Stocks, Mutual Funds, Fixed Deposits, Bonds, Real estate, Gold etc., are various Asset Classes that are popular among the investor community. It’s very important for investors to have a proper asset allocation to achieve financial goals.

Different asset classes have different tax implications. The returns (or) gains generated by these various asset classes are taxed differently.

For example- the interest income from Bank Fixed deposits is a taxable income, the long-term capital gains of upto Rs 1 lakh from Equity Funds is tax-free, and the capital gains from sale of your property can be a taxable income and so on..

As an investor you should be aware of these tax implications so that you can create a tax-efficient investment portfolio. (However, your investment decisions should not be based on tax-saving criteria alone.)

In this post, let us understand the tax implications on various asset classes, how are the returns / gains from various asset classes like Stocks, Mutual Funds, Real Estate, Bonds, Gold etc., taxed in FY 2023-24?

Asset Classes & Financial Instruments – Tax Implications FY 2023-24 / AY 2024-25

Below are the details of tax implications on investments in various Asset Classes;

How are investments in Stocks Taxed for FY 2023-24?

- If you hold your stock investments for less than 12 months, the gains are treated as Short Term Capital Gains and are taxed at flat 15%. (Applicable for Shares which are listed on stock exchanges and are sold on stock exchanges)

- STT (Securities Transaction Tax) at the rate of 0.1% is charged on sale of Shares.

- If the aggregate amount of dividend distributed or paid during the financial year to a shareholder exceeds Rs. 5,000 then an Indian company shall deduct tax at the rate of 10%. Dividend income is taxable in the hands of taxpayers irrespective of the amount received at applicable income tax slab rates.

- If you hold your stock investments for more than 12 months, the gains are treated as Long Term Capital Gains and are taxed at a 10% rate (plus surcharge and cess), if they reach Rs. 1 lakh in a fiscal year

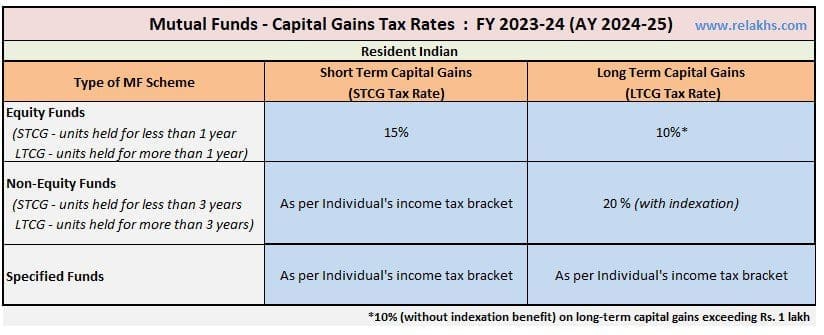

Mutual Fund Taxation Rules AY 2024-25

With effective from FY 2023-24, no indexation benefit is available while calculating long-term capital gains on Specified Mutual Fund (i.e a mutual fund which invests less than 35% of its proceeds in the equity shares of domestic companies). We can consider these specified funds as pure Debt oriented funds and any gains (STCG or LTCG) on these are now taxed as per income tax slab rate. This new rule is applicable for investments made on or after April 1, 2023 only.

With this new amendment, we now have three broad type of funds – Equity, Non-Equity & Specified Funds.

| Percentage of Equity Exposure | 0% to 35% | 36% to 64% | 65% & more |

| Type of Fund | Specified Fund | Non-Equity oriented Fund | Equity Mutual Fund |

Equity Mutual Funds (Regular Equity funds, ELSS, Equity oriented Balanced Funds etc.)

- If you make a gain / profit on your investment in a Equity Mutual Fund scheme that you have held for over 1 year, it will be classified as Long Term Capital Gain.

- If your holding in an Equity mutual fund scheme is less than 1 year i.e. if you withdraw your mutual fund units before 1 year, after making a profit, then the profit will be considered as Short Term Capital Gain.

- The STCG (Short Term Capital Gains) tax rate on equity funds is 15%.

- The LTCG (Long Term Capital Gains) tax rate on equity funds is 10%.

Non-Equity Funds (Hybrid Funds)

- If you make a gain / profit on your investment in a Non-Equity Mutual Fund scheme that you have held for over 3 years, it will be classified as Long Term Capital Gain.

