Life Insurance Corporation of India (LIC) has launched a New Whole-Life plan called as ‘LIC Jeevan Umang‘ on 16th May, 2017. This new plan from LIC is a traditional, Non-linked, with-profits, Whole Life Assurance and Limited Premium Payment Option plan.

What is ‘Whole-Life Insurance Plan’? – It is a life insurance policy which is guaranteed to remain in force for the insured’s entire lifetime. The Sum assured is paid to the Policyholder’s nominee in the event the insured dies.

The main feature of LIC’s New plan – Jeevan Umang is it provides annual Survival Benefits from the end of the PPT (Premium Paying Term) till policy maturity and also pays lump sum amount at the time of maturity (or) on death of the policyholder (during the policy tenure).

In this post, let’s understand the key features & benefits of LIC Jeevan Umang Policy.

Key Features of LIC Jeevan Umang Whole Life Plan

Below are the main eligibility conditions to buy LIC’s new policy – Jeevan Umang;

- Minimum Age Entry : 90 days

- Maximum Age at Entry :

- 55 years for 15 year premium period

- 50 years for 20 year premium period

- 45 years for 25 year premium period

- 40 years for 30 year premium period

- Minimum age at the end of PPT : 30 years

- Maximum age at the end of PPT : 70 years

- Age at Policy maturity : 100 years

- Policy Term (Tenure) : 100 – age at entry. (For example : If a 30 year old individual buys LIC Jeevan Umang policy then the policy term would 100 years minus 30 years = 70 years.)

- PPT (Premium Paying Term options) : 15, 20, 25 & 30 years

- Minimum Basic Sum Assured : Rs 2 Lakh

- Maximum Basic Sum Assured : Not Applicable

- Optional available Riders : Accident Death Benefit & Disability Rider, New Term Assurance Rider & New Critical Illness Benefit Rider.

Benefits under LIC Jeevan Umang Policy

- Death Benefits under Jeevan Umang Plan ;

- On death before the commencement of Risk: An amount equal to the total amount of premium/s paid without any interest shall be payable. (Life assured aged 8 or more, risk will commence immediately.)

- On death after the commencement of Risk: Death Benefit is defined as sum of “Sum Assured on Death” and vested simple reversionary bonuses and Final Additional Bonus, if any shall be payable to the Nominee. Where “Sum Assured on Death” is defined as the highest of ;

- 10 times of annualized premium (or)

- Sum assured on Maturity (or)

- Absolute amount assured to be paid on death ie Basic Sum Assured. (The death benefit will not be less than 105% of all the premiums paid as on date of Death.)

- Survival Benefits :

- On the life assured surviving to the end of the premium paying term and all the premiums in policy have been paid, Guaranteed survival benefits at the rate of 8% of Sum Assured will be available annually after completion of the premium paying term till maturity or death which ever is earlier.

- First survival benefit shall be paid at the end of the premium paying term and thereafter on completion of each subsequent year till life assured survives or policy anniversary prior to the date of maturity, whichever is earlier.

- Maturity Benefits under Jeevan Umang Plan : Maturity benefit = Basic Sum Assured + Simple Reversionary Bonuses + Final Additional Bonus (if any) shall be payable to policyholder on surviving to the end of the policy term.

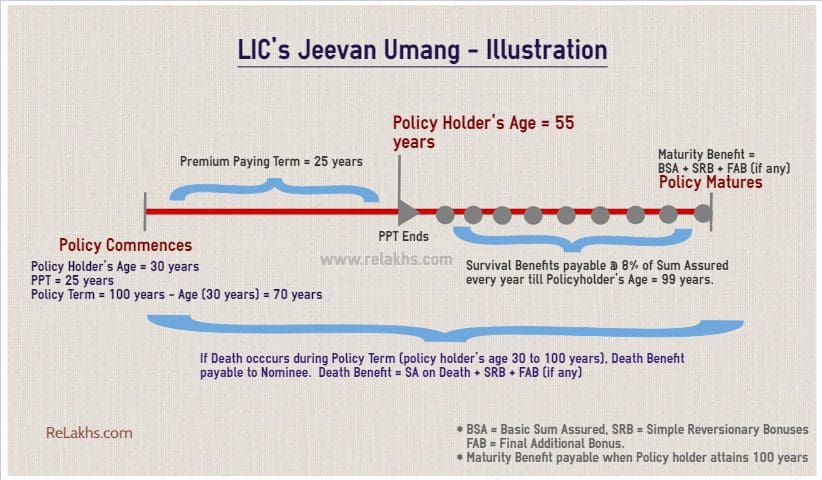

Graphical Illustration of LIC Jeevan Umang Plan – How does this plan work?

