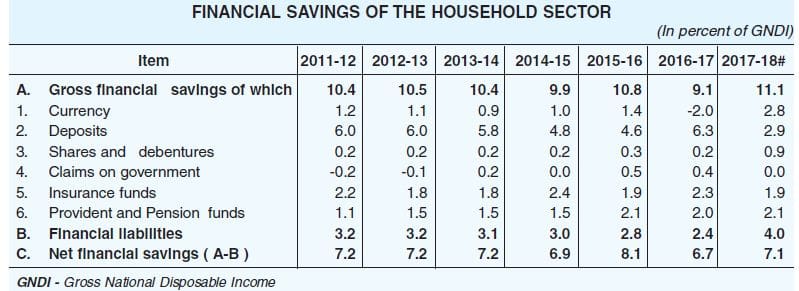

India has one of the highest ‘net savings rates’ in the world (the national saving rate is about 20 per cent of GDP). However, the net savings rate as a % of GDP has been steadily declining since 2011-12.

The other day, I was going through the IRDA’s annual report and noticed that the Domestic saving declined to 29.6% of gross national disposable income (GNDI) in 2016- 17 from 30.7% in 2015-16.

‘Household financial saving’ – the most important sourcefr of funds for investment in the economy declined to 6.7% of GNDI in 2016-17, down from 8.1% in 2015-16.

The below table indicates that the ‘Gross Savings’ of Indian Household sector has been on the down-ward trend.

As per the estimates by the RBI, the rate of financial savings by the Indian households have again picked up in 2017-18.

As per the above data, the savings in Deposits have declined considerably and we preferred to keep the savings in the form of ‘currency’. You can also notice that the financial liabilities of the households have increased. Considering this scenario, each rupee that you can save is valuable, more than that ‘where you save’ is what matters the most.

This has prompted me to publish a post that lists all popular investment options that are available in India. Coincidentally, one of my blog readers have also requested for a similar article.

Let’s now discuss on popular investment avenues that are available in India. For simplicity sake, I have segregated the investment products in four categories. Kindly note that this article is not about ‘best investment options’ but to highlight the important features of popular investment products, so that you can select right investment option(s) that are suitable for your financial goals.

Popular Investment Options in India for 2020-21 | Features & Snapshot

Below are some of the top investment avenues that are safe or have low risk. These are Fixed income or Debt oriented products.

Fixed Deposits / Recurring Deposits :

- FDs/RDs are ideal saving options for short term goals and recurring expenses. Safety of capital is the most important feature of FDs/RDs. (Related Article : ‘ Why not to invest in FDs for long-term?‘)

- The rate of interest vary from bank to bank and it also depends on the quantum of investment, your age and deposit tenure.

- The interest income is taxable as per your income tax slab rate. (The Budget 2018-19 has proposed to insert a new section 80 TTB so as to allow a tax deduction of up to Rs 50,000 in respect of interest income from deposits held by senior citizens.)

- You can get tax benefit u/s 80c by investing in a 5 year Fixed Deposit.

- TDS is applicable. You can submit Form 15G or Form 15H (if eligible) to avoid TDS.

Non-Convertible Debentures (NCD) :

- NCDs are fixed income products that come with slightly higher risk when compared to FDs/RDs. These are one of the most popular investment options in the recent past.

- NCDs offer slightly better interest rates than Fixed deposits. These are suited well for low-risk & conservative investors. Kindly note that interest income is taxable. TDS is not applicable on listed debentures.

- No tax benefits are available on your investments in NCDs. (Related article : ‘What are the risks associated with NCDs?‘)

Tax-Free Bonds :

- TFBs are also one of the safest and low risk investment product. The interest income is tax-free. The coupon rates offered on these bonds are generally lower than NCDs.

- In this FY, there are no TFB Public Issues are proposed. You may have to buy them from Secondary market only. Though the interest earned on these bonds is tax-free, any capital gain from sale in the secondary market is taxable.

