I am paying my home loan since last 2 years and eats up 40% of my salary every month. I used to wonder should I invest whatever is left in mutual funds or repay my home loan.

This dilemma is faced by a lot of homeowners in India. We don’t like to have loan on our head and we want to repay it as soon as possible.

To understand this, I did a cost benefit analysis with focus to repay my home loan in the shortest period time without getting swayed with emotions.

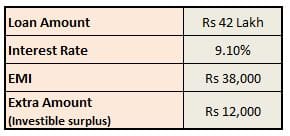

Facts on My Home Loan

I have a 20-year home loan of Rs. 42 Lac at 9.1% (base rate so didn’t change much) from SBI with monthly EMI of Rs. 38,000 and I can spare Rs. 12,000 more per month for investment (or) pre-paying home loan.

So, math should work out if I am able to generate 9.1%+ from mutual funds.

Investing in Mutual Funds

Advantages of investing in mutual funds

- High Returns : Mutual funds have potential to give higher returns if invested for long term and chosen wisely. I am targeting reasonable 14% returns from 10 years SIP.

- Tax Benefits : The principal component of your EMI of home loan will be considered for tax benefit under Section 80C. Even interest paid on home loan has exemption of up to 2 lakhs every year under Section 24.

- Liquidity : You will have the ability to maintain your liquidity. I am less worried about liquidity since I don’t expect much risk in my job.

Disadvantages of investing in mutual funds

- Risky : If mutual funds generate very low returns or you are not able to pay your home loan due to some reason then you might lose more than you gain. Considering my expectation of returns, tenor and way of investing as SIP, I think it’s reasonably under control.

Pre Paying Home Loan

Pros

- Interest rate : By prepaying home loan, we effectively save the interest that we would need to pay with EMI.

- Free mind : You will be debt free (hanging sword) and you live without this burden.

Cons

- Liquidity : You will lose your liquidity as in case you need money for any emergency then you are stuck.

- Taxes : Over and above you will get less tax benefit on interest post 7th year and end up losing huge amount in taxes also.

Let’s predict my situation after 10 years

Case 1 : If I invest Rs. 12,000 per month in SIP

| Loan Amount | Rs. 42 Lacs |

| Principal Re-Paid in 10 years | Rs. 12 Lacs |

| Outstanding Principal Amount after 10 years | Rs. 30 Lacs |

| Accumulated SIP Value | Rs. 30 Lacs* |

(*Assume 14% returns on mutual funds)

So, if I do a SIP in mutual funds of Rs. 12,000, I can pre-pay my left loan in 10th year using my corpus which has been accumulated through Mutual Fund SIPs. You may also use this corpus for any of your other long-term goals.

Case 2 : If I pre-pay home loan by paying Rs. 50,000 instead of Rs. 38,000 per month

| Categories | With Prepayment |

| Loan Amount | Rs. 42 Lac |

| Principal Re-Paid during 10 years | Rs. 35 Lac |

| Outstanding Principal Left after 10 years | Rs. 7 Lac |

So, if I use Rs. 12,000 to pre-pay my loan, I will be left with Rs. 7 Lacs outstanding loan amount after 10 years.

Summary

So, it’s pretty clear from the above calculation that investing while paying home loan can be more beneficial than just prepaying your home loan with extra savings amount.

Over and above there are other benefits like liquidity, which give you flexibility. So, be smart and take maximum benefit from your home loan by doing cost-benefit analysis.

This is a guest post by Ishan of Groww.

About Author

Ishan Bansal is a CFA and has been investing since last 10 years. He is the co-founder of Groww, a startup that is making investing simple in India. He has worked with companies like Flipkart and ICICI Bank and has graduated from BITS Pilani and XLRI

Continue reading :

- How to select right Mutual Fund Schemes based on Risk Ratios?

- What is 200 Day May Average? How to use it when investing in Mutual Funds?

- Should you avoid investing in Mutual Fund Schemes with higher NAVs?

Kindly note that ReLakhs.com is not associated with Groww. This is a guest post and NOT a sponsored one. We have not received any monetary benefit for publishing this article. The content of this post is intended for general information / educational purposes only.

(Assumptions : MF returns @ 14% 7 Home loan interest rate around 9%. Kindly note that Mutual fund investments are subject to market risks and returns are not guaranteed.)

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net) (Post published on : 03-November-2017)

Join our channels

If you are looking for most affordable Home Loans in India, try India’s first loan distribution company, mymoneymantra. We have an association of over 50+ banks and NBFCs and have experience of more than 25 years in providing financial services – Secured Loans, Unsecured Loans, Credit Cards, Insurance.

yes sir i looking for home loan, but my CIBIL score is not as good as it should be, but i heard there is some ways to get a loan even from Leading banks or NBFCs. kindly please advise how to apply to get a loan with suitable interest rate %.

Thanks

Rohit Bidhuri

Hi Srikanth,

can you please provide your view on the Guaranteed insurance plan, like Aditya Birla Sun Life Insurance Guaranteed Milestone Plan or any other plan.

is it advisable to invest in such type of instruments or not.

kindly provide your view and how it will work .

regards

Mihir

Dear Sir,

Thanks a lot for your information, Great job keep it up

Dear Sreekanth,

Ishaan Bansal article is Very nicely explained. Congrats to him. My small doubt, will you advice home loan preclosure considering its income tax benefits. Think of next scenario after 10 years. Continue same MF investment at 14% targeted CAGR and continue with the home loan instead of preclosing it. I think it would be more beneficial and you will have huge corpus in your hand by MF and home loan closed in next 10 years. Hope i am clear what i mean to say. If you dont preclose and continue with both, you will be in more profit i feel ( at the end of loan tenure of 20 years and 20 yrs of MF investment)

regards

RAJ

Completely agreed with you Raj. I would just say if you can continue based on your other commitments don’t prepay.

In this analysis, I was just trying to compare from preceptive of prepaying now or later.

Thank you dear Ishan for replying…agree with your views!

Hi,

I am too planning to take a home loan of 40L for 20/ 25 Years. How can I benefit from both investing in MF and paying EMIs at the same time. My EMI would nearly be 50% of my Salary.

Kindly guide pls.

Hi Sumit

If you can afford to invest after EMI and you forsee that you can continue to invest for long term (10 yrs +), do a SIP along with home loan. You will more value out of your money.

Please switch your Home loan from SBI Base rate to MCLR system

I did that and now my interest rate is 8.7% and earlier it was like you about that 9.4% or 9.3% something

Please read for details : https://goo.gl/MUQv3D