Investing is easy! Figuring out ‘where to invest’ is the hard part. Irrespective of my quantum of earnings, I have been judiciously saving money for making investments.

As I opined, it can be a challenging task to identify right financial investments. I too learnt the investment lessons the hard way only.

I have been investing in Equities since 2003 and Mutual Funds from 2009 onwards. A major chunk of my investible surplus now goes towards mutual fund investments for two of my important financial goals i.e., my Son’s higher Education (six years to go) and my retirement (wealth accumulation).

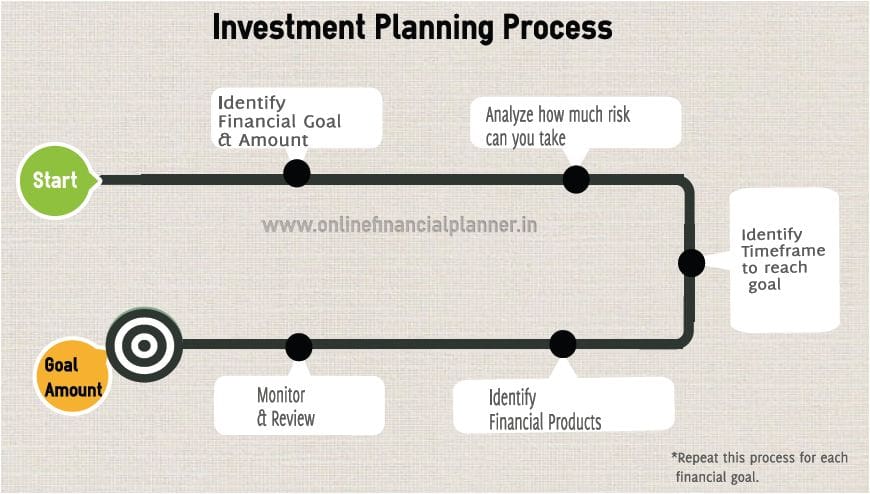

Below is the investment planning process that I follow without fail for my financial goals.

My Latest Mutual Fund Portfolio

My previous article on ‘my MF picks‘ (published in June, 2015) I had mentioned below mutual fund schemes as part of my portfolio;

- Short Term Goal

- Aditya Birla Sun Life Regular Savings Fund (erstwhile Aditya Birla MIP II Wealth 25 Plan)

- Medium Term Goal(s)

- HDFC Hybrid Equity Fund (erstwhile HDFC Balanced Fund)

- Long Term Goal

- Axis Long Term Equity Fund

- TATA Balanced Fund

- UTI Mid-cap Fund

Over the last 4 years, I have redeemed units of Birla Regular Savings Fund and utilized the proceeds, have redeemed units of TATA Balanced fund and re-invested in HDFC Hybrid Equity Fund.

I have also moved out of UTI Mid-cap Fund and started investing in Franklin Smaller Companies Fund since May, 2016. (Kindly note that I have remained invested for more than 6+ years in TATA & UTI fund before churning my portfolio).

I have very recently added UTI Nifty Next 50 Index Fund to my portfolio (from May 2019).

So, my existing mutual fund portfolio has below investments..

Some more important points on my investment planning & strategy..

- You can notice that I am currently not investing in any Debt Mutual Fund Scheme(s).

- For Emergency Fund, we (family) used to invest in Fixed Deposits & Liquid / Arbitrage Funds. We now prefer to keep the ‘rainy day fund’ in Bank Fixed Deposits only.

- I follow a combination of SIP + Lump sum investment strategy. Off-late, my SIP amounts are meager and prefer to invest additional sum whenever financial markets give us an opportunity.

- Besides Emergency Fund (Cash Fund), we also maintain a ‘Crash Fund’ to invest lump sum amount (additional investments) in MF portfolio & Equities whenever there is a market crash/downturn.

- Whenever I review the performance of my mutual fund portfolio, I give first priority to check my overall Portfolio returns. I do not initially get too worried about the not-so-good performance of individual Fund/scheme.

- I prefer to compare my Funds’ performances primarily with their Benchmark returns and not with its Peers. Trust me, the best performers list keeps changing every year, so the best strategy is to stick to consistent performers and also the Funds with decent ‘downside protection’.

- I make sure that I keep an eye on ‘who are the fund managers’ of the MF schemes that I have invested in.