I have tried to explain the features of Jeevan Umang Policy and how it works through the below info-graphic. (You may click on the image to open it in a new browser window.)

Let’s consider an example – Policy holder’s current age is 30 years (male), buys this policy for Sum Assured of Rs 10 Lakh and with Premium Paying Term as 25 years. So, the policy term would be for 70 years (100-30 years).

The policyholder has to pay premiums for 25 policy years (till he attains 55 years of age). After PPT ends, survival benefits @ 8% of Sum assured are payable till one year before policy maturity year. So, benefits are payable till policy holder attains 99 years. Maturity benefit is payable to policyholder when he attains 100 years (ie policy term completes, on 70th policy year).

In case, policy holder expires during the policy term then death benefit is payable to his nominee.

LIC Jeevan Umang & Returns Calculation

Below is the IRR (return on investment) calculation on Jeevan Umang policy.

The above calculation is for sum assured of Rs 2 Lakh, PPT is 25 years, for a 30 year old male and no optional riders have been chosen. The premium of around Rs 7,879 is payable for 25 years. From 26th policy year onwards, survival benefit is payable. On surviving till 70th policy year end, the policy holder will get a maturity benefit of around Rs 18.9 Lakh.

I have assumed Final Additional Bonus of around Rs 3,550 per Rs 1,000 Sum Assured.

I have also assumed Simple Reversionary Bonus @ Rs 70 per Rs 1,000. I believe that this is on a higher side. If you observe the past bonus rates declared by LIC, Rs 70 has been the SRB on Whole Life plans. However, Jeevan Sugam can be considered as a combination of Whole life + Money back plan (as survival benefits are payable). So, LIC may or may not declare higher bonus rates on this plan when compared to their pure Whole-Life plans. (Read : ‘LIC’s latest Bonus Rates for 2016-17‘)

My Opinion on LIC’s new Whole-Life Plan – Jeevan Umang

- Is Life insurance cover required till 100 years? -It is not required. Ideally, as long as you have liabilities to take care of and as long as you have family members who are financially dependent, you need to have life insurance cover. Almost all of us would like to lead a debt free life and with no financial obligations during retirement age. So, I believe that having adequate Health insurance cover is a must for whole-life and same may not be the case with Life insurance cover.

- Adequate Life cover : You nee do to pay Rs 7,879 as premium for a Sum Assured of Rs 2 Lakh. If your priority is to get sufficient life cover at cheaper premium rates then you can buy a Term insurance plan. A 30 year policy holder (non-smoker) can buy an e-Term insurance policy from LIC itself with a life cover of Rs 50 Lakh by paying a premium of Rs 7,812 p.a. for 30 years. (Read : ‘Best Term Life Insurance plans‘)

- Investment Returns: If you would like to invest in this plan for decent Returns then you may be up for a disappointment. These kind of traditional plans can at best give you 5-6% returns. The returns are primarily dependent on the quantum of bonuses declared by LIC. Also, note that these bonus amounts are not paid to you immediately. They are accrued and paid on maturity or claim. Compounding is not done. If your investment objective is better returns then there are plenty of other investment options available in the market. (Read : ‘List of best investment options‘)

- Tax Savings : If your objective is tax saving cum better returns, you may consider investing in an ELSS mutual fund scheme. Even PPF (Public Provident Fund) can give your better returns than this policy and it is tax-efficient too. (Read: ‘Best ELSS Tax saving Mutual Fund Schemes‘)

Continue reading :

- LIC New Plans 2019-2020 | Features, Snapshot & Review of all the Plans

- If life is unpredictable, Insurance can’t be optional!

- Term Insurance plan : Is it just a waste of your money?

- Traditional Life insurance plan : a terrible investment option?

(Post first published on : 13-May-2017)

Join our channels

hi

please suggest me i am 37 years old i want pay premium for 15 years

i want to pension 15000/-

how much amount i have to pay early.

Dear srinivasball,

May I know if you have already invested in any other investment schemes? Have you calculated your retirement plan goal amount?

