LIC (Life insurance Corporation) is set to launch one more traditional policy which is Limited Payment Endowment Plan.

The main feature of this new plan is, the payment of premiums is limited to a term shorter than the policy. The maturity amount is payable at the end of the policy term, or on the death of the policy holder whichever is earlier.

Features of LIC Limited Payment Endowment Plan :

- Type of plan : Endowment plan with limited premium paying term.

- Minimum Entry Age : 18 years

- Maximum Entry Age : 62 years

- Maturity Age : 75 years ( Maturity age is, the date at which the face amount of a life insurance policy becomes payable by either death or other policy terms and conditions).

- Policy duration : Under this plan three types of durations are available – 12/16/21 years

- Premium Paying Term : 8 years (or) 9 years

- Minimum Sum Assured : Rs 3 Lakh

- Maximum Sum Assured : Not applicable

LIC Plan 830 – Maximum Age at entry Vs PPT :

Benefits of LIC New plan – Limited Payment Endowment Plan :

- Death Benefit – On death of policy holder during the policy period, his or her nominee will receive Sum Assured on Death+Accumulated Bonus and Final Additional Bonus if declared by LIC.

Sum Assured on Death will be higher of the below

(i) 10 times of annualized premium paid. (Or)

(ii) Absolute amount to be payable i.e 125% of Basic Sum Assured.

This death benefit shall not be less than 105% of all the premiums paid as on date of death.

- Survival Benefit – If policy holder survives till the end of policy term then he/she will receive Sum Assured on Maturity+Bonus+Final Additional Bonus (if declared by LIC). Here Sum Assured on Maturity is equal to Basic Sum Assured.

Optional Riders of Limited Payment Endowment Plan :

The policy holder has an option to avail two riders under this plan. These are optional riders and are available on payment of additional premium.

- Accident Death & Disability Benefit Rider – This rider can be opted for at any time within the premium paying term of the Basic Plan provided the outstanding premium paying term is at least 5 years . So for a Plan which has Premium Paying Term of 8 years, this rider can be opted anytime in the initial 3 years. For a PPT of 9 years, this rider can be opted in the initial 4 years. The benefit cover under this rider shall be available during the policy term or before the policy anniversary on which the age nearer birthday of the Life Assured is 70 years, whichever is earlier. The minimum Sum Assured offered under this rider is Rs 10,000 and maximum SA is Rs 1 crore (subject to maximum basic sum assured).

- Term Assurance Rider – You can opt for minimum Sum Assured of Rs 1 Lakh and maximum of Rs 25 Lakh under this optional rider.

This rider can be opted for at any time within the premium paying term of the Basic Plan provided the outstanding premium paying term is at least 5 years The benefit cover under this rider shall be available during the policy term or before the policy anniversary on which the age nearer birthday of the Life Assured is 70 years, whichever is earlier.

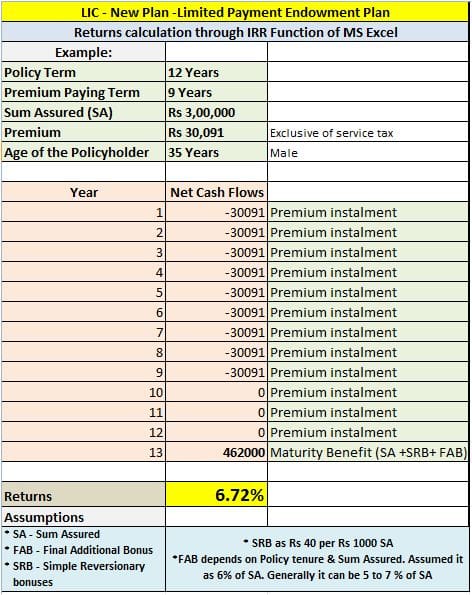

Example of a Limited Payment Endowment Plan :

Mr. Nair aged 35 years, plans to take Limited Payment Endowment Plan for the term of 12 years and the premium payment term (PPT) of 9 years. He chooses the sum assured of Rs 3 Lakh.

In this case, he is required to pay an annual premium of Rs 30,091 pa (excluding service tax) for 9 years only. After the PPT of 9 years, he will stop paying premium but the policy will continue till the policy term of 12 years.

The possible events that can happen are :

- On Death of Policy holder – If Mr Nair dies during the policy term, his nominee will receive the Sum Assured + Accrued Bonuses. After this, the policy will cease to exist.

