Life Insurance Corporation of India (LIC) is launching a New Child plan called as ‘LIC Jeevan Tarun‘. This new plan from LIC is a traditional, Non-linked, with-profits and Limited Premium Payment Option plan. It also has an optional Money back feature.

In the month of March (2015), LIC had launched New Children’s Money back plan. Jeevan Tarun plan is very similar to it, but it offers more Survival Benefit options to the policyholder.

I am against these kind of so called ‘CHILD PLANS’. Before analyzing the details and returns of this new LIC child policy, if you understand how this child plan works, I am sure you as a parent / guardian of your child, may definitely ignore these kind of meaningless schemes.

Under this plan, you (parent / guardian) are the proposer. Whereas, your kid’s life is covered. Your baby’s life is insured. Sounds stupid? Yes, generally you would like to have a risk cover on your name/life, so that in case of any unfortunate event, your kid / legal heir/ nominee will receive the claim amount.

In this plan, in any unfortunate event (on kid’s death, can’t even imagine this happening!), you (parent) will receive the death benefits. If kid survives till maturity, he/she will receive the money-back payments (survival benefits) at periodic intervals (after 20 years of child’s age)

Unfortunately, if parent dies, kid will receive all survival benefits, only if ‘Premium Waiver Benefit Rider’ is selected.

Its very disappointing and disheartening to see LIC come up with bad schemes like these. If you are convinced about my views, you may ignore buying this plan. Need more details?…ok..here you go!

Features of LIC Jeevan Tarun Plan

- Minimum & Maximum Entry Age : 90 days to 12 years (Kid’s age)

- Life Assured / Insured : Your kid’s life is insured under this plan

- Proposer’s Minimum / Maximum Age : 18 years / 55 years (Proposer can be Kid’s parent / guardian)

- Policy Term : Maximum upto 25 years of kid’s age. ( 25 years – Age at entry. For example, ff kid’s age is 10 years, policy tenure is 15 years)

- Premium Paying Term (PPT) : Maximum upto 20 years. (20 years – Age at entry. For example, if kid’s age is 10 years, PPT is 10 years)

- Minimum Sum Assured : Rs 75,000

- Maximum Sum Assured : Not Applicable (No limit)

- Premium Waiver Benefit Rider (optional) : Available. (LIC’s Premium Waiver Benefit Rider is available as an optional rider on the life of proposer aged between ages 18 to 55 years by payment of additional premium. In case of death of the proposer, the premiums under the basic plan falling due after the date of death shall be waived.)

- The policy’s maturity amount is payable on completion of 25 years only (insured’s age).

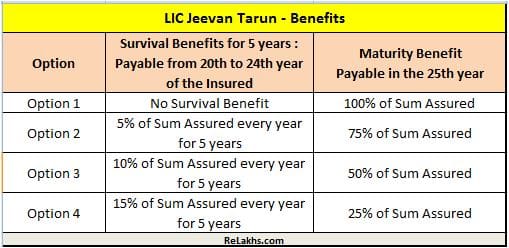

- Depending on the requirement, the proposer (parent / guardian) can choose any of the 4 options for SB (Survival Benefit) payments from 20 to 24 years of age.

LIC’s New Plan – Jeevan Tarun : Death Benefits, Maturity & Survival Benefits details:

- Death Benefit :

- If death occurs before the commencement of risk, an amount which is equivalent to the premium payments is paid.

- If death of the proposer occurs after the commencement of risk, death benefit amount which includes ‘Sum Assured on death + Accrued Bonuses + Final Additional Bonus‘ will be paid. (Commencement of risk is linked to kid’s age. If kid’s age is above 8 years, date of commencement of risk is immediate. Sum Assured on death is higher of 10 times of annualized premium or Absolute amount assured to be paid on Death i.e. 125% of Basic Sum Assured.)

- Maturity Benefit: On Survival of the life assured till the end of the policy term, maturity benefit will be paid as below.

Maturity Benefit = Sum Assured on maturity + vested Simple Reversionary Bonuses + Final Additional Bonus (if any)

- Survival Benefits & Maturity Benefit – Options under Jeevan Tarun Policy (Money Back payments) : In this plan, the policy holder can opt for any of the below 4 options.

LIC’s New Plan Jeevan Tarun – Returns Calculation

This plan defeats the whole purpose of insurance. I believe that there is no need to do in-depth analysis on this plan. JUST IGNORE BUYING THIS PLAN!