You may go through below articles :

* Retirement Planning in 3 Easy steps

* List of all Popular Investment Options in India – Features & Snapshot

Age

32 Yrs

Instalment Premium

₹ 98,180.00

Policy Benefits

₹ 12,50,000

Premium Paying Term

15 Yrs

Policy Term

68 Yrs

Commencement Date

28/12/2017

Date of Maturity

28/12/2085

Can you help me in finding the survival benefits and and maturity benefits for the above please

mail me on mitesh_s_jain**@yahoo.co.in

Dear mitesh,

Survival benefit :

On the life assured surviving to the end of the premium paying term and all the premiums in policy have been paid, Guaranteed survival benefits at the rate of 8% of Sum Assured will be available annually after completion of the premium paying term till maturity or death which ever is earlier.

First survival benefit shall be paid at the end of the premium paying term and thereafter on completion of each subsequent year till life assured survives or policy anniversary prior to the date of maturity, whichever is earlier.

Maturity benefit = Basic Sum Assured + Simple Reversionary Bonuses + Final Additional Bonus (if any) shall be payable to policyholder on surviving to the end of the policy term.

So, MB is dependent on the assumed bonus rates as mentioned in the article.

You can expect returns of around 5% from this plan.

lic policy are costly and worthless

LIC just fools people with past performances when they had monopoly. I was given just 67K in place of 1.10 Lakhs – Sum Assure at maturity.

They never show to customers IRDAI prescribed Illustrations of guaranteed – means 0 bunses / 4% yield/8% yield. WHY NOT WHEN ALL COMPANIES ARE MANDATED.WHY NOT LIC do fair play.

They are blinding us of times 1956 to 2000 monopoly. I have seen till date they are fully computerized. Customers are treated badly . Agents and clerks take money to release claims.

LIC is just cashing on its name and fooling people. As my sum assure in Jeevan Surbhi was 1.10 lakhs whereas the maturity which i got was just 67K..Moreover majority play is on assumptions and past performance. Because of gotlas recently i saw 5000 Cr. advertisement ghotla for which High court has asked clarification.

Your IRR computation missed out an important element. At the end of premium paying terms (age 55), the policy holder should get Maturity benefit in addition to Survival benefit. Please read the term of policy carefully. You have mentioned this in your description as “Maturity Benefits under Jeevan Umang Plan : Maturity benefit = Basic Sum Assured + Simple Reversionary Bonuses + Final Additional Bonus (if any) shall be payable to policyholder on surviving to the end of the policy term.” This will make whole calculation of IRR different.

Dear Narasimhan,

Kindly note that I have included Basic sum assured (Rs 2Lakh) besides Simple Reversionary bonuses + FAB to arrive at Rs 18.9 Lakh as maturity benefit.

It may be good for those who will invest and take the tax benifit at the early age. As per my calculation , if I take a term of 15 years with a SA or Rs.10 lac , it will take 15 year to get back my money to return at an rate of 8% of SA. So it is not at all a good plan.

Hi Sreekanth Reddy, i am not sure why you outright reject this plan from LIC.

Take for instance someone who had enough equity exposure thru MF or stocks and want to look at confirmed returns thru debt instruments for a monthly/steady income after retirement. Someone say at age around 40. Why cant he/she look at this as this seems attractive to me. This is how I compare

LIC Umang Policy – SA 25L, Monthly Premium of ~17K.

After 15 years, confirmed pension of 2L (8% of 25L SA) & also the corpus becomes ~40L growing at 5% PA. I am considering only the minimal without any bonuses etc.,

So, if I continue to get the 2L PA for 10 more years, the corpus would have grown to 70L & I would have got 20L (10 years * 2L PA pension) making it 90L.

I compare this to monthly RD & then FD after 15 years (Remember, someone not looking at equity investments)

Monthly investment of 17K on a RD with 5% interest (After Tax) gives about 45L. Putting this in FD again for 5% after tax returns will give 2.3L per year with the principle remaining at 45L.

Note – This is not considering the bonuses that LIC gives and also, considering 5% returns on RD & FD. I am not sure if we can look at 5% interest after tax after 15 years from FD/RD .

What am I missing. If what I have done is all correct & true, why should anyone not invest in LIC Umang?

Sri

Dear Sriram,

I have presented the Pros & Cons and arrived at suggestions. I have not ‘rejected’ this plan on ‘outright’ basis!

