Our honorable PM, Shri Narendra Modi has launched three JAN SURAKSHA schemes on 9th May, 2015. These three schemes are Atal Pension Yojana (APY), Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) and Pradhan Mantri Suraksha Bima Yojana (PMSBY) .

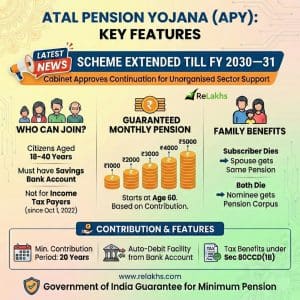

PMJJBY and PMSBY are insurance related schemes, whereas APY is a pension scheme for citizens of India, primarily focused on the unorganized sector workers. Under the APY scheme, a guaranteed minimum pension of Rs. 1,000/-, 2,000/-, 3,000/-, 4,000 and 5,000/- per month will be given at the age of 60 years depending on the contributions made by the subscribers.

In case of death of the subscriber, pension amount will be given to the spouse, and on the death of both (subscriber & spouse), the accumulated pension corpus would be returned to the subscriber’s nominee.

Let’s understand more about Atal Pension Yojana (APY) scheme in FAQ format.

Atal Pension Yojana (APY) – Details, Features & FAQs

- Who can enroll for (or) join APY scheme? – Any Citizen of India can join APY scheme. The following are the eligibility criteria;

- The age of the subscriber should be between 18 – 40 years.

- He / She should have a savings bank account/ open a savings bank account.

- The prospective applicant should be in possession of mobile number and its details are to be furnished to the bank during registration.

- Can subscribers / members of EPF (Employees Provident Fund) subscribe to APY scheme? – Yes, the beneficiaries of any social security schemes can also enroll for this scheme.

- Can I open two or more APY accounts? – No, only one account per person is allowed. Savings bank account is mandatory to open an APY account.

- How to open Atal Pension Yojana Account? – Approach the bank branch where your savings bank account is held. Fill up the APY registration form. Provide Aadhaar/Mobile Number. Ensure keeping the required balance in the savings bank account for transfer of monthly contribution.

- Latest update (26-Jan-2018) : Small Finance Banks and Payment Banks to offer Atal Pension Yojana.

- What is the mode of contribution to APY A/c? – All the contributions are to be remitted monthly through auto-debit facility from savings bank account of the subscriber.

- I don’t have Aadhar number. Can I join Atal Pension scheme? – It is not mandatory to provide Aadhaar number for opening APY account. However, For enrollment, Aadhaar would be the primary KYC document for identification of beneficiaries, spouse and nominees to avoid pension rights and entitlement related disputes in the long-term.

- How much pension am I going to get? – The lifelong pension amount that you receive from 60 years of age is dependent on the contribution amount during accumulation stage. The pension amount ranges from Rs 1,000 to Rs 5,000 (in the multiples of 1000’s).

- Which authority is going to administer this scheme? – APY scheme is administered by PFRDA (Pension Fund Regulatory and Development Authority ) Or Government. (PFRDA also administers National Pension System – NPS)

- Is Government going to contribute any amount to my APY account? – Government co-contribution is available for 5 years, i.e., from 2015-16 to 2019-20, for the subscribers who join the scheme during the period from 1st June, 2015 to 31st December, 2015 and who are not covered by any Statutory Social Security Schemes and are not income tax payers. That means, if you are contributing to say EPF or any other similar schemes, then you will not be eligible to receive Govt’s co-contribution amounts.

- (Latest News : 19-Jan-2016 – Extension of time-line upto 31st March, 2016 for Government Co-contribution under the Atal Pension Yojana (APY). The Government has decided that the co-contribution by the Central Government will be available for those eligible subscribers, who join APY before 31st March, 2016)

- Latest News : The Union Cabinet on 22-Jan-2026 approved the continuation of the Atal Pension Yojana (APY) till the financial year 2030–31, extending government support for the popular social security scheme aimed at unorganised and low-income workers.

- What will happen if required or sufficient amount is not maintained in the savings bank account for contribution on the due date? – Non-maintenance of required balance in the savings bank account for contribution on the specified date will be considered as default. Banks are required to collect additional amount for delayed payments, such amount will vary from minimum Re 1 per month to Rs 10/- per month as shown below:

- Re. 1 per month for contribution up to Rs. 100 per month.

