Only Wealthy and rich people need a financial plan! Is this true? What about the individuals and families who have very low income & who struggle to meet their ends? Do they require help and assistance in planning and managing their finances?

These low-income households can be some of your helpers like – your domestic maids, drivers, care-takers, cook and so on…

In India, we have the luxury of maids who can clean and cook at home, drivers who can take us to our work. They are an essential part of our work and home routines. We often realize it on the days when they take an off and our schedules can go for a toss.

If you have sufficient financial resources, it’s not that difficult to create a financial plan. You can plan well and lead a good life.

But, it is very tough for low income households like your domestic helpers, with limited financial resources, to plan well and lead a good life.

These are the people who help us continuously with no paid or sick leaves, no provident fund, no job security. Is it possible for us to assist them become ‘financially secure’, atleast to a certain extent? How to make a big difference in their financial lives?

Let me talk about a real-life incident happened during the last year..

From 2010-2014, I had offered Financial Planning and Real estate services in Bangalore. During that time I had employed one person to assist me in providing property-related services. More than an employee, we became good friends. He was a very hard-working and sincere person. We were involved in few real-estate deals in Bangalore. It is very rare to find a person like him especially in real estate industry.

He studied till 9th standard and he is from a very very poor family background. He has no other source of income except for ‘brokerage / commission’. His wife, two kids and parents are his dependents. I had advised him a couple of times to take term insurance and also a health insurance plan for self and for his family members. He was planning to take a health insurance plan, but God had other plans. He died due to DENGUE fever and kidney failure. They couldn’t afford to pay for medical treatment in a private hospital. (Unfortunately, I came to know about this event after everything was over, as I have relocated to Andhra Pradesh.)

The main reason for sharing this incident now is, it is very tough to convince and educate the domestic help & low-income households about the importance of insurance and the whole idea of ‘saving something now for a better tomorrow’.

I am sure, most of you might be dependent on domestic help in one or the other ways. If you decide to assist them in managing their finances, the toughest part would be to convince and educate them. It can be a challenging task, but definitely not an impossible one! Identifying right financial products based on their affordability is relatively easier!

Ways to make your domestic help secure their future

You may kindly note below suggestions before you make a financial or investment plan for your domestic help or friends who belong to low-income group ;

- Kindly try to understand their family’s position and know about their other family members. Your domestic maid might be willing to save, but his/her spouse might be spending lot of money for drinking/smoking. So, you may need to know the root-cause for their financial issues/misery.

- Do know if they have any Debts (especially about high-cost loans). Most of the domestic workers are never debt-free. As they do not save or unable to save, they keep on taking loans to meet unforeseen expenses. The moment one cycle of repayment ends, another begins. The loans can be to pay their children’s school fees or to clear their medical bills or even to make essential purchases. I have observed that high medical costs / unaffordable healthcare is one of the primary reasons for the perennial cycle of debt most hired help fall victim to.

- As they have a very low-disposable income, you have to be very careful in identifying right financial products which are affordable as per their requirements/priorities.

- Your domestic help might be willing to save but most of the times they do not have idea about the available investment options. In most of the scenarios, you need to change their perceptions, misconceptions and apprehensions about the organized financial system. For example : Our domestic helper and driver invests almost 90% of his savings in local Chit Funds, as he trusts them blindly. Last year, I had suggested him not to invest heavily in one financial product, especially in chit funds which are not registered. I educated him about the pros & cons of chit funds.

- You may have to help them in getting valid Identity Documents (IDs) done.

- Be it for the Rich or Poor, the basic blocks of Financial planning remain the same.

Let’s now discuss on simple suggestions that you can give to your domestic help. Make sure that they implement your suggestions!

- Insist them to open a Savings Bank Account : Thanks to the Govt’s push for financial inclusion, most of the families have now own at least one bank account, to get govt subsidies (like LPG and other benefits). In case, your domestic maid or helper do not have a bank account then encourage and assist them to get one. Educate them on how to use a Debit card, benefits of having a bank account, cheque book etc., You may suggest them to have a basic savings account like Jan Dhan Account.

- They can get RuPay Debit card.

- Rs 1 Lakh as Accidental Insurance cover at no extra cost is available.

- A Life insurance cover of Rs 30,000 is provided.

- Overdraft facility of upto Rs.5000/- will be available to one account holder of PMJDY per household after 6 months of satisfactory conduct of the account.

- They can have access to other Insurance & pension Schemes (low-cost schemes offered by the Govt).

