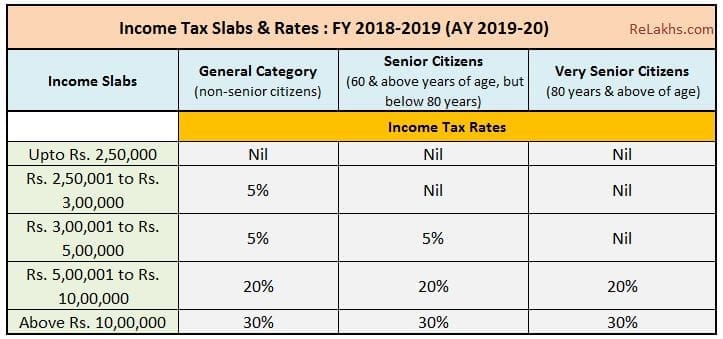

Indian Finance Minister, Shri Arun Jaitley has tabled today, the Union General Budget 2018-19 in the Parliament. Below are the latest Income Tax Slab Rates for FY 2018-19 or AY 2019 -20. Kindly note that there has been no changes made to personal Income tax structure. (FY is Financial Year and AY is Assessment Year)

Latest Income Tax Slab Rates FY 2018-19

The income tax slabs & rates are categorized as below;

* Individual resident aged below 60 years.

* Senior Citizen (Individual resident who is of the age of 60 years or more but below the age of 80 years at any time during the previous year) &.

*Super Senior Citizen (Individual resident who is of the age of 80 years or more at any time during the previous year).

Budget 2018-19 : Key Highlights

Below are the latest proposals that have been made in Budget 2018-19 ;

- Income Tax Slabs : No change has been proposed on tax slab rates.

- Standard Deduction : A standard deduction of Rs 40,000 in lieu of travel, medical expense reimbursement and other allowances has been proposed for salaried employees and pensioners.

- Increase in Cess : Currently, there is 3% cess on personal income tax (2% for primary education and 1% for secondary and higher education). This will be replaced with 4% Health & Education Cess.

- Senior Citizens & Income Tax exemptions :

- The Interest income earned on Fixed Deposits & Recurring Deposits (Banks / Post office schemes) will be exempt till Rs 50,000 (current limit is up to Rs 10,000). This deduction can be claimed under new Section 80TTB. However, no deductions under existing 80TTA can be claimed (the current limit for FY 2017-18 u/s 80TTA is Rs 10,000).

- Currently, if interest income on Bank/Post office deposits is more than Rs 10,000, TDS is deducted u/s 194A. Budget 2018-19 has proposed to raise the threshold for deduction of tax at source on interest income for senior citizens from Rs 10,000 to Rs 50,000.

- The premium paid on health insurance plans by senior citizens of up to Rs 50,000 can be claimed as tax deduction under Section 80D (current limit is Rs 30,000).

- The limit under section 80DDB has been proposed at Rs 1 lakh towards medical expenses, for treatment of Critical Illnesses.

- The maximum investment under Pradhan Mantri Vaya Vandana Yojana has been increased to Rs 15 Lakh.

- No Section 80TTA Benefit : Section 80TTA of Income Tax Act offers deductions on interest income earned from savings bank deposit of up to Rs 10,000. From FY 2018-19, this benefit will not be available for late Income Tax filers.

- Single/Multiple year Premium Health Insurance Policy : In case of single premium health insurance policies having cover of more than one year, it is proposed that the deduction shall be allowed on proportionate basis for the number of years for which health insurance cover is provided, subject to the specified monetary limit.

- Long Term Capital Gains on Shares & Equity Mutual Funds :

- The Budget 2018-19 has proposed to introduce tax on Long Term Capital Gains on sale of stocks and equity mutual fund units.

- LTCG tax at 10% on gains of above Rs 1 lakh from Equities & Equity mutual funds.

- No change has been proposed to STT tax rate.

- No change has been proposed to holding period to arrive at LTCG/STCG.

- STCG will continue to be taxed at 15%.

- Any LTCG accrued on Stocks/Equity funds up to 31-Jan-2018 are tax-free, if held for 1 year period.

- For Example : If the equity share is purchased 6 months before 31st January 2018 at Rs 1,000 and the highest price quoted on 31st Jan is Rs 1,200. There will be no tax on the sale, if the stock is sold after 1 year.

- However, any gains in excess of Rs 200 earned after 31st Jan 2018 will be taxed at 10% if this share is sold after 31st July 2018.

- Equity Oriented Mutual Funds will now have to pay a dividend distribution tax (DDT) of 10%. (Read : ‘10% LTCG Tax on sale of Stocks/Equity Mutual Funds.’)

- The Bonds issued u/s 54EC for saving of LTCG on sale of property will now have a lock-in period of 5 years instead of 3 years from fY 2018-19.

- The four state-owned general insurance companies namely : New India Assurance, Oriental Insurance, National Insurance and United India may be merged into one Entity and the new entity would be listed on the Stock exchanges.

