Capital asset typically refers to anything that you own for personal or investment purposes. It includes all kinds of property; movable or immovable, tangible or intangible, fixed or circulating.

Capital assets are further classified as Financial Assets and Non-Financial Assets. Financial assets are intangible and represent the monetary value of a physical item.

Stocks (Shares) and mutual funds are the best examples of Financial Assets.

The profit (if any) that you make on your mutual fund investments when you redeem or sell the MF units is referred to as Capital Gains. It can be a Short Term Capital Gain (STCG) or a Long Term Capital Gain (LTCG) depending upon the ‘Period of Holding’. The tax that is applicable on these profits is known as ‘Capital Gains Tax’.

In this post let us understand: What are the factors that determine the tax status of mutual funds? What are the tax implications on mutual fund investments? What are the Budget 2019-20 proposals related to Mutual Funds Taxation? – Mutual funds taxation & capital gains tax rates on mutual funds for Financial year 2019-2020 (Assessment year 2020-2021).

Related Latest Article : Mutual Funds Taxation Rules FY 2023-24 (AY 2024-25) | Capital Gains Tax Rates Chart

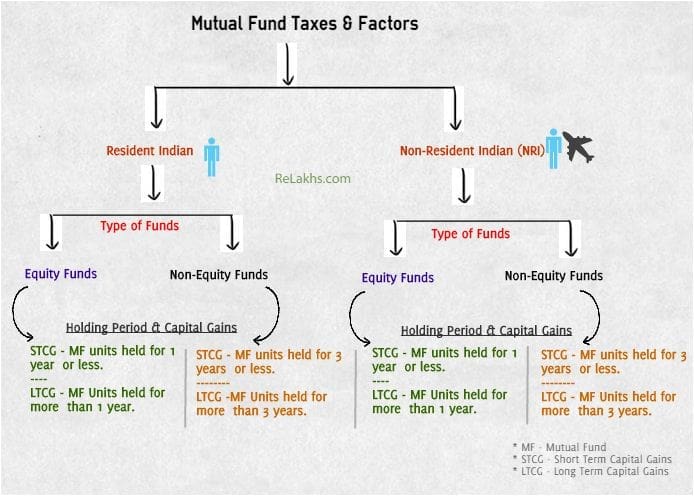

Factors determining the tax status of mutual funds

The capital gains tax on mutual fund withdrawals is based on the factors as below;

- Residential Status

- Fund Type (whether the fund is an Equity-oriented fund (or) a Non-Equity Oriented Fund)

- Holding Period (Duration of your investment)

1. Residential Status & Mutual Funds Taxation

The capital gains tax rates are determined based on the residential status of an individual / investor. Residential status can be either ‘Resident Indian’ or ‘Non-Resident India” (NRI). (Related article : ‘Residential Status online calculator.’)

2. Type of Funds & Mutual Funds Taxation

What are Equity-oriented Mutual Funds? – MF schemes that invest at least 65% of its fund corpus into equity and equity related instruments are known as equity mutual funds. Examples are : Large cap, ELSS tax saving funds, Mid-cap, Balanced funds (equity oriented), Sector funds etc.,

What are Non-Equity Mutual Funds? – MF schemes that hold less than 65% of their portfolio in equities and equity related instruments are known as Non-Equity Funds / Debt funds. Examples are : Liquid Mutual funds, Money Market funds, Gold funds, Infrastructure debt funds, MIPs, FMPs, Hybrid funds (Debt oriented) etc.,

3. Period of Holding & Capital Gains on Mutual Funds

Capital gains on Mutual funds could be either long term capital gains or short term capital gains, depending on your investment horizon.

- Long Term Capital Gains

- If you make a gain / profit on your investment in a Equity Mutual Fund scheme that you have held for over 1 year, it will be classified as Long Term Capital Gain.

- If you make a gain / profit on your investment in a Non-Equity Mutual Fund scheme (or in a Debt Fund) that you have held for over 3 years, it will be classified as Long Term Capital Gain.

- Short Term Capital Gains

- If your holding in a Equity mutual fund scheme is less than 1 year i.e. if you withdraw your mutual fund units before 1 year, after making a profit, then the profit will be considered as Short Term Capital Gain.

- If you make a gain / profit on your Debt fund (or other than equity oriented schemes) that you have held for less than 36 months (3 years), it will be treated as Short Term Capital Gain.

Budget 2018-19 & Mutual Fund Taxation

- The Budget 2018-19 has proposed to introduce tax on Long Term Capital Gains on sale of stocks and equity mutual fund units from FY 2018-19 (or) AY 2019-20 onwards.

- LTCG tax at 10% on gains of above Rs 1 lakh from Equities & Equity mutual funds.

