Buying a property (home/plot/flat) is one of the most important decisions that you will ever make. It involves a lot of money and is a serious money decision. It is an emotional one too!

There can be instances where you had to sell a property due to various reasons. In case, you wish to sell an already constructed property (ready-to-move-in) then it is pretty straight-forward to calculate the holding period and capital gains (if any).

For example : Mr Pawan Kalyan has bought a ready-to-move-in property through a Registered Sale Deed and sells (re-sale) it to Mr Chiranjeevi (for a profit) in 2018. Here, the holding period for this transaction is 3 years (2018-2015) and the gains are treated as Long Term Capital Gains. So, the holding period is calculated from the date of registration (in his name) to date of Sale.

When you sell a capital asset, the difference between the purchase price of the asset and the amount you sell it for is a capital gain or a capital loss. Capital gains and losses are classified as long-term or short-term.

If Land or house property is held for 36 months or less 24 months or less (w.e.f. FY 2017-18) then that Asset is treated as Short Term Capital Asset. You as an investor will make either Short Term Capital Gain (STCG) or Short Term Capital Loss (STCL) on that investment.

If Land or house property is held for more than 36 months more than 24 months (w.e.f FY 2017-18 / AY 2018-19) then that Asset is treated as Long Term Capital Asset. You will make either Long Term Capital Gain (LTCG) or Long Term Capital Loss (LTCL) on that investment.

You may have to pay Capital Gains Tax on STCG / LTCG.

What if Mr Pawan Kalyan books an Under-construction property by paying Rs 10 Lakhs to a builder. He gets a ‘Flat allotment letter’ after paying the booking advance. But, the property is yet to be registered in his name. He then decides to re-sell it before taking the possession / registering it. In this scenario, as the property is not yet Registered, how to calculate the holding period? On what basis the holding period and capital gains can be calculated? – Let’s discuss….

How is Holding Period calculated on sale of an Under-Construction Property?

Capital gains on transfer of property has always been a reason for dispute between the taxpayers and IT authorities. While the Income Tax Act mentions that the period of holding determines the amount of tax payable, it does not clearly specify from when the period of holding actually starts.

Does it start from the date of allotment (or) from the day the sale deed is signed or when a property is registered?

Though there are certain ambiguities related to the calculation of holding period for an under-construction property, there have been several court judgments in different cases. The biggest question (as mentioned above) pops up while calculating holding period — whether it has to be calculated from the date on which the property was booked (or) agreement has been done (or) date of registration (if any) or its possession date.

As per the Supreme Court order, the Date of registration (Title Deed/Sale Deed) should be considered as date of acquisition while calculating the holding period and Capital Gains.

In some cases, the Registration might not have happened (or) the property might have been kept for re-sale during its under-construction period. Let’s consider these cases different scenarios…

Scenario – 1

Let’s say you have booked a Flat by paying the required down-payment or initial booking amount on 1st April, 2014. The builder then issued you an Allotment letter on the very same day. The builder and you enter into an Agreement of Sale on 1st May, 2014. The property is still under-construction and you decide to re-sell it to some other buyer. The re-sale (with gains) happened on 1st March, 2018.

Under this scenario, once you pay a booking amount, the builder might allocate a Flat in your name and issue an ‘Allotment Letter’ to this effect. In such a case, the holding period can be calculated from the Date of Allotment of property.

In this example, the holding period is more than 2 years (2018-2014), hence the capital gains made by you are treated as Long Term Capital Gains.

Kindly click on the below image to download the IT Tribunal order and various High-court judgements on this matter.

There can be instances where, the builder can clearly state in the Allotment letter that it does not confer you any ownership right. In such circumstances, the date of Agreement can be considered for holding-period calculation.

Scenario – 2

Let’s say you have booked a Flat by paying the required down-payment or initial booking amount on 1st March, 2016. The builder then issued you an Allotment letter on the very same day. The builder and you enter into an Agreement of Sale on 1st May, 2016. You have paid all the installments to the builder and also received the possession certificate from them. But, you are yet to get the Registration done in your name. Meanwhile, you decide to re-sell it to some other buyer. The re-sale (with gains) happened on 10th March, 2018.

Under this scenario, if you consider ‘Date of possession’ for holding period calculation then your capital gains fall under Short term capital gains and you have to pay taxes based on your income tax slab rate, which can be a hefty amount.

Even in this case, you can consider ‘Date of allotment‘ for calculation of holding period and your capital gains can then become Long Term Capital gains, as your holding period is more than 2 years on date of re-sale (2018-2016).