- Rs 2 per month for contribution up to Rs. 101 to 500/- per month.

- Rs 5 per month for contribution between Rs 501/- to 1000/- per month.

- Rs 10 per month for contribution beyond Rs 1001/- per month.

- What will happen to my APY account if I discontinue the payments? – Discontinuation of payments of contribution amount shall lead to following:

- After 6 months account will be frozen.

- After 12 months account will be deactivated.

- After 24 months account will be closed.

Subscriber should ensure that the Bank account to be funded enough for auto debit of contribution amount.

- Are there any income tax benefits available? –

No tax deductions are available on the contribution amounts to APY.Latest update (23-Feb-2016) : Contributions to ‘Atal Pension Yojana’ are now eligible for Tax Deduction under section 80CCD. - How to know my APY account balance amount? – You will receive SMS alerts related to account details/activity. You will also receive a physical statement at regular intervals.

- Can I change monthly contribution amount? – Yes, the monthly contribution can be changed once in a year for higher / lower pension amount.

- Can I exit from APY scheme before attaining 60 years? – The Exit before age 60 would be permitted only in exceptional circumstances, i.e., in the event of the death of beneficiary or terminal disease.

- Settlement of Death Cases before the age of 60 years of the Subscriber :

- If the subscriber dies before the age of 60 years, his/her spouse would be given an option to continue contributing to APY Scheme, for the remaining vesting period, till the original subscriber would have attained the age of 60 years.

- In case the spouse of the subscriber wishes to exit from the scheme and close the account, the corpus will be settled in the name of surviving spouse (if spouse is not present, will be settled in the name of the Nominee).

- Below is the Account Closure Form (Death cases).

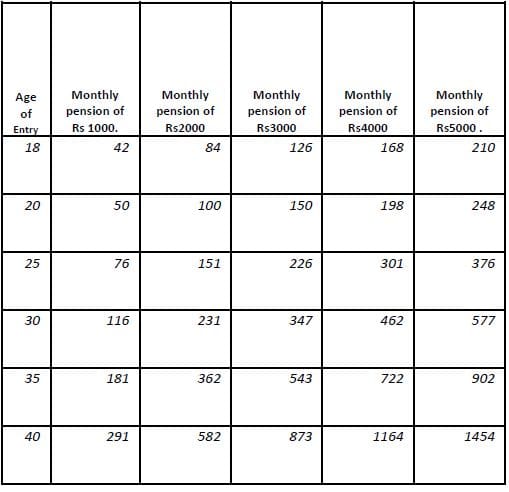

How much should I invest in Atal Pension Yojana to get the guaranteed pension of Rs. 1000 / Rs 2,000 / Rs 3,000 / Rs 4,000 / Rs 5,000?

Below is the indicative contribution chart (Age Vs Pension amount). For example – A 30 year old individual has to contribute Rs 577 per month, to get Rs 5,000 per month pension amount. He/she has to make the contributions for 30 years (60 years minus 30 years age).

What is the corpus amount under Atal Pension Yojna Scheme?

What is the corpus amount under Atal Pension Yojna Scheme? If a subscriber opts for Rs 5,000 as the pension amount, in case of death of subscriber, pension would be available to the spouse and on the death of both of them (subscriber and spouse), the pension corpus (as indicated in the above table) would be returned to his / her nominee.

If a subscriber opts for Rs 5,000 as the pension amount, in case of death of subscriber, pension would be available to the spouse and on the death of both of them (subscriber and spouse), the pension corpus (as indicated in the above table) would be returned to his / her nominee.

Latest update (20-Aug-2015) : Government has modified some of the conditions & features related to Atal Pension Yojana Scheme as below;

- The APY subscribers shall now have an option to make the contribution on a monthly, quarterly, half yearly basis instead of on a monthly basis earlier

- Discontinuation of payment of contribution provision has been substantially modified in favor of the subscriber. The account will not be deactivated and closed till the account balance with self-contributions minus the Government co-contributions becomes zero due to deduction of account maintenance charges and fees

- Also the penalty on delayed payment has been simplified to Rs. One (1) per month for contribution of Rs. 100, or part thereof, for each delayed monthly payment instead of different slabs given earlier

- Similarly, premature exit from the scheme before sixty years of age was not permitted earlier except in exceptional circumstances, i.e., in the event of the death of the beneficiary or terminal disease. Now the modified provision permits the subscriber to voluntarily exit with the condition that;

