We receive income through different ways, it can be your Salary, Dividend income from mutual funds or stocks, commission, rent, interest on your Bank Fixed Deposits / Securities etc.,

The providers of these incomes (like your company / bank) can deduct a certain percentage of income as TDS (Tax Deducted at source) based on certain threshold limits.

TDS or tax deducted at source is a process of collecting Income Tax at source by the GOI (Government of India). It is a deduction of tax from the original source of income. It is essentially an indirect method of collecting tax which combines the concepts of “pay as you earn” and “collect as it is being earned.”

TDS is calculated and levied on the basis of a threshold limit, which is the maximum level of income after which TDS will be deducted from your future income/payments.

TDS is deducted as per the Indian Income Tax Act, 1961. TDS is controlled by the Central Board for Direct Taxes and it is a part of the Indian Revenue Service Department.

Let us understand about TDS with an example;

You book a Bank Fixed Deposit for Rs 5 Lakh for 1 year @ 10% pa interest rate. You will earn an interest income of Rs 50,000 after one year. Your Bank may deduct TDS at the rate of 10% i.e., Rs 5,000 (10% of Rs 50,000) and deposits this Rs 5,000 with Income Tax Department (on behalf of you). Bank issues you a TDS certificate (Form 16A) which reflects this deduction. (Read : ‘Understanding your Form 16A‘)

Besides interest income earned on bank deposits, TDS is levied on various incomes & expenditures. Salary income, lotteries, interest income from post office, insurance commission, rent payment, early EPF withdrawals, sale of immovable property, rent payments on property etc., fall under the ambit of TDS.

Latest Article: Latest TDS Rates Tax Year 2026-27 (AY 2027-28) – Complete Chart

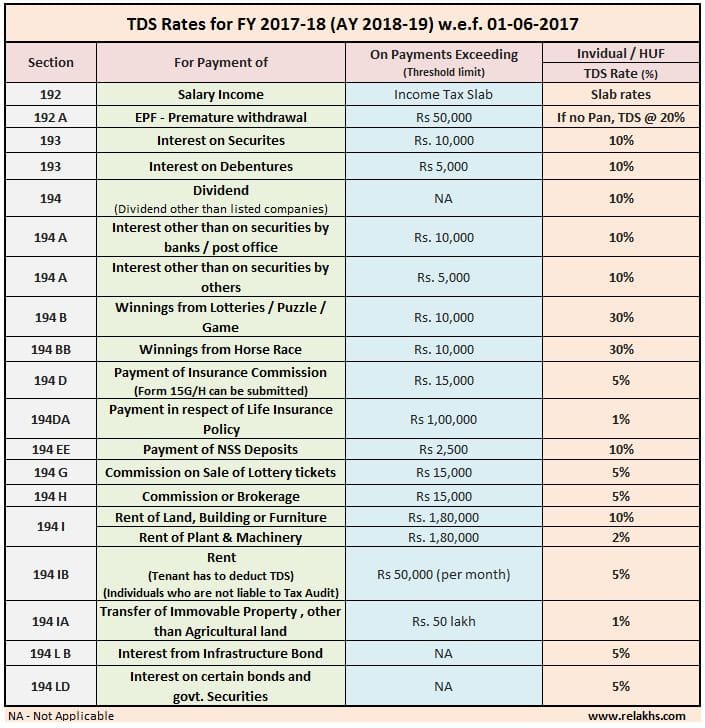

Latest TDS Rates Chart for Financial Year 2017-18 (Assessment Year 2018-19)

Based on the Financial Act 2017-18, following are the revised TDS threshold limits & rates of TDS applicable for the FY 2017-18 (AY 2018-19).

You may also need to be aware of the below important points ;

- TCS (Tax Collected at Source) is applicable on purchase of Motor vehicle worth more than Rs 10 Lakh. (Section 206 C – IF)

- 1% TCS on cash purchases of above Rs 2 Lakh has been removed. However, 100% penalty is now applicable on Cash transactions (including jewelry purchases) exceeding Rs 2 lakh (Related Article : ‘Cash Transaction Limit – Penalty Details & Examples‘)

(Difference between TDS & TCS : TDS = Tax Deducted at Source i.e. deducted by PAYER or BUYER. e.g. Employer making salary payment or buyer of immovable property or person paying interest or commission or rent would deduct TDS and pay to the IT department. TCS = Tax Collected at Source i.e. collected by RECEIVER or PAYEE or SELLER. e.g. A Car Dealer selling motor car can collect TCS and pay to the IT department.)