- If you make a gain / profit on your Debt fund (or other than equity oriented schemes) that you have held for less than 36 months (3 years), it will be treated as Short Term Capital Gain.

- The STCG tax rate on Non-Equity funds (or) Debt funds is as per the investor’s income tax slab rate.

- The LTCG tax rate on non-equity funds is 20% (with Indexation benefit).

- With effective from 1st April 2020, the dividend income received by investors from mutual funds(Equity or Debt funds) will be subject to TDS @ 10%. This TDS is applicable if such income is in excess of Rs 5,000 u/s 194K. Also, such dividend income is a taxable income in the hands of investor as per his/her income tax slab rate.

Related Article : Mutual Funds Taxation Rules FY 2023-24 (AY 2024-25) | Capital Gains Tax Rates Chart

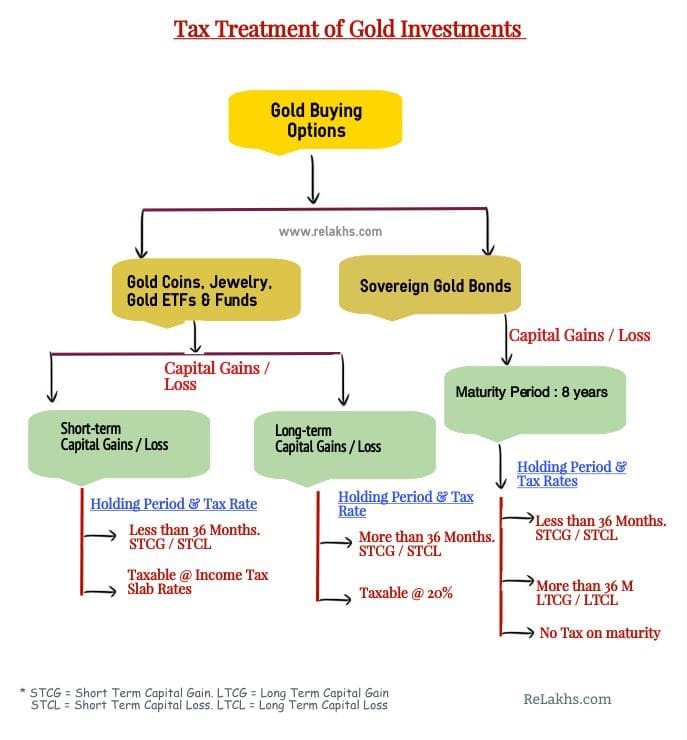

How are Gold Investments Taxed in FY 2023-24?

- Gold

- Gold ETFs or Gold Funds are treated as Non-Equity funds only .

- The tax implications on gains of selling Physical Gold are same as in the case of Non-Equity mutual funds. (Indexation benefit is available for Long Term capital Gains)

- TDS rate is not applicable on selling of Gold. However, buying jewellery over Rs 2 lakh in cash will attract 1% TDS.

- Sovereign Gold Bonds

- The interest payments on Gold Bonds shall be taxable as per your income tax slab rates.

- Gold bonds are exempted from capital gains (LTCG) tax at the time of maturity.

- However, kindly note that Long term capital gains arising to any person on transfer of SGB will continue to be taxable at 20% and eligible for indexation benefits.

- TDS is not applicable on the bonds. However, it is the responsibility of the bond holder to comply with the tax laws.

Tax Implications on investments in Real Estate Properties

- Real Estate

- If Land or house property is held for 24 months or less then that, such Asset is treated as Short Term Capital Asset. Short Term Capital Gains are included in your taxable income and taxed at applicable income tax slab rates.

- If Land or house property is held for more than 24 months then that Asset is treated as Long Term Capital Asset. Long Term Capital Gains on sale of property are taxed at 20% (with indexation).

- If you receive any rental income from the property then it has to be included in your income and taxed at income tax slab rate.

- If you are claiming HRA (House Rent Allowance) of more than Rs 50,000 per month (or) paying rent which is more than Rs 50,000 then the tenant has to deduct TDS @ 5%. The TDS could be deducted at the time of credit of rent for the last month of the tax year or last month of tenancy, as applicable.