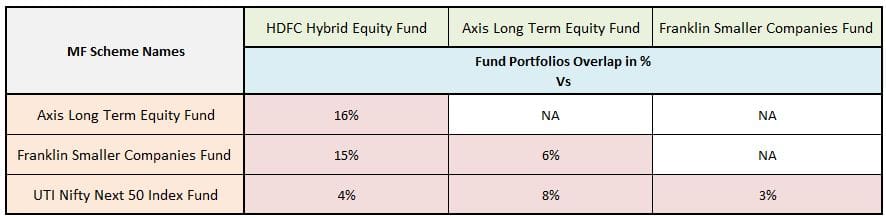

- As much as possible, I make sure that overlap % among my Equity Mutual Funds is reasonable. It should be as little as acceptable because if there is a 50-70 per cent overlap then this diversification (holding multiple funds) is only optical. Actually, there is very less diversification. In case of equity, the least of overlap is more desirable. (But, do note that the Fund Portfolios do change over a period of time, so keep keep a track of overlap %.)

So, are these the only best Mutual Fund Schemes to invest for your financial goals? – The answer is NO. These are just my Picks.

Please note that the above mentioned Mutual fund investments are done based on my financial risk profile and goals. This article is for information & knowledge sharing purposes only. If required, kindly take help of a Registered Investment Advisor in designing a Portfolio that is based on your requirements.

Continue reading :

- My Latest Stock Portfolio | Direct Equity Investments (Shares)

- Top Mutual Fund Schemes to invest in 2019 | Best Equity Funds for Long-Term

- List of all Popular Investment Options in India – Features & Snapshot

- Long Term Investment Horizon : Importance & Benefits | My father’s risky investments! (Real-life examples)

- Mutual Fund Investments are subject to Market Risks! – My opinion

(Image courtesy of iosphere at FreeDigitalPhotos.net) (Post published on : 21-June-2019)

Join our channels

hello Srikanth, are u planning to update it for 2020?

Hi Sree, Which fund do you recommend for a new investor, out of Kotak Standard Multipcap or Canara robeco Multicap.

Dear Rajni,

Can consider Kotak Fund..

Thank you. Happy New Year!

Thank you dear Rajni.. Wish you too a very happy new year 🙂

Hi Sree,

How do you evaluate this portfolio:

Axis Long Term Equity

Mirae Large Cap

Mirae Emerging – Large and Mid cap

HDFC Hybrid Equity

Kotak Standard Multicap

Do you suggest any addition/removal?

Dear Rajni,

May I know your investment objective and time-frame??

ThankYou for replying. About 7-10 years. Goal is to build wealth.

Dear Rajni,

The portfolio overlap between Mirae Large and Mirae Emerging funds is around 60%. So, you may avoid investing in Emerging fund.

The rest looks fine.

Read : Mutual Fund Portfolio Overlap Comparison Tools

ThankYou, What about removing HDFC hybrid coz after few years its still giving me 3-4% return. Do we have to have a hybrid fund in a portfolio? I was thinking of removing HDFC hybrid and adding Kotak Multicap(I dont have currently) . I have these four:

Axis Long Term Equity

Mirae Large Cap

Mirae Emerging – Large and Mid cap

HDFC Hybrid Equity

Dear Rajni,

I am a strong advocate of hybrid equity funds.

Personally, i too have investments in hybrid fund.

A MF investor can make include hybrid fund as part of his/her core portfolio.

In most of the scenarios, hybrid funds give almost similar returns as that of typical multi-cap equity funds, but with a better risk-return trade-off.

If you are not convinced with HDFC, you may switch to other hybrid funds..ICICI Equity/Debt, Mirae Hybrid, SBI etc.,

Thank You so much. I will take your advice into consideration to organize my portfolio 🙂

Hi Sreekanth,

Glad that you are active to respond to all our queries and posting great finance articles that helps plenty of people.

Keep doing it !!!

I’m investing in below funds through SIP from last 1 year, looking forward to do for next 3-5 years

Aditya Birla Sun Life Tax Relief 96 – 5k

Axiz Long term equity fund – 5k

SBI BLue chip fund – 4k

Suggest me that do i need to modify the amount for those funds or is it good to continue in the same way?

Also i’m planning to add one more fund (~4k), recommend which one suits for me by comparing with the existing funds?

Dear Boopalan,

Thank you for your appreciation!

Are you investing in 1 & 2 funds for tax saving purpose as well? Do you need these monies in next 3-5 years?

Yes I’m investing 1&2 for tax saving purpose.

Actually i have long term goals , so i want to continue to invest for next 5 + years.

Dear Boopalan,

You may continue with your investments!

