The Tax Deducted at Source (TDS) mechanism ensures that tax is collected by the government at the time income is generated rather than later when returns are filed.

Under this system, the payer deducts tax before making certain payments such as salary, interest, rent, professional fees, commission, etc., and deposits it with the Income Tax Department.

In this post, let us look at the latest TDS rate chart for Tax Year 2026-27 (earlier referred to as FY 2026-27 / AY 2027-28) along with threshold limits and important sections.

Budget 2026 Highlight: From April 2026, the Income Tax Act introduces the concept of “Tax Year”, replacing the traditional Financial Year (FY) and Assessment Year (AY) terminology to simplify the tax framework.

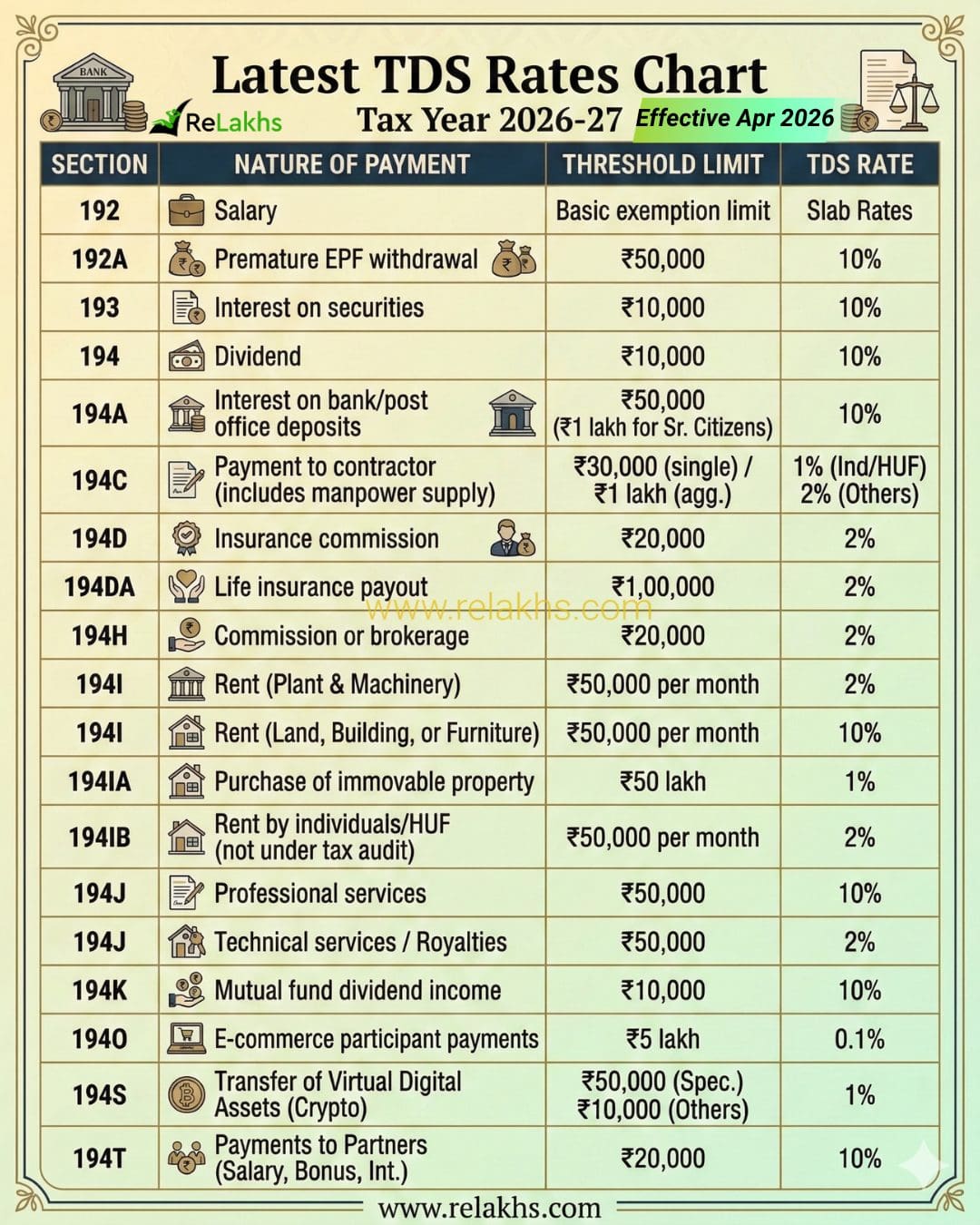

Latest TDS Rate Chart for Tax Year 2026-27

The latest TDS rates for Tax Year 2026-27 (as per Budget 2026) specify the tax deducted at source on various payments such as salary, interest, rent, commission, professional fees, property purchase, and e-commerce transactions. The applicable TDS rate generally ranges from 0.1% to 10%, depending on the nature of the payment and the threshold limit prescribed under different sections of the Income Tax Act. The updated TDS rate chart below summarizes the section-wise rates, threshold limits, and key compliance changes applicable from April 2026.

| Section | Nature of Payment | Threshold Limit | TDS Rate |

| 192 | Salary | Basic exemption limit | Slab Rates |

| 192A | Premature EPF withdrawal | ₹50,000 | 10% |

| 193 | Interest on securities | ₹10,000 | 10% |

| 194 | Dividend | ₹10,000 | 10% |

| 194A | Interest on bank/post office deposits | ₹50,000 (₹1 lakh for Sr. Citizens) | 10% |

| 194C | Payment to contractor (includes manpower supply) | ₹30,000 (single) / ₹1 lakh (agg.) | 1% (Ind/HUF) / 2% (Others) |

| 194D | Insurance commission | ₹20,000 | 2% |

