Year 2014 saw lot of changes in the Indian Insurance industry. IRDA (Insurance Regulatory & Development Authority) had implemented a slew of changes with respect to insurance regulations. These changes were applicable to both traditional (endowment/moneyback) and Unit Linked life insurance plans.

Some of the changes were related to minimum death benefits, guaranteed surrender value, use of new mortality table (for fixing premiums) etc., All Insurance companies had to abide to these new regulations with effective from 01-Jan-2014.

LIC (Life Insurance Corporation of India) had hence withdrawn all its popular plans by the end of 2013 and had to launch all new traditional plans throughout 2014. I tried to compile “LIC 2014 new plans list” in this article. I have provided the basic features of all new LIC policies that were launched in 2014. I have also given my recommendation on all these plans.

LIC had launched 14 new plans in 2014-2015. Five LIC Endowment plans, Four LIC Moneyback plans, Four LIC Term Insurance Plans and One Pension oriented plan.

( Endowment plan is a combination of insurance and investment. The insured will get a lump sum along with bonuses (if any) on policy maturity or on death event.

Money-back policies provides life coverage during the term of the policy and the maturity benefits are paid in installments by way of survival benefits.

In Term Plan which is a pure insurance there is no maturity benefit. It means if a person dies during the term of policy then only his beneficiaries will get some money otherwise at maturity, at the end of the term there is no benefit)

Below is the list of latest LIC policies that were launched during 2014 to 2015 :

- LIC Single Premium Endowment Policy (Plan/Table no 817) : This plan was launched on 1st January,2014. It is an endowment policy. The main feature of this policy is that you pay single premium and the risk coverage is available through out the policy term. Maturity Benefit under this policy is the addition of Sum Assured, Simple reversionary bonus and Final Additional bonus. The expected returns from Single premium endowment policy can be in the range of 4% to 6%. My view is that you can ignore buying this policy. (Date of Commencement of risk under this plan:In case the age of Life Assured at entry is less than 8 years, risk under this plan will commence either 2 years from the date of commencement or from the policy anniversary coinciding with or immediately following the attainment of 8 years of age, whichever is earlier. For those aged 8 years or more, risk will commence immediately)

- LIC New Endowment Policy (Plan/Table no 814) : This plan was launched on 3rd January, 2014. It is also an endowment policy but not a single premium plan. This plan has accidental death and disability benefit as an optional rider. The returns from this new endowment policy too can be in the range of 4% to 6%.

- LIC New Money Back Plan (Plan/Table no 820) : This plan was launched on 6th January, 2014. The main feature of this plan is limited premium paying term. The policy term is 20 years and the premium paying term (PPT) is 15 years. You can get Survival Benefits of 20% of Sum Assured (as money back amounts) at the end of 5th, 10th and 15th policy year. The expected returns can be around 5% to 6%.

- LIC New Money Back Plan (Plan/Table no 821) : This is a similar money back plan like the above one. The policy term is 25 years in this plan and PPT is 20 years. Maturity benefit under plan no 821 is the addition of 40 % of sum assured plus Bonuses and Final Additional bonus (FAB, if any).

- LIC New Bima Bachat (Plan/Table no 816) : New Bima Bachat plan was launched on 7th January, 2014. This is a money back plan. This plan offers 3 policy terms (9/12/15 years). It is a single premium payment plan. The expected returns can be in the range of 4% to 6% from New Bima Bachat plan.

- LIC New Jeevan Anand (Plan/Table no 815) : New Jeevan Anand plan was launched on 8th January,2014. This is an endowment cum whole-life plan. This is a modified plan of old Jeevan Anand plan, one of the popular plans of LIC. Death Benefit under New Jeevan Anand is ‘higher of 125% of Sum Assured )or) 10 times of annual premium paid. In addition to this, death benefit also includes ‘Accrued simple bonuses.’ This death benefit is payable if unfortunate event happens during the policy term. If death happens after the policy term (whole life), death benefit includes Basic Sum Assured along with vested simple reversionary bonus and FAB. This is one of the better plans of LIC. But I still suggest you not to mix insurance with investment.

- LIC Anmol Jeevan II (Plan/Table no 822) : This is an offline Term insurance plan from LIC. The maximum sum assured offered under Anmol Jeevan II is Rs 24 Lakh.

- LIC Amulya Jeevan II (Plan/Table no 823) : This is an offline Term insurance plan with higher minimum sum assured of Rs 25 Lakh. No optional riders are available under Amulya Jeevan. Before buying Anmol Jeevan or Amulya Jeevan, you can compare the premiums of other offline term insurance plans offered by other insurance providers.