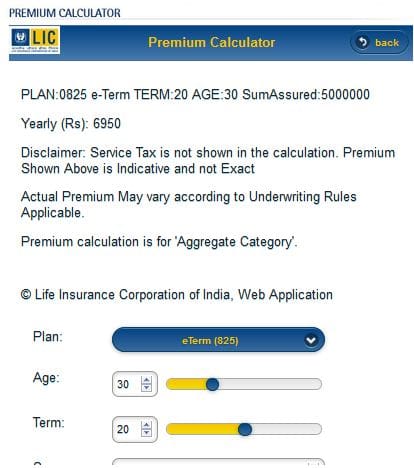

Life insurance premium quote – LIC Jeevan Tarun (Vs) LIC’s Online Term Insurance plan e-Term :

For a Sum Assured of Rs 1 Lakh, the premium amount on Jeevan Tarun policy is Rs 6,375 (as per the illustration on LIC’s website ).

Whereas, a 30 year old individual can opt for LIC e-Term plan of Sum Assured Rs 50 Lakh at a premium rate of Rs 6,950 (policy term 20 years).

My opinion on LIC Jeevan Tarun Child Plan

As per LIC, Jeevan Tarun plan is specially designed to meet the specific expenses such as children’s education, marriage and other future needs.

But, what is the main purpose of investing in child insurance plans? Most of us may say, ‘ I want to secure my child’s future’ (or) I want to accumulate / create a fund to meet my kid’s education or marriage expenses.

- Cost of Education : We all are aware of the rising costs of higher education. Each year, tuition, books and other expenses increase. Education inflation is definitely in the range of 10% to 15%. Do you agree with me? In this scenario, if you choose to invest in this kind of savings cum protection oriented plan, which can generate returns of around 5% to 6% (or max 7%), your main objective (i.e., to secure your kid’s future) will not be met.

- Also, the survival benefits are payable from the 20th year onwards. Normally the college education (graduation) may start from 18th year onwards. The maturity benefit is payable upon the completion of 25th year only. So, this plan does not serve the purpose.

- You will be better off taking a good Term Insurance Plan (Read my article on “Top 7 best Online Term Insurance Plans“) and invest a portion of your savings in different asset categories. These asset categories can be mutual funds, bank deposits, equity (shares), Public Provident Fund, Sukanya Samriddhi Account Scheme… you have plethora of investment options to choose from. (The premium contribution towards a Term plan can be claimed as Tax deduction under Section 80c)

- Defined Investment plans with names like ‘Child plans’ (or) ‘Retirement plans’ may not meet your actual requirements. These kind of defined packages may attract your attention. But, you can create you own portfolio of investments and aim at beating the inflation. Be aware and beware of these kind of Child Plans.

- Also, do note that the returns from these kind of plans are largely dependent on Bonus rates (which are not guaranteed). The bonuses (if any) are accrued and are payable only on maturity of the policy. So, you are losing the benefit of COMPOUNDING factor.

Before buying a life insurance policy, follow these steps;

- Analyze your life insurance requirements. Calculate the required amount of insurance.

- Understand the plan(s) features / benefits.

- Understand the rate of return calculations & assumptions (if any).

- Check if the sum assured is sufficient to cover your life?

- Ask yourself these questions..Is the premium affordable? Can the family members lead the same standard of living in case of any unfortunate event?

And then take a decision to buy or not..

What is your opinion on LIC Jeevan Tarun Plan? Do you think is it worth to invest in this new policy? Do share your views and comments.

Continue reading :

- Traditional Life Insurance Plan – A terrible Investment option?

- If Life is unpredictable, INSURANCE can’t be optional

- Life insurance : How to get rid off unwanted life insurance policies?

- Calculate how much you need to save for your KID’s Education?

- LIC New Children’s MONEY BACK PLAN – Review

Join our channels

Hi Sreekanth Sir,

Today my wife met one lic agent. He informed one Jeevan Tarun Plan for my son.

My son age. 3.5 Years.

They suggested ,

1 st year monthly payment 2142/- rupees and from 2 nd year monthly payment till end 2104/- rupees.

Then money back will get 18 to 22 years continuously 5 years * 75000/- rupees, and finally 23rd year will get more than 11 lacks.

How is this policy?

Can you suggest me is it good or not and its correct?

Dear DIBIN,

Did you go through above article??