- (Kindly read related article : ‘PMJDY & Life Insurance Coverage‘)

- Encourage them to open a Recurring Deposit : You can suggest them to save a certain amount of money every month in a RD, linked to their bank account. You can let them know that they can cancel the RD at any time and withdraw funds for any emergencies. If you have been giving an annual bonus or any gifts to them during festivals, you may advice them to deposit this money in FD/RD.

- Get them a Life Insurance cover : If your domestic help is a sole-bread winner of his/her family, make sure you insist him to get a life cover.

- Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) is a low cost life insurance cover launched by the Govt of India.

- This life insurance plan is available to people (all citizens) in the age group of 18 to 50 years and having a bank account. You can suggest your domestic help to buy this plan and link it to his/her savings account.

- A sum of Rs 2 Lakh is provided as a life cover for a premium of Rs 330 per annum. The sum assured is payable in case of death for any reason (natural or accidental death).

- Make sure that a proper nomination is provided for the policy. You may have to follow-up every year to know if the premium has been paid or not. (Related Article : ‘PMJJBY – Scheme details & benefits‘)

- Based on the affordability, you may identify other low-cost term insurance plans offered by other life insurance companies.

- Suggest a Personal Accident Cover : As your domestic worker is highly dependent on daily or monthly wages, any physical disability if happens, may lead to loss of job/earning, permanently or temporarily. So, getting them a stand-alone PA cover is a must.

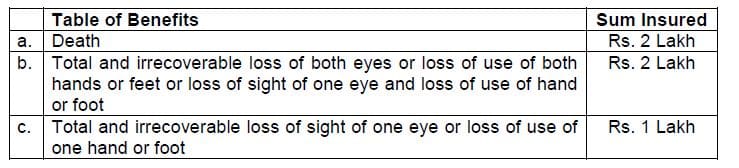

- You may also suggest Pradhan Mantri Suraksha Bima Yojana (PMSBY). A premium of Rs 12 pa has to be paid for accidental death and full disability – the coverage amount is Rs.2 Lakh and for partial disability the risk coverage is Rs.1 Lakh.

- You can get this policy linked to their bank account. Make sure to submit the nomination form.

- If you are advising your driver, you may suggest a stand-alone PA cover with higher sum assured and can get this from general insurance companies. Kindly make sure he/she has a valid driving license. (Related Article :’How to claim Insurance Benefits under PMJJBY & PMSBY?‘)

- You may also suggest Pradhan Mantri Suraksha Bima Yojana (PMSBY). A premium of Rs 12 pa has to be paid for accidental death and full disability – the coverage amount is Rs.2 Lakh and for partial disability the risk coverage is Rs.1 Lakh.

- Suggest a Health Insurance Cover : Health insurance could be a way of removing financing barriers and improving access to health care. Identifying an affordable health insurance plan can be a bit tough task, as the premium rates on regular mediclaim or family floater plans are high.

- I believe that each State Govt offers their own low-cost health insurance cover for BPL (Below Poverty Line) families (or) Low income groups. You may do a little research on this and identify if any suitable health insurance cover is available for your domestic help. For example : The current AP Govt offers YSR ArogyaSree Scheme. It provides financial protection for individuals who are below the poverty line in the state.

- If your hired help or any of their family members are a physically/mentally challenged, you can suggest ‘Swavlamban’ health insurance cover offered by The New India Assurane Co. This plan provides health cover of Rs 2 Lakh on family floater basis (1+3, primary insured is person with disabilities) at a premium rate of Rs 357 pa.

- You can go through another useful product called Janata mediclaim policy.

- You can suggest them about Jan Aushadhi scheme. Kindly go through this related article – ‘Jan Aushadhi Scheme – Govt’s low cost & affordable Generic drugs‘.

- Suggest a Pension Plan : This can be a tough product to explain to your domestic worker! Nevertheless, highlight the importance and benefits of subscribing to a pension plan to them.

- You may suggest Atal Pension Yojana. Under the APY scheme, a guaranteed minimum pension of Rs. 1,000, Rs 2,000, Rs 3,000, Rs 4,000 and Rs 5,000 per month will be given at the age of 60 years depending on the contributions made by the subscribers.

- The age of the subscriber should be between 18 – 40 years.

- A 30 year old individual has to contribute Rs 577 per month, to get Rs 5,000 per month pension amount. He/she has to make the contributions for 30 years (60 years minus 30 years age).