- LIC e-Term Plan (Plan/Table no 825) : LIC has launched its online Term insurance plan on 17th May, 2014. LIC was a late entrant with respect to the launch of online term plans. But one good point about e-term plan is that is about 35% cheaper than Anmol Jeevan/Amulya Jeevan (LIC’s offline term plans). However, when you compare the premiums of LIC’s e-term plan with private insurance players’ online products, you may find it bit costly. But, LIC has the highest claim settlement ratio among the life insurers. You can surely consider buying LIC e-Term plan.

- LIC Jeevan Rakshak (Plan/Table no 827) : Jeevan Rakshak plan was launched by LIC on 19th August, 2014. This is a traditional endowment policy. ( You may visit my article on ” Detailed analysis on LIC Jeevan Rakshak.”)

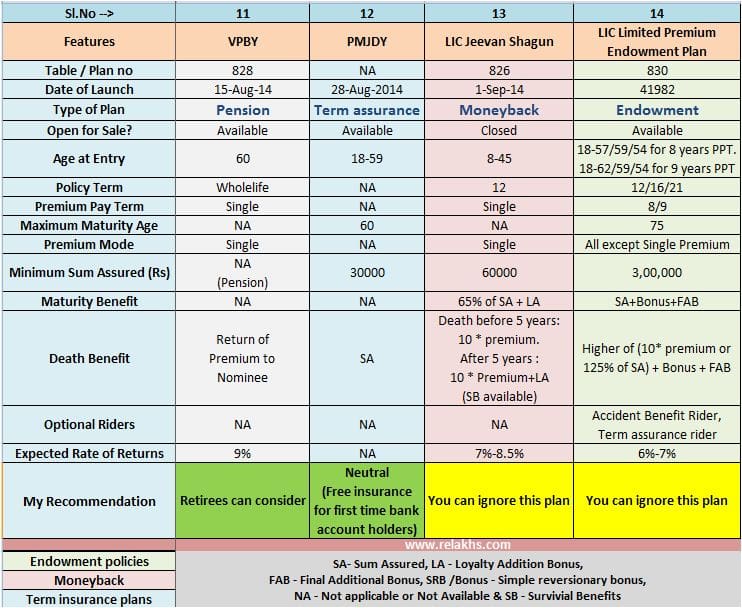

- LIC Varishtha Pension Bima Yojana (Plan/Table no 828) : VPBY is launched by the Government of India. LIC is an exclusive administrator of this Varishtha pension plan. ( You may visit my post on “VPBY-review” for more details)

- LIC & Pradhan Mantri Jan Dhan Bima Yojana : Government launched this financial inclusion programme on 28th August, 2014 to encourage people to open bank accounts. PMJDY Scheme offers Rs 30,000 as free term insurance coverage for the first time bank account holders. LIC will provide the life cover under PMJDY scheme from 26th January,2015. Life cover is available for the Jan Dhan Bank Account holders who have opened accounts between Aug 2014 to 26th Jan, 2015 only. ( For more information you may visit my post on “PMJDY & Life insurance coverage details“)

- LIC Jeevan Shagun (Plan/Table no 826) : Jeevan Shagun is a money back plan. This plan was open for sale for limited duration only. Jeevan Shagun is a single premium plan. The expected returns on this plan can be around 7% to 8.5%. (Visit my post for detailed analysis on “LIC Jeevan Shagun – Review & Return Calculation“)

- LIC Limited Premium Endowment Plan (Plan/Table no 830) : This is a limited premium payment plan. You pay premium for limited period and can get insurance coverage for the entire policy term. The available policy terms under this plan are 12/16/21 years. Premium paying Terms options are 8/9 years. ( You may like visiting my post on “LIC Plan no 830 – Features & Review“) ( or you can visit another article on this plan “ LIC Limited Premium Endowment plan offers Limited Returns“)

LIC 2014 new Plans list – Snapshot

I have listed down the basic features of LIC of India’s new plans that were launched in 2014 along with my recommendations (whether to ignore a plan or to buy). (Click on the images to enlarge or open in a new browser window).

LIC Plans 1 to 5..

LIC Plans 6 to 10..

LIC Plans 10 to 14..

( To know and understand more about various types of bonuses, you may visit my post on LIC’s latest Bonus rates 2014-2015)

Be careful while buying Single premium plans. Generally the maturity benefits (like money-back payments, policy maturity amounts) of Life insurance plans are tax free. You are entitled for a tax free maturity/death benefit under Section 10 (10D) only if the minimum sum assured throughout the policy term remains 10 times the single premium paid. The tax benefit under Section 80 C is available only if the annual premium is at least 10% of the sum assured. Regular premium plans may pass this criteria but some single premium plans may not meet this criteria.