Misconceptions on Tax Deducted at Source (TDS)

One of the biggest misconceptions that exist in the mind of many honest taxpayers is that since they receive their salary/ other payment after deduction of Tax at Source (TDS) and thus they are not required to file their Income Tax return (ITR), assuming that their tax liability has been discharged. Following are some of the common misconceptions on TDS;

- No TDS means no Tax liability

There is a common misconception / myth that if there is no TDS then the schemes (or) investments are tax-free.

For example – If an employee withdraws his EPF money before 5 years of service and if the withdrawal amount is less than Rs 50,000 then TDS is not applicable.

But, this does not mean that the withdrawal is Tax-free. It is just that there is no need for an employer/EPFO (Deductor) to deduct TDS on these types of withdrawals. However, the onus of paying taxes (if any) on this EPF amount lies with the employee.

So, whether it is EPF withdrawals within 5 years or National Savings Certificates (5 year tenure) or any other investments, the interest income is taxed until and unless it is specifically mentioned that the income from that scheme is tax free. For example PPF enjoys tax benefit for which its interest is non-taxable. (Related Article : ‘Tax treatment of various financial investments‘)

- TDS deduction removes tax liability completely

- It’s a misconception that, if the employer has deducted TDS, you need not worry about filing your income-tax return. Your employer deducts TDS on your salary income only, whereas you may have income from other sources (like interest income from Bank Deposits, rental income etc.,) and you have to include those in your Tax Returns. (Related Article : ‘TDS deducted by Employer but not Deposited? How to check TDS details online?‘)

- Another misconceptions is – ‘No additional Income Tax is payable, if taxes are already deducted (TDS) on income’. Actually, depending on nature of income, TDS rates vary. On salaries, employers adjust the rate such that the entire tax liability of the employee is deducted by the year-end. On fixed deposit interest, banks charge TDS at 10%. But if the deposit holder does not provide his PAN, banks deduct tax at 20 per cent.

If your income tax slab rate is different to that of the TDS rate then you may have to pay the ‘balance tax’ or in some cases you can claim ‘refund’ too. It is advisable to be aware of TDS rates on various incomes that you have.

The TDS rate can be say 10% , whereas your are in the 20% tax slab, in this case you have to pay the differential tax (this can be Advance Tax or Self-Assessment Tax). If you are not a tax assessee then you can claim the TDS amount as refund by filing your Tax Returns. If you are in 10% tax bracket and the TDS rate is also 10% then there is no need to pay any additional tax.

Most of the Senior Citizens submit Form 15H to avoid TDS. In many cases, senior citizens feel if they have done this, they are not liable to pay tax. But if you have two or three fixed deposits in separate banks and you submit a Form 15G or 15H in all the banks, you will have to pay tax if the total interest from all the fixed deposits exceeds the taxable income limit.

Like most of us, the Government doesn’t like to wait for its money. It wants us to pay tax dues or at least a portion of it as and when we get our incomes. So, make sure you meet the compliance requirements which are related to TDS. Kindly note that false declarations for TDS avoidance can result in penalties and interest charges. So, kindly avoid doing it!

Continue Reading :

- When to submit Form 15G & Form 15H (Clarifications based on CBDT’s latest notification)

- Why is it advisable not to invest in FDs/RDs for longer period?

- High Value transactions that are tracked by the Income Tax dept

- Different Asset classes have different Tax implications – How Returns are taxed?

(Post published on : 21-July-2017)

Join our channels

Hi Sreekanth

Ideally i want to ask this under section ‘How to reply to Non-Filing of Income Tax Return Notice?’. But could’t find a comment option there.

So asking it here.

My Father is an NRI workinjg in UAE for the last 35 years.

Recently my father received a letter from Income Tax for ‘Non Filing of lncome Tax Return’

Below is the letter

Subject: Non Filing of lncome Tax Return

1.The lncome Tax Department has received information on financial transactions/activities relating to you.

A list of some of the information for Financia-Year 2014-15 is provided below.