- These are one of the best savings options for the Individuals who fall under highest tax slab rate and are conservative.

- Not Tax benefits are provided.

- (Related Article –

Company Fixed Deposits:

- Company Fixed Deposit schemes generally gain popularity in low-interest rate scenario. The interest rates offered on Corporate FDs are better than traditional FDs.

- Interest income is taxable. TDS is applicable on interest income of above Rs 5,000.

- Kindly do not invest in Company FD schemes which offer unusually high interest rates. (Related Article : ‘How to check if a Company can collect Deposits from the Public?‘)

Senior Citizen Savings Scheme :

- This is an Indian government-sponsored investment scheme and hence is considered to be one the safest and most reliable investment options for the Senior Citizens in India.

- The maximum amount that can be invested in this scheme is Rs 15 lakh.

- The interest income is taxable. The interest rate on SCSS is generally better than FD rates. Tax benefit u/s 80c is available. TDS is applicable on interest income of above Rs 10,000. You can submit Form 15H to avoid TDS.

- It has a tenure of 5 years but premature withdrawals are allowed (subject to certain terms).

Post office Monthly Income Scheme :

- This is one of the best periodic income product. You can receive interest income on monthly basis. But, interest income is taxable.

- PO MIS has a tenure of 5 years.

Sukanya Samriddhi Scheme :

- This is a girl-child oriented scheme offered by the Govt of India. The minimum amount that can be deposited in SSA is Rs 250 only.

- The interest rate offered on SSS deposits is now market-linked.

- The maturity of the account is 21 years from the date of opening of account or if the girl gets married before completion of such 21 years (whichever is earlier). However, pre-mature withdrawals from SSA are allowed.

- This is a decent long-term savings option for your girl child.

- Tax benefit u/s 80C is available and interest income is tax-exempt. (Related Article : ‘All you want to know about Sukanya Samriddhi Deposit Scheme‘)

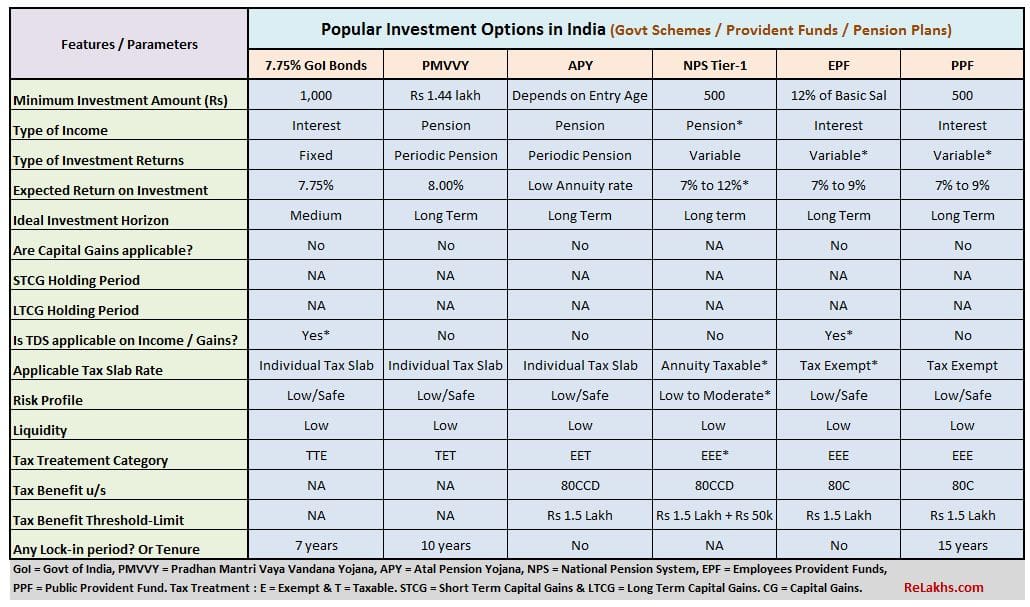

In the below section, let us go through the features of some of the popular Govt sponsored Pension oriented schemes and Provident Fund Options.