Kindly read:

Traditional life insurance policy – a terrible investment option?

If life is unpredictable, insurance cant be optional!

Best term insurance plans.

sir just give me simple explanation about what I asked to you

Dear DIBIN ..I have given simple explanation in the above article about this plan.

Personally, I would not buy these kind of insurance plans.

Hey shrikant, I want to know that if i purchase jeevan tarun of 600000/- for my 1 year daughter, so how much will be Quarterly premium for that with ST. please reply fast.

Dear seema ..Did you go through the above article?

If your requirement is insurance/life cover, you may kindly consider a Term insurance plan.

Thank you so much Sreekanth for this insightful review. I fully agree with your views on this plan. I was holding back myself from buying this plan for my child because of the exactly same flaws in the plan as pointed out by you. It’s a bad child plan although not all LICI plans are bad. Jeevan Anurag was one of the best child plans brought forth by LICI but sadly the same has been withdrawn for the reason best known to LICI. At present (as on 5.2.17), such a big corporation as LICI surprisingly has only two types of child plans both of which do not fulfill the basic requirements of a child plan as rightly pointed out by you. Hence I would be very grateful if you could kindly suggest some alternative child plans from other insurance companies at my email id. Thank you once again.

Dear Subba,

May I know if you have adequate life cover in your name?

Suggested reading : If life is unpredictable, insurance cant be optional!

Dear Sreekanth,

I read the reviews of Jeevan Tarun Policy. You have given your unbiased and honest openion. Its 100% right. you should not be bothering about LIC agents troubling or abusing you. Your work is appreciated by followers. Please carry on with your blog and ignore these LIC agents. We know how that company is fooling people. We are with you. Majority of the premium paid by us is eaten by these agents and without any effort they suck the profit of company also. Please go ahead

Regards

RAJ

Dear Raj,

Thank you for endorsing my views.

Not all agents are bad, we do need the intermediaries to spread awareness on importance of insurance.

Mis-guiding & miselling need to be stopped.

Hi Shreekanth,

I would like to take a Jeevan Tarun policy for my grandson of age 2 yrs who’s in US. What would be the procedure to go for this policy?.

What all documents needs to be submitted?

Also can you please correct if my understanding is correct regarding this policy? I will be the proposer or policyholder and my grandson will be the life assured.

Also can you please suggest if there is any other plans that I can take for my grandson?

Thanks in advance

Dear Mohan,

Kindly let me know if you have read and understood the points listed in the above article.

Your grandson does not require any life cover.

hi u can cont me on 9335616137 for taking the policy

Good work Sreekanth. Keep going.

Dear Sir,

I have a 2.5 year old kid. I am planning to take a insurance policy for him. I have a policy named LIC Jeevan Anand under my name. Plz suggest any good policy for my child.

Also I dont want to be fix with only LIC for insurance. So can we have a faith on another players in the field

Dear Rastogi,

Kindly let me know if you have gone through the above article or not?

Do you have existing life insurance policies in your name?

Hi Srikanth,

Thanks for your unbiased feedback ,One of LIC agent came to my house and explained about Jeevan Labh..he was telling the plan like if I pay around 8L for 16 years ..at 21st year I would receive 23 L it seems.do you think can I believe these figures?I

Dear Giribabu..May I know if you have any existing life insurance policies?

Suggest you to kindly ignore buying these kind of traditional plans.

If your objective is to get decent life cover then buy a Term insurance plan.

Read:

If life is UNPREDICTABLE, insurance can’t be optional.

Term insurance Vs Traditional plans.

Best Term insurance plans.

Best Personal Accident insurance plans.

Hi Sreekanth, I do have Term insurance plan for 50L which is SBI Eshield ..LIC agent was explaining this scheme and was unable to decide his figures or correct or not ..What is your suggestion

Dear Giribabu..Suggest you to ignore buying it.

Hi Sreenkanth, Thanks for your suggestion,I have a Jeevan anand policy which is in-force ,half year primum is around 26K and this was taken on 2012 Nov , I have paid 7 half year premiums till now,I would like to go for Paid -up option..Please suggest what is the procedure for paid up ?should I go for Paid up or surrender which is better ?As I have 50L term insurance and 8k SIP MF investments monthly I would like to go for either paid up /surrender . suggest me.

Dear Giribabu,

As the policy is only 3 years old one, suggest you to surrender the policy and re-invest the surrender value amount in decent investment options based on your financial goals.