| 194DA | Life insurance payout | ₹1,00,000 | 2% |

| 194H | Commission or brokerage | ₹20,000 | 2% |

| 194I | Rent (Plant & Machinery) | ₹50,000 per month | 2% |

| 194I | Rent (Land, Building, or Furniture) | ₹50,000 per month | 10% |

| 194IA | Purchase of immovable property | ₹50 lakh | 1% |

| 194IB | Rent by individuals/HUF (not under tax audit) | ₹50,000 per month | 2% |

| 194J | Professional services | ₹50,000 | 10% |

| 194J | Technical services / Royalties | ₹50,000 | 2% |

| 194K | Mutual fund dividend income | ₹10,000 | 10% |

| 194O | E-commerce participant payments | ₹5 lakh | 0.1% |

| 194S | Transfer of Virtual Digital Assets (Crypto) | ₹50,000 (Spec.) / ₹10,000 (Others) | 1% |

| 194T | Payments to Partners (Salary, Bonus, Interest) | ₹20,000 | 10% |

NRI TDS Rate Chart: Tax Year 2026–27 (AY 2027–28)

Unlike residents, NRIs usually face TDS from the first rupee of income (no basic exemption limit for TDS) under Section 195, unless a Lower Deduction Certificate is obtained.

| Nature of Income | TDS Rate (Base) | Remarks |

| Dividends (Equity/MFs) | 20% | No threshold; applies to first rupee. |

| Interest on NRO Deposits | 30% | Effective rate is 31.2% (incl. 4% cess). |

| Interest on NRE/FCNR | NIL | Tax-exempt for NRIs. |

| LTCG: Residential Property | 12.5% | For assets held > 24 months. |

| STCG: Residential Property | Slab Rates | Taxed at the NRI’s applicable income slab. |

| LTCG: Listed Equity/Units | 12.5% | Under Sec 112A; exempt up to ₹1.25 lakh. |

| STCG: Listed Equity/Units | 20% | Under Section 111A. |

| Rental Income | 30% | No basic threshold; deducted by the tenant. |

| Royalties / Technical Fees | 20% | Reduced rate compared to “other” income. |

| Online Gaming Winnings | 30% | Deducted on net winnings. |

Example: How TDS Works

Suppose you earn ₹80,000 interest from a bank FD in a year.