As per records, you do not appear to have filed lncome Tax Returns for Assessment year(s) 2015-16.

2.You are requested to furnish your response in the Compliance Module on the e-filing portal at https://incometaxindiaefiling.gov.in

lf you are not registered with e-filing portal, use the ‘Register Yourself’ link to register.

The response to this letter has to be submitted electronically by clicking on the ‘Compliance’ link after logging into the e-filing portal.

You may keep a printout of the acknowledgement of submitted response for your own record.

3.A copy of the acknowledgement is required to be submitted to the office of the undersigned within 20 days

of receipt of this letter failing which appropriate proceedings under lncome Tax Act,1961 may be initiated.

lnformation Summary for PAN XXXXXXXXXXXX

———————————————–

2014-15 CIB-403 Time Deposit exceeding 2,00,000 with a banking company

2014-15 TDS-195 TDS Return – Payment to Non-residents (Section 195)

When i checked Form26AS for AY2015-16 i could see some entires under ‘PART A – Details of Tax Deducted at Source’

But this total amounts to only Rs 45/- as shown in Form 26AS.

Please let me know what should be done in this case.

Why we received this letter from Income tax this month.ie Dec 2017, ..even if its for FY14-15.

Please help me how to respond to this notice.

Dear Vishnu,

They have indicated two reasons, ie deposit of Rs 2 Lakh in FD and TDS u/s 195 – which is TDS deducted at the time of making the payment to the NRI. The information about the TDS deducted and rate should be mentioned in the sale deed between the NRI seller and the buyer.

Suggest you to kindly consult a Chartered Accountant in this regard.

Thanks Sree

But i wonder why TDS was deducted as he deposits the money in NRE account which is not taxable.

Dear Vishnu,

Yes, need to go through the documents/statements.

Kindly consult a CA in person at the earliest!

194 J for Professional services is not present ?

Dear Umasankar,

You may find more details on Sec 194j..here..

Dear Sir,

we are builders hiring jcb and diesel generators in our project sites. what will be the tds rates and limits on hire charges?

Dear Surya..Suggest you to kindly consult a CA.

Hi Sree

Is this threshold limit separate for FD’s,RD’s and Savings account…i.e for FD’s there is a threshold limit of 10000 ,

for RD’s there is a separate threshold limit of 10000 and for savings there is another threshold limit of 10000.

Or is it combined, ie. the threshold limit is only 10000 for FD’s RD’s Savings together.

Dear Vishnu,

Deduction from gross total income of an individual or HUF, up to a maximum of Rs. 10,000/-, in respect of interest on deposits in savings account with a bank, co-operative society or post office can be claimed under this section.

Section 80TTA deduction is not available on interest income from fixed deposits.

Banks do not deduct TDS if the Interest income earned on Fixed Deposits/RDs is less than Rs 10,000 per year. That does not mean this is a tax-free income in your hands. You still need to add this as ‘income from other source’ when you file your Income Tax Returns. (If the interest exceeds Rs 10,000 in a financial year, the bank will deduct 10 per cent tax before crediting the interest to the account.)

Kindly read : RDs/FDs – tax implications..

Hi Sree

Thanks for your reply and i have read the article you suggested.But i have still one doubt.

Suppose i work in a private company in India and my salary falls in the 10% tax bracket.

My father is an NRI, sometimes he used to deposit money as fixed deposit in my account.

Some of his money may lie in my savings account also.

My, question is

1. Is this deposit amount added to my gross income.Suppose my annual total salary income is 8 Lakh and if my father deposits his 3 Lakh in my account,

does my annual gross income becomes 11 Lakhs and i fall in 30% tax bracket ?

2. Do i need to pay tax on interest earned on these amount (FD’s and savings).

3.Since he’s an NRI is there any change in taxation rules.

If the interest is taxable is there any way/any form which can be submitted to bank so that this income is not considered as my income.

Dear Vishnu,

You may treat the income deposited in your account as either GIFT or loan.

If gift, then it is tax-free and you can disclose the amount under ‘Exempt income’ section of your income tax return.

Kindly read : Gifts & Income tax implications.

2 – Interest income on FDs is a taxable income and need to be disclosed under ‘income from other sources’ head.