Do invest across Asset classes (equity, debt etc.,).

Related articles :

* Mutual Fund Portfolio Overlap Comparison Tools

* List of all Popular Investment Options in India – Features & Snapshot

Dear Sreekanth,

Would like to hear from you about my MF portfolio (risk profile is moderate) which is as below

My Debt part is seperate which lies mostly in one Liquid fund & one Ultra short term fund.

Equity part

Near future Goal (5 years) – HDFC Hybrid Equity-Direct Growth

For long term wealth Creation – Kotak Standard Multi Cap – Direct Growth &

Mirae asset emerging Bluchip – Direct Growth

Confused bit regarding the overlap between these funds. Is it ok to Invest in Multicap and large and midcap MF or should i replace Mirae asset with any index fund (since i m not ok with the returns in actively large cap MFs)

Thanks in advance.

Dear Prakash,

5 year goal – Fund is fine. But, kindly do not stay invested till the 5th year, can be a risky bet. You may make partial withdrawals from this corpus before you reach your goal year and switch to safer investment avenues.

The other two funds are fine.

But if you want to invest in a large-cap specific fund then index fund can be a better choice – Ex : UTI Nifty Fund.

Thanks sreekanth for your quick & prompt response.

Dear Sreekanth,

First of all I would like to say BIG THANK YOU for running this beautiful site.

Now, Lets move to the query….

I am 30 Year old male want to build wealth for my own house & daughter education in next 15-20 years.

My daughter is 2 years old now & I can wait for next 12 to 15 years for her higher education & I need around 75 Lacs for that.

I want to purchase a house in next 10 to 15 years & I need 75 Lacs for that.

My mutual Fund Portfolio is as below. (Investing 23000 PM via SIP route in different funds).. Investing from last 3 years..

1. DSP Tax Saver Fund (SIP-3000 PM)

2. ABSL Tax Relief 96 Fund (SIP-5000 PM)

3. ABSL Banking & Financial Services (SIP-3000 PM)

4. HDFC Mid Cap Opportunities (SIP-3000 PM)

5. DSP Small cap (SIP-3000 PM

6. SBI Small Cap (SIP-3000 PM)

7. L&T Emerging Businesses (SIP- 3000 PM)

My question is that, Am I investing in right mutual fund.?

Or If any correction to be done than pls suggest which mutual fund to be stopped or merged with other.

For my retirement my Employee Provident Fund will take care.

Best Regards,

Nitin

Dear NITIN,

Are the ELSS funds (1&2) for tax saving as well?

Any specific reason/strategy for picking two Small cap funds?

Dear Sreekanth

Yes, I am saving tax also under 80C from my ELSS funds.

Reason for investing in small cap is for higher return as my time horizon 10+ years.

Serial no 5,6 & 7 in my portfolio are the small cap funds. I need your suggestion on that… Should I continue with the same funds or any change/merge required in the funds.?

Regards,

Nitin

Dear Nitin,

You may continue with both the ELSS funds.

HDFC Mid-cap is fine.

Sectoral fund can be very risky, you may avoid it as most of the funds do have sufficient exposure to the banking/Financial institutions’ shares in their portfolios.

Rs 12k of your SIP amount is being invested in Mid/small cap funds. If you are absolutely fine with high risk then you may continue with them.

Else, you may add one Equity aggressive fund (equity balanced fund) to your portfolio in place of one of the Small cap funds.

Related articles :

* Mutual Fund Portfolio Overlap Comparison Tools

* How to select the right and best Mutual Fund Scheme based on the Measures of Volatility?

* What are Mutual Fund Upside / Downside Capture Ratios? | How to use them in MF Performance Analysis?

Dear Sreekanth,

Kindly give your suggestion on the below funds…

1. SBI Small cap

2. DSP Small cap

3. L&T Emerging businesses

Out of the above 3 small cap funds.. In which fund i should continue my sip and In which fund I should stop my sip..?

All the 3 funds are giving negative returns…

Best Regards

Nitin

I am asking this question on behalf of your comment as you have suggested to stop 1 small cap and invest in equity oriented balanced fund instead..

Dear Nitin,

Three of them have almost similar profile. You may continue with SBI Small cap (high Standard deviation with high returns) and L&T Emerging..

Equity Hybrid, examples : HDFC Hybrid Equity or ICICI Equity & Debt.

