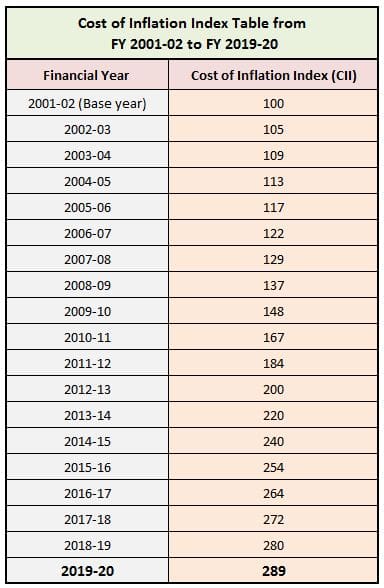

The cost of inflation index (CII) for the financial year 2019-20 has been notified by the Ministry of Finance. The ministry has set the Cost Inflation Index FY 2019-20 as 289. For the previous FY 2018-19, CII was 280.

The rate of inflation for indexation purposes have been specified by the Indian Government for every financial year. The base year has been considered as 2001-02.

The base year has been shifted from 1981 to 2001 in Budget 2017.

This CII number is important as it is used to arrive at the inflation adjusted purchasing price of assets (indexed cost of acquisition) which have been sold or planned to be sold in FY 2019-20.

The indexed cost of acquisition can then be used in the calculation of Long-term capital gains (LTCG) or Long Term Capital Losses (LTCL).

Kindly note that CII is used to calculate inflation-adjusted cost only for those assets where inflation-adjusted (indexation benefit) is allowed. For example, in the cases of debt mutual funds, real-estate property, gold etc.,

Latest Cost Inflation Index FY 2019-20 | CII Chart FY 2019-20

Here is the table of Cost Inflation Index numbers, as stipulated by the Income Tax Department. You can take values from the table to compute the indexed or inflation-adjusted cost of acquisition.

How do you calculate the indexed cost of purchase or indexed cost of acquisition (ICoA)?

The indexed cost is calculated with the help of a table of cost inflation index as given above.

Divide the cost at which you purchased the Property by the index as on the date of the purchase. Multiply this by the index as on the date of sale.

ICoA = Original cost of acquisition * (CII of the year of sale/CII of year of purchase)

Let’s say you have invested in a debt fund in August 2014. Your investment amount was Rs 2,00,000 (20,000 units @ Rs 10 each). Five years later, you redeemed your investments in August 2019, at a value of Rs 3,00,000 ( 20,000 units @ Rs 15 each).

Hence, when you sold your investments, the value of your investments was Rs 3,00,000. Your investment made capital gains worth Rs 1,00,000. However, you need not pay tax on this entire amount of Rs 1,00,000.

All you need to do is apply the formula.

- Cost of acquisition is Rs 2 lakh.

- CII number for purchase year (2014-15) was 240.

- CII during sale year (2019-20) is 289.

This would mean that your indexed cost price of acquisition would be – (2,00,000 * 289/240) = Rs 2,40,833.

As again, your Long term capital gains would come down to Rs. 59,167 (Rs 3,00,000- Rs.2,40,833), you will be taxed 20% of this amount (as compared to Rs 1,00,000 without indexation) which will again, greatly reduce your tax obligations.

Thus, with Indexation, you can enjoy the benefits of your own investments without losing an excessive amount of taxes.

Continue reading :

- What is Inflation?

- Cost Inflation Index FY 2020-21 / AY 2021-22

- What is Indexation of Mutual Funds and why is it important for you?

- How to save Capital Gains Tax on Sale of Land / House Property?

- Different Asset classes have different Tax implications – How Returns are taxed?

(Post published on :13-September-2019)

Join our channels

Hi Sreekanth,

How is the cost of inflation index calculated for the property which was bought under construction?

2013 – Paid 8 lakhs To builder

2014 – Paid 15 lakhs to builder

2015 – Paid 15 lakhs to builder

2016 – Paid 10 lakhs to builder

Got the possession in August 2016.

Now that I am selling the flat this month , what would be the indexation ratio?

Should it as of 2013 or 2016?

301/220 or 301/264?

I am a NRI and I think 22.88% will be the TDS from the buyer as the property is being sold above 50 lakhs < 1 Cr.

To calculate the LTCG I am not sure how to go about it. Any inputs will be helpful.

Thank you in advance,

Keeran

Dear Keeran,

I believe you can get the indexation benefit year wise.

“By making the payment to the builder and having received allotment letter in lieu thereof, the assessee will be holding capital asset and, therefore, the benefit of indexation has to be granted to the assessee on the basis of payments made by him for acquiring the said asset “.

Any payments made before allotment is to be provided indexation from the date of allotment and any payment made after is to be provided benefit of indexation from the date the payment is made.

Related article : How to calculate Holding Period & Capital Gains on sale of an Under-Construction property?

You may kindly take help of a CA as well!

In your example, can we calculate as

1) 10% without indexation, i.e. 10% of (300000-200000) = INR 10000/-

2) 20% with indexation, i.e. 20% of (300000-240833) = INR 11833/-

Can I say, sometimes LTCG calc without indexation may be more beneficial.

Please clarify

Dear Ram,

The LTCG tax rate on non-equity funds is 20% (with Indexation benefit).

We have 300 ncd of Muthoot finance ltd bought in may 2018 direct buying

DUE TO MR SHIVKUMAR OF BANGARU IN CUSTODY WILL THIS HAVE EFFECT ON MUTHOOT FINANCE. WILLCPMPANY MAY BE CLOSED, AND WE ARE LEFT WITH NOTHING. PLEASE reply my worries.

Mrs Mrudula N. Shah.

Dear Narendra,

If the said NCD series are Secured ones, the investors will be given some priority in case if NCD issuer defaults in payments..