3 – Then he needs to deposit in his NRE account. For an NRI, interest earned on NRE deposits is exempt from tax in India. So long as you continue to be an NRI or a resident but not ordinarily resident – the tax exemption will continue to apply for these deposits held by NRI.

Dear Sreekanth,

I have received an intimation U/S 143(1) on 9th September 2017 saying that Ihaven’t paid 234B interest of Rs 475/- and 234C interest of Rs 531/-. Total due of tax Rs 1010/-. I paid self assessment tax of Rs 5942/- after deducting the relief U/S 89 of Rs 4633/-, in addition to TDS. This is due to the FD interest. Kindly advice how to deal this intimation. Whether I have to pay this amount. If I paid, whether I have to file the return again.

Thanks and Regars

Raveendran

Dear Raveendran,

Kindly note that Interest under section 234B of Income Tax Act is levied upon those taxpayers who default in payment of Advance Tax.

If you have to pay Rs 10,000 or more in taxes in a financial year, advance tax may be applicable to you.

If you have to pay Rs 10,000 or more in taxes in a financial year, advance tax may be applicable to you.

You may have to pay the tax dues…kindly check the compliance link in your account of e-Filing portal, respond to it.

There is no need to file ITR.

Sir,

I have purchased a flat of 42 Lakh for which I have taken a loan of 30 Lakh. I have taken 6 Lakh from my sister via NEFT.

1. Do I need any sort of agreement (GIFT agreement) so that no problem arise in future for this transaction ?.

2. Do I need to disclose this income in ITR ?

3. Will I need to pay any tax for it ?

Dear Ashu,

Have you taken this as loan? (or) did she gift you?

Sir,

She has gifted me .

Dear Ashu,

1 – Getting a Gift Deed is advisable but it is not mandatory though.. also as the transfer has been done through NEFT, your bank statement reflecting this transaction can be considered as a documentary evidence (if required).

2 – You can disclose this amount under ‘Exempt income’ section of your ITR.

3 – It is tax exempt.

Kindly read : Gifts & Tax implications..

Sir,

First of fall thanks for your precious time and advice. I have few more queries:

I am a salaried professional with total salary of around 6 lakhs. For this financial year I had already received a gift of 6 Lakh . Now my other family members are planning to gift me 8 lakh. So this will be my roughly income for the year :

1. 6 lakh from salary

2. 14 lakh from gift

Here are my queries :

1. So do I need to fill ITR-1 only or some other ITR ?

2. As there is no occasion like Birthday, Marriage etc so it will be safe to receive such a huge amount of 14 lakh as gift ?

Dear Ashu,

1 – Which ITR form ? This can be based on the new ITR forms for FY 2017-18 (which will be released in Mar/Apr 2018 only).

For reference you may go through this article – Which ITR form to file?

2 – As long as the gifts are from defined family members, its ok, they are tax-exempt.

Okay, Thank you sir.

yes according to income tax u have to pay

Hello sreekanth,

I am 26 years old, working in a IT service company. I am receiving salaried income. I used to invest in my company shares for about 2 years. The shares are bought by my company every month from my salary.

Last month I sold all the shares I was holding. some of them will be short term and some will be long term.

How do I declare my capital gains in IT returns? what form should I submit? and how to pay capital gains tax?

kindly advise.

Dear Muthu,

You may have to file ITR 2 form.

If you have held the shares for more than 1 year then it is Long term capital gains, and is tax-exempted.

<12 months , then gains on redemption are treated as STCG, which are chargeable to tax @ 15%.

Kindly read : Which ITR form to file?

Dear Sreekanth,

very nicely explained. Will Recurring Deposits maturity proceedings will be done TDS? if yes, how much TDS? RD of 2000/pm for 5 years for example with interest rate of 8%.

regards

RAJ

Dear Raj,

Suggest you to kindly go through this article…

Thank you Sreekanth for your kind reply

I read that article. one small doubt. Is it mandatory for bank to do TDS for RDs?. they never did that in my case, but i have always included the interest income in my income tax calculations. May be interest is small amount ( around 10 K for 5 years) i felt.

regards

RAJ

Dear Raj,

The budget 2015-2016 has put RDs at par with FDs for TDS purpose. Banks are deducting Tax Deducted at Source (TDS) on Recurring Deposits too, from 1st June, 2015.

Yes, may be your interest income is below Rs 10k..