You may kindly go through the points given under the sub-title -‘My Opinion on LIC’s new Whole-Life Plan – Jeevan Umang’.

Hi Sreekanth

I went through that.

I was expecting you to comment or give your opinion on the comparison example I have written about. And as I said, if someone wants a guaranteed pension after retirement, what other better products you can suggest?

Sri

Dear Sriram,

My suggestions are generally based on keeping in mind of the majority of the investors.

Don’t you think that you are giving a very hypothetical situation – ‘Take for instance someone who had enough equity exposure thru MF or stocks and want to look at confirmed returns …’ .

* Do you believe that majority of us have adequate investments in equity oriented products in India?

* In a growing enconomy like us, with an average inflation of around 5 to 8%, any returns beyond 8% is what one needs to aim for, so that he/she can get decent real rate of return.

* How many of us have adequate life cover in India? – If one needs life cover, he/she does not need to buy these kind of unaffordable traditional product for life cover.

If one has invested adequately in equity oriented products, have adequate life cover and is content with 5% returns, he/she can consider these kind of products.

But, how many of us can meet this criteria?

Do note that accumulation of corpus through these kind of products is highly dependent on bonus rate (which is not guaranteed one, can vary year on year).

Thanks Sreekanth. Obviously I am not trying to say LIC Umang is the best, but I have done some calculation, and I want opinion from experts like you…. See below (I am comparing this LIC with equity investments)

Assume someone is investing 10,000 per month for the next 20 years (from 2018 to 2038) – until retirement in Equity with an assumed CAGR of 12% (I think 12% is pretty decent?)

In 2038, the corpus would be ~91L

After retirement, investing this 91L in a debt instrument for another 10 years with an assumed 5% after tax returns

So every year, this is what we’ll get

2039 ₹ 463,602.00

2040 ₹ 463,602.00

2041 ₹ 463,602.00

2042 ₹ 463,602.00

2043 ₹ 463,602.00

2044 ₹ 463,602.00

2045 ₹ 463,602.00

2046 ₹ 463,602.00

2047 ₹ 463,602.00

2048 ₹ 463,602.00

So, In 2048 – the total returns would be 1,37,36,020

Comparing the same with LIC Umang, premium of 10,000 per month for 20 years

From 2038, YoY guaranteed pension would be

2039 ₹ 1,76,000.00

2040 ₹ 1,76,000.00

2041 ₹ 1,76,000.00

2042 ₹ 1,76,000.00

2043 ₹ 1,76,000.00

2044 ₹ 1,76,000.00

2045 ₹ 1,76,000.00

2046 ₹ 1,76,000.00

2047 ₹ 1,76,000.00

2048 ₹ 1,76,000.00

And if we close the policy in 2048, along with the pension & surrender value, the total guaranteed returns would be ₹ 11,046,200.00

Which is better. Guaranteed 1.1 Cr or Equity returns of 1.3 Cr?

If we reduce the equity CAGR by 2% (making it 10%), the total returns at the end of 2048 would come to ₹ 10,717,000.00 (Lesser than LIC Umang)

* Returns from Umang that I have quoted is guaranteed minimum. I am not considering the bonuses etc.,

* Considering returns of 5% after tax from debt instrument after 10 years is a very tall order

I am not an expert like you in these, so I want to know from you if anything that I have calculated and projected is incorrect. Again, I am not a LIC agent – just trying to compare returns. Thats all.

Thanks.

Dear Sriram,

You havn’t answered my questions!

No one is an expert here! We are all learning together!

* How did you get Rs 4.63 Lakh? Is Rs 91 Lakh re-invested for 10 more years and 5% withdrawn during these 10 years?

* Does this plan offer pension?

* How did you get Rs 1.76 Lakh? What is the accumulated corpus in 20 years? How did you arrive at this corpus?

* How did you arrive at surrender value, may I know the calculation? (Rs 1.1 cr in 2048).

Regarding the corpus accumulated through ‘equity oriented products’, the investor can have the flexibility and control to re-invest the accumulated wealth after 20 years, he/she can have a look at his/her financial position, alternative investments, expectations etc and can plan investments.

How did you get Rs 4.63 Lakh? Is Rs 91 Lakh re-invested for 10 more years and 5% withdrawn during these 10 years?

91L is invested in a debt instrument assuming 5% interest after tax. that gives 4.63L per annum.

Does this plan offer pension?

