When you are investing in a mutual fund scheme, you primarily get to see four different options to choose form ; An MF Scheme has Regular & Direct plan versions and also growth & dividend options.

Under growth option, you will not receive any returns in the intermediate. You will not receive any payments in the form of interest, dividends, gains, bonus etc. You will get your returns only on selling the units.

Under dividend option, you will receive returns at periodic intervals. However, the intervals are not certain and dividend amount is also not fixed.

If your investment objective is wealth accumulation, you pick Growth option. In case, you would like to receive dividend income at periodic intervals, you pick Dividend option.

The behavior, investment objectives, portfolios & fund manager are all the same for all the above listed options (Regular, direct, Growth or Dividend plans).

(Related article: ‘What are direct Mutual Fund plans?‘)

We know that the returns from Direct plans outperform their respective Regular plans of MF schemes. But, what about the Dividends? Are dividends declared by regular and direct plans same? Or, do regular plans pay you more dividend? If yes, what is the reason? Let’s discuss….

How are dividends paid by a Mutual Fund scheme?

Dividends reflect distribution of gains and profits. All mutual fund houses calculate the dividends for each of their plans based on the distributable surplus.

What is Distributable surplus? – A plan’s distributable surplus is computed as its Net Asset Value (NAV) minus its face value, unrealised gains and accumulated Unit Premium Reserve (UPR).

Distributable surplus = NAV – (Face value + Unrealized gains + Accumulated UPR)

Let’s take an example : You invest in a fund at an NAV of Rs 25, Rs 10 would go to an account called unit capital account, as the face value is Rs 10. The balance of Rs 15 (Rs 25 – Rs 10) would go in an account called unit premium reserve. If the invested amount of Rs 25 grows up to Rs 30, the fund can declare a dividend from Rs 5 which is the gain on Rs 25, the NAV. Out of this Rs 5, if the fund manager sells securities worth Rs 3 then it is called as realized gains and Rs 2 can be unrealized gains. In this case, the scheme can declare a dividend of Rs 3 only (maximum).

(Related article : ‘What is NAV? How is it calculated?‘)

(In March 2010, Sebi asked mutual funds not to use unit premium reserve to pay dividends. It was noted that some fund houses were paying dividends from their unit premium reserve instead of the realized gains. Realized gains arise from sale of mutual fund assets or appreciation of assets.)

Why dividends in direct plans of MFs can be different?

If you analyze the percentage of dividends declared by various schemes for the last 3 to 4 years, you can notice that for some of the schemes, you will be paid a different, usually smaller, dividend than a regular plan investor.

Data from portals like Value Research/moneycontrol show that this is not a trend across mutual funds and schemes. It is specific to some schemes. The reason why some direct MF plans did not declare dividends (or) declared lower dividend, was because of the above quoted SEBI’s rule that dividends can only be paid from realised gains.

We now understand that fund houses should not touch UPR for dividend declarations.

How is UPR determined? – UPR is determined at the plan level after apportioning realised and unrealised gains in the ratio of the respective assets under management.

Distributable surplus = NAV – (Face value + Unrealized gains + Accumulated UPR)

&

UPR = Units * Unrealized Gain component in NAV

So, the ability to declare dividends in a plan depends on the Gains & UPR balance. Even if the returns in the direct and regular plans under a scheme are similar, the dividend could vary depending on the UPR balance in the mutual fund plans.

Some Direct plans may not have a distributable surplus (or have a low surplus) due to a higher proportion of UPR and, therefore, they may not been able to declare dividends in those plans (or declare lesser dividend % when compared to respective regular plan).

Also, the differences between plans can arise because direct plans were introduced only recently in early 2013. The realised gains are higher in the case of regular plans than direct plans simply because the former have been around for longer.

SEBI’s rule as cited above forces AMCs to distribute dividend only out of the accumulated gains that the fund has made. Typically, proportion of accumulated gains is much larger in the corpus of regular plan, and much smaller in direct plans. This obviously happens because the regular plans are older.

Therefore, since the rules have to be followed, the regular plan has a much higher amount available for dividend distribution.

To sum up, the dividend declared in a plan depends on its performance, position of gains and the UPR balance. But, let’s understand the fact that RETURNS generated by a Dividend and Growth Options of a Scheme remain same. Also, the returns generated by a Direct plan (div/growth) will outperform the Regular plan of a Mutual fund scheme.

So, the difference in dividend payout is not a ploy by fund houses to make direct plans less attractive, but it’s a regulatory requirement / an accounting challenge.