- No change has been proposed to STT tax rate structure.

- No change has been proposed to holding period to arrive at LTCG/STCG.

- STCG will continue to be taxed at 15%.

- Equity Oriented Mutual Funds will now have to pay a dividend distribution tax (DDT) of 10%. (Read : ‘10% LTCG Tax on sale of Stocks/Equity Mutual Funds | How are Capital Gains calculated on Investments made before 01-Feb-2018?’)

Budget 2019-20

There has been no new proposals made in the Interim- Budget 2019 with respect to Mutual Fund Taxation. Hence, the capital gain tax rules that were applicable for FY 2018-19 remain the same for FY 2019-20 as well.

As per latest Full Budget (July) 2019, the government will launch its Central Public Sector Enterprises (CPSE) exchange-traded fund (ETF) in a tax-saving mutual fund scheme format like ELSS Mutual Funds. The CPSE ETF is an initiative by the government of India to divest its shareholding in select state-owned companies.

Also, a proposal to allow the concessional rate of tax for short-term capital gains on the transfer of units of FoF (Fund of Funds).

- Currently all FOFs irrespective of the underlying asset class gets taxed as per debt fund taxation. The concessional short term cap gains is being proposed for certain type of FoF only and not all of them.

- The STCG @ 15% rate will be applicable on FOFs that invests in a CPSE fund or CPSE ETFs. (STCG rate for debt funds is as per individual’s tax slab rate.)

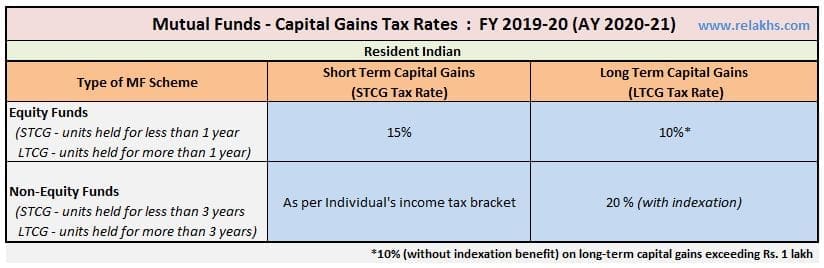

Mutual Funds Taxation Rules FY 2019-20 | Latest Mutual Funds Capital Gains Tax Rates AY 2020-21

Capital Gains Tax Rates on Mutual Fund Investments of a Resident Indian are as below;

- The STCG (Short Term Capital Gains) tax rate on equity funds is 15%.

- The STCG tax rate on Non-Equity funds (or) Debt funds is as per the investor’s income tax slab rate.

- The LTCG (Long Term Capital Gains) tax rate on equity funds is 10% on LTCG exceeding Rs 1 Lakh.

- The LTCG tax rate on non-equity funds is 20% (with Indexation benefit)

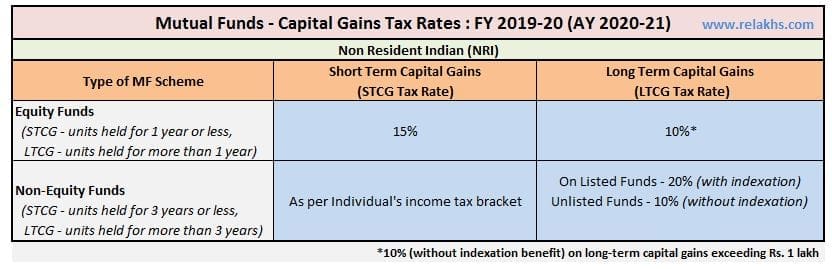

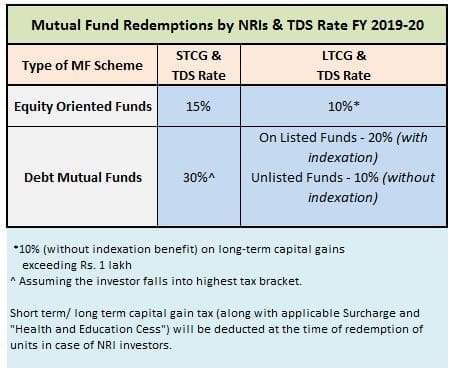

Capital Gains Tax Rates on NRI Mutual Fund Investments for the Financial Year 2019-20 (Assessment Year 2020-21) are as below;

- The STCG tax rate on equity funds is 15%.