LIC Umang gives 8% on SA till 100 years of the insurer.

How did you get Rs 1.76 Lakh? What is the accumulated corpus in 20 years? How did you arrive at this corpus?

SA with 10,000 per month premium is 22,00,000. 8% PA on it gives a pension of 1.76 Lakh till 100 years. Accumulated corpus in 20 years is ~45.3L. Arrived based on LIC app. These are guaranteed & additional bonus would be given, which I have not considered.

How did you arrive at surrender value, may I know the calculation? (Rs 1.1 cr in 2048).

At a minimum, the corpus (which is 43.5%) grows at 5% every year. This is again guaranteed. You can get this also from LIC app (available with agents). So in 2048, the corpus would be 92.8 L. Adding the 1.76L for 10 years gives 1.1Cr.

Seems good only to me. What do you think.

Dear Sriram,

Kindly re-visit my calculation of IRR for the entire policy term.

Even after accounting for non-guaranteed bonus rate (FAB & SRB) + survival benefit (not pension) of 8% of SA, the IRR turns out to be around 5 to 6%, which I believe is way less with inflation of around 6% for the last one decade or so.

Kindly note that bonus rates vary year to year and I have assumed them on the higher side only in my sample calculation.

Considering the control & flexibility part as well, given a choice, personally I would bet my money on equity products to these kind of traditional life insurance plans.

However, if you are convinced and have a conviction that this is better than other alternatives, you may kindly go ahead with your plan(s). It is PERSONAL Finance.. you are the best person to decide what is good for you financially!

Hi,

I am being suggested by friend to invest in Jeevan Umang and Jeevan Labh of Rs20Laksh. Currently I am 45 yrs of age. Should I invest in the above two or look for something else. The premium in both the case is too high and I am in dilemma as I am in private job. Please suggest at the earliest on mail if possible.

Thanks

Pramod

samalpramod**@gmail.com

Dear Pramod,

Did you go through above article?

Also, kindly read my review on Jeevan Labh plan.

May I know your requirement? Is it getting adequate life insurance cover or decent returns on maturity?

Hi,

Thanks for the reply. Yes I went through the above post. I am looking for investment. Though I have ensured myself adequately, I am not sure that is a good amount as they say you need to ensure 10 times of of your annual salary. In that sense I am insured twice of my annual salary. Please suggest is it better to take an term plan with investment as suggested in above post.

Thanks

Pramod

Dear Pramod,

If you are under-insured, suggest you to buy a Term insurance cover and invest in some other better alternatives for wealth accumulation.

Kindly read :

Traditional life insurance plans – a terrible investment option?

IS term plan a waste of your money?

Best Term insurance plans

Approx premium will be 2 lacs yearly

Dear Jayesh,

So, how many individuals in India can afford to pay this much as annual premium?

Don’t you think this is un-affordable?

Instead, an individual can buy a Rs 50 Lakh term plan for say around Rs 10k pa (approx) and then invest the rest of the amount in better investment avenues as per his/her requirements and try to get positive real rate of return from the investments.

What say?

So, if one takes these kind of traditional life insurance policies, how does it benefit if unfortunately a person meets with an accident and is permanently disabled?? (assuming a person goes for only Base policy without any riders).

Say the Sum assured is Rs 50 lacs the policy holder premium will get stop plus he will get Rs 50 Lacs in equal installments in 120 months i.e. 41000 every monthly. plus he will get maturity as usual if the policy attains maturity term and policy holder ia alive.

Disability benefit is always inclusive in the premium whereas sometimes pWB is extra.

Dear Jayesh,

Do you mean to say that Accident benefit rider and/or Disability benefit rider is always inclusive in base premium?

And what would be the approx premium for Rs 50 Lakhs for this policy for a healthy 30 year old male (for an ex)??

Lic knows very well their are some mind who are very pathetic to apply for term plans and forgets their old age.”

Means : Some Humans feels during the period of earnings they should only apply for term plan whereas they don’t there are other risk too such as accident injury and disability to work which can also make loss of earnings.

Dear Jayesh,

So, if one takes these kind of traditional life insurance policies, how does it benefit if unfortunately a person meets with an accident and is permanently disabled?? (assuming a person goes for only Base policy without any riders).

Sir, i want clarification regarding policy surrender value, for example if i take Rs/-1200000 sum assured, what will be the surrender value in 7th year?