Read:

How to get rid of unwanted life insurance policy?

Hi ,

If I am looking for only investment option , Which plan is good ?

Dear naegndra ..Kindly read : List of Best investment options in India.

Sir this is sanjay form Mysore ( Karnataka) working as driver, i have one year old son, can you please recommend which plan is better for my son for his education etc, whatever you suggest i will follow you, because i ask some insurance advisor they will suggest from their beneficial point of view, since my earnings is average, so whatever you suggest i will follow, because i dont want my son to be driver like me , please suggest me

Dear Sanjay,

Do you have any life insurance & health insurance policy in your name?

Meanwhile, kindly go through below articles;

If life is unpredictable, insurance can’t be optional.

Best Term insurance plans.

What a terrible child plan!!!!

Besides pathetic traditional plan to fool the parents, the major flaw of this plan is that the child is the life to be covered and not parent. So dumb.

In-spite of being such a bad product, I am surprised to see a lot of positive response / comments from many people on many forums for this plan.

I wonder whether those are real parents or LIC agents? God knows

However, a good analysis. Any financially literate person will never buy such product.

Keep up good work

Dear Rupali,

Unfortunately, any product which has ‘CHILD’ attached to it will sell like hot cakes in India.

Most of the investors do not even check the features of these plans before buying them.

Thank you for endorsing my views and sharing your inputs.

Let’s do our bit to increase financial literacy levels in India.

Keep visiting 🙂

Dear Shrikant,

You are CFP u know very well dat wht kind of role insurance planning play in FP, and onething we must know dat Insurance is saving pool not a investment pool.

It only compensate the losses on occuring of uncertain/unforseen events.

Any insurance plan in india approved by IRDA. Whoes works on principles to protect to insured person concerns or rights.

Dear Rahul,

Yes, I am very well aware of the importance of INSURANCE.

Kindly read my article : Why Insurance is very important?

I believe that insurance is neither a savings tool nor an investment vehicle.

Believe this article is aimed to put LIC Low in the eyes of public. Life is uncertain and we should have different perspective to life. Having child as a policy holder and parents benefiting from it should not be looked negatively. Every parent loves their child.

It’s a decent plan not the best though. Returns are not very lucarative but they way the article has been written is that LIC is trying to rip off public. Crazy..

This plan has been accepted by public who is knowledgable and well read. So ppl make your own opinions and do not be taken away by some body else’s biased comments.

Dear Anonymus,

1 – Life is uncertain : That’s why one has to have adequate life cover and can consider taking a Term plan instead.

2 – Don’t you think that as a responsible parent, one has to have adequate cover on self rather than taking an insurance cover in the name a child ?? May I know why do you think “Having child as a policy holder and parents benefiting from it should not be looked negatively??”

3 – Every parent loves child – That’s why a parent has to have adequate cover. These kinds of plans are just not affordable to have high life insurance cover.

4 – Returns are not lucrative – Thanks for agreeing to this fact! If this plan does not offer life cover at affordable rates and if this plan does not offer ‘decent returns on maturity’ then why one has to invest in these kind of plans..kindly share your views?

One has to go through the pros & cons of a financial product and can take an informed decision. From my side there are absolutely no un-biased comments, as I am not associated with any financial product/service provider. Cheers!

jeevan tarun is a good child money back policy.

Hello dear. which plan is best for child like. post of suknaya and lic jeevan tarun. please suggest.me.

Dear Manoj,

Did you go through the above article?

Do you have sufficient life insurance cover?

Srikanth do you think government of India is fool like u man better understand the concept and think of yourself so called certified financial adviser.

Every plan has its own feature, pros and cons,

SSA is meant only for girl child below 10 yes, where inJeevan Tarun is for both boy and girl.

SSA provides you good return than Jeevan Tarun. This is because SSA doesn’t cover life risk, but Jeevan tarun covers the life risk of both child and father/ mother

Do you think there is no need of financial support to child when the guardian dies, do you think the father doesn’t want the return for which the he has paid premium for his child carrear.

Moreover all government owned organisation say LIC Postal Nationalised bank launches there plans with the concent and approval from the finance department. The secretariat of finance department ensures that the plan is for the benefit of the society.

If ur correct answer me through this blog,

1.

Which is the plan to have high return, with low beta, with government sovereign guarantee by Govt of India against such investments.

2.