Brother,

I want to invest in debt mutual funds (equity portfolio already running). As of now, I have extra 5 lacs which I dont need for 2-3 years. With your old debt mutual funds post (hope u will write new one shortly 🙂 ) and my own research, I have sorted 5 debt mutual funds. Returns are almost similar but I want to diversify little bit so that is why selected 5 funds, just in case, something goes wrong.

Valueresearchonline..

Please click on above mentioned link – I have done Fund comparison on valueresearch.

My priority is – safety, better return that FD/NSE & lastly most imp LIQUIDITY which we dont have in NSE and FD (early redemption charge + TDS).

So, I wanted to ask, if u were in my situation, how would u have spitted 5 L LUMP sum amt in above funds? Which one to avoid? Which new one I can add ? (if u have any suggestion)? I mean, returns are almost similar so which funds are safest to go with. 🙂

Your suggestions will be highly appreciated.

Thanks in advance for your reply.

Rahul

Dear Rahul,

If safety is my first priority then I would invest in Bank FDs.

In case, you wish to take some risk and are aware of the possible risks associated with debt funds and considering your investment time-frame, you may shortlist Franklin Ultra Short Bond Fund and Kotak Low Duration fund.

But, both these funds portfolios have medium credit quality

Hello Sree,

I would like to do a Lumpsum investment for 1-2 years. What type of fund do you recommend for better returns in comparison to Bank fixed deposits.

Thanks,

Hemant

Dear Hemant,

But do note that better returns come with higher risk profile.

You may consider an Ultra Short term Debt Fund.

brother, I am curious to know, on what reasons you have opted for UTI next 50 instead of UTI 50 index fund. Thx in advance!

Dear Rahul,

I have opted this fund keeping in view of my overall Portfolio.

I wanted to pick a low-cost, passive index based fund that has large+mid-capish orientation, as I came out of UTI mid-cap fund.

Hi Sreekanth. Thank you for sharing your portfolio. Ever since I discovered your blog, I have learned a lot about financial planning and have also shared your blog with colleagues. I am 30 years old and my financial goal is to buy my own home in 10 years and create wealth of 2 crore for retirement in 25 years. Here’s my SIP portfolio:

HDFC Hybrid Fund – Rs. 5000/- (Since 1.5 year, increased from Rs. 1500)

SBI Bluechip Fund – Rs. 5000/- (Since 1 year)

L&T Mid Cap Fund – Rs. 5000/- (Since 9 months)

Mirae Emerging Bluechip Fund – Rs. 5000/- (Since 2 months)

HDFC Small Cap fund – Rs. 5000/- (Starting next month)

Apart from this, I invested 1 lakh lumpsum in Aditya Birla Tax Relief 96 last year and have Rs. 10 lakh in FDs. Is my portfolio looking alright?

Dear Anisha,

Glad to know that you find my articles informative and useful.

The listed funds are ok. However, you may reduce allocation to mid/small cap funds and pick a pure Multi-cap fund.

You already have a bluechip and a mid-cap fund, so you may reduce allocation to Mirae fund.

Related articles:

* Mutual Fund Portfolio Overlap Comparison Tools

* Top Mutual Fund Schemes to invest in 2019 | Best Equity Funds for Long-Term

Thanks, Sreekanth!

Currently I invest on these three funds

1) Hdfc hybrid equity fund almost 9 years ongoing

2) Nifty next 50 for last one year ongoing

3) Parag parikh long term equity last. 5 month

Is it fine.

Regards

Pradipta

Dear Pradipta ..Looks fine to me..you may kindly continue with your investment plan..

Thanks Sreekanth for sharing the same. Just a suggestion if its suits you – if you can tell the % amount you have distributed in the selected funds and risk appetite which explains why the selection of these funds … may be a new topic to start a thread …… just a suggestion if you are comfortable in disclosing the same.

Dear Abhinav,

My current allocation is around 50 to 60% to Hybrid Fund, followed by ELSS fund, minor allocation to Small cap and Index Fund.

Hybrid fund gives me a downside protection to my portfolio, plus risk – reward trade off is much better in case of Equity Hybrid Funds.

I strongly believe that one can seriously consider a large cap index fund or Large midcapish index fund if one is looking for large-cap fund.

Thanks Sreekanth for your reply.

So 50 to 60% in hybrid is for long term Goals?? I believe in some other post (which i read now) you told 40:40:20 in midcap:elss:bal fund … Anyways it’s as per user risk profile. But i believe 40-45% would be good idea for Midcap/Small cap for long term (about 10+ yrs goals)

Dear Abhinav,

40:40:20 for my portfolio?

Kindly go ahead with your investment strategy/plan and conviction.