Dear Rajesh ..You can get surrender value details on LIC website.

U will get on surrender is Paid Premium Amount Plus 394000 as bonus

Jayesh 9323485795

Why is LIC coming up with such pathetic and irrelevant products instead of promoting term plans?

Lic never comes any pathetic plans. Lic knows very well their are some mind who are very pathetic to apply for term plans and forgets their old age. Trust Jeevan Umang is a new feather to provide 8% tax free income till death with self desire maturity and minimum commitment of only 3 yrs to pay the premium for all benefits.

Dear Jayesh,

I dint get your point – “Lic knows very well their are some mind who are very pathetic to apply for term plans and forgets their old age.”

Could you please re-phrase this for me??

Hello, Mr Reddy,

thanks for your views, just want make one point that IRR is considering 100 years, which is only in exceptional case, if some one die after 70 years then IRR may be around 8%, if you consider 100 years then obsessively IRR will be low.

SIR CAN YOU PLEASE CLARIFY REGARDING THE TAXABILITY OF THE SURVIVAL BENEFIT OF 8% EVEN AFTER THE POLICY MATURITY EVERYYEAR,

Dear Mr Joshi,

Money back amount received by you are tax free under section 10 (10) (d) as these are received by you as survival benefit from a life insurance policies, provided if your policy’s sum assured is more than 10 times the annual premium.

im 32 years old and my boy child is 4years old. and i am saving only rs 2000.00/ month from my income from a small bussiness and i have’nt any policy not having any type of savings..

so you r requested to please suggest me the best way to save some money for either my future or my son future and my whole family in approx 15 years..

Dear prasad,

Suggest you to kindly first take a Term insurance plan, personal accident cover and a Health insurance cover for family.

Kindly read this articles and you may revert to me..

Financial planning pyramid..

If life is unpredictable, insurance can’t be optional!

Please take a combination of Bima Diamond and Jeevan Umang Money back+Retirement

Jayesh 9323485795

the viability can be ascertained only after we get the prm rates

jeevan umang plan is a realy very excellent insurance plan. you can buy this plan as a pension plan also. you can plan the future of your children. marriage provision of a girl child and for higher education of children also.

Dear Avinash,

May I now how is it possible to plan for these goals? and what Cost?

Kindly share your views.

pls send your details

Keegan umang is going to be more attractive among public. Since the kind of benefits this plan offers can’t match by one insurer.

1. Guaranteed 8% annual return on SA which is not even available in pension as scheme and the annual return is fully tax free

2. The insured also secured with life time insurance coverage

My advise is that this plan is more suitable for people who thinks about pension

Thanks,

Jagadeesh

Lic advisor 9710037371

This is reasonable argument. guarantee of 8% interest after 25-30 years on whatever you accumulate till then is a big risk for provider. No other institutions can match it. Those who criticize aren’t considering decreasing rates of interest as a country develops. what you buy here is not returns to build corpus but guarantee on returns on corpus after a long duration of time. effective 5-6% I agree but that would be too good after 25 years.

Dear Asit,

Thank you for sharing your views!

1 – Interest rates can be cyclical. What if the rates increase and there are better alternatives over the next many years?

Have you accounted for inflation and raise of prices in a growing economy like India?

2 – All of us are aware of the fact that ‘insurance penetration’ is very low and average insurance cover per head is also low. So, the first priority for many Indians is to get adequate life cover at affordable rates through Term plan(s). And these kind of plans are surely not affordable to get adequate life cover.

3 – If one has to accumulate retirement corpus through a plan like this, what is the total cost involved to get decent accumulation (can be very high) and dont you think not investing in other better alternate avenues can itself is a big risk factor.

May I know your views on PPF Vs these kind of plans in terms of returns.

Hi Sreekanth

What are you other investment avenues in comparison to LIC Umang? PPF is different. Upon maturity you will have to close it and invest the corpus into a FD. The interest rate would be at best 5% and that too is taxable. Dont compare LIC with equity instruments.

Is there anything else that you think that is comparable and is equally good?

regards

Sri

Dear Sriram,

May I know, what do you mean by – ‘PPF is different?’

PPF matures after 15 years, if an account is opened now. How can you predict interest rates on FDs are going to be around 5%, 15 years from now??

Why should not we compare with equity investments, when someone is investing for long-term?

By the by, LIC as an institution invests thousands of crores in Equities year on year!