5 yrs investment returns after 20 yrs but can cut it down

I am also saving Rs 10000 pm in RD

and Rs 8000 pm in PPF

I have a term insurance:

HDFC click 2 protect plus: Rs 13000 annually.

Have an Car EMI : Rs 18000 pm

My current goals are to buy house after 5-6 yrs

And wealth creation

I want to invest in MFs and ELSS

PLZ ADVICE.

Also plz suggest How to invest in MFs and ELSS online?

Dear Himanshu,

May I know what do you mean by ‘returns after 20 years but can cut it down’?

Are you satisfied with the performances of your ULIP policies?

Any specific investment objective for saving Rs 10k in RD?

If your investment horizon is around 5 years, you may consider investing in a balanced fund. If you have tax saving as one of the investment objectives then consider investing in Franklin Taxshield, but kindly note that the units will be locked for 3 years.

Kindly read:

Best ELSS Funds.

Download the calculator to know the required savings (approx) to reach your goal amount.

The 6 most common personal finance mistakes..

Hi Sreekanth,

Thank you so much for reply, I appreciate your time.

I can’t close TATA AIA ULIP because as per T & C of policy if I close prior to 9 years I’ll get only 75% of total fund value which is less than my investment (total paid premiums). I have completed 7 years and only Rs. 9000 surplus as of now. To get at least all my paid money, I should stay invested for next 2 years. I have switched to Equity fund and I am sure I’ll not be in loss after 2 years. As of now I could not find any better option if I surrender that policy and invest that lump sum amount. So that’s not a problem, I’ll continue as of now.

Request you to advise me on other problems. Apart from my regular income of around 14L, I earn about 4-5L doing some part time work as well from professional websites and get paid though PayPal or Direct transfer to my bank account.

If you are having any consultancy charges, please let me know. I need serious financial planning.

What do you suggest for following investment options? ( I am going to exhaust 80C limit in this year any how.)

I am going to start Rs. 84000/annum for Sukanya Samridhdhi Scheme.

How much should I invest minimum on Axis LTE – ELSS as you replied previously ?

It would be great if you can suggest some specific MFs to invest irrespective of tax saving.

Should I go for PPF, NPS, Rajiv Gandhi Equity Saving Scheme, National Saving Certificate? If yes, how much amount?

I don’t have any specific financial goals apart from Retirement(60-70) and Home (3-5 years later). I may move to abroad in this year and can earn more.

Looking forward for many more interactions.

Thanks,

Sandeep

Dear Sandeep,

Kindly do not start your Financial plan by identifying the financial products.

Its better to identify/set your financial goals first and then pick right investment avenues.

Read: How to create a solid investment plan?

Retirement Goal: Use the calculator and find out avg (approx) savings required to achieve accumulate your retirement corpus.

Retirement planning goal calculator.

Also, read: How to calculate the Future Value of investments through MS Excel?

You may enhance your term insurance cover at the earliest + buy a personal accident insurance plan.

Hi Sreekanth,

Very nice articles. I am a fan of your articles.

I have few questions about my financial planning.

Current Position:

Salary: Around 90,000/ month + 100000 annual bonus

Term plan : HDFC Click2protect, Sum Assured : 25L, Planning one more of Rs. 50L

ULIP: Tata AIA, 2083/month, can’t close before 2018, will continue, fund switched to equity, Total investment Rs. 224000

MF: Axis LTE dividend, In loss so investing just Rs.500/month ( What is 3 years lock-in period? Does that mean, I can withdraw Rs.500/month after 3 years or the entire amount) What is RTA? Total investment: Rs. 35000 only

Rented Flat: Rs.13750/month

No other investment.

Please more better options.

Thank you,

Sandeep

Dear Sandeep,

May I know why you can’t close TATA policy? What’s the reason?

ELSS Fund : It is an equity oriented fund, so don’t worry about short-term fluctuations in returns.You got to remain invested for longer period.

The funds allotted under each SIP will be locked for 3 years. So, the units allotted in say Jan 2016 can be redeemed only after Jan 2019.

Read: Best ELSS funds.

Read:

The 6 most common personal finance mistakes..