- He shall only be refunded the contributions made by him to APY, along with the net actual interest earned on his contributions (after deducting the account maintenance charges) and ;

- The Government co-contribution, and the interest earned on the Government co-contribution, shall not be returned to such subscribers

(Source : pib)

Latest Update (22-March-2016) : The Government has decided to give an option to the spouse of the subscriber to continue contributing to APY account of the subscriber, for the remaining vesting period, till the original subscriber would have attained the age of 60 years instead of present provision of handing-over lump-sum amount to spouse on the premature death (death before 60 years of age) of the subscriber. The spouse of the subscriber shall be entitled to receive the same pension amount as that of the subscriber until the death of the spouse. After the death of both the subscriber and the spouse, the nominee of the subscriber shall be entitled to receive the pension wealth, as accumulated till age of 60 years of the subscriber. (Source : pib)

Latest update (13-June-2017) : Any individual who is eligible to receive benefits under the APY will have to furnish proof of possession of Aadhaar number or undergo enrollment under Aadhaar authentication. Accordingly, an APY subscriber will have to get the Aadhaar number recorded in his or her APY pension account and also in his/ her savings account where the periodic pension contribution installments are debited and government co-contribution is to be credited. In case a subscriber is not yet having an Aadhaar card, he/ she should immediately get him/ her enrolled for the Aadhaar card for which he or she can visit the nearest Aadhaar enrollment centre.

APY Calculator

Kindly click on the below image to visit APY online calculator link.

My opinion on APY Scheme

The pension amount under APY scheme is a guaranteed one. This may sound attractive, but from returns point of view and considering the rate of inflation in India, the pension amount (maximum Rs 5,000 per month) may not be sufficient during the retirement age.

However, in India we do not have any Social Security System. So, this scheme is an attractive one especially to the lower income group or individuals who are working in the unorganized sectors. However, the higher income group families may also reap the benefits of this scheme, which is primarily meant for the poor.

You may consider opting for Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) and Pradhan Mantri Suraksha Bima Yojana (PMSBY) before subscribing to APY.

Do you think that this is a good scheme? Do share your views and comments on Atal Pension Scheme?

For more details on APY, you may dial Toll Free number (national) 1800-180-1111 /1800 -110-001. Download Atal Pension Yojana’s application form (account opening form or registration form).

Continue reading : ‘How to view APY Transaction Statement online?‘

Join our channels

Hi

My month of birth is July , so if join APY on August or December or next year June or join before next birthday . Will Premium remains ?same .since premium is same ,it’s best to register APY month before your birthday.

My wife and I have that apy. After I die, my wife will receive a pension as a nominee. What will you get at both pension?

In Atal Pension Yojana what happens to the contribution made when the person has not completed age of 60yrs in the event of

a. Payment is stopped in between

b. Death

Dear Priyanka,

The Exit before age 60 would be permitted only in exceptional circumstances, i.e., in the event of the death of beneficiary or terminal disease.

You can refer to the section – “Settlement of Death Cases before the age of 60 years of the Subscriber ” in the above article..

I have withdrawn myself from APY contribution, how can I rejoin it

HI Sreekanth Reddy i have started the APY at the age of 37 and paying 990rs for 5000rs scheme what will be the amount of corpus

Hi Sreekanth,

Can I open APY account from my NRI HDFC Account?

Dear Pandiarajan,

Only Indian citizens are eligible to open the Atal Pension Yojana account. If the subscriber becomes an NRI, then his account will be closed and treated as a voluntary exit done before the age of 60.

Well written article, thank you Sreekanth.

I had read somewhere that if subscribed for E.g. for Rs.5000/- p.m as pension, then the returns is guaranteed to be equal to Rs.5,000/-, though it can be more than this amount as well (according to actual returns earned by fund manager). Is this understanding correct?

Dear Kris,

I believe its the maximum pension..

Can you kindly share the resource url link??

Let’s consider after 60 years, I’ll start getting monthly pension of 5000/- as per the scheme. Till what age I’ll get pension?

if a person dies at a age of 80, still spouse will get pension because that person had taken a pension for 20years?

Dear Mohammed,

If a subscriber opts for Rs 5,000 as the pension amount, in case of death of subscriber, pension would be available to the spouse and on the death of both of them (subscriber and spouse), the pension corpus (as indicated in the above table) would be returned to his / her nominee.