- In case the short-term capital gains were on account of listed equity shares which were sold on a stock exchange or equity-oriented mutual fund, then the provisions for tax calculations as per section 111A of the Income Tax Act provide that 15% tax is payable by non-residents on a flat basis without getting any benefit of the initial exemption limit of Rs 2,50,000. Unfortunately, the basic exemption limit is available only for resident individuals and HUFs, and not for any other entities. If the short-term capital gains is not on account of either of the two types of sale mentioned above, then the benefit of initial exemption will be available even to non residents.

- The STCG tax rate on Non-Equity funds (or) Debt funds is as per the investor’s income tax slab rate. (Tax Deducted at Source – TDS @ 30% is applicable)

- The LTCG tax rate on equity funds is 10%, on LTCG exceeding Rs 1 Lakh.

- The LTCG tax rate on non-equity funds is 20% on listed mutual fund units and 10% on unlisted funds.

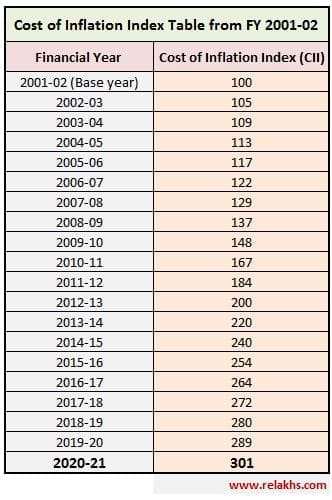

Base Year & Indexation : As per Budget (2017-18), the base year for calculation of Indexation has been changed to 2001. It has an affect (mostly positive) on investments where indexation benefit is available when calculating Capital gain taxes.

- For example: Suppose you are holding on to your investments made in debt funds (or) Property before 2001, the Fair Market Value (NAV) as on 1 st April, 2001 will be considered as cost of acquisition for calculating capital gains. This will help the investor to reduce the capital gains taxes.

- As of now, the base year is 1981. To calculate the capital gains at the time of selling any Deb fund units / property purchased before 1981, its purchase price is now calculated on the basis of the fair market value of 1981. Calculation at the fair market value of 2001 will increase the cost of acquisition and lower the capital gain.

(How do you calculate the indexed cost of purchase? The indexed cost is calculated with the help of above table of cost inflation index.

Divide the cost at which you purchased the Mutual Fund units by the index as on the date of the purchase. Multiply this by the index as on the date of sale.

For Example : If purchase year is 2011 and year of sale is in Financial Year 2015. Then indexed cost of purchase would be –

Indexed cost of purchase = (Purchase price / 184) * 254.)

(Related Article : ‘What is Indexation in Mutual Funds & why it is important to you?‘)

Taxation of Mutual Fund Dividends

- Dividends on Equity Mutual Funds : The dividend received in the hands of an unit holder for an equity mutual fund is completely tax free. However, w.e.f. FY 2018-19, the fund houses have to pay 10% Dividend Distribution Tax (DDT) on equity oriented mutual fund schemes. (Effective DDT rate is 11.648% inclusive of 12% surcharge & 4% cess.)

- Dividends on Debt Funds : The dividend income received by a debt fund unit holder is also tax free. But, the mutual fund company has to pay a dividend distribution tax (DDT) before distributing this dividend income to its Unit-holders. DDT on Debt Mutual Funds is 29.12% (inclusive of surcharge & cess).

NRI Mutual Fund Investments & TDS Rate

Below are the TDS rate applicable on MF redemptions by NRIs for AY 2020-21.

Hope this post is informative. Do you check your capital gains statement(s) every year? Do you include your capital gains taxes (if any) in Income Tax Returns (ITR). Share your comments.

Continue reading :

- Best SIP Mutual Fund Schemes to Invest in 2019 & beyond!

- Top 5 Best ELSS Mutual Funds 2020 | Tax Saving Equity Mutual Fund Schemes

- Cost Inflation Index FY 2019-20 / AY 2020-21

- Income Tax Slab Rates for FY 2019-20 / AY 2020-21

- List of Income Tax Deductions for FY 2019-20

(Assumption – STT (Securities Transaction Tax) is payable) (Featured Image courtesy of Stuart Miles at FreeDigitalPhotos.net) (Post published on 05-Feb-2019) The above taxation rules are based on the Interim Budget 2019 and if required, the details will be edited/updated in the future.

Join our channels

Hi Sreekanth

My query is – Can the Long Term Capital Gain from Mutual Funds be adjusted against either : 1-Long Term Loss from Equity Shares . 2: Short Term Loss from Equity Shares or Both Long and Short Term Loss from Equity shares

Very informative article. One doubt. While carrying forward mutual fund or equity losses are Indexed losses carried forward or only actual losses?

No mention is made of short term losses incurred from Debt Funds. If short term gains from debt funds are to be added to the income for a FY and taxed as per his slab.; are short term losses from Debt Funds deductible from his income?? Or can they be offset against some other capital gains?? Please clarify.

