LIC has launched 7 new plans in 2017. In this post I have tried to list down the important features, details and my recommendations on all LIC New Plans that are launched in 2017-18.

From January 2017 to December 2017, LIC has launched two Endowment plans, one Single Premium Traditional plan, one Whole-life plan, a Cancer specific Insurance plan and two Money-back plan. These new plans are namely; LIC Aadhaar Stambh, LIC Aadhaar Shila, Jeevan Utkarsh, Jeevan Umang, LIC Cancer Cover , LIC Jeevan Shiromani & LIC Bima Shree Plan.

Before discussing more on the LIC New Plans list, let us understand more about the different types of Traditional Life Insurance plans.

What is an Endowment plan? – It is a combination of insurance and investment. The insured will get a lump sum along with bonuses (if any) on policy maturity (or) on death event.

What is an ‘Whole-Life Insurance Plan’? – It is a life insurance policy which is guaranteed to remain in force for the insured’s entire lifetime. The Sum assured is paid to the Policyholder’s nominee in the event the insured dies.

What are Money-back policies? – They provides life coverage during the term of the policy and the maturity benefits are paid in installments by way of Survival Benefits (money-back payments).

What are Limited Premium Payment Insurance Plans? – A limited premium payment plan is a plan where you pay the premium for a shorter span of time and enjoy the benefits of an insurance cover for a long time.

What is a Single Premium Plan? – It is the insurance policy where you pay insurance only in the first year but continue to enjoy the life cover and other plan related benefits throughout the term of the policy.

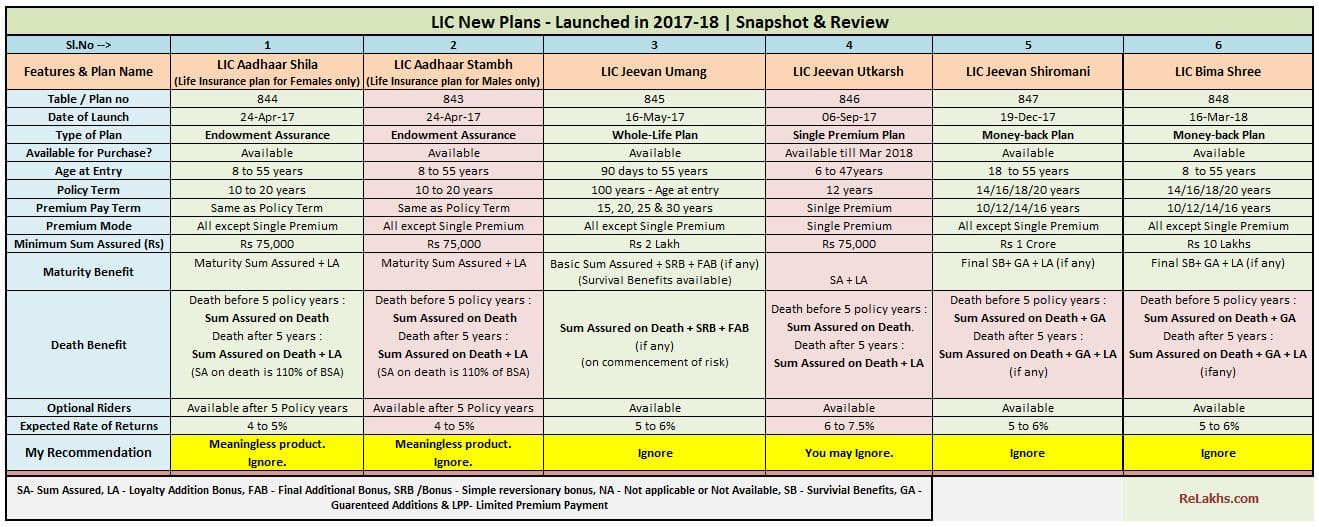

LIC New Plans list – Launched in 2017 – Snapshot & Review

I have listed down the important features of LIC of India’s new plans that are launched in 2017 along with my recommendations (whether to ignore a plan or to buy).

(Click on the image to open it in a new browser window)

LIC Aadhaar Stambh Plan

- Aadhaar Stambh plan was launched in April, 2017. LIC claims that Aadhaar Stambh life insurance policy has been exclusively designed for Male lives who are having Aadhaar card.

- LIC Aadhaar Stambh plan is a typical with profit, non-linked regular premium paying Endowment assurance plan.

- The maximum sum assured offered under this plan is Rs 3 lakh only.

- I believe that LIC has launched this new plan keeping in view of the popularity of the word ‘Aadhaar’. I believe that there are no ‘exclusive’ features in this insurance policy for Male lives and can be ignored in case your requirement is to get adequate life insurance cover.