Govt of India Savings Bonds :

The central Govt has decided to replace 7.75% Bonds with new RBI Floating Rate Savings Bonds 2020 (Taxable) scheme. These bonds will be issued by the RBI. You may go through my latest article @ RBI Floating Rate Savings Bonds 2020 : Features & Review

- The GoI bonds carry an interest rate of 7.75% with a lock-in period of 7 years.

- Premature withdrawal facility is available to the eligible investors after lock in period of 4, 5 and 6 years in the age bracket of 80 years and above, between 70 to 80 years and 60 to 70 years respectively.

- The interest income is taxable as per your income tax slab rate. TDS is applicable on interest income of above Rs 10,000. (Related Article : ‘Features of 7.75% GoI Bonds‘)

Pradhan Mantri Vaya Vandana Yojana :

- Indian Citizens aged 60 years and above are eligible to invest in PMVVY. The scheme has been extended up to March 2020.

- As per Budget 2018-19, the maximum investment permissible has been increased to Rs.15 lakhs for a monthly pension of Rs 10,000.

- One time premium payment of around Rs 1,50,00/- fetches a monthly pension of Rs 1,000 for 10 years.

- No tax benefit is available.

- The Scheme offers assured return of 8% p.a. (Related Article : ‘PMVVY Scheme : Review‘)

Atal Pension Yojana:

- Under the APY scheme, a guaranteed minimum pension of Rs. 1,000/-, 2,000/-, 3,000/-, 4,000 and 5,000/- per month will be given from the age of 60 years depending on the contributions made by the subscribers.

- Pension is a taxable income. Tax benefit u/s 80CCD is available.

NPS Tier-1 Account:

- The Government of India rolled out the National Pension Scheme (NPS) for all the citizens of India from May 1, 2009 and for corporate sector from December, 2011.

- National Pension System (NPS) offers two types of accounts – Tier I and Tier II. Income Tax benefits are currently available on Tier-1 deposits only. The NPS works like mutual funds. The returns are variable based on the Fund/Scheme chosen by the subscriber.

- At present, 40% of the accumulated corpus utilized for the purchase of the annuity is tax-exempt. Of the remaining 60% corpus withdrawn by the NPS subscriber at the time of retirement, 40% is tax-exempt and 20% is taxable. The tax exemption is now extended to the entire 60% (w.e.f April 2019).

- The annuity income generated by the Annuity plan is taxable.

- Tax benefits are available u/s 80CCD. (Related Article : ‘Best NPS Funds to invest in 2019‘)

Employees Provident Fund (EPF) :

- If you take out your monthly pay-slip and check, you can understand that every month 12% of your “salary” is contributed towards EPF account. Your total monthly contribution is routed towards Employees’ Provident Fund.

- The rate of interest is notified by the central government periodically (every fiscal year).

- The interest income on EPF is tax-exempt after you complete 5 year service period. Tax Benefit is available u/s 80c. (Related Article : ‘Tax treatment of Financial Instruments‘)

Public Provident Fund (PPF):

- PPF is one of the best long-term savings options in India. The interest rate is now market linked and is generally better than most of the other fixed income and safe investment avenues.

- The Deposits have a lock-in period of 15 years and can be extended in blocks of 5 years each.

- Tax benefit u/s 80c is available. The tax treatment of PPF falls under EEE tax category. (Related Article : ‘Tax implications of EPF, PPF & NPS Withdrawals‘)

Let us now review the features of mutual funds and direct equities.

Mutual Funds :

- Mutual Funds are slowly gaining tremendous popularity with the retail investors. One can start investing in a Mutual fund with a very nominal investment. Mutual funds are suited for all types of Financial goals and investment horizons. But, kindly be aware of the risks associated with mutual fund investments.

- The gains on Mutual Funds are treated as Capital Gains. Depending on the type of mutual fund (Debt / Equity) and the holding period (Short term / Long Term), the capital gain taxes are applicable. Close-ended schemes like FMPs (Fixed Maturity Plans) come with lock-in periods.