Which organisation apart from LIC sends you notice to pay your installments( premium) against your estate creation

——#——

What ever we save today will enjoy at the end realising that this what I could save in my life.

Dear Chetan,

Thank you for sharing your views.

Let us understand the basics first before assuming ‘who is fool here’ 🙂

What is life insurance? What is ‘high return’ according to you?

I don’t know who the hell gave u certificate. What u speak is seems to be psycho, hope being unemployed you lost iq

One-off the person asked whether the premium paid against children’s plan can be claimed under 80 c and ur reply for is question was ( why you took this plan.) Man I don’t understand your views.

Ever investments has its own benefits, SSA plan gives you high return compared to any recurring deposit.

.

See what’s the basic points I have stated in my first comments are u a dropout school guy ur answers and suggestion in the blog are childish and arguing.

Sreekanth sir – I have gone through the conversations in this article. Thank you for sharing unbiased views.

Chetan – After going through the conversations, it is very clear as to who is a Psycho here. Sreekanth has shared his ideas/views. You and me have all the rights to share our views too. But you do not have basic manners. Is this the way to talk on a public forum? Sreekanth has asked couple of basic questions rightfully. I think instead of answering those questions, you are just beating around the bush. Also, in one of your comments you say, this policy gives ‘high return’ and in another comment you say ‘low return’, contrasting views.

Thanks for the suggesting Agarwal ji,I do understand and I apologise, but before that let me say no person or the organisation has to blame other companies financial products , why am saying is see the suggestion that he has given to the public (

Sreekanth Reddy says

August 6, 2015 at 4:51 pm

Dear Amit..Did you go through the above article? LIC jeevan tarun you may blindly avoid it. No second thoughts about it. )This was the suggestion given for the visitor (Amit Patel says

August 6, 2015 at 3:10 pm

i have paln for lic policy of my daughter but i am cofuse about Jivan tarun and Sukanya Samridhi of post in both the case rturn are same but sukanya policy are matutrity is 21 year and this age is higher eduction / marriage time so this time i have need money and jivan tarun maturity time age is 25 year….So please help on urgent basis because this weekend i have finalise poicy).

Clearly observe the conversation,

point 1.

Mr amit is planning some investments, but SSA cannot provide return uto 21 , so amit specified clearly that he needs return in-between,

Point No 2.

He asked suggestions amoung SSA and J. Tarun. Was it made clear by shreekanth?

————————

On what basis did he come to conclusion that avoiding Tarun is better and suggested not to go to tarun.

He is Misguiding public.

How can he say that the Tarun is meaningless product. Is he an actuary.

Do Govt organisation like postal, nationalised banks, LIC offer meaningless plan. If so his comment saying meaningless is true.

Chetan Ji..I don’t think Sreekanth is misguiding or misleading. His views are honest, clear and simple. I too believe that plans like Jeevan Tarun are meaningless.

One need not be an Actuarian , minimum common sense is more than enough.

If you think that ‘who is sreekanth’ to give conclusions or suggestions here, then some people like me may say that ‘who are you’ to comment about someone’s IQ/Employment status/skills on public platform. Instead of leaving comments on Product you are unnecessarily misleading investors. Answering to your other question ‘lol’ is ok compared to your comments which are not making any sense.

Dear DrAgarwal,

Thank you for sharing your views and also for endorsing my views. I have always tried to highlight the Pros and Cons of Financial products in an unbiased way. Let the blog readers / investors take informed final decisions 🙂

i have paln for lic policy of my daughter but i am cofuse about Jivan tarun and Sukanya Samridhi of post in both the case rturn are same but sukanya policy are matutrity is 21 year and this age is higher eduction / marriage time so this time i have need money and jivan tarun maturity time age is 25 year….So please help on urgent basis because this weekend i have finalise poicy

Dear Amit..Did you go through the above article? LIC jeevan tarun you may blindly avoid it. No second thoughts about it.

Hi, I am 35 yrs and planning to buy a child policy for my son (1yr 11 months). One of the LIC agent has proposed to club jeevan tarun and jeevan lakshya for a SA of 8 lacs for a monthly premium of Rs.3200. The agent also mentions that this product has future premium waveoff on death of the proposer. Death benefit as 10% of SA on every policy anniversary.

Please advise. what to do.

Dear Vinod,

Did you go through the above article? Are you able to understand ‘what is life insurance’ and its importance?

Are you convinced to buy life insurance policy like Jeevan Tarun?