You may or may not have bought any of these LIC plans. If you want to invest in any of them, you can analyze my reviews and consider taking decisions accordingly.

In case you have already invested/bought any of these LIC plans and are not happy with your investment decision then you can either SURRENDER your policy or can make them (it) PAID-UP. My suggestion would be to make these unwanted endowment or money-back plans LAPSE, as these plans were launched during the last one year only. You may buy a Term plan from LIC itself and invest the saved premium in other investment options (like mutual funds, bank fixed deposits etc., depending on your financial goals).

If you have liked this article, do share it with your friends. And do not forget to leave your valuable comments. Cheers!

( Image courtesy of David Castillo Dominici & bplanet at FreeDigitalPhotos.net)

You may visit my post on “how to get rid off bad or unwanted insurance” to know more about PAID-UP and SURRENDER options. You may also visit my post on “Comparison of online Term Insurance Plans” to know more about the best online term insurance plans.

Join our channels

Hi Shreekant Reddy Bro…

it seems like you are working for a private Insurance Company (from all your comments n reviews about LIC product) and they are paying you very heavily for this thing. but still the Plan details you provide is nice n very useful. just want to tell you that people will never buy a policy only for insurance purpose , Specially in India even people wants Maturity Returns in Term Insurance Plans. about LIC, you must share Previous years Death n Maturity Claim settlement comparison Chart of LIC n other Private Players

God Bless You. in all your Works, n gives Wisdom..!!!!!

Dear Jonah,

Thank you for your warm wishes.

Kindly note that I am not associated with any (PSU / Pvt) financial service / product provider.

If people WILL NEVER BUY a policy only for insurance purposes then let’s change their perception & viewpoint, for their good.

For Claim Settlement Ratio : Kindly read this article.

Hi Sreekanth,

I’m Vinod and we are looking for health coverage for parent’s who are 60 yrs (Dad) and 55 (Mom) old. Dad had a heart attack at 27 and now he has no problems, no BP. Mom is in the border of Sugar. Do we take a Health Insurance or Term Insurance ? Could you pls recommend policies for their age with better coverage at the right premium . We are based in Erode a town in Tamil Nadu, so the hospital coverage should be local as well, kindly help, Thanks.

Vinod

Dear Vinod,

You have to consider buying health insurance plans for them.

Kindly read below articles:

Best Portals to compare health insurance plans. (Use coverfox portal to check about the network hospitals for cashless claims in your locality)

Best Health insurance plans for parents/Sr Citizens.

It seems that people in our country do not want to learn basics of life insurance or they are not being educated by the so called financial advisors appointed by Insurance companies.(Since their commission is primarily dependent on traditional plans sold. who cares about financial planning without vested interests?)

For example, LIC boasts of regaining 70% market share recently with launch of new plans. More than 85% share of those are traditional plans where a person neither gets enough life cover nor inflation beating returns. What kind of financial advisory is it?

LIC top officials are also at blame since they only think of traditional plans as once a gullible customer enters into these pathetic plans, he is virtually trapped for a long time since surrender value of these plans in the initial years is nothing to minimal. Its a win-win situation for LIC and its agents at the cost of customers.

Hope the situation will improve in future when people get to know that Insurance means term plan and Insurance and Investment are two altogether different things.

Dear Rupali,

Thank you for sharing thought provoking views.

In India unfortunately, life insurance products are positioned or bought primarily as tax saving products / savings oriented products. Very rarely they are sold / bought for risk-coverage purposes.

Kindly go through the comments shared on one of my articles ” LIC jeevan Tarun“, its very clear how some of the agents (hard-core fans of traditional plans) sell or vouch for traditional plans. Highly misleading, meaningless and non-sense comments.

Appreciate your views, keep visiting 🙂

Dear Srikanth,

I am prabhakar age of 30years and having 2 kids.i am doing marketing job and looking for best risk policy.

request you please suggest and do the needful.

Thanking you

Dear prabhakar,

Buy a Term plan at the earliest. Kindly go through my article : Best Term insurance plans.

Hi Srikanth,

Nice information, i am looking a policy to invest in LIC plz suggest me the best policy for investment purpose so i get high return without risk.

Thanks

Amit Tygai

Dear Amit,

Kindly do not mix insurance with investment. Buy a term plan for life insurance cover.Also, you go to take risk to get high returns 🙂

Kindly read my articles:

Best term insurance plans

Term insurance Vs traditional plans

The 6 most common presonal finance mistakes

Dear sir,

Greetings

I am 22 years old give me idea about best lic scheme duration 5 years and 10 years …thank u

Dear Nayn,

Consider buying a Term plan till your retirement age.