- Gold Monetization Schemes to be revamped.

- Budget 2018-19 has proposed to keep the EPF deduction at 8% (instead of 12%) for women employees, in the first 3 years of their employment.

- Govt to pay Employer’s contribution 12% of wages to EPF for new employees of all sectors in the first three years of employment to boost job creation.

- The new budget has proposed to launch National Health Protection Scheme, to provide Rs 5 Lakh health insurance cover for 10 cr poor families. This can benefit 50 crore individuals in India.

- Loans to the tune of Rs 3 lakh crore would be sanctioned under Pradhan Mantri Mudra Yojana during the FY 2018-19.

Continue reading :

- Income Tax Slab Rates for FY 2017-18 / AY 2018-19 (Budget 2017-18)

- List of Income Tax Exemptions FY 2017-18 : Important IT Deductions for AY 2018-19

- Income Tax Declaration & List of Investment Proofs

- Best ELSS Tax-saving Mutual Fund Schemes

- Income Tax Deductions List FY 2018-19 | List of important Income Tax Exemptions for AY 2019-20

- Rs 40,000 Standard Deduction from FY 2018-19 | Does it really benefit the Salaried?

- FY 2018-19 Section 80TTB | Tax Exemption of Rs 50,000 on Interest Income to Senior Citizens

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net)

(Post published on 01-February-2018)

Join our channels

deductor (DDO) , allow the Donations or not ( section 80g ) of the Employees

Dear NageswaraRao,

80G deductions are allowed as per the applicable eligibility criteria.

If my Total Inxome (say Rs 2 Lakhs) excluding STCG/LTCG from mutual funds is less than exempt slab of Rs 2.50 Lakhs. Also I have Rs 20000 STCG from Equity MF, Rs 25000 STCG from Debt MF, Rs 30000 LTCG from Equity MF in excess of Rs 1 Lakh and Rs 35000 LTCG from Debt MF. My question is wether I will have to pay tax on entire STCG/LTCG?

Dear Gaya,

Your total income is in excess of Rs 2.5 lakh.

LTCG in excess of Rs 1 lakh will attract tax at the rate of 10 percent and not entire LTCG (equity).

STCG rate on equity is 15%.

STCG rate on Debt MF is as per applicable individual’s slab rate.

Related articles :

* Mutual Funds Capital Gains Taxation Rules FY 2018-19 (AY 2019-20) | Capital Gains Tax Rates Chart

* Different Asset classes have different Tax implications – How Returns are taxed?

LATE INCOME TAX RATE

I had started receiving salary, 3 years after the date of joining a Govt aided firm. Now I had received the arrears along with monthly salary of Rs 56029/= after calculating the anticipatory income tax till Feb2019, I was asked to make a payment of Rs46000/= including the tax of the arrears received. Is there any tax exemption scheme to invest the same amount.

Dear Tobias,

Suggest you to kindly consult a CA in this regard.

You may kindly go through this article..

Since the budget was populist with the 2019 elections in mind, there has not been any changes in tax slabs and no added benefits to the middle class as compared to the previous year.

Nice article about Income tax. It will be helpful

Is it possible to get income tax refund of AY 2015-2016 as there was 10% TDS by my contractor under 194J this year, I have not filed returns for AY 2015-2016 as per CDBT circular no. 09/2015 on 9th June

Dear ABISHEK,

You can not file ITR of FY 2014-15 now.

Hello sir

Is rent agreement mandatory for HRA exemption?

Dear Vikash..Yes, advisable to have it.

In view of recent Section 80TTB, whether for Super Sr Citizens, No income tax is payable for FY 2018-19 AY2019-20 for Only Interest income upto Rs.5,50,000/-earned from Bank/Post office/Saving Bank A/C y

Dear Prakash,

Yes.

Dear Sreekanth,

Thanks for confirmation.M/S Clear Tax misguided me and they said, Income Tax on RS. 50,000/- @ 20% will have to be paid, which I do not agree I deleted the correspondence with them. I really wonder how they are misleading.

Hi Prakash

Request you to check the interest income amount mentioned by you in the 1st query which is Rs.5,50,000. So for Rs.50,000 there will no tax but on balance interest income for Rs.5,00,000 there will be 20% tax as correctly suggested by clear tax. You can refer tax slab given in the chart by Sreekanth in this blog. I think the interest amount was Rs.50,000 in your mind but you wrote as Rs.5,50,000 which created the confusion and misinterpretation. Sreekanth also had overlook the figures I suppose.

I apologized to both of u, there will be no tax. I read the slab incorrectly. But bank may deduct the TDS as it exceeding limit of 50,000 & you need to claim refund in your ITR.

If you submit 15-H to the bank that there will not be any income tax payable on the interest income, no TDS will be deducted by the Banks.

Hello sir I would like to know what will be my tax amount for the fy 2018-2019 .I am giving my particulars 1) pension 360000 2) interest on FDs 250000. My investment

In health insurance will be 30000. I am a senior citizen. Can you please show me the

Calculation of tax

Dear Ivarin ji..For FY 2018-19 even the pensioners can claim Rs 40,000 standard deduction.