- In case of death of subscriber, pension would be available to the spouse and on the death of both of them (subscriber and spouse), the pension corpus (as indicated in the above table) would be returned to his / her nominee. (Kindly read : ‘Atal Pension Yojana – Details, Features & Beneftis‘ (or) Pradhan Mantri Shram Yogi MaanDhan – PMSYM)

Above suggestions are simple and easy ways to empower your domestic help financially. In case, they can afford to take some risk and based on their financial positions, you may suggest below financial products for corpus accumulation. But, do let them understand the pros & cons of these investment options ;

- Sukanya Samriddhi Deposit Scheme for Girl Child

- NPS Lite

- Public Provident Fund

- Mutual Funds etc.,

If your domestic worker or any of their family members are looking for Education Scholarships, you may help them to know if they are eligible for any Govt scholarship(s) by visiting portals like National Scholarship portal (or) VidyaLakshmi Portal.

Our Domestic Helpers & Here’s How we are assisting them to manage their Finances

We have a domestic driver and maid at home. Though they are our helpers, we have always treated them as our family members. In fact, my son affectionately calls our driver as MAMA (uncle)! Below is the pic of my son playing happily with his MAMA!

I have explained to our driver about the importance of having a term insurance cover, personal accident & health insurance (Family Floater) covers and made him to buy all these three plans. Over the last couple of years, he has started investing/saving in FDs, RDs & Mutual Funds. Also, going to be a proud owner of a small independent house!

We also have a female domestic maid. She has very high will power. Though her husband is a drunkard, she has been able to save money at regular intervals and got her younger son well-educated. I have recently referred him to one of the IT companies and he is now working with an IT company in Bangalore, very talented guy! He has created his own Financial plan now.

For the last two years, whenever I need to get my hair-cut, have been visiting a saloon (in my home-town) and became very close to an employee (barber) of the hair-saloon. I like his hard-working nature and very sincere in his work. He has two very young kids and has no idea about how to save and plan his investments.

I have made him to open a bank account, subscribe for PMJJBY, PMSBY and open a monthly RD. We are planning to submit an application for business loan under PM Mudra Yojana now, as he wants to open his own hair-saloon shop!

Your domestic workers may not remain employed with you forever, but make sure they know the importance of saving consistently, paying premiums of their insurance policies, continuing their contributions to any investment or pension plan etc., Also, encourage them to send their children to schools and get them well-educated.

“If your domestic helpers are happy, you will be double happy. Happy Helper = Happy Home!”

You may go through below articles, which can be useful to identify suitable investment options ;

- List of Best Investment Options

- Lump sum investment options for Senior Citizens| Regular Income Investment options

- Basics of Financial Planning (PPT)

This post is for information purpose only and is not ‘for or against’ any political party. I have given the details of the Govt Schemes based on their merits. Hope you find this article useful and informative. Request you to kindly share your views and comments!

(Image courtesy of digitalart at FreeDigitalPhotos.net) (Post published on : 25-October-2017)

Join our channels

I was looking for insurance and a home loan for my maid and this was immensely helpful, thank you so much!

Dear Priya.. Glad to know you find this information useful. Keep visiting ReLakhs.com!

My maid has taken a loan at 120 percent per year…is there any scheme where she can take that Fromm banks…she needs 50000

Dear Arun,

What is the purpose of Loan?

She can try PM Mudra Yojana.

Also, most of the State Govts have been implementing loan schemes for the BPL families, small-time traders, self-help groups, Anganvadi groups etc., Kindly check if she can get some finance there??

This is such an informative article, heartwarming too.

Thank you for spreading knowledge. May God bless you!

Thank you dear Mumtaz for your kind and encouraging words!

Keep visiting ReLakhs !

Please help me to SHARE this page through Face book as I am not seeing the Shared Link!! Thanks.

Dear Saravana,

You can share the link through the floating social media icons available on the left hand-side of the blog post (if accessing through a desktop).

(or) you may just copy the url link of blog post and share it on your FB account.

Thank you!

Simply Outstanding Sir and I will definitely help my Maid to open all the Accounts as you have posted. Thank you very much and will share in FaceBook.

Hi Sreekanth,

Wonderful thoughts, this shows how dedicated you are with society as well.

Thanks for letting us know these details and wisdom thoughts.

Regards,

Shravan

Dear Shravan..Thank you for your appreciation and kind words!

Kindly share the article with your well-wishers!

Thank you for such a great article. I am regular reader but have never commented but with this brilliant article could not resist.

Dear Arvind..Thank you for following my blog posts! Keep visiting ReLakhs.com .

Kindly share the article with your friends!

Very good article as usual focusing towards our society. :):)

Thank you dear Kiruba! Keep visiting ReLakhs.com

Excellent Blog with real time examples . Good work Sreekanth .

Thank you bava!

This is an excellent article Sreekanth and these tips are things that each of us can follow. Keep up the great work!

Thank you so much!