- Threshold limit = ₹50,000

- TDS rate = 10%

Bank will deduct:

₹80,000 × 10% = ₹8,000 TDS

This amount will appear in your Form 26AS / AIS and can be adjusted when filing your income tax return.

Key Changes Related to TDS for Tax Year 2026–27

- No TAN Required for NRI Property Purchases: Starting October 1, 2026, individual buyers purchasing property from NRIs no longer need to apply for a TAN. You can now deduct TDS and deposit it using a simple PAN-based challan, similar to resident property purchases. This removes a massive compliance hurdle for one-time home buyers.

- One-Time Form 15G / 15H via Depositories: Investors with demat accounts no longer need to submit declarations to every individual company. You can now submit Form 15G or 15H once to your depository (NSDL/CDSL), and they will automatically share it with all companies where you hold shares to prevent TDS on dividends.

- Section 194C Expansion: As per the 2026 Budget, the definition of “work” under Section 194C now explicitly includes the supply of manpower, ensuring these payments are taxed at the lower contractor rates (1% or 2%).

- Section 194T Implementation: A critical check for Partnership Firms. Any salary, bonus, interest, or commission paid to a partner exceeding ₹20,000 annually requires a 10% TDS deduction.

- Threshold Rationalization: Most thresholds (like 194H and 194J) have been rounded up to ₹20,000 or ₹50,000 to simplify the math and reduce small-ticket compliance.

- PAN Requirement: If the payee does not provide a PAN, the TDS rate remains at a flat 20% (or the applicable rate, whichever is higher), except for sections 194O and 194Q where it’s 5%.

- Automated Nil / Lower TDS Certificates: Following Budget 2026, the process for obtaining certificates under Section 197 has been overhauled. Applications are now processed via a rule-based automated system using AIS/TIS data, drastically reducing manual officer approval and speeding up liquidity for taxpayers. (AIS: Annual Information Statement & TIS: Taxpayer Information Summary)

TDS is Income Tax? Misconceptions on Tax Deducted at Source (TDS)

One of the biggest misconceptions that exist in the mind of many honest taxpayers is that since they receive their salary/ other payment after deduction of Tax at Source (TDS) and thus they are not required to file their Income Tax return (ITR), assuming that their tax liability has been discharged. Following are some of the common misconceptions on TDS;

1. No TDS ≠ Tax-Free Income

Just because a bank, employer, or the EPFO doesn’t deduct tax at source doesn’t mean the income is exempt from tax.

- The Reality: TDS is simply a collection mechanism for the government. Whether it’s an EPF withdrawal under ₹50,000 or interest from a National Savings Certificate (NSC), the “onus” remains on you.

- The Rule: Unless a scheme is specifically labeled “Tax-Free” (like PPF interest), you must declare that income in your tax return and pay the applicable tax based on your total income slab.

2. TDS is a “Down Payment,” Not Full Settlement

A very common myth is that once TDS is deducted, your tax job is done. In reality, TDS is often just a flat-rate advance payment that may not cover your entire liability.

- The Reality: TDS rates (like the 10% on Fixed Deposits) are often lower than your actual tax slab (which could be 20% or 30%). You are responsible for paying the “differential tax” as Advance Tax or Self-Assessment Tax.

- The Catch: This applies to Senior Citizens too—submitting Form 15H only stops the deduction at the bank; it doesn’t magically wipe away the tax liability if your total interest across all banks exceeds the taxable limit.

The idea behind TDS is simple — the government collects a part of the tax when income is paid, instead of waiting until the year ends. So it is important to understand and comply with the TDS rules. Avoid submitting incorrect declarations just to escape TDS, as this can lead to penalties and interest later.

Continue reading:

- How to Avoid TDS in FY 2026-27 Using Form 121 (Replaces Form 15G & 15H)

- Income Tax Deductions FY 2026-27: Complete Guide to Old vs New Tax Regime

(Post first published on : 05-Marcjh-2026)

Join our channels