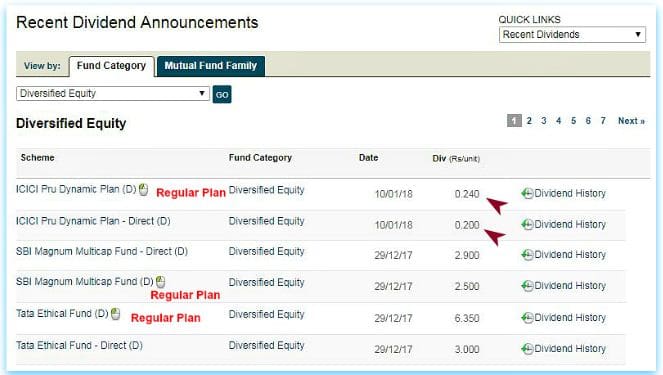

In the below table, I have tried capturing the dividend history of few popular Mutual Fund schemes and this clearly indicates that there is no clear trend as such (as of now).

As reserves grow, the funds may declare more or less same % of dividends for regular and direct plans. We might also see direct plans declaring higher dividends in the long-run.

Budget 2018 has proposed 10% tax on Dividend distribution on Equity oriented (Dividend option) units (payable by the Fundhouses). Also, note that as per Budget 2016, income by way of dividend in excess of Rs 10 lakh is also chargeable at the rate of 10%.

Continue reading :

- Mutual Fund Investments are subject to Market Risks! – My opinion

- Switching to Direct Mutual Funds From Regular MFs? Keep in mind these handy tips!

- Why your Best Mutual Fund Schemes may not remain as ‘the best’? | Categorization & Rationalization of MFs

- Mutual Funds Vs ULIPs – Which is better? | Post Budget (2018) LTCG Tax proposal on Equity Mutual Funds & Shares

- Budget 2018 LTCG Tax on Equity Mutual Funds & Important Implications

(References : Valuereasearchonline, moneycontrol, thehindubusinessline & freefincal.com)

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net) (Post first published on : 11-January-2018)

Join our channels

Hi Sreekanth – I have 5 lac contingency fund that I am looking to invest in a debt fund. What would be your recommendation? 3 year time horizon is good for me

Dear Rajan,

You may pick either a Liquid Fund or an Arbitrage Fund.

Ideally a liquid fund.

Kindly read :

* What is an Emergency Fund? | Why, Where & How much to save?

* All you need to know about Arbitrage Funds

Thank you Srikanth in giving insights of funds direct and regular plans. Usually, the managers or sales person will never explain the expences or commissions involved while selling the funds. I made huge mistake in buying ULIPS from SBI LIFE and has lost almost rs. 2.75 lakhs within 5 months on a total investment of rs. 12 lakhs. Even an educated person like me and worked in MNC fell into this scheme played out by the SBI CHEIF MANAGER who has sold this product .

Every month my units are reducing in the form of expences (almost RS 9000. mortality charges etc) . They bought EACH unit at rs 14.36 and after my calculation I found that only at rs. 18 my amounts I deposited will even out at the end of the year. Hope the market rises and If it is less than rs.18.50 then I found the amount has gone out as expences despite buying each unit at rs14.36. SBI LIFE is doing a REVERSE SWP on the amount I paid for It seems like a PONZI scheme where in almost 10 % – 15%of of the money deposited by customer is taken away by SBI LIFE in the form of expences. I am cancelling this scheme and I take a loss of almost rs. 2.5 lakh now itself rather waiting to erode my total value at the end of 5 years. Please explain. Thank You Prasad

Dear PRASAD,

To get decent returns from ULIPs, an investor has to remain invested for long-term ie till the end of the policy term.

Personally, I believe that MFs are better than ULIPs, and advisable not to mix insurance and investment..

For life cover, one can buy a Term insurance plan.

Kindly read :

MFs Vs ULIPs

Best Term insurance plans

Aditya Birla SL Top 100 -13000

SBI Bluechip Direct-13000

SBI Magnum Balanced-8000

Canara Robeco Emerging Equities-8000

Franklin India High Growth Companies -8000

Franklin India Smaller Companies-8000

Mirae Asset Emerging Bluechip-8000

Total sip:66000

SBI Pharma-G-50000 Lump sum

The above is my portfolio I have started sip from 2015 and this year i have double my SIP installments. Am i going the right direction for long term.5-10years.AGE-27

Dear bharath,

Individually all the listed funds are good ones. You may continue with your investments.