- In case, you have already invested in this plan, suggest you to let it lapse (if you stop paying future policy premiums, policy will automatically get lapsed).

- For complete details on this plan, kindly visit this link – ‘LIC Aadhaar Stambh (Life insurance plan for Males) – Features, Benefits and Review.’

LIC Aadhaar Shila plan

- Aadhaar Shila plan was launched in April, 2017. LIC claims that Aadhaar Shila life insurance policy has been exclusively designed for Female lives who are having Aadhaar card.

- Like Aadhar Stambh plan, LIC Aadhaar Shila plan is also a typical with profit, non-linked regular premium paying Endowment assurance plan.

- The maximum sum assured offered under this plan is also Rs 3 lakh only.

- In case, you have already invested in this plan, suggest you to let it lapse.

- For complete details on this plan, kindly visit this link – ‘LIC Aadhaar Shila Plan – Review.’

- If you are looking for lower Sum-assured and low cost life insurance plan, you may look at ‘Pradhan Mantri Jeevan Jyoti Bima Yojana – Govt’s Life Insurance Scheme‘.

LIC’s new Plan – Jeevan Umang

- LIC launched this new Whole-Life plan in May, 2017.

- This new plan from LIC is a traditional, non-linked, with-profits, Whole Life Assurance and Limited Premium Payment Option plan.

- The main feature of LIC’s New plan – Jeevan Umang is it provides annual Survival Benefits from the end of the PPT (Premium Paying Term) till policy maturity and also pays lump sum amount at the time of maturity (or) on death of the policyholder (during the policy tenure).

- The Maturity benefit under this plan is Basic Sum Assured + Simple Reversionary Bonuses + Final Additional Bonus (if any) shall be payable to the policyholder on surviving to the end of the policy term.

- Death Benefit is defined as sum of “Sum Assured on Death” and vested simple reversionary bonuses and Final Additional Bonus, if any shall be payable to the Nominee.

- The expected returns from Jeevan Umang can be around 5% to 6%.

- If you have already invested in this policy, you may let it lapse (if your requirements are higher life cover and decent returns on maturity).

- If you are planning to buy this plan, ignore it.

- For more details on this plan, kindly visit this link – ‘LIC Jeevan Umang – New Whole Life Plan | Features, Illustration & Review‘.

LIC’s new Single Premium Plan – Jeevan Utkarsh

- LIC has launched Jeevan Utkarsh plan in Sep 2017.

- This new plan from LIC is a traditional, non-linked, with-profits, savings cum protection plan.

- This plan is available for purchase till 31st March, 2018.

- The expected returns on this plan can be around 7%. But do remember that the returns are highly dependent on the bonus rates that LIC declares every year. (Read : ‘LIC’s latest Bonus rates 2017-18‘)

- If you are planning to buy this plan for life cover, you may ignore it.

- For more details on this plan, kindly visit this link – ‘LIC Jeevan Utkarsh – Features, Review & Returns Calculation‘.

LIC Cancer Cover Plan

Besides the above four new plans, LIC has also launched a Cancer specific insurance plan namely – LIC Cancer Cover. It is very tough to provide generic suggestions on Health-oriented insurance plans. My suggestion would be to maintain seperate Emergency Fund for medical expenses, maintain a Mediclaim cover (individual/family floater) and can consider adding one Super-Top health-cover to it. If you have already planned for these things (or) if your family’s medical history is not that good, you may consider buying a Critical Illness / Illness specific cover(s). Kindly compare the health plans offered by other insurers and then take a prudent decision. (Read : ‘What are Super-Top up Health Insurance plans‘)

LIC Jeevan Shiromani – New Moneyback Plan (Plan 847)

- LIC has launched Jeevan Shiromani plan in Dec, 2017.

- Jeevan Shiromani is a Non linked, Money back, Limited premium payment with guaranteed additions plan. This plan is specifically designed for HNIs (High Net-worth Individuals).

- The expected returns on this plan can be around 5 to 7%. But do remember that the returns are highly dependent on the LA rates.

- For more details on this plan, kindly visit this link – ‘LIC Jeevan Shiromani – New Moneyback Plan | Features, Review & Returns Calculation.’

LIC Bima Shree Plan

- LIC has launched Bima Shree plan in Mar, 2018.

- Bima Shree is a Non linked, Money back, Limited premium payment with guaranteed additions plan. This plan is specifically designed for HNIs (High Net-worth Individuals).

- The expected returns on this plan can be around 5 to 6%. But do remember that the returns are highly dependent on the LA rates.

- For more details on this plan, kindly visit this link – ‘LIC Bima Shree – New Moneyback Plan | Features, Review & Returns Calculation.’