Do note that I factor in my family’s investments and my investments in other Asset classes (especially, real estate ones) before allocating my investible surplus to my MF portfolio.

Also, I invest monies in HDFC hybrid fund for both medium + long term goals, hence higher allocation in % terms..

I was talking about:

this article ..

Below line under Long-Term Financial Goals

/* I have been holding TATA & UTI funds for the last 6 years or so. The percentage of allocation among these funds is 40:40:20 (UTI : Axis : TATA funds respectively). */

Dear Abhinav,

Got it!

Yeah, the allocation was way back in June 2015.

Dear Sreekanth, it would be good to know your strategies around real estate too. Are they part of this blog?

Hi Sreekanth,

First of all I want to thank you for your blog. You have been doing a fabulous job. Now coming to my question…

My age is 35. I have been investing in SIP since last 3 years. My current portfolio has the following mutual funds.

1. DSP Small cap fund (Investing since 03/2016)… 1K/Month

2. HDFC Mid Cap Opp (Investing since 03/2016)….2K/Month

3. Motilal Oswal Multicap 35 (Investing since 11/2017)……3K/Month

4. SBI Bluchip (Investing since 12/2016)……2K/Month

5. SBI Magnum Midcap (Investing since 03/2016)….1K/Month

6. Aditya Birla Sun Life Tax Relief 96 (Investing since 01/2018)……3K/Month

7. Reliance Small Cap (Investing since 01/2019)

Shall I continue with these funds?

Please do let me know if you need any other information which can help you to answer my query in a better way. Looking forward to hear from you. Thanks.

Dear Avisek,

Thank you for your appreciation!

May I know your investment objective(s) and time-frame??

Hi Sreekanth,

Many thanks for your reply..

My main investment goals are to arrange funds for my child’s(2 years old) education, buying a house & also for my retirement. My investment horizon is long term, minimum 12-15 years.

Note: I have been also investing Rs.4000/Month in PPF since last 3 years.

Thanks.

Dear Avisek,

Your portfolio has two mid cap and two small cap based funds, can have higher risk profile.

Suggest you to check the funds portfolio overlap especially funds from same fund category and can try trim down your portfolio.

You may also look adding one pure Multi-cap fund and/or Aggressive hybrid fund to your portfolio.

Read :

* Mutual Fund Portfolio Overlap Comparison Tools

* Top Mutual Fund Schemes to invest in 2019 | Best Equity Funds for Long-Term

* Top 5 Best Aggressive Hybrid Equity Funds (Balanced Equity Mutual Funds)

What is market crash for you? Is there any specific rule that tells you it’s right time to invest lump-sum?

Dear Arun,

One can track the Daily Moving Averages of Fund’s respective NAV and its Benchmark Index to know if it is in Uptrend or Downtrend.

Related article : What is 200 Day Moving Average? | How to track DMAs? How to use them in Mutual Fund investment decisions?

Thank you Sreekanth for your quick response. However, I could not find it for “Franklin India Smaller Companies Fund”. Can you help me find 200 day moving average for this?

Dear Arun,

In economic times portal, you can get the trend of NAV range – ‘Monthly’ & ’52 week’ and you can check the respective benchmark DMAs as mentioned in the above link (provided in the comment).

Sreekanth sir, I’m a regular reader of your blog. I’m also parking my money in MF. All short term/ mid term and long term in different MF schemes. Recently I came to know about a new feature of scam done by MF with our hard earned money. LT Finance was having reliance power shared pledged by AA or his company against the fund. The pledged shares were counted for cost around Rs. 60 at the time of lending money. Now the company has shown no willingness to pay money against pledged shares. They do not in position. So LT MF sold its share in market at Rs. 10 just few days back, and height is that.. the sold shares purchased by AA group company only, some other than the comapny came to pledged it. It means that they gave shares to LT MF @ 60 and buy back from MF @10. MF invested our hard earned money and ultimately it make loss of our money. LT MF has not invested anything from their pocket.

Can you show some way to find out such MF, which are involved in such dirty game? so retail invester like us can be saved. – Nimish

Dear Nimish,

I believe that SEBI is now contemplating to re-write some rules related to Pledging of shares..

Related article : Sebi tightens norms for MFs, pledged shares to boost investor confidence

Hi Sreekanth sir, You r doing a glorious job with these posts. No matter how, it comes with great responsibility.