- You can also receive Dividend income from your Mutual Funds.

- Investments in Equity oriented ELSS funds can get you tax deduction u/s 80c. TDS is applicable on NRI investments.

- Tax @ 10% on long-term capital gains of above Rs 1 lakh is levied on Equity Funds.

- Related Articles :

Shares / Stocks:

- Equity Mutual Funds are an indirect way to take exposure to stock markets. In case, you can stomach more risk, you can consider investing in Stock markets directly as well. Managing your emotions (financial behavior) play an important role when it comes to equity investments.

- Tax Benefits of Rajiv Gandhi Equity Savings Scheme (RGESS) under section 80CCG has been withdrawn. However, if an investor has invested in the RGESS scheme in FY 2016-17 (AY 2017-18), they can claim deduction under this Section until AY 2019-20.

- The taxation rules are same as to Equity Funds. (Related Article : ‘10 Rules to select good Shares/Stocks for Value Investing‘)

In the next section, the features of Real estate property and Gold investments are provided.

Real Estate Property:

- If you can afford to take high risk and big-ticket investment, can consider investing in a real-estate property (other than your self-occupied property).

- The ideal rental income yield to expect should be above 4%.

- TDS @ 1% is applicable on an investment of above Rs 50 lakh. TDS rules are also applicable on NRI investments.

- Section 54EC bonds can be used to save long term capital gain taxes on sale of property. (Related Article : ‘How to save Capital Gain Taxes on sale of Property?‘)

Gold & Gold Bonds:

- Gold prices have become very volatile in the last few years. It is no more the safest asset. But, you can easily ‘sell’ (high liquidity) at the prevailing market prices, as GOLD is the ultimate form of money in the world and is “universally acceptable”. But, do not expect abnormal returns from your Gold investments.

- If you HAVE to invest a portion of your savings in Gold for long-term, Gold bonds outscore the Gold funds / physical gold and can be a preferred mode of investing in Gold.

- A nominal interest is payable on SGBs and the capital gains (if any) are tax-exempt. (Related Article : ‘All about Sovereign Gold Bonds‘)

Our culture and tradition encourages us to save more. But, we are also extremely risk averse and generally place greater importance on safety than rate of return on investments.

If you would like to accumulate sufficient corpus for a long-term goal, you may have to take calculated risk and invest in right financial product(s) which can beat inflation & give better tax-adjusted returns. If your investment horizon is short, kindly give high priority to safety & liquidity and do not chase returns aggressively.

Your investment portfolio should have a fair mix of both conservative as well as aggressive investment options. Kindly try to maintain an ideal asset allocation.

Request you to let me know if any of the details provided in the above Tables (images) needs to corrected or updated. Cheers!

The returns quoted in the above tabular data are indicative only and they are not guaranteed. The investment horizons mentioned in the above post are for IDEAL scenarios only. I believe that investment and insurance should not be clubbed together and hence Insurance investment options like ULIPs, Traditional life insurance plans and Pension plans are not included in this article.

Continue reading :

- RBI’s statistical data on Indian Household Investments & Savings (2018-19) | How & Where do we save & invest?

- Different Asset classes have different Tax implications – How Returns are taxed?

- Lump-sum Investment options for Retirees

- How to set-off Capital Losses on Mutual Funds, Stocks, Property, Gold, Bonds & Debentures?

(Image courtesy of fantasista at FreeDigitalPhotos.net) (Post first published on : 24-January-2019)

Join our channels

Hello Sree,

Happy New Year!

My father wants to invest 25 lakhs, he is already investing under 80C and has medi and life insurance. Also he has no short term goals, just needs to invest the money instead of keeping in savings account. He is a senior citizen and willing to take low- moderate risk. He has other sources for monthly income.

Are you please able to suggest an option mix for him.

Kindest regards

Dear Ksam,

Happy new year to you too!

Apologies for my late reply!