Pradhan Mantri Vaya Vandana Yojana

- Though PMVVY has been launched by the Central Govt, LIC is the exclusive administrator of this scheme. One can purchase this scheme offline as well as online through Life Insurance Corporation (LIC) of India which has been given the sole privilege to operate this Scheme.

- PMVVY is a Pension scheme for Senior citizens who are above 60 years of age. The assured return on PMVVY would be 8%.

- The plan is open for subscription from 04-May-2017 to 03-May-2018.

- One time premium payment of Rs 7,22,892/- would give a monthly pension of Rs 5000 (maximum). Below are the premium (purchase price) and pension details of PMVVY Scheme;

- For more details, you may kindly read my review on PMVVY scheme.

My standard suggestions :

- Returns : Are you investing in these kind of plans for maturity returns? – The traditional life insurance plans can offer returns in the range of 4 to 7%. Personally, I believe that this is a very low return on investment, considering the fact that one has to remain invested for 10+ years. So, unless you are content with low returns and also have adequate life cover, these kind of conventional insurance plans may not be for you. (Read : ‘Traditional life insurance plan – a terrible investment option?‘)

- Life insurance cover : Are you investing in these kind of plans for insurance cover? – The main point to note here is, ‘quantum of life cover’. These kind of plans are very costly to get high sum assured. So, if your requirement is to get adequate life cover, affordable Term insurance plans are the right choice.

- Tax Saving : Are you investing in these kind of plans for tax saving under section 80c? – if that’s the case, even a long term Small Savings Scheme like PPF (Public Provident Fund) can be a better choice than traditional life insurance plan. (Read: ‘PPF + Term plan Vs Traditional life insurance plan‘). You can also consider investing in ELSS tax saving mutual funds for long-term goals.

Generally, December to March is the peak season for the life insurance companies in India. Most of the life insurance plans are offered as ‘tax-saving cum investment’ schemes. So, kindly be aware of the pros & cons of the financial products before you invest.

Continue reading related articles :

- LIC New Plans 2019-2020 | Features, Snapshot & Review of all the Plans

- If Life is unpredictable, Insurance can’t be optional!

- Traditional Life Insurance plans – a terrible investment option?

- How to link Aadhaar to LIC policies?

- How to get rid-off unwanted Life insurance policies?

- Is buying a Term life insurance plan a waste of your money?

- Best Term Insurance plans

(Featured Image courtesy of bplanet at FreeDigitalPhotos.net) (Post published on : 15-December-2017)

Join our channels

Great one ……

Hi Sreekanth,

Just wanted to know if we surrender the policy after 5 years (21 year term plan) then the amount we get is taxable?

Regards,

Anchit

Dear Anchit.. Is there any maturity benefit / return of premium under the mentioned term policy?

No, it wont be taxable.

Kindly read : 7 ways you could lose your Income Tax Benefits

Is there any LIC Endowement/Moneyback plan worth considering ?

Or all the plans are low returns-high premium-long lock in products?

Dear sankalp,

Generally the traditional life insurance plans (offered by any insurer) can at best provide returns of around 4 to 6%.

Let’s not try to mix Insurance and investment together.

If adequate life cover is required, Term plan can be considered. Else, for long-term goals, there are plenty of other investment alternatives.

Wise analysis and advice…..

Thank you! Keep visiting ReLakhs ..

Dear Sreekanth,

very well and nicely written blog. Regarding LIC Cancer Care, I personally feel that it is MUCH BETTER plan when compared to similar existing cancer care policies in the market at present. The Premium they charged is reasonable when compared to other companies, also the EXCLUSION CRITERIA AND WAITING PERIOD clause is much better than other similar policies in market (compared to HDFC cancer care and ICICI cancer care, Max cancer plan). As you know, Cancer treatment is very expensive and with mediclaims and by creating EMERGENCY FUNDS, the expenses may not be met fully. (recently a Delhi hospital charged 1 crore for a liver cancer treatment, treated with liver transplantation).

regards

RAJ

One main POSITIVE thing i noticed in LIC cancer care is, it charges very less to females of the same age group when compared to other existing cancer care policies. For Ex,

a 40 year old female if she wants to buy cancer care of 20 Lalk, premium paid is least in case of LIC which is not the case in other policies like HDFC/ICICI/MAX. This is the best advantage, because females are more at risk when compared to males at 40-50 age group.

Dear Raj,

Thank you for sharing your views and valuable information on LIC cancer care plan.

However my point is, having an emergency fund+Mediclaim is must. One has to first plan for this and then can surely consider a critical illness plan (if required).

Fully agree with your openion

regards

RAJ