- On Survival till maturity – If Mr. Nair survives till the end of policy term, he will get the Sum Assured + Accrued Bonuses. The policy will terminate thereafter.

As analyzed above, the returns from ‘Limited Payment Endowment Plan’ can be somewhere in the range of 5.5% to 7 %. I have mentioned this range after calculating the returns for all the possible combinations of Premium Paying Terms ( 8 or 9 years ) and Policy duration ( 12/16/21 Years).

Kindly stay away from these kind of plans if you are expecting higher Rate of Returns. Do not buy this plan just because it offers you Tax Saving benefits. There are better Tax Saving Investment options available in the market.

For example, PPF (Public Provident Fund) will give you better returns than these kind of Endowment Plans (if safety of capital and tax benefits are your priority). (You may visit my post on “ Is Term Insurance a waste of your money? Endowment Policy Vs Term insurance policy.“)

I hope this post is useful and informative. Do share your views and comments. Cheers! (You may like visiting my post on “LIC’s Limited Payment – Endowment Plan offers LIMITED RETURNS.”)

Join our channels

I want to know about lic policy’s minimum term and minimum premimum paid.And in this condition which lic policy is suitable for me.

Dear ..If insurance is requirement, you may opt for LIC’s e-Term insurance plan.

Can u guide me what happens if I want to close the policy by 10th year instead of waiting for the 12th year.

I Assume have the paid entire premium till 9th year.

Thanks & Regards

M.Prakash

Dear Prakash..You will get the Surrender value.

Hi Sreekanth.

Please could you inform me of the maturity taxation on the LIC limited premium Payment Endowment Plan (Table no 830). if premium paid yearly is more than 10% of Sum assured. Like for ex. i pay yearly approx 36500 for a SA of 300000.Actually i have 2 questions

1. do i get any tax benefit under 80c and 2. tax on maturity amount.

thanks a lot.

Dear Mr Pal..kindly go through this link..

Dear Srikant,

I am a taxpayer in 30% bracket and also do the full PPF investment.I also have critical illness insurance separately but no term insurance.I was thinking of investing 17L for 21 yrs and my age is 35. Will you suggest this plan for me?

Any other investments like RD,FD will also give me 5-6% interest considering my tax bracket.What is your thought?

Thanks

Dipu

Dear Dipu,

Beofre you work on your investment plan, kindly get Term plan cover at the earliest. Read my article : Best Term insurance plans.

Do you have health insurance coverage?

Totally wrong calculation and genuinely its not called expert advise. Please calculate this plan with higher term. First wrong thing you calculate this returns with full premium. Do first minus insurance cost premium in the actual premium then calculate. Do you know in 2015 what LIC give actual return in endowment type of policies? Its nearer 9% after minus insurance cost. 9% is actual return and its also tax free. Basically Only term insurance is not right, only PPF is not right & only endowment plan or mutual funds is also not right.

Dear Alok,

I agree with you on one point that is – I am definitely not an EXPERT. But I blog with good intentions. I try my best to provide ‘unbiased’ suggestions/views to my blog readers.

‘Only Term insurance is not right’, yes having term insurance alone is not right, one also needs to invest in mutual funds, bank deposits, PF, real estate etc., But definitely not in Endowment or money-back policies (of any company’s).

We are still in the first quarter of 2015 and how come you are talking about the Returns generated by Endowment policies in 2015?

Example:-

Date of commencement of policy was :- 04/02/1990

Client age at the time of taking policy:- 30 yr.

Sum Assured :- 5 Lac

Term – 25 years

Premium yearly :- Rs. 19,409/-

Maturity Date :- 04/02/2015

Now see how much get actual returns to the client from LIC

Premium Yearly :- Rs. 19,409/-

Actual investment in endowment plan :- Rs. 16,998/- (Rs. 19,409 – Rs. 2411 this cast is natural and accidental risk cover.)

So, we need calculate returns with Rs. 16,409 not with Rs. 19,409/-

Maturity amount he got on date from LIC is Rs. 14,94,500/- (5,00,000 (actual sum assured) + 9,94,500 (Total bonus of 25 years & Final addition bonus))

I.R.R. Value on investment :- 8.6892% (please note its tax free and get peace of mind, its decent return from LIC)

This is the LIC’s past performance.