May I know what type of life insurance plans your father has?

Is he looking for regular monthly income or is this for just accumulation or a mix of both??

There are so many options of investments available in India. If you are a beginner you should start from basic options like Fixed deposits. Then you can move on to other options but be sure that you have enough knowledge to jump into market investments. Mutual funds are a great option for beginners who want to invest in the market.

Hey Sreekanth, Thanks for sharing such an informative article. The details did help me with my decisions on my investment options.

Hi,

Thank you so much for providing your valuable inputs.

I have few queries need your valuable guidance.

1. I would get some money (8 lacs) which I would like to invest in corporate bonds to get monthly interest which finally to invest in MF’s for better returns. Can you pls suggest is it good idea or else can you suggest any other tool which can give more than 9 % return (monthly). Else I have max gain home loan with interest rate 8.9 %, is it good to park it.

Pls suggest.

Regards

Rama.

Dear ramakrishna,

May I know your investment horizon?

Definitely more than 5 years, in fact this is for capital building. Pls also note I have SIPS for 35 k.

I have SIP in icici pru value discovery fund 3000 for last 3 years, returns are poor, can you pls suggest to continue or divert into any other?

Dear ramakrishna,

If your investment objective is to wealth accumulation then any reason for planning to pick Bonds that may monthly interest??

You may invest in mutual funds or other options for corpus accumulation.

You may kindly share your MF Scheme names..

The idea is to invest in SIP’s from the interest obtained on corporate bonds. At the same time don’t want invest in lump sum in MF’s. Moreover, I feel, we get more than > 9 % interest in corporate bonds.

I appreciate you to suggest any other options available which is suitable to my rudiments. As already mentioned I have home loan @ 8.9 %.

My SIP’s are:

Icici value disc – 3 k investing last 3 y, low return, should be continued?

HDFC hybrid eq. 10K

Kotak sta. multi 6 k

Rel. small cap -8k

SBI multi cap 2k

Rel. eq. hybrid -2k

Sundaram mid cap -2k. I can add another 10 k, pls suggest.

NPS is also there for around 1.5 lacs p/y.

Pls suggest.

regards

Rama.

Dear ramakrishna,

Corporate Bonds – Are you referring to Debentures or Debt funds or ??

You may continue with your ICICI Fund.

Reliance Hybrid is not a great performer. You may invest in HDFC hybrid fund itself.

Related article : Top Mutual Fund Schemes to invest in 2019 | Best Equity Funds for Long-Term

Hello Sreekanth,

Please review HDFC Click2Wealth ULIP plan which is a new product and also how does it compares to earlier Click2Invest plan. Thanks in Advance…

Sonit

Dear sonit,

Most of the new-age (latest) ULIP plans are almost same, just they bundle some new features (value added ones).

But, I prefer to pick Mutual funds to ULIPs.

Kindly read :

* Mutual Funds Vs ULIPs – Which is better? | Post Budget (2018) LTCG Tax proposal on Equity Mutual Funds & Shares

* ULIP Returns vs Mutual Fund Returns: A Comparison

Sir,I am now 30 age, got married . In a couple of months I will go abroad and we planning to stay there for next 15 -20 years or more .I have some equity mf schemes in mind for long term purposes (I will share it with u later) , but now in a great confusion whether to start a PPF account or NPS before becoming NRI..

what do u think?

In my knowledge, 1 }ppf- it is completely tax free but heard that Govt planning to implement new rules for NRI. 2} NPS- Tax is on withdrawal amount and there is compulsory to buy an annuity..

Expecting ur valuable comments

Dear Albin,

PPF is a good long-term savings option.

If PPF account is opened by a Resident Indian and later on if he/she becomes an NRI, can still continue his contributions to PPF account for the full 15 year term.

But, recently there was a notification by the Govt that NRIs should close the PPF accounts. This notification was later withdrawn.

So, there has been policy flip-flop w.r.t PPF by the Govt.