I am in 30 now,have ppf,rd, ncd for debt part.Now planing to invest in MF,start with Parag Parikh Long Term Equity Fund – Direct Plan – a monthly SIP of 5000 for 10-15 years.I would like to do more MF invests in small cap,hybrid mf in a couple of years and all are for long term too. So what do u think about Parag Parikh Long Term Equity Fund for such a long term investment?

Dear albin,

Hope your NCD investments are with Popular companies.

PPLTE is a good bet.

You may go through this article..

Thank you so much.

Hi Albin,

You can choose SBI Small Cap or HDFC Small Cap Fund. Both are great funds. Let me call on 75749 23412 for more information.

Hi Sreekanth,

I have been investing for last couple of years using all the advice from you- so thanks for that.

Once again, need your guidance.

I am going to buy a property next month for which I shall be taking a home loan.

While I dont plan on and dont need to redeem my existing MF holdings, I will not be able to continue the SIPs once the home loan EMI starts.

Do you suggest it is OK to “stop” SIPs and stay invested till I can restart (may be in 2 years).

My MF portfolio is around 2-3 years old and giving me around 15% returns avg.

How should I go about it? Please advise.

Thank you!

Gaurav

Dear Gaurav,

How confident are you that your investible surplus (Income – expenses – EMIs etc) can be good after 2 years?

May I know your other financial goals (besides your Retirement..)

Hi Sreekanth,

Financial goals-

1. Buying this house for which I have the query

2. Retirement

3. Child’s education and wedding(kid is 6 months old at this time)

4. Wealth generation

The reason I feel confident of investible surplus two years from now is that EMI + all current expenses will be 70% of our current income.

Over 2 years, the income will go up and so the saved percentage will increase beyond 30%.

Although expenses around the kid may also increase, I feel at least 25% can still be set aside as investible surplus.

Please advise.

Thanks

Gaurav

Dear Gaurav,

Ok. But, kindly do not over leverage (stretch) yourself regarding the budget (Property cost). Is this property for your self-occupation?

You may also go through this article @ Investing in Mutual Funds while paying Home Loan EMIs | Cost-Benefit Analysis

Hi Sreekanth,

Yes, property is for self- I currently live in a rented accommodation.

I read through the article, and seems like investing any surplus in MF through SIP while paying home loan EMI will be a good choice- I will plan accordingly, instead of hoarding up to prepay my home loan.

Please do advise on whether there will be any problem in “stopping” my current SIPs for some time though- till I can figure out how much I can invest and then restart my MF SIPs.

Or should I close all current SIPs and use them to increase downpayment on my loan?

Thanks

Gaurav

Dear Gaurav,

Suggest you not to redeem your existing MF Units for now.

Based on your financial position after 2 years or so, you can re-start your SIPs, may be, with slightly higher SIP amounts to achieve your long-term Fin goal values..

Sreekanth,

Thanks for sharing your portfolio and the changes in past few years.

Is this the end of road for UTI Midcap fund?

I was hoping that there could be a midcap rally this year that will prop up the returns of this fund.

Interesting to see you have moved from midcap to a smallcap fund.

Dear Pradeep,

Yes, there has been a correction in mid/small cap stocks last year and there is no decisive up-tick this year till date.

May I know the other scheme names that you have invested in (if any)??

Franklin SCF is a midcapish small cap oriented fund 🙂

Hi Sreekanth,

I am also investing in UTI Midcap. The other schemes are Franklin India Equity, Smaller Companies, Mirae Largecap. I started Kotak Emerging Equity as an alternative to UTI Midcap, but not yet stopped. Perhaps its time now?

Dear Pradeep,

Personally, I prefer HDFC Mid-cap or Franklin Prima funds in mid-cap space. These funds have very long track record and have seen different market cycles.

UTI mid-cap : The risk – return trade off is not in its favor and the fund’s performance Vs its benchmark has not been well for the last 5 years or so.

Hi Sreekanth,

I ignored HDFC fund due to its size while I have 2 Franklin funds already. So I chose Kotak fund. But I agree that UTI fund isnt going back to the glory days of Anoop Bhaskar. I will also get out and possibly UTI Nifty Next 50 is an option.

Good to see your portfolio Sreekanth. It has balanced fund, small cap fund, index fund and tax saving fund. I usually invest in largecap and multipcap and midcap too along the above categories as these funds tend to perform differently in various market cycles.

Thank you dear Suresh for sharing your views!

I consider Tax saving Fund (Axis LTE) as a typical Multi-cap fund.

My portfolio has a higher allocation to Hybrid Fund, followed by ELSS fund, Small cap and then Index Fund.