Read my review on LIC Jeevan Lakshya.

Go through these articles;

Top term insurance plans

Term insurance Vs Endowment policies.

Hi,

The answer is with you my friend if you want high returns mean go for SSA if you want average return + risk coverage on both of your life means got LIC jeevan tarun…. Both Postal and LIC are government owned organisation

Dear Vinod,

Do not mix insurance with investments. If you want risk cover, you can consider buying a Term plan.

For investment requirements (based on your financial goals and tenure), you have plenty of options to choose from.

Hi

If i am proposer who has taken Jeevan Tarun policy on my child’s name. Can i claim the premium amount which i paid under section 80 C?

Thanks

Kalyan

Dear Kalyan..Why do you want to buy this policy?

Yes you can claim under 80 c

1. What makes you to suggest Sukanya Samridhi is a better option than Jeevan Tarun. The returns will be almost same & moreover the Jeevan Tarun provides Insurance coverage too.

2. I have already 2 boy kids, I don’t wish to try my luck third time for a girl baby to become eligible for Sukanya Samridhi.(LOL)

3. Of course your point on getting benefit for education from 20th years onwards while College education is starting at 18 years is a point of concern.

Dear Sridhar,

What is your opinion on this plan?

3rd point itself is enough to prove this plan is a meaningless one. Don’t you think so?

My view is that Jeevan Tarun is alternative for SSS if one does not have a girl child. If not for education use it for higher education of the son.

You avoided answering my point 1 & 2 . You either chose to give a easy answer which goes easy with your views on the scheme.

You did not answer my primary question of what justice does GOI do for a male kid.

Dear Sridhar,

Tell me one thing, at what age generally kids opt for higher education in India?

Before discussing 1st and 2nd point, you answer me a simple question..according to you ‘what is insurance?’.

Your last sentence makes me laugh 🙂

If a parent buys these kind of meaningless insurance products, tomorrow his/her kid(s) will ask a similar question to their parents.

Please find answer for your question.A protection against the loss of income that would result if the insured passed away. The named beneficiary receives the proceeds and is thereby safeguarded from the financial impact of the death of the insured.

Dear shreekanth before laughing please answer for the question point 1 and 2. Asked by Shreedhar

Personally

Suggest me a plan which I need for my child career say about 18 years. Where the returns are not subjected to market risk

Dear Chetan,

If insurance is for protection or risk cover then why should one take a policy like LIC jeevan tarun and why not just a Term insurance alone? Under this plan, the insured is KID and not the parent. So, don’t you think the whole purpose of having an insurance coverage is defeated here. Read your above answer and this reply.

You have not yet answered my 2nd question 🙂

can lic agent share their part in premium. for what service we pay them throughout the policy term….just for befooling….. any way…keep on doing good work….

they have upto 25% share in your premium…. which they never tell…

Dear Bhupendra,

Thanks for sharing your views. I will keep posting unbiased reviews and do share the articles with your friends too and help them understand the pors & cons of these kind of plans.

From 1956 to till now LIC is doing its best to serve the people. It is peoples money for peoples safety. The author might have come from well to do family. Always he is thought of higher education etc. For many small low and middle class families, it makes a habit and for some it will help to do a small business to live on. Insurance is sharing of losses. It is a virtue, if anybody taking LIC policies. Your money is not only benefit for yourself but also it lightens unfortunate families where the main bread winner has short life. Only selfish people are go behind the money. Don’t misguide the people. Do some good to people. Don’t always go behind money money money

Dear Srikanth,

Are you an Agent (or) an Investor (or) both ? Kindly confirm.

(I am not associated with any company. So, there is ‘no conflict of interest’ from my side)

Hey Sreekanth Reddy the so called advisor. Can u shut ur hell up and stop misleading the common public by your stupid advise and constant yelling up on the name of LIC.

I think you get perks from the private companys to ruin the name of LIC as they dont find way to stabilise themselves in the market against the biggest giant.

How much r u paid for doing this bull shit. Do you know the road, railways, etc etc you use are being funded majorly by LIC.

Can you name any insurance company which covers natural calamities. LIC does it.

In next coming 5 years LIC wll fund 1.5 lakhs crores to Indian railways. Why does it do this coz the shit like u can get a better standards to live.

With your stupid advise persons going for cheap private insurance and mutual funds. If any uneven happens and the market collapes will u pay these persons from your blady pocket..

