LIC is proposing to launch its new MONEY-BACK plan called LIC Bima Shree (Plan no.848) on 16th March, 2018. Bima Shree is a Non linked, Money back, Limited premium payment with guaranteed additions plan.

This plan is almost similar to LIC’s recently launched plan i.e., Jeevan Shiromani.

What are Money-back policies? – They provides life coverage during the term of the policy and the maturity benefits are paid in installments by way of Survival Benefits (money-back payments).

What are Limited Premium Payment Insurance Plans? – A limited premium payment plan is a plan where you pay the premium for a shorter span of time and enjoy the benefits of an insurance cover for a long time.

Basic Features of LIC Bima Shree Plan

Below are the eligibility conditions for Bima Shree Policy ;

- Minimum Age at entry : 8 years

- Maximum age at entry : 55 years for 14 years policy term (PT), 51 for 16 PT, 48 for 18 & 45 for 20 PT

- Minimum basic sum assured (BSA) : Rs 10 Lakh

- Maximum basic sum assured (BSA) : No Limit

- Policy term and premium paying term : PPT = Policy Term – 4 years

- For a 14 year Policy -> PPT is 10 years

- 16 year Policy -> PPT is 12 years

- For a 18 year Policy -> PPT is 14 years

- For a 20 year Policy -> PPT is 16 years

- Guaranteed Additions under Bima Shree Plan;

- Guaranteed Addition for first 5 policy years is Rs 50 per Rs 1,000

- From 6th Year onwards, GA is Rs 55 per Rs 1,000.

- Settlement option for the death benefit and survival benefit available.

- The policyholder can receive the settlement amount, it can be either death (nominee will receive death benefit), survival benefit (or) maturity benefit, in installments over the chosen periods like 5 years, 10 years or 15 years (or) in the form of one-time lump sum payment.

- The policy is eligible for Paid-Up and Surrender after the completion of two policy years.

- Optional riders like Accidental Death and Disability Benefit, Critical Illness Benefit etc., are available.

Benefits under LIC’s new Bima Shree Plan

Below are the benefits under Bima Shree Money-back plan;

- Death Benefit : Under this new plan, the risk commences immediately on issuance of Policy.

- If the insured dies within 5 years : Sum assured (SA) + Guaranteed Addition (GA) is payable to the nominee.

- If the insured dies after 5 years : Sum assured (SA) + Guaranteed Addition (GA) + Loyalty Addition (LA) is payable to the nominee.

- Meaning of “Sum Assured on Death” is defined as HIGHER of the below.

- 10 times of your annual premium (excluding taxes, the extra amount due to underwriter decisions or rider premium).

- 125% of Basic Sum Assured.

- 105% of all the premiums paid as on date of death.

- Survial Benefits (or) Money-back options under Bima Shree Policy;

- For 14 year Policy : 30% of Sum-assured is payable in 10th & 12th policy year and the remaining 40% is payable after the 14th year.

- For a 16 year policy : 35% of SA in 12th & 14th year and the remaining 30% is payable after the 16th year.

- Under 18 year policy : 40% of SA in 14th & 16th year and the remaining 20% of SA is payable after the 18th year.

- For a 20 year policy : 45% of SA in 16th & 18th year and the remaining 10% of SA is payable after the 20th year.

- Maturity Benefit : After completion of the policy term, the remaining sum assured (Sum Assured excluding survival benefits already paid) along with Guaranteed Additions and Loyalty Additions (kindly note that Loyalty Additions are payable after five policy years only) is payable to the life assured.

LIC Bima Shree – New Money Bank Plan – Graphical Illustration

Below is the graphical illustration of Bima Shree Plan (20 year term).

- For a 20 year policy, the Premium paying term would be 16 years.

- 1st Survival benefit of 45% of Basic Sum Assured is payable in 16th year and 2nd SB in 18th year.

- Guaranteed Additions at the rate of Rs 50 p.a. per Rs 1,000 Sum Assured is payable for the first five policy years. Form 6th year till 20th year, GA @ Rs 55 p.a. per Rs 1,000 SA is payable on maturity/death of the policyholder.

- If death occurs during the first five years, death benefit of Sum assured on death + accrued Guaranteed Additions is payable to the nominee. In case, death occurs after 5 years, death benefit = SA + GA + Loyalty Addition is payable.

- After 20 years, the maturity benefit would be equal to 10% of BSA + accrued GAs + LA is payable.

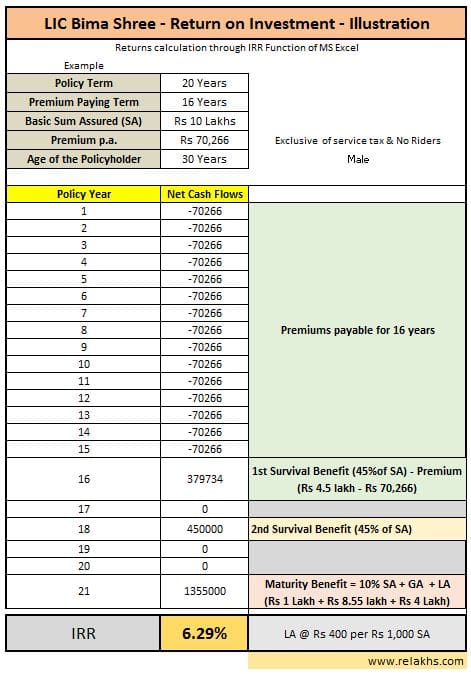

LIC’s New Moneyback Bhima Shree Plan – Returns Calculation

Let’s calculate the IRR (Internal Rate of Return) of a 20 year LIC New Bima Shree policy.