However, kindly check their portfolios overlap..

Dear SR! Thanks for the article. When can we expect you to write an article about Best Mutual Funds to invest in 2018?

Dear Kumar,

I am waiting for the fund houses to re-structure the currently available schemes based on new SEBI norms.

As of now, this exercise can get over by March 2018.

I wish to review and write on ‘best equity funds’ after the re-categorization is implemented. Hope this is the right approach and my blog readers will accept my decision.

Thank you!

Dear SR! Thanks for your reply. Well said and I am also one among your blog readers for long time.

Hello Sir,

Is there anyway, we can track, what my current fund manager is buying or selling. Suppose, I am invested in Franklin India bluechip fund and I want to know, what my fund manager did today, which stocks he is buying/selling and what quantity? Monthly sheet is updated on the website but what about last day trades? Please help!

Thanks!

Dear Rahul,

Very good question!

But I do not have the answer or links to share to track the MF portfolios on a daily basis.

However, monthly basis portfolio can be checked on portals like Moneycontrol.

Hi Rahul,

Can I understand what objective does it serve to compare each stock portfolio that on daily basis? It is too much of a admin work and will result in additional expense ratio with no obvious benefit to the retail investor. Moreover, fund manager will then get more cautious and his freedom to invest in the stock based on the stock picking skills is limited. It’s like saying that your company (if you working on 9-5 ) wants activity list of every hour you did on your job.

The reason you are buying the mutual funds is because of the reputation of the funs and the fund manager, let him do the job or be ready to pay more. Instead you would be better off making you own investment if you can track pelothra of stocks and think you make make better decision.

Rakesh Brother, I appreciate you want to understand my objective regarding my above comments but I am sorry, as of now, it’s impossible for me to explain it here. 3 reasons. 1) Biggest>> My plan/strategy is not final. 2) It will take 5-6 pages to write here. I am not sure, Sreekanth sir will allow me to write here (Frankly, I also dont want to disclose here as of now cause, I am still not 100% confident here so why confuse others). 3) Its very difficult to understand and track fundaments on companies on a daily basis so Fund managers has a set of people to guide him, so they will take headache and research and I will earn lol (sorry acting like a child).

Very soon, I solve this puzzle myself. Brother, but I want to share few other things with everyone, which might help you or help others.

Plz note, this is my first reply on any forum so sorry in advance for all the errors (customization etc) lol. I am new to this and trying my best to be successful one day. I know, I will fall many times but every time, I fail, I will learn >> will not repeat same mistake again and move forward.

2-3 rules which I follow strictly: –

1) I listen to everyone with open mind but never follow anyone. All of us have some role models in this market, ohh, xx person, did some in 80’s and he now a millionaire. What they did years back, I dont want to know or neither I follow. I take their suggestions and then research on my own and do my work accordingly. We need to understand, every day of market is a new day so we cannot compare 2 days.

2) I try to avoid all market related news channels, rumors. I just follow and learn from this kind of forums who are putting some genuine efforts.

3) I try to strict with my original plan and change only when its required (no space for emotions or anyone’s suggestions)

WHY I AM WRITING ALL THIS >> JUST TO HELP U ALL THAT >> IF U WANT TO MAKE SERIOUS MONEY HERE >> THEN U NEED TO COME UP WITH A GREAT PLAN >> U NEED TO DO THINGS >> WHICH OTHERS OR ATLEAST NORMAL PEOPLE >> CANNOT THINK OF. LET ME SHARE ONE OF MY SIMPLE PLANS.

If we read any forums including this one (Sreekanth sir), they are correct, you should expect more than 12% return in MF but WHY NOT? >>> This answer is not true for me. I know, I can generate more returns here so below is my explanation.

PLZ NOTE = I try to PLAY SAFE and EXPECT HIGH RETURNS (which everyone wants lol)

Example = I have 10k to invest/save (total investment amount) (horizon 10+ years or when goal is achieved, if I have reached to my amount, I will change my plan)

Now, if we want to follow 70:30 allocation (equity:debt) which 7k/3k. Which plans and investment are best for u for equity/debt, u can plz read Sreekanth sir forums.

What I do little different here is>> My allocation is 80:20 (equity:debt) which 8k/2k.

But for the past 2 years, I am investing my 50% amount only in equity (MF) and 50% in debt. I am saving my 30% amount in debt every month for equity (I will PLAY with this amount later in the market).