Related articles :

* Latest NSC & PPF rules for Non-Resident Indians (NRIs) | New Amendments to PPF Act & NSC

* National Pension Scheme (NPS) – Why it is not a good Investment Option?

thnk you for effective reply

You are welcome! Keep visiting ReLakhs.com..

HI Srikanth,

why every financial blog relate real estate with house only, why not land, commercial property etc, I have seen only of your article where your parents have invented in a land and benefited immensely and you have boasted about long term nature and effect of compounding in that article. Can you do article on real estate which shows ideally if a Rs 1 lakh invested it should become x by so many years (y) to have better returns than any product like FD or MF or NDC etc this will help people to compare if their real estate investment is correct or needs some correction, this will also bust myths of investing in realestate is great etc.

Dear harsha,

Agree with your views!

For most of the real estate reviewers, real-estate means FLATs/Apartments. Yes, RE is much more than that..

May be, we have reliable data only on Flats hence the analysis by most of the reviewers is done on Flats only.

I am strong believer that an investor who can afford to take risk can also consider RE as an investment option (especially land/independent house). I do not like to invest in Flats though.

But, real estate (direct) investment may not be suitable for every retail investor. Thanks to high-price valuations and low liquidity concerns.

One good thing about RE has been , improvement in ‘regulatory framework’…

Hi Srikant,

Could you please let me know your opinion about RBL bank. Do you think it will do well in near future? Is it safe to invest in a term deposit for 12 months with RBL bank? In case of any bankruptcy, Deposit Insurance and Credit Guarantee Corporation of India (DICGC) can offer amount up to 1 lakh only. So, just wanted to know if its safe to invest a few lakhs with RBL in a term deposit for 12 months as they are providing a very good interest rate of 8%.

Thank you!

Dear Sunil,

Indian banking system is a very well regulated one.

If your investible corpus is minor (compared to your overall portfolio) then you may go ahead and invest for 1 year.

Else, you may stick to popular banks.

Thank you so much for your efforts you put in preparing this list of all popular investment options in India.

Sir

How can we protect our mutual fund portfolio from AMC DEFAULTS

Dear Amit,

Mutual Funds are regulated by Government bodies such as Securities Exchange Board of India (SEBI) and Association of Mutual Funds in India (AMFI). These associations want to make the process of investing in Mutual Funds a household names and the Asset Management Companies aim to do the same. Hence, the chances of a Mutual Fund scheme going bankrupt despite regulations are slight and negligible.

You may stick to schemes offered by popular Fund house names..

Mr.Reddy please let me know where or how do you rank Life insurance (excluding term plans) investments. My no. is 97420818**

Dear JAYARAM,

I am firm believer that insurance and investment should never be mixed.

Traditional life insurance plans (Endowment & Moneyback) yield lower returns. And for plans like ULIP, mutual funds can be a better choice.

Hey Sreekanth,

i am so much impressed with you . i mean you explain everything with so much details.

very helpful thanx buddy.

Thank you dear Vikas.

Keep visiting ReLakhs!

Dear Sree

1. Nice article as usual and always.

2. It will be highly appreciated if for a financial year could be made, as some changes are bound to occur in each FY. In addition–if we could add on the IT sections applicable for various stages.

Looking forward for an updated Table for For FY 2018-19.

Thanks

G S Dhillon

Dear Mr Dhillon,

2 – I have already included the features related to ‘tax implications’ in the tabular data. As when there are changes being proposed in the Financial Budget(s), will surely try to update them. Hope I got your point correctly.

Thanks for the suggestion.

hey such a nice blog

I am a big followers of your blog’s Your article is very useful for us how can I reach you directly sir please tell me

Dear Mr Chauhan,

You can reach me through the Service-Contact page..

Sreekanth ji,

I am regularly reader and follower of your blog. Very nice information .

I would like to know more about PMVVY.

Should we go for investment in above ? How much

Dear Sunil ji,

Thank you for following my blog posts!

You may kindly go through this article @ PMVVY – Features & Review