List of best investment options.

Hi,

I am saving monthly 10k which I want to park in scheme where both liquidity and good returns are available.

FD and RD are not options as interest rates are low will decrease further.

I was evaluating option of liquid funds/ultra-short term funds or Monthly income plans (MIP).

Can you suggest me in which schemes should I invest. Also I want to avoid taxation on returns as much as possible.

Thannks

Dear Kaustubh..Let me know your investment horizon? (time-frame).

If your investment objective is long-term, to save taxes, liquidity and good returns then you can consider investing in ELSS funds.

Read: Best ELSS funds.

dear sreekanth,

I have invested haphazardly in variously MF without knowing how to invest properly,Below is the MF

I have invested.-

1. Reliance regular saving fund- sip-1000/m

2. Reliance banking fund-sip-3000/m

3. Reliance retirement fund-sip-10000/m

4. Reliance pharma fund-sip-4000/m

5. Reliance regular saving fund(equity)-sip-2000/m

6. Reliance regular saving fund(balanced)- lump sum- 100000

7. Reliance growth fund-sip-2000

8. Reliance dual advantage -VIII- lump sum-200000

9. Reliance growth fund- lump sum- 25000

10. BLS mid cap fund-sip-2000

11. BLS frontline equity fund-sip-1000

12. HDFC prudence fund-sip-1000

13. HDFC growth fund-sip-1000

14. SBI Magnum comma fund-sip-2000

15. SBI Magnum contra fund-sip-1000

16. SBI Magnum global fund-sip-1000

17. SBI Magnum balanced fund -sip-1000

18. SBI Magnum multicap fund-sip-1000

19. SBI Magnum blue chip fund- lump sum-10000

20. ICICI equity income fund- lump sum- 1000000

21.ICICI focused blue chip fund- lump sum- 10000

22.Axis Hybrid bond-lump sum-500000

23.IRFC Tax free bond- lump sum-791000

24.Reliance capital builder -II-lump sum-740000

25.LIC premium-43000 anually

26.PPF- 150000 anually

27. Sukanya sambridhi-150000 anuall

Can you suggest what to do know? I am puzzled.I I was guided by some investment agent I want go give my portfolio a proper shape, so that return will be more and investment become more systematic. Please help me .I am 38 yrs, having 2kids. monthly income around 80000.

Dear swati,

Way tooooo many funds. Kindly trim your portfolio. You may just need 2 to 4 good funds to achieve your financial goals.

Funds like (from your portfolio) BSL frontline equity, HDFC prudence, ICICI Bluechip are good ones.

Kindly read:

Best Equity mutual funds for 2016.

Best Balanced funds.

MY mutual fund portfolio.

Kindly provide more details about your LIC policies. Are you a salaried person?

Read:

Kid’s Education goal planning.

HELLO, IN MY OPINION FINANCIAL PLANNING IS CHANNELIZING YOUR RESOURCES TO YOUR FUTURE GOALS AND MAKING A CORPUS WHICH IS REQUIRED FOR YOUR FUTURE. Tax planning

Deer Sreekanth,

I am a first time investor in Mutual Funds Through SIP I want to do a Monthly SIP of

around Rs 4,000/- with a starting lumpsum investment of Rs 30,000/- which are my arrears my age is 30 years and i want to invest for long term wealth creation and TAX benefits. I want to know what kind of portfolio i can have and how to pic funds to have diversified portfolio for my investment goals. Please suggest.

Regards

Siladitya.

Dear Siladitya,

If you have a long-term view, want tax benefits, suggest you to look at ELSS Funds. Go through my article – “Top ELSS Funds“.

Do you have term insurance cover? Read my article – Top 7 best online term insurance plans.

Awesome, a great start for 2015 following this tips.

Dear Emebu,

Thank you. Keep visiting! Have a great year ahead. Cheers!

A very concise and informative post. Thanks for sharing the same.

Dear Jaidip,

Thank you. Keep visiting. Cheers!

Amazing shree…can u pls share ur number..my number is 97693951**

Dear Ajay,

I have noted down your number. Request you to get in touch with me @ sreekanth [at] relakhs.com