2 VERY IMP FACTORS >> 1) We need to understand, P/E ratio and 2) DMA – Daily moving average.

P/E ratio >> u can search google and learn. DMA >> As of today, moneycontrol is showing

30 Days : 10,537.31 50 Days : 10,421.11 150 Days : 10,115.82 200 Days : 9,939.57

We need to invest more, when we are below DMA. We need to understand and study this in detail. We will find many good blogs on this on Google.

People have a habit of entering markets, when its on high (book less profits, even if they try to do it). Same with MF industry. Dont we hear, every month, we are receiving more and more domestic inflows? We never question, why this is happening?

Now, the questions comes, so we should not invest in MF, when marketing is going high. WELL answer to this question is, we should invest regularly via SIP. We cannot predicts highs/lows. If we ONLY WAIT for lows and markets get doubled in 3-4 years>> we will cry.

My plan >> I am investing only 5K in equity for the past 2 years as per above example (My original allocation is 8k equity and 2k debt).

Remaining 30% (3 k) >> I am also investing in debt. >> I AM WAITING FOR THE RIGHT TIME.

When I see P/E ratio and DMA as per my rules. I am extremely sorry, I cannot everything in detail, its very hectic and everyone will get confused.

I will put some %, when P/E ratio and DMA is xx, then some more, when its xx, some more, xx till my amount of 30% gets 0.

Now, if I have to wait for that moment for 3 years, 5 years, 7 years or it never comes, I am ok with it.

One more IMP thing >>> out of 30% amount (3K as per above example). 2 k will go in LUMP sum IN MF and 500 rs will go in large cap direct stocks and rest 500 rs in mid/small cap stocks >> this plan I will only implement in bear market, until then I will wait.

OK, let me share one more plan with everyone. We need to identify few things which we see around us. Example = DONT U THINK, day by day, pollution is getting high in our cities, people want organic foods , government want eco friendly vehicles etc etc. So DONT U THINK, we should invest in those companies to get good returns.

Now, let me share little strategy on this. You are in bear market or shares u are getting at good P/E ratio and numerous other small factors. Assuming you have 10 k and you select 5 stocks of different sectors as per your research, do you think, you will loose your money. I dont think SO. Even if 3 companies out of 5 are not doing well and your amount is 0 (which never/rarely happens) still you will be in big profits.

Bro, if we actually look at my actual portfolio in direct shares, its only 10% in which 5% are blue chip stocks and 5% small/mid cap stocks. So, you can see, I trying to play safe.

So, my actual plan is 70% MF, 10% direct stock 20% debt but for the past 2 years, I am maintain 50% MF and 50% debt portfolio >> waiting for the right time/valuations >> even if it never comes >> I am happy and ok with it. I also have some fixed rental incomes so I dont worry about my debt portfolio.

Again, my advice from my heart for everyone is no 2 persons are same. So, define your goals, your risk taking abilities, your goal time frame and use your own brilliant mind to do same things in a different way.

I have never taken any fundamental skills course. I am also a middle class person with some realistic dreams and I hope, I can achieve them. My work schedule allows me to do research on few silly things and I love doing this, so you can say, its my passion to work things differently but in a safe manner.

PLZ NOTE >> Investment we do for our comforts >>> Money/things will never give you happiness >> so save only that amount which you can comfortably save and invest. In our old age, our health will not be good, we will have less energy. What you will do with 2CR, 10CR, if you cannot enjoy with that money. So please try to live every moment to the fullest and be good and do good to everyone. Thanks all and my best wishes to everyone. Please try to make this world a better world in all aspects! 🙂

Thanks for your reply. Seriously, instead of doing this. You can just setup a seperate portfolio that mimics that of a fund and start monitoring on hourly basis!

haha, thanks for your suggestion but I am small person and I dont have huge amount of money to copy full mutual fund even if I do, will I get more returns than that actual fund ?? lol

No offense but I feel, I wasted my precious 1 hr to write everything above.

I am investing in MF since 2006 so I know, with above plan there is major difference in CAGR* fund returns and CAGR* my portfolio returns. I have many things to show and prove but really dont want to say anything here now.

I have mentioned above things, not to show myself as super human or super smart person but I wanted to show to everyone, if we do little hard work and catch small things, especially if we have passion and can give good amount of time in research, we can surely earn good money without taking any high risks.

Above I only said things, which I have achieved. I am not hitting bullets in air.

Ok, this is my FINAL comment. By nature, I consider myself as fool and willing to learn from everyone then give my best but this scenario I can clearly feel, its going in arguments.