If any one want more returns then I suggest go through mutual funds with SIP.

Dear Alok,

Hmmmmm… before discussing ‘the returns’part, lets start the discussion from scratch.

Kindly share your views as to “What is insurance?“

Dear Sreekanth,

I am planning for LIC – Limited premium endowment plan (plan no. 830) with 8 year premium – 12 year maturity.

My age is 41, do I have better choice in LIC?

My consideration is, short term, less investment with good return.

I was told, premium is approximately 35000/- for 8 years and after 12 year return is 4,50,000/-

Please clarify.

Murali

Dear Murali,

Kindly do not mix insurance and investment. Insurance is for risk protection. Do not expect profits/returns from an insurance plan.

Kindly read my article on “The most common Personal Finance mistakes people make..”

Do you have a Term plan? Suggest you to first calculate your insurance requirement (sum assured). Once, you know how much insurance coverage you require, consider taking a good term plan (if you do not have one or under insured).

Read my articles, “Top 7 best Online Term insurance Plans in India” & “Is Term insurance a waste of your money?“

Dear Sreekanth, Here in your reply to Krishana is you haven’t much details on LIC’s Limited Payment Endowment Plan. But you are talking like an Expert. First gather much genuine information/details about the product.

Dear Sujith,

With reference to Mr Krishna’s below comment.. I wrote the first version of this post on 5th December, 4 days before LIC launched this plan (so that I can atleast help few investors in taking right investment decision) .

When Mr Krishna raised this query, i have mentioned the approximate returns. As soon as the premium chart for this plan is available, you could see in the post, that i have calculated the returns based on IRR. The returns do match my initial assumption right?

If you want you can visit my other post on “LIC Limited Premium Endowment Plan offer LIMITED RETURNS” for more information on how to calculate returns on endowment policy (if you are not aware of how to calculate?) 🙂

If possible, let me know what else GENUINE information do you require? I prefer to give facts and figures to justify my suggestions/recommendations on any financial product. I always try to list the pros and cons of a financial product. So that my blog visitors can read, understand, analyze and take informed decisions. Cheers!

Lic Endowment plan is very good plan for new investor in market & withtogether provided high riskcovee, Returns.

Dear Nilesh,

I have provided the facts and figures in my article. Now, it is upto my blog visitors to analyze the pros and cons of this plan. If someone is content with 6% kind of returns over a period of more than 10 years, can go ahead and buy this plan 🙂

If I am looking for a life insurance plan for risk coverage then I will definitely ignore these kind of endowment plans.

Why do you think this is a very good plan for a NEW INVESTOR? Could you justify your statement?

Why dont u calculated IRR with 21 years of term

Insurance is nt for short term purpose

And u should consider the sirk factor

For ur kind information – insurance is mainly for risk and this kind of day lanning help people to save + risk cover

Ppf dosent gives u risk cover

Dear Mayuresh,

You may visit my other post on IRR calculation for 21 years policy duration. Your are contradicting your own statements. Are you for or against this plan? I agree with you that Insurance is for risk coverage. Then why do we need these kind of insurance cum savings plan? If risk coverage is the priority then don’t you think Term insurance is the best option? For investors who are risk averse, PPF + term insurance coverage can be a better option (this is just an example). If someone can stomach volatility then equity mutual funds + Term insurance would be even better.

Respected Mr. Sreekant Reddy,

Your Comments may give bad impact to the many of LICian and trust of them on LIC, What do you know about LIC and you are not and LIC Agent, This plan is one of the Best ever product than any Non Linked investment in Indian Market,

who ever is interested to know more about this plan, please call for meeting.

Regards,

Nayan J Prajapati.

LIC – MDRT Agent

Mob. 09321025267

Dear Nayan,

To give an honest review it is not necessary to be associated with a financial institution. Yes, I am neither associated with LIC nor any other fin insti.

Could you justify as to why this plan is the BEST EVER product?

Wow. Excellent analysis. You are so fast in updating us (investors) on new plans. Its like alerting us. Thank you and appreciate your hardwork.

Thank you Sudha. Keep visiting and share your views.

Good analysis Srikanth!!

Thank you Yashwanth. Good to see you back.

What is the XIRR of this endowment policy?

Hi Krishna. Complete details are still not available. I will soon provide in-depth analysis. Generally, you can expect returns in the range of 4-6% from Endowment/money-back plans.