You may kindly use the calculator available in this link….

Dear Sree,

Could u plz tell me how I can avail standard deduction for medical expense for 2017-2018.

Dear Rajan,

If medical allowance is part of your salary then you can submit medical bills of up to Rs 15k this FY 2017-18 and can claim it.

Dear sir,

Interest on SB acct, up to 10,000/- was not taxable for all and interest on FDs are taxable to all. The increase from 10,000/- to 50,000/- should be applicable to SB interest only and not applicable to interest on FDs. Please clarify.

Dear Subramaniyan,

A new section 80TTB has been proposed to claim tax deduction of up to Rs 50,000 in respect of interest income earned on deposits held by Senior citizens (FDs/RDs).

However, no deduction under section 80TTA shall be allowed in these cases

Also, the TDS threshold limit on interest income earned on Savings a/c has been increased from Rs10,000 to Rs 50,000 u/s 194A.

Below is the extract from Budget document ;

“At present, a deduction upto Rs 10,000/- is allowed under section 80TTA to an assessee in respect of interest income from

savings account. It is proposed to insert a new section 80TTB so as to allow a deduction upto Rs 50,000/- in respect of interest

income from deposits held by senior citizens. However, no deduction under section 80TTA shall be allowed in these cases.

This amendment will take effect from 1st April, 2019 and will, accordingly, apply in relation to the assessment year 2019-20

and subsequent assessment years.

It is also proposed to amend section 194A so as to raise the threshold for deduction of tax at source on interest income for

senior citizens from Rs 10,000/- to Rs 50,000/-.

This amendment will take effect, from 1st April, 2018.”

No body has given correct version of budget including you.No exemption on FDR interest was available to senior citizens.This limit was only for no TDS deduction only but Interest was taken in income.Now 50000 limit is being allowed to them.Nothing said on saving account interest where 10000 deduction was allowed which will remain same

Dear AHUJA,

A new section 80TTB has been proposed to claim tax deduction of up to Rs 50,000 in respect of interest income earned on deposits held by Senior citizens (FDs/RDs).

However, no deduction under section 80TTA shall be allowed in these cases

Also, the TDS threshold limit on interest income earned on Savings a/c has been increased from Rs10,000 to Rs 50,000 u/s 194A.

Below is the extract from Budget document ;

“At present, a deduction upto Rs 10,000/- is allowed under section 80TTA to an assessee in respect of interest income from

savings account. It is proposed to insert a new section 80TTB so as to allow a deduction upto Rs 50,000/- in respect of interest

income from deposits held by senior citizens. However, no deduction under section 80TTA shall be allowed in these cases.

This amendment will take effect from 1st April, 2019 and will, accordingly, apply in relation to the assessment year 2019-20

and subsequent assessment years.

It is also proposed to amend section 194A so as to raise the threshold for deduction of tax at source on interest income for

senior citizens from Rs 10,000/- to Rs 50,000/-.

This amendment will take effect, from 1st April, 2018.”

Hello my salary details are below:

Basic Pay 37625.00

D A 16893.63

H R A 2633.75

Transport Allow 1330.00

Temp Cash Allow 1800.00

Gross Salary = 60282.38

Cash medical benefit 13300 every year.

Is standard deduction good or bad for me?

Dear Tigmanshu,

As of now, you can claim Rs 29260 as allowances, but from FY 2018-19, you can claim Rs 40,000 pa as Standard deduction, that too without submitting any bills to your employer.

Thanks. I got the idea now.

Hi Sreekhant,

If I have purchased shares last year in Sep 2017.

when selling after 1 year, Do i still need to pay LTCG ?

Please confirm if the new LTCG rule doesn’t apply on the people those who have purchased earlier in 2017.

Thanks in advance. cheers.

Dear Nishant,

Yes, you need to pay.

I have published a dedicated article on this topic, suggest you to kindly go through it..click here..

Hi,

Thanks for the wonderful explanation of each points.

I have few doubts:-

1- They have mentioned something related to Saving bank interest: Tax exempt on 30k instead of 10k. ( For whom )

2- LTCG – If I have purchased shares on 1st Jan 2018 ( 5 lakh ) and sold on 2nd Jan 2019 ( 10 lakh ) – ( Do I still need to pay LTCG of 10% on 4 lakh profit after deducting 1 lakh exempt profit ).

Thanks.

Dear Kapil,

1 – It is for Senior Citizens only.

2 – I have published a dedicated article on this topic, suggest you to kindly go through it..click here..

Hi Sreekhant,

I’m not clear on the LTCG, Starting Jan 2018 I started invested in equity & debt MF growth plan via SIP (9 k per month). With long term investment goal of 10-15 yrs. Does the new rule means, the profit will be taxed at 10%, when I plan to withdraw it post 12 months ?

Thanks,

Atanu Dutta

Dear Atanu,

I have published a dedicated article on this topic, suggest you to kindly go through it..click here..