You will be the first one to dig a hidout for urself..

If you cant contribute towards a nation building then pls stop abusing other who r doing it.

Dear Shyam,

Lol 🙂 Thank you for your kind words.

I can understand your frustration and desperation.

Show me a single sentence in my article that has made you to think that I am misleading people Lol 🙂

For your kind information, I not associated with any company.

Do you know that how much LIC invests in Stock market? Do you know that LIC is the single largest domestic investor in stock market?

If market falls, LIC is the biggest loser.

I may not be as talented as you are to speak about topics like – LIC Funding Indian Railways. But, I can confidently say that these kind of plans are not at all beneficial to a common man.

Is this the way to speak in public forum? If you are an agent, God must save your clients. Instead of giving generic and idiotic comments, if you have stuff, kindly share your views based on facts and logic lol 🙂

Srikanth,

Keep up the good work, there are lot of silent readers who don’t comment but read every article and understand the reliability( after doing due diligence) and keep quiet.

Parents insuring on kids will never understand this article, nor the agents working to trap people in such bogus schemes.

I just pity them.

Dear Sats,

Thank you for sharing your views and I totally agree with you.

Most of the LIC agents who leave their comments here are very good at sharing ‘Generic & meaningless’ comments.

I will try my best to spread awareness about the financial products and need support / encouragement from individuals like you. Thank you & keep visiting!

Dear Sreekant Reddy, as you mentioned in your earlier post “I may not be as talented as you are to speak about topics like – LIC Funding Indian Railways.”

So those who are talented let them speak.

You don’t know even if the market crashes LIC has Potential to give it to customers. The corpus fund which LIC has is far more than sum total of all the banks taken together.

If market crashes You are zero in stock market ( that depends on your portfolio, am not opposing to investement in stocks) You should but you should have base which is strong enough to safeguard your future.

Personally I have seen people running from pillar to post for the claim. Recently last month a private firm asking for IT return, family doctor name, last five year medical report etc. Inspite of submitting the required documents for processing the claim. The policy is one year old and inforce, (Find out)

You can have claim settlement ratio may be nearly equal or close to LIC or improved over years. These are statistics and don’t play with statistics.

e.g A new school having 12 kids admitted in first year next year they again get 12 kids. They would say growth rate of school is 100% (as far as statistics studied I know), I am not CFP, just service class common man)

You can play with statistics and common man doesn’t go or dig dip to understand and have proper decision.

I would advice not to take any views form this kind of forum or form any one LIC agent or any.

If you have fully understood what you are buying whether LIC or Private Company. GO for it, Don’t change your decision as you read someones post. After all its your choice. I would advice Mr. srikant, You should review everything pros and cons and let the people decide what to do. You should not critcize and give your decision as mentioned by you earlier ” this plan is meaningless” This is your choice (See deepikas My choice video). Let people decide then it will be your unbiased comment and views.

Dear Shailendra,

If LIC has so much corpus, why are its Term insurance polices so steeply priced? Can’t LIC afford to price them in a reasonable way? as term insurance plans are a MUST for everyone.

I am talented enough to write unbiased reviews on specific financial product. Instead of giving generic statements, you keep it simple. What is your opinion on LIC Jeevan Tarun? (Also, read other comments which are posted by investors lol 🙂 )

Are you give financial planning advice free of cost to your clients????

Dear Srikanth,

As of now, I am not offering FP services (one to one).

What r readers talking here.. seems they are promoting private companies..

Dear Anonymus,

Don’t you think that we are promoting the right life insurance plan that one has to take?? irrespective of whether it is pvt or public 🙂

What do lol ? indicate, is this the good manners by shreekanth Dr Agarwal should answer. Is this the manners by Misguiding public saying meaningless by Mr shreekanth

The writer calls himself knowleagable but does not take into account people with medium income. LIC has not survived for decades just like that.. Misleading..

Dear Anonymus,

There is no need to be an expert to understand how a simple life insurance works. For ex- Term insurance plan.

But to understand a traditional plan like this, a prospective investor / agent should have some knowledge about how they work. Once they understand then I am sure a client/investor do not see any major benefit from plans like these.

A bread winner of a family whose income is MEDIUM may not require to invest in these kind of plans. He/she just needs one simple life cover plan.

Thanks Sreekanth. You really changed my concept on investment and life cover plan. It is really helpful for me.

Glad you find my blog useful … Kindly share the article(s) with your friends 🙂