Below is the High court judgement on ‘Date of Allotment’ Vs ‘Date of Possession’ scenario ;

A word of advice : ‘If you want to sell your under-construction property, try to sell it before taking the possession, and only if the period is more than two years.’

Scenario – 3

Let’s say you have booked a Flat by paying the required down-payment or initial booking amount on 1st March, 2014. The builder then issued you an Allotment letter on the very same day. The builder and you enter into an Agreement of Sale on 1st May, 2014. You have paid all the installments to the builder and the Registration in your name has been done on 1st March, 2016. The possession certificate has also been issued by them on 1st March, 2017. You then decide to re-sell it to some other buyer. The re-sale (with gains) happened on 10th March, 2018.

This can be a trick one! Under this scenario, you can consider ‘Date of Registration’ for holding period and capital gains calculations purposes. If the registration date is used then holding period is long-term and in case, you use the possession date then your gains can be considered as short-term capital gains.

Some experts may argue that the ‘allotment date’ can be considered instead of the ‘registration date’. This is where , you can find conflicting judgement orders given by the honorable Supreme court and IT Tribunals / High courts.

How to calculate Capital Gains on sale of property AY 2024-25?

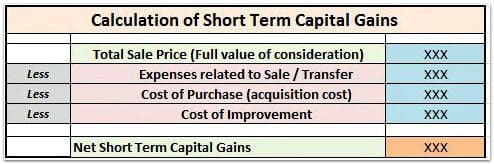

Once you classify your capital gains (based on holding period) as either STCG or LTCG, you can then try calculating the net STCG or LTCG as shown below;

Short Term Capital Gains Calculation is calculated as below:

STCG = Total Sale Price – Cost of acquisition – expenses directly related to sale – cost of improvements.

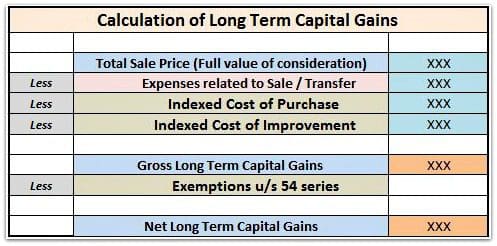

Long Term Capital Gains Calculation;

The LTCG calculation is similar to STCG. The only differences are, you are allowed to deduct Indexed Cost of Acquisition/Indexed Cost of Improvements from the sale price and also claim certain exemptions to save capital gains tax.

In case you acquire a property, which was under construction at the time of allotment and payments were made in installment basis then any payments made before allotment is to be provided indexation from the date of allotment and any payment made after is to be provided benefit of indexation from the date the payment is made.

With effective from Financial Year 2017-18, the base year for calculation of Indexation is going to be 2001.

(Indexation is done by applying CII – cost inflation index. This increases your cost base ie purchase price and lowers your gains. Your purchase price is adjusted for the impact of inflation.

How do you calculate the indexed cost of purchase? The indexed cost is calculated with the help of a table of cost inflation index.

Divide the cost at which you purchased the Property by the index as on the date of the purchase. Multiply this by the index as on the date of sale.

For Example : If purchase year is 2011 and year of sale is in Financial Year 2015. Then indexed cost of purchase would be –

Indexed cost of purchase = (Purchase price / 184) * 254.)

Below is the table of Cost Inflation Index numbers, as stipulated by the Income Tax Department. You can take values from the table to compute the indexed or inflation-adjusted cost of acquisition.

| Financial Year | Assessment Year | Cost of Inflation Index (CII) |

|---|---|---|

| 2001-02 (Base year) | 2002-03 | 100 |

| 2002-03 | 2003-04 | 105 |

| 2003-04 | 2004-05 | 109 |

| 2004-05 | 2005-06 | 113 |

| 2005-06 | 2006-07 | 117 |

| 2006-07 | 2007-08 | 122 |

| 2007-08 | 2008-09 | 129 |

| 2008-09 | 2009-10 | 137 |

| 2009-10 | 2010-11 | 148 |

| 2010-11 | 2011-12 | 167 |

| 2011-12 | 2012-13 | 184 |

| 2012-13 | 2013-14 | 200 |

| 2013-14 | 2014-15 | 220 |

| 2014-15 | 2015-16 | 240 |

| 2015-16 | 2016-17 | 254 |

| 2016-17 | 2017-18 | 264 |

| 2017-18 | 2018-19 | 272 |

| 2018-19 | 2019-20 | 280 |

| 2019-20 | 2020-21 | 289 |

| 2020-21 | 2021-22 | 301 |

| 2021-22 | 2022-23 | 317 |

| 2023-24 | 331 | |

| 2023-24 | 2024-25 | 348 |

Applicable Capital Gains Tax Rates on Sale of Property

- Short Term Capital Gains are included in your taxable income and taxed at applicable income tax slab rates.