- The buyer of the property needs to pay TDS @ 1%, on sale of property which is valued at Rs 50 Lakh or more.

- Effective 1 September 2019, the limit of Rs 50 lakhs would be towards consideration of the immovable property including all other charges incidental to the purchase of immovable property such as parking fee, society fee, club membership fee paid by the buyer.

- The Registrar of properties reports purchase & sale of all immovable properties exceeding Rs 30 Lakh to the Income Tax authorities.

- The monetary limit for quoting PAN for sale or purchase of immovable property has been raised to Rs.10 lakh from Rs.5 lakh. Properties valued by Stamp Valuation authority at amount exceeding Rs.10 lakh also need PAN.

- The Long Term capital Gains on sale of property can be saved by investing in specified investment avenues.

- REITs (Real Estate Investment Trusts)

- If units of REIT are held for 36 months or less than that, such Asset is treated as Short Term Capital Asset. Short Term Capital Gains are taxable at 15% without indexation benefit.

- If units of REIT are held for more than 36 months, such Asset is treated as Long Term Capital Asset. Long Term Capital Gains of more than Rs 1 lakh are taxable at 10%.

- The Interest and rental income from REIT units are taxed at the resident’s applicable tax slab rate.

How are investments in Bonds, NCDs, Fixed Deposits taxed in India?

- Fixed Income & Bonds

- Tax Free Bonds

- Interest received on TFBs is tax-free. TDS is not applicable.

- Short-term capital gains from sale of tax-free bonds on exchanges are taxed at your income tax slab rate.

- Long-term capital gains are taxed at 10% without indexation. The indexation benefit is not available for Bonds.

- For STCG holding period is less than 12 months. For LTCG holding period should be more than 12 months.

- Non-Convertible Debentures

- Effective from 01st April 2023, 10% TDS will be deducted on interest income of above Rs 5000, on listed NCD as well.

- Interest earned on NCD bonds is taxable as per the tax slab of the investor.

- If you sell NCDs on stock exchange before one year from the date of purchase, Short Term Capital Gains Tax is applicable. Tax rates depend on the tax slab you fall into.

- If you sell NCDs on stock exchange before maturity but after one year, Long Term Capital Gains Tax (if any) at 10% without indexation is applicable.

- Company Fixed Deposits

- TDS is not applicable on interest earned upto Rs 5,000 pa.

- You have to club the interest earned on these deposits as ‘income from other sources’ and file your annual Income Tax Returns.

- Fixed Deposits / Recurring Deposits

- The interest income earned on Fixed deposits/RDs is taxable.

- For Senior Citizens, the Interest income earned on Fixed Deposits & Recurring Deposits (Banks / Post office schemes) of upto Rs 50,000 is tax exempted. This deduction can be claimed under new Section 80TTB. However, no deductions under existing 80TTA can be claimed if 80TTB tax benefit is claimed.

- Section 80TTA of Income Tax Act offers deductions on interest income earned from savings bank deposit of up to Rs 10,000. From FY 2018-19, this benefit will not be available for late Income Tax filers.

- No TDS of up to Rs 40,000 on interest income from Bank / Post office deposits (the FY 2018-19 TDS threshold limit u/s 194A is Rs 10,000). Kindly note that no TDS does not mean no tax liability. Interest income on Deposits (FDs/RDs) is still a taxable income.

- Tax Free Bonds

If you are aware of the tax implications at various investment stages, you can pick tax-efficient investment options. Tax efficiency is a measure of how much an investment’s return is left over after taxes are paid. Tax efficiency is essential in order to maximize net returns on our investments.

Asset Allocation is a very important investment strategy. You should invest in suitable financial products or Asset Classes based on your financial goals. If an investment option meets your requirements and is also a tax efficient one then it is well and good. Your investment strategy is to max out your after-tax returns.

Continue reading:

- Income Tax Deductions List FY 2023-24 | Under Old & New Tax Regimes

- Latest TDS Rates AY 2024-25 | TDS Rate Table for FY 2023-24

(Post first published on : 07-October-2016) (Post last updated on 15-Aug-2023)

Join our channels

Hello Sreekanth

Suppose a person comes under 5% Tax Slab.

His income is around 5lpa.