Upon entering the MF gains under LTCG (Rs 90000/=) the itr 2 form is not showing exemption of upto 1 lac. It is taking the entire amount for taxation. I was under the impression that there was no tax for LTCG upto ! lakh

Dear Vikram,

Under the law, income tax at the rate of 10% is to be calculated only on the gains in excess of Rs. 100,000.

If the total amount of such capital gains is less than Rs. 100,000 then the tax on the same would be calculated as zero. Note that, all these numbers in Schedule SI are pulled from the CG schedule and automatically populated by the income tax department’s software.

Your article is very instructive for the investors in Mutual Funds and also for those opting for redemption enabling them to calculate LTCG/STCG.

Further, let me know CII for 2019-2020.

RK Bhuwalka

Dear BHUWALKA,

I think CII for FY 2019-20 not yet notified..Generally we get the update in the month of June..but this year, not yet..

Hi Sreekath, I had invested Rs. 3,00,000 in “DSP Black Rock Equity & Bond Fund” with Dividend option last year and receive Rs. 2426 as dividend every month. Cumulatively I had received Rs. 29112 in FY-18/19. Is this dividend amount in taxable? Where do I show it in ITR? Thank You.

Dear Vai,

DSP Equity & Bond Fund is an Aggressive Hybrid Equity Fund. It is considered as an Equity fund for taxation purposes.

Dividends on Equity Mutual Funds : The dividend received in the hands of an unit holder for an equity mutual fund is completely tax free. However, w.e.f. FY 2018-19, the fund houses have to pay 10% Dividend Distribution Tax (DDT) on equity oriented mutual fund schemes. (Effective DDT rate is 11.648% inclusive of 12% surcharge & 4% cess.)

You can disclose this dividend income as exempt income (section 10(34)) in your ITR.

Hi Sreekanth,

Thank you for the highly useful post.

I invested in Feb.2004, Rs.2 Lakhs in UTI (MIS). I has wrongly been adding the entire MIS amount (Rs.1400/-pm =Rs.16,800 pa) in the taxable income all these years.

UTI local staff told me to show this in indexed LTCG. Any taxable income work-out is available for UTI MIS (as CG) ?

Dear Raghavan,

You need to show only the capital gain amount in your ITR. UTI MIS is treated as a Debt fund.

You can get the Capital gain computation statement from the RTA (Karvy) and use it to disclose the CG in your ITR.

Kindly read : How to get Mutual Fund Consolidated Account Statement / Capital Gains Statement Online?

Hi Sreekanth,

Thank you for the very valuable post.

If I get LTCG less than a lakh, Do I need to declare the amount (45K) at the time of failing the return?

Can we carry forward the STCL / LTCL in following years?

Dear Mukesh,

It is advisable to disclose the capital gains calculation and you can declare such amount as ‘exempt income’ in ITR.

Mutual fund investments are subject to market risks. Please read the offer documents carefully before investing.

Very Informative post

Hi Shreekanth,

I dont know whether my question is relevant to this article or not but still posting here.

Is it possible to transfer my demat account(ICICI Direct) to my spouse name with all the investments in direct equity and mutual funds? Is this will be treated as a withdrawal?

Actually, I would like to handover this demat account and its investment which will continue as it is, to my wife as I will be going out of India for some time.

Thanks and Regard

Anil

Dear Anil,

If your Spouse has a demat account then you can get all the Securities transferred to her name.

You can GIFT the Shares to her name. Gift transaction is a tax-exempt. However, if there is any taxable income gets generated through these gifts then such income should be clubbed to your income and taxed accordingly.

Related articles :

* Got a Gift? Find out, if it is Taxable or Tax-free?* Article – 2

Regarding Mutual Funds :

The person desirous of gifting the units may either bequeath the units to the person whom she/he wishes to gift through a Will or transfer the units through De-mat mode via an off-market transaction in the transferee’s De-mat account. For the latter mode, the units must be held in Dmat mode only. If the units are held in physical mode, then the same will first need to be dematerialized and then transferred through off-market mode as stated above. (Source : AMFI Portal – FAQs)

Thank you Shreekanth for this detailed explanation. I got some idea now.

One thing still I am thinking about is, can I change or transfer this demat account to my wife’s name as she doesn’t have any demat account till now?

Otherwise I will have to open a demat account for her, gift all securities/MFs and then close my account, which I was trying to avoid.

Thanks and Regards

Anil

Dear Anil,

I think you may have to get her a new Demat Account.

Thank you so much Shreekanth for the prompt reply as always.

Really appreciate your efforts.

Very informative