- Long Term Capital Gains are taxed at 20%.

To get exemption on long term capital gains tax, you can invest in another residential property or in Section 54EC bonds. (Related article : ‘How to save Capital Gains Tax on Sale of Land / House Property?‘)

To sum it up :

- In case you sell a property booked by you before you get it registered or take the possession, the taxability of profits made on such sale will depend on the time interval between your date of booking the property (or) the date of agreement to transfer your right in the under construction property.

- In case, you sell a property booked by you after getting the registration done or taking the possession then the Tax treatment in such case will depend on the facts of the case, as there are conflicting views and court judgements. Hence, it is prudent to consult a legal / tax expert in this regard.

Continue reading :

- 5 ways of transferring your Immovable (or) Real Estate Property

- Income Tax Deductions List FY 2023-24 | Under Old & New Tax Regimes

- Checklist of Important Property Documents in India | Legal Checklist for Property Purchase

- Under Construction House : How to claim Tax deduction on Home Loan Interest payments?

- Long Term Capital Gain Exemptions on Sale of Property & Recent Court Judgments

- How Home Buyers can file complaints against Real estate Builders online? | RERA Act

(Image courtesy of dan at FreeDigitalPhotos.net) (Post published on : 21-March-2018) (Post last updated on : 23-Sep-2023)

Join our channels

Hi Sreekanth i have sold one property and going to construct a new property. I just want to know that the cost of plot will also be included in the cost of new property or not.

Dear Janak,

YEs, its included.

Hi

we have land offered in 2012 in an under-construction township.

We had paid installments as and when they came from the builder till 2014. Till 2014 about 15L was in totality paid. Although, further requests for installments did n;t come after this and we had to sell it in 2022 for exactly same amount to another broker because the land acquisition had not happened till that time.

It seems this is a case of long term capital gain. Although, how do we calculate long term capital gain for this property? Only allotment happened in 2012 but Possession / Registration never happened on it.

Dear Mamta,

Has the property been registered in your name?

You are saying, the property has been sold in 2022?

Thanks Sreekanth

My Scenario is:

– We have land purchased in 2012 in an under-construction township for 22 L.

– Paid installments Till 2014 about 15L was in totality paid. Although, further requests for installments didn’t come because builder couldn’t simply do land acquisition.

– After waiting for many years, I had transferred it (on Affidevit of 100 Rs E-Stamp paper) in 2022 for exactly same amount i.e. 15L. No registeration / No possission / No handover nothing happened till date. Basically, builder was not able to do land acquisition till date.

My questions are:

– This is a case of long term capital gain?

– If Yes, how do we calculate long term capital gain for this property? Only allotment happened in 2012 but Possession / Registration never happened on it.

Dear Mamta,

“In case you sell a property booked by you before you get it registered or take the possession, the taxability of profits made on such sale will depend on the time interval between your date of booking the property (or) the date of agreement to transfer your right in the under construction property.”

In your case, it is Long term capital gains’. But, as you transferred the rights for the same amount, with indexation benefit, you may actually incurred Long term capital loss.

Suggest you to consult a Chartered Accountant in this regard.

Hi Sreekanth, I had purchased a property in Mar 2003 and sold it in Jan ’19. The property was taken at Rs. 570540, and I had also taken an amount of Rs 7 lacs for renovation a few years back. As I have sold the property, want your help to understand that what will be the amount that I am supposed to pay as an Income Tax as there is no plan of re-investment in any property as such. Appreciate your guidance.

Dear rachana,

Under this scenario, you might be realizing Long Term capital gains on this transaction.

You have to deduct the indexed cost price (purchase price) and indexed cost of improvement from the Sale price.

The net Long Term Capital Gains will be taxed at 20%.

You may kindly go through this article @ How to save Capital Gains Tax on Sale of Land / House Property?

Thanks sreekanth

Can you also help as how to calculate indexed cost of improvement?

Dear Rachana,

This article can give you some idea about the calculation part..

You may kindly consult a Chartered Accountant regarding the exact calculations applicable to your case.