Now if he sells his immovable property within 2 years , he will be liable for STCG.

The property was purchased at a price of 10 lac and he sold it at 14 lac making a STCG of 4 lac.

Now will this 4 lac will be added to his income (annual income 5 Lac ) making it 9 lac and then will he be liable to pay tax on 9 lac (that will come under 20%)

or

He will pay 5% on STCG of 4 lac and will pay his income tax as usually he pay i.e at 5% .

Dear Bharat,

The first scenario is correct (20%).

Dear Mr. Sreekanth,

I had a STCL of Rs. 5000/- during the financial 2015-16 and it has been c/f to FY 2016-17. Now I have a capital gain of Rs.3000/- during the current FY 2016-17. Since my income after taking into account the STCG of Rs.3000/- is below the taxable income (after considering the rebate under sec 80C, 80D etc., should I compulsarily adjust the STCG against the c/f STCL in this year or can I adjust the total loss of Rs.5000/- against my future year gains. Can you please clarify?

Thanks and regards

H. R. Krishnan

Hi Srikanta,

I want to invest around 12 to 14L in MF. Felling insecure to invest in MF because of risk factor. I am looking for a low risk funds, at least get an interest above 10% after 5 years. Please can you suggest best MF funds , so that I can invest my money. I have long terms target after 5 years or so. Please suggest three or four funds, I want to invest as a lump sum.

Dear Pradeep,

To get returns of around 10%, one may have to necessarily take risk.

Kindly read :

MFs are subject to risks – My view

List of investment options

Best Balanced funds

dear srikanth how bhavishya nirman bonds are taxed,in their prospects it said that they are zero coupon bond ,hence indexation benefit will be available.can you please clarify

regards

Dear Yashpal,

As there are no interest payments in zero coupon bonds, these bonds are taxed under the head income from capital gains. Long term capital gains attract indexation benefits, i.e, the tax rate is 20% with indexation and 10% without indexation.

In case of short term capital gains it will be included in the investor’s total income and tax rate will be as per the tax slab in which the investor falls.

dear sreekanth many thanks for your reply

warm regards

Dear Srikanth, please clarify the below:

My fixed deposit of 4 Lacs got matured. If I transfer this amount to my savings acct in another bank thru RTGS, Is this amount is taxable ? If so, how can I avoid getting taxed ? please advise.

Dear Suresh,

Kindly note that the interest income earned on Fixed deposit is taxable and the interest income earned on Saving account is taxable (if interest income on saving bank accounts is less than Rs 10,000 then it is tax exempt).

Read: FDs/RDs & tax implications.

Hi Shrikant

I am doing SIP in few debt funds from last 1 year. How much tax (%) will get deducted if i redeemed my SIP’s now. As I am in 10% tax bracket it is not a good idea to withdraw before 3 years as LTCG tax is 20% with indexation is more than 10 % ?

Dear Sanket,

The tax rate is as per your income tax slab rate.

Suggest you to go through detailed article on – MF Taxation rules. In case if you need more info, you my revert to me.

Thanks Sreekant for your comment.

I read MF Taxation rules article but I am still not sure what would be approx estimated tax I need to bare.

Lets simplify with an example.

Mr. A is in 10 % tax bracket & invested 10000 in Nov, 2015 in Debt fund like short term Gilt Fund. Now consider 2 situation :

1. Mr. A decided to withdraw that money in Nov2016 so those 10 k will become 11047 with 10 % retun for 1 year.

So STCG is 1047 which will be taxed with 10 % . So approx 104.7 Rs.

2. Mr. A stayed invested in same fund for 3 years so now 10 k becomes approx 13482 with 10 % return,

Now LTCG is 3482 which will be taxed as 20% with indexation benefit.

How much tax will get deducted for Mr. A in this case ?

Dear Sanket,

If purchase date is 1-Apr-2013 & Sale date is 1-Apr-2016 then calculation will be as follows;

Investment Type:Debt Mutual Funds

Time between :3 years 1 days

Gain Type: Long Term Capital Gain

Difference between sale and purchase price: Rs 3,482

CII (Cost Inflation Index) of the Purchase Year: 2013 month: Apr : 939

CII of the Sale Year: 2016 month: Apr : 1125

Purchase Indexed Cost: Rs 11980.83

Difference between sale and indexed purchase price: 1501.17 (Rs 13,482 – Rs 11,980)

Long Term Capital Gain Tax with indexation (at 20%):300.23

Superb Shreekanth,

For your valuable feedback now I understood MF jargon “Indexation Benefit”.