Rakesh bro, I am sorry, if you are upset with any of my comments. I just trying my best, maybe, you are better and knowledgeable person than me (cause level of understanding is different from person to person). Just a suggestion >> You should never comment in between, if you cannot respect others person questions.

Disclaimer: – For other people reading my comments>> (I forgot to write this in previous comment). Please do not take my comments seriously and definitely do not invest a single hard earned penny. Do your own research and then take best judgments as per your capacity, risks etc. There is no one in this world who can understand yourself better than you.

Again readers, this is very nice website. Believe me, till date I am still learning many things from here and tracking this website on a monthly basis.

Sreekanth Sir, just to share one secret with you. Today, as you know markets were hitting new highs so I was just happy to share some of view points which I usually dont do. I know, its very hectic thing to read, comment which you get on a daily basis but sir, you are really doing this job very well. Believe me Sir, in the past 12 years, I have read hundreds of websites but if it comes to personalization, I will rate you in top 3. Very very great work sir.

To All >> I am sorry for all the troubles (if any). Be happy, be blessed and love yourself. JAI HIND!

Dear Rahul & Rakesh,

I have great respect for each and every visitor/reader of my blog. I learn a lot from my blog readers’ comments/queries.

Every one of us have our own way of analyzing. There is no right or wrong approach.

Both of you are correct with your viewpoints.

End of the day, as opined by Rahul, its PERSONAL finance, let’s customize as per our requirements. Let’s stick to our convictions.

Keep visiting, Cheers!

I have these 3 MF. Please tell me your opinion. Total investment 20,000 every month from last 5 years. Thank you.

1. Birla SL Equity

2. DSP blackrockt Top 100

3. Reliance regular savings – growth equity

Dear Richa,

The first two ones are fine.

I believe that there are better options than Reliance Regular Savings Fund – Equity Option. As of now, this fund has allocation of around 60% to mid/small cap stocks. In case, you would like to replace it then you may consider options like HDFC Mid-cap/ Franklin prima/ Mirae Emerging bluechip fund etc.,

Kindly read:

How to pick right mutual fund schemes?

MF Portfolio overlap analysis tools

Sir, I am following your blog for the past 2 years and just curious to know, when you will post ” Best mutual fund to invest in 2018″? Thanks! 🙂

Dear Rahul,

Thank you for following my blog posts!

Ideally I would have posted the best Equity funds 2018 list by Dec month end, but SEBI has suggested re-categorization of mutual fund schemes and the fund houses have to re-structure the schemes totally.

“Only one scheme per category would be permitted.”

Hence, waiting for the fund houses to implement these norms. Initially they have informed the time-line as 3 months…

thanks Shreekanth for your valuable article regarding dividends.Good work.

I could not understand the table put at end. There is no difference of dividend %age paid either for regular or direct plans, hence your comparison between 2 are not correct. Am i missing anything ?

Dear Suresh,

Its my attempt to convey that there we can not establish any clear trend that only Regular plans higher dividend (or) both plans can pay same dividend rates… it can be either way and sometimes a Regular plan can pay dividend and its Direct plans may not pay anything at all and vice-versa!

Hope this makes things clear!

Great Content. Thank you for the information.

Dear Sreekanth, Anand Shastri’s understanding of “returns” is incorrect and it is better that you state it clearly in the article. There is no difference in returns between a div option and growth option. SEBI clearly mandates that div option returns should be calculated by assuming returns are reinvested at ex-nav and this make both returns the same.

Therefore even if direct plan dividends are lower, the direct plan ALWAYS will have higher returns than a regular plan. Many investors do understand that a dividend is a redemption made by the amc – resulting in lower NAV. Whereas when we make the redemption, the NAV does not change and out units become lower.

There is an article by Uma Shashikant that SEBIs accounting rule is incorrect and will result in such imbalances. That aside, I think it is simple business tactics that determine the quantum of dividends declared. Many distributors routinely tell investors to buy before a dividend.

It is not easy to spot a clear reason for this as it changes from fund house to fund house. Direct plan investors should not worry and be rest assured that they are not being short-charged in anyway because of a lesser dividend.

Dear Pattu sir,

Thank you for sharing your views and suggestions.

Agree with your view that returns from Div / growth option remain same and I have now highlighted this point in the above article.

If possible, request you to kindly share Uma mam’s article/concept paper link (if any). Tried to trace it on the net, but could’nt find it.

Thank you Sreekanth. I will send it to you.