Let’s calculate the IRR (Internal Rate of Return) of a 20 year LIC New Bima Shree policy.

- The applicable premium rate for a 30 year male is around Rs 70,266 for Basic Sum Assured of Rs 10 lakh.

- The Survival Benefit of Rs 4.5 Lakh is payable in 16th and 18th year. The 3rd SB of 10% BSA is payable on maturity.

- The total accrued amount in the form of Guaranteed Additions on maturity would be around Rs 8,55,000.

- I believe that we can assume Loyalty additions in the range of Rs 200 to Rs 400 per Rs 1,000 Sum assured.

- In case, we take LA rate as Rs 400, the LA amount on maturity is around Rs 4 Lakh, payable at the end of 20th year.

- So, Maturity benefit is equal to Rs 13,55,000 and the return on investment is around 6.29%.

- If we consider LA at the lower end i.e., Rs 200, the IRR falls to around 5.53%.

My opinion on LIC Bima Shree

- High Sum Assured & High Cost plan : The minimum Basic Sum Assured under this plan is Rs 10 Lakh. The premium rate to get Rs 10 lakh for a 30 year male is Rs 70,266 per annum. So, the main target clients for this plan can be High Net-worth Individuals only.

- No Compounding Factor : Kindly note that the Guaranteed Additions are not paid to you immediately. They are accrued and paid on maturity or death claim only. Compounding is not done. Also, they are payable till Premium Paying term only and not for the entire policy term. On a 20 year plan, guaranteed additions are payable till the end of 16th policy year only.

- Loyalty Additions : Do note that LA is not applicable if death happens during the first 5 policy years. Also, the GA rate is Rs 50 per Rs 1000 SA in the first five years of policy term.

- Return on Investment : Under this plan, the returns are mainly dependent on the LA amount. I have noticed that even most of the LIC agents have no clarity on the LA rates. As this plan has Guaranteed Additions, I strongly believe that LIC may declare lower LA rates. If we consider LA of Rs 50 per Rs 1,000 sum assured the return on investment can be around 4.91%. In case, we assume LA of Rs 400 then RoI comes around 6.29%. In any case, it is clear that returns can be in the range of 5% to 6%.

- Tax benefit under Section 80c : I believe that most of the HNIs might have adequate investments in their kitty, to claim tax deductions of up to Rs 1.5 Lakh u/s 80c. Also, the premium under this plan is going to be more than the limit of Rs 1.5 Lakh. So, the entire premium amount can not be claimed as tax deduction.

- What do you expect from your Life Insurance plan?

- Adequate Life cover : If your priority is to get adequate life cover at cheaper premium rates then you can buy a Term insurance plan. A 30 year policy holder (non-smoker) can buy an e-Term insurance policy from LIC itself with a life cover of Rs 50 Lakh by paying a premium of Rs 7,812 p.a. for 30 years. (Read : ‘Best Term Life Insurance plans‘)

- High Investment Returns: As an HNI, if you can afford to take risk and would like to multiply your wealth then there are plethora of other investment options. If you would like to invest in this plan for decent Returns then you may be up for a disappointment.

- Are you content with 5 to 6% returns? – In case, you are an HNI with adequate Life cover, believe that you have enough exposure to risk-oriented investment products and content with returns of around 5% over a period of say 15 to 20 years then you can consider investing in LIC Bima Shree plan.

Continue reading :

- LIC New Plans 2019-2020 | Features, Snapshot & Review of all the Plans

- LIC’s latest Bonus Rates 2017-18

- LIC Jeevan Shiromani Plan – Review

- How to link Aadhaar to LIC policies online/offline?

- Traditional Life Insurance plan – a terrible Investment option?

The above details are based on the limited available information available with us. If required, the details provided in this post will be modified.

(Post published on : 15-March-2018)

Join our channels

Dear Sreekanth,

I am a Close follower of your Blog for various Finance decisions and Knowledge base.

I Need Your inputs/Views regarding SBI Wealth Builder. Plz provide if possible and your time permits.

Thanks again for your wonderful blog.

Dear Rajesh,

SBI Wealth Builder is an ULIP.

Have you already invested in this plan? May I know your investment objectives and time-frame??

Hi Sreekanth,

Think there is no inbuilt critical illness benefit under this plan.

Needs to be purchased as a rider. Can you please recheck?

Dear Deepesh,

Yeah, this plan is a mini-version of Jeevan Shiromani!

Critical Illness is available as an optional rider at the inception of the policy, I have corrected the mistake…Thank you!

Hi Sreekanth,

Isn’t this exactly the same plan as LIC Jeevan Shiromani? 🙂

Guess only the minimum Sum Assured has been reduced to Rs 10 lacs.