Hi Sreekanth,

My spouse and myself have purchased a under-construction property in Nov’17 and registration too done in the same month for our flat. Bank had released the amount as per the progress of the construction. We are in the last phase of the construction (only for our flat whereas other 4 flats are still under slow progress of construction). The builder each time receives the money from bank and absconds for a month without any further progress & only after our continuous push, he makes slight progress and comes back asking money. By mistake, we missed including the clause in the agreement that if he delays construction rent to be payed by him. Kindly provide your suggestions if any to take strict action on him to complete the house as early as possible

Dear Madhu,

Is the project registered under RERA?

Kindly go through these articles, can be useful :

* How Home Buyers can file complaints against Real estate Builders online? | RERA Act

* Real Estate Regulations & Development Act (RERA) | Key points & Review

Hi Sreekanth, thanks for your quick response. Yes, it is registered under RERA. I shall go through the links provided, thanks for your time.

Hi Sir,

I booked a residential apartment in Aug 2012 and allotment letter was given in Nov 2012. I have received Offer of possession in March 2018 and paid all the remaining dues on 12th March 2018. The builder has not yet registered the property in my name and will be done in few more days. I am stuck between the decision to rent it or sell it. Kindly help me regarding following questions.

1) will this property be counted as to be “constructed within 5 years” clause of income tax laws ?

2) If I sell this property after registry within FY 2018-2019, will it be considered as a short term capital gains or a LTCG.

3) Since my employer has already deducted tax from my salary, if I need to get tax benefit on interest paid in loan during 2016-2017 (as it is the year in which possession is offered), I will need to file return with a refund ?

4) Can I get tax benefit on the Prior Period Interest ( from 2012 till March 2017) ?

5) if I sell this property in FY 2018-2019 and had claimed benefit under 24b on interest paid . will I have to return that benefit in the return of FY2018-2019

Thanks a lot in advance.

Best Regards

Dear Dharmesh,

1 – When did you take home loan?

“In view of the fact that housing projects often take longer time for completion, it is proposed that clause (b) of section 24 be amended to provide that the Deduction under the said provision on account of Interest paid on Home Loan for acquisition or construction of a self-occupied house property shall be available if the acquisition or construction is completed within FIVE years from the end of the financial year in which capital was borrowed.

This amendment will take effect from 1st day of April, 2017 and will, accordingly apply in relation to assessment year 2017-2018 and subsequent years.”

2 – If you sell the property immediately after the Registration (in FY 2018-19) then you may have to consider it STCG (however this can be subjective).

3, 4 & 5 – Have you accepted the offer of PC? If the property is not yet registered in your name, I believe you may not be eligible to claim tax benefits.

Kindly consult a CA.

i book flat in 2011 builder block ,didnt build it and 2015 5 oct he trasfer my funds in to new building and i got possetion in new building on 12 feb 2018 and sold same property with final payment 29 march 2018.so whether it is stcg or ltcg

Dear Neha,

It is LTCG, as the holding period is more than 2 years..

Related articles :

* How to save Capital Gains Tax on Sale of Land / House Property?

* Long Term Capital Gain Exemptions on Sale of Property & Recent Court Judgments

in case of under construction property being sold before registeration. The total purchase value of the property has to be taken for indexation (as per allotment letter date) or the installment amounts need to be indexed individually

thanx

manoj sharma

Dear manoj,

In case you acquire a property, which was under construction at the time of allotment and payments were made in installment basis then any payments made before allotment is to be provided indexation from the date of allotment and any payment made after is to be provided benefit of indexation from the date the payment is made.

thanx a lot dear

Hi Sir,

I have query regarding to take the benifit on home loan interest in Incometax . How much I will take the benifit? Pls, do the needful for the same.

Thanks in advance.

Dear Avadhesh,

The maximum that can be claimed as loss under the head ‘income from house property’ is Rs 2 Lakhs.

Kindly read :

Income from House property & tax implications!

Income tax deduction list FY 2018-19

Thanks a lot for the valuable replay.

Hi Sreekanth,

What would happen in a scenario where I have sold a residential house and then bought a plot of land to construct a house? When i buy the land, it will be registered, but does this date count for purpose of calculating holding period? Or do we have to get some sort of completion certificate from any authority for construction of house to calculate holding period?

Dear Sandeep,

The registration date of ‘buying plot’ can be considered as the date of purchase and holding period can be calculated from that date.

Your propositions for calculation of Capital gains are right but You have to calculate with examples and solve the prob,ems ,than, it would be better for general investors

Dear Hrishikes,

Thank you for the suggestion!

Will try to publish one more article with solved examples!