Thanks once again.

Happy Diwali !!!!!!!!!

Cheers……….

Thank you dear Sanket.. Happy Diwali 🙂

Keep visiting and do share the articles with your friends!

Hi Sreekanth,

I must agree that you have explained everything in detail, this is what I was looking for when I have started to search for assets & income tax implications.

I think, this is very useful information, which can help a person who wishes to learn about asset and income tax implications.

If any business person wants to make huge in the industry ten he should be aware of the numbers so that he can calculate and come up with a strategy.

Thank you dear Rajkumar ..Keep visiting!

Hi Sreekanth, When I am purchasing shares, I observed stamp duty also being charged. So can I get this benefit under Sec 80C.

Dear Sivaram,

Kindly note that the cost of acquisition of shares would include expenses incurred on purchase of shares like service tax, stamp duty, brokerage, etc., except STT. Similarly, consideration received on sale of shares should be after deduction of service tax, stamp duty, brokerage, etc., except STT.

So, one can claim it when calculating capital gains and not as tax deduction u/s 80c.

Hello Shreekanth,

Such exhaustive information under one article is really nice to see. Keep up the good work..

Thank you dear ASN. Keep visiting!

Hello Srikanth, wish you a very happy festive season! I’ve three questions-

1. While registering a property we pay stamp duty+registration fees. Later we pay mutation fees. I know stamp duty paid is tax exempted under 80c. Are registration fees + mutation fees paid also exempted from tax ?

2. I’ve purchased my first flat costing below 20 lakh by home loan, and don’t have any other property in my/spouse’s name. So I’m eligible for 50000 additional tax benefits under 80EE. Is this one time benefit or I can claim it every coming financial year?

3. Now if I book an under-construction flat / buy another ready flat in current financial year, will I be disqualified for the above benefits under 80EE? If I buy it in next FY?

Dear Das,

1 – Along with the Stamp duty charges, one can claim the Registration fee too under section 80c. Mutation charges – I dont think one can claim them.

2 – Section 80EE :

First time Home Buyers can claim an additional Tax deduction of up to Rs 50,000 on home loan interest payments u/s 80EE. The below criteria has to be met for claiming tax deduction under section 80EE.

The home loan should have been sanctioned in FY 2016-17.

Loan amount should be less than Rs 35 Lakh.

The value of the house should not be more than Rs 50 Lakh &

The home buyer should not have any other existing residential house in his name.

I believe that one can claim tax deduction under this section as long as you have outstanding loan amount.

3 – Good question. I believe you can keep claiming the tax deduction.

Nice post, Sreekanth!!! Quite exhaustive.

Just wanted to add a point about taxation of insurance plans (with investment benefits) i.e. ULIPs and traditional plans.

In case where Sum Assured is more than 10 times annual premium (policies issued on or after April 1, 2012), the maturity proceeds are not exempt from tax.

Term plans won’t be affected.

However, traditional plans and ULIPs may face problems, especially single premium plans.

Dear Deepesh,

Thanks for leaving your inputs.

I have visited your Blog and read some of your articles, they are very useful and unbiased. Great job! All the best!

Hi Sreekanth,

Thanks for the kind words.

I am regular visitor of your blog and have learnt a number of things from your blog posts.

Keep up the good work!!!

Are term insurance (online and offline) premiums are taxed? Because sum assured is much more than annual premium paid.

Dear Das,

Are you referring to tax benefits??

Service tax is levied on the Premiums.

Kindly note that there wont be any maturity proceeds on Basic Term insurance plans.

Surrender/Maturity proceeds of ULIPs whose Premium in any year is more than 10% of Sum Assured (this is 20% for Policies bought between Apr 2003 to Mar 2012) are taxable and do not come under EEE category. Generally Single Premium Policies come under this category.

Thanks for sharing this point.

Kindly note that I have intentionally tried to keep the taxation part of Life insurance policies simple.