Go through below articles;

Best Term insurance plans

Term insurance plans Vs Endowment insurance plans

It is very pity to see advising people not put there money in traditional LIC plans.Not knowing any thing about the plan details ,returns and its advantages in there life. I see number of blogs , asking people to become rich on investing in mutual funds and other trading funds.

History has proven time to time globally , on not investing there money people become poorer and poorer.its on saving money and keeping money for their heirs.

Dear Sir/Madam,

This is to inform you that i am a Sr. Agent of the Insurance Company from Delhi, if you have any query or plan to buy an LIC policy or any type of Insurance just like Mediclaim (Individual or Floter), Car, Scooty, Truck, Bike or any type of Vehicle Insurance, Burglary or fire Insurance, Money Insurance….,,,,

Directly contact me on my below mentioned Mobile no.

Thanks,

Upasna

8826111811

(When you call, Please talk to me you see the advt. on the Internet)

I have taken LIC jeevan anand initially in 2012 for sum of 5lacs. Now after reading your article, i came to know that investment is different from insurance. Can you suggest me whether i can continue or drop? Please suggest best mutual funds for 20k yearly.

Hi Srikanth,

I am 24 years old.I have done a LIC policy in 830 plan.I have to pay a premium of 10000 quarterly.I have chosen 8yrs,sum assured is 500000,maturity 21 yrs. I have done this policy in March,2015.I have to pay next premium on 2nd June.Recently I have come to know about mutual fund and elss scheme.I have already invested in that as you have told me.Now I think that I have taken wrong decision adopting this policy.Now please tell me what should I do.should I continue or discontinue accepting 10000(Frist premium) as a loss?please advise me I am confusing.i know that I cannot get through much return from this.

If i invest 50 lakhs for e-term what will be the amount at the time of policy end will be available for me

I am non-smoker,policy term-10yrs,my age is-28yrs

Dear Pruthvi,

Kindly understand what is a term insurance plan.

Suggest you to read my article – “ Is Term insurance plan a waste of your money?“

Thanks Mr.Srikanth for your valuable suggestion.Can you please suggest me any money back plans.I can afford only 20,000 per annum

Dear Pruthvi,

Why do you want to buy a Money back plan? Did you read the suggested article?

Hi Srikanth,

Can you please suggest me any money saving plans.

Can you also give the details of private insurers policies and your recommendations

Dear Anilkumar,

I will try to write… Thank you for the suggestion.

sreekanth…sir I am government higher secondary School Teacher …give me idea about best lic scheme duration 5 years and 10 years …thank u

Dear Chinnathambi,

What is your age? Do you have dependents?

Hi,

I already have LIC policy .. Looking to get one more policy BASICALLY for the purpose of high returns and TAX benefits.

Jeevan shagun shows highest return but still u ignoring it .. Why ??

I cannot do Single deposit .

Please advice . best plan with highest returns.

Thanks

Dear Vidhanshu,

Suggest you not mix investment with insurance. What is meant by HIGH RETURNS according to you?

I can not suggest you a life insurance plan from investment point of view. Trust me, do not invest in traditional plans.

Hi Sreekanth. Thanks for that detailed comparison of the LIC plans. I have just got married and neither me or my wife have a life insurance & we realised we have to take one right away. Wanted your suggestion on which of the above mentioned would be the right choice for the both of us with each other as nominee.

Dear Avinash,

Do not get confused with so many types of life insurance plans. Keep it simple. Kindly consider buying a good term insurance plan.

You can consider buying LIC e-term plan, HDFC Click2protect plus,Kotak’s e-preferred plan etc., These are online term insurance plans.

If you want comprehensive term plans with optional riders like Accident Death benefit, Total Permanent disability rider, Critical illness riders then you have to consider buying offline term insurance plans.

You may visit my post on “Comparison of online Term insurance Plans.”

Is your spouse employed? She can take a term plan if she is an earning member of your family. Re-check your insurance requirement once you have new additions to your family 🙂

All the best!

Dear Mr. Avinash,

This is to inform you that i am an LIC Consultant from Mumbai, if you have any query or plan to buy an LIC policy kindly contact me on my below mentioned cell no.

Thanks,

Mahesh

8422037490

Sreekanth, thank you for listing all lic policies at one place and providing us your suggestions. This is like all-in-one guide 🙂

Dear Bhuvana,

Thank you. Keep visiting!