It’s that time of the year when you have to submit the Investment Proofs (Tax saving investments) to your employers. It is also the right time for some Life Insurance / Financial advisors to mis-sell financial products.

Recently LIC of India has launched a new plan called, LIC Limited Premium Endowment plan. Without any doubt, this plan is creating quite a buzz in the market. The unique selling point (feature) of this plan is “pay premiums for limited period and get risk coverage for the entire policy term.”

Let’s do the calculations and analyze the returns of LIC Limited Premium Payment Endowment Plan. Let’s find out what this plan has to offer, high returns or low returns??

Limited Premium Paying Terms:

As I said, the main feature of this plan is Limited paying term. For example, if you opt for 21 years policy term and 8 years as PPT (Premium Paying Term) then you need to pay the premiums for 8 years only. The risk coverage will be available till the maturity of the policy (i.e., 21 years).

This plan offers the following options with respect to Policy Terms and Premium Paying Terms.

- Policy Term as 21 years and PPT as 9 years

- Policy Term as 21 years and PPT as 8 years

- Policy Term as 16 years and PPT as 9 years

- Policy Term as 16 years and PPT as 8 years

- Policy Term as 12 years and PPT as 9 years

- Policy Term as 12 years and PPT as 8 years

Now that you are clear with Policy term and PPT, let us analyze the Returns on Limited Payment Endowment Plan.

Returns of LIC Limited Premium Endowment plan

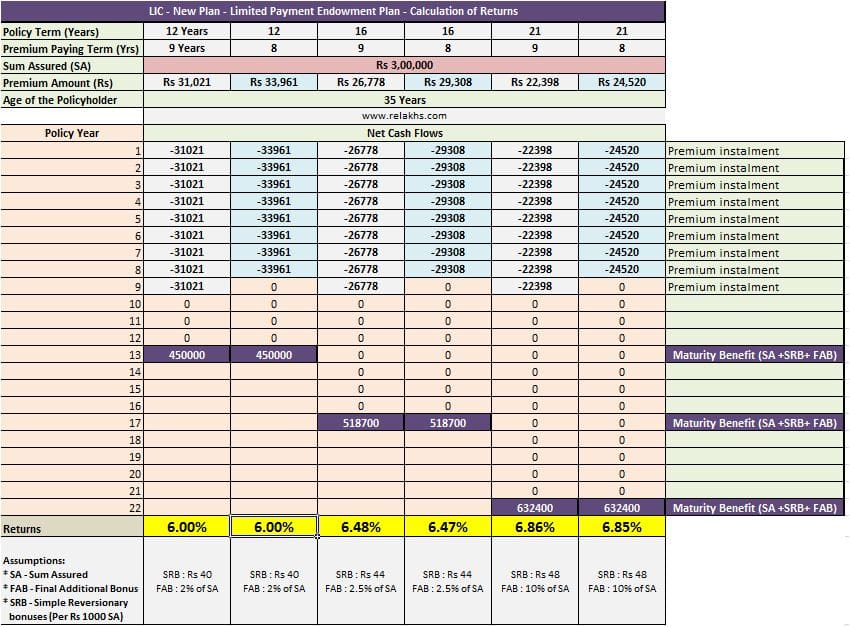

Let us consider an example, MR Gupta (35 years) wants to invest in LIC’s new plan Limited Premium Payment Endowment policy. He is not clear as to which is the best combination (policy term and PPT). He wants to calculate return on investment under various combinations of Policy and Premium Paying Terms. (Click on the below image to open it in a new browser window).

If Mr Gupta opts for Policy term of 12 years and PPT as 9 years, premium is Rs 31,021. Under this option he has to pay the premiums for 9 years. In the beginning of 13th year he may receive the maturity benefit of Rs 4.5 Lakh ( inclusive of Sum Assured, accrued bonuses and final additional bonus). The expected return on his investment is around 6%.

Like wise, Mr Gupta will get returns in the range of 6% to 7% under different options of LIC limited Premium endowment plan.

Assumptions:

- The returns are very much dependent on the bonus rates ( Simple Reversionary and Final Additional Bonuses) that LIC declares every year.

- I have assumed SRB and FAB (provided in the above table) based on LIC’s bonus rates for 2014-2015.

- Generally LIC do not pay FAB on policies that have less than 15 years as the term. So, we need to wait till next year to know the actual bonus rate for a plan which has 12 years as Term. But I have considered 2 % of SA as FAB.

I am sure you are now very clear on how much returns can we expect from these kind of endowment policies. Returns of 6% to 7 % that too over a period of 12 to 21 years sounds very low for me. Kindly be aware of financial products before you buy. Let me know your views. Do share your comments. Cheers!

(You may like visiting my post on “LIC Limited Payment Endowment Plan – Features & Graphical Presentation”)

Join our channels

Dear Sreekanth,

I have an LIC Endowment Assurance Policy – Limited Payment (T.No. 48),started on 28/12/2002 and maturing in 2022. All Premiums Paid(Total 2 lakh rupees in 5 years) . Last transaction was on 27/06/2008 . Sum assured was 3 lakh and now online it is showing a vested bonus of Rs.198000. I wish to surrender this policy and want to take an online term plan . I am planning to invest balance amount in an equity fund.Is it a wise decision ? How much money can I expect now? OR I should continue till 2022 ? Please advise.

Dear KUMAR ..IF premium paying term is over and also only 5 years remaining (out of 20 year term), suggest you to just continue with the LIC policy.

But do take a new Term insurance plan at the earliest.

Read:

Best Term insurance plans

Best Personal Accident insurance plans

Hello Sreekanth,

I have taken a LIC Endownment Plan (table no. 14) in 2010 at the age of 28. There are 7 policies, each sum assured 2L and term is 20, 22 , 24, 26, 28, 30 and 32 yr with total premium of 51k yearly.

1. As the total insurance is only 14L which I feel very very low. So I am thinking of taking a term insurance

2. The return of above policies are 9% (as my LIC agent informs) which i feel is very low.

As these policies are taken for tax benefits and as a investment for long term but now when I studied them thoroughly about the insurance cover and returns I am thinking of surrender these policies and take a term insurance and reinvest the remaining amount (from premium which I need to pay every year) in good mutual funds or equities for better returns.

The surrender value of all these policies are @1.3L only. 🙁

Is it advisable to surrender theses policies and reinvest the money to get better returns?

Please suggest me ASAP. Your advise is valuable.

Thanks and Regards,

Deepali

Dear Deepali,

The returns can be less than 9%, may be in the range of 4% to 6% (Example – Kindly read my review on LIC New Endowment Plan).

It is advisable to book losses and do not COMPOUND your mistake. (You may make them PAID-UP too).

Kindly go through my article – How to get rid off unwanted insurance? to understand about PAID-UP option.

Also go through this – Best online term insurance plans.

Hi Sreekanth,

Thank you for your reply.

I am working woman but now took a break since last 1 year ….

If I surrender my endownment policies, can I apply for term insurance?

Also, My hubby has 4 similar policies and decided to surrender these and take a new term insurance policy.

As I come to know if anyone surrender any LIC policy, LIC will not allow to take a new policy for next 3 years. Is it correct?

Is this rule applicable for other insurance companies also? I mean if my husband surrender his LIC endownment policy and want to take a new term insurance from ICICI direct or HDFC security, is it possible?

Thanks and Regards,

Deepali

Dear Deepali,

Yes, you can surrender your policies and also apply for term insurance. But, suggest you to first buy a term plan and then surrender your policy.

Since you are not working now, getting a term plan cover (for sum assured of say more than Rs 25 Lakh) may not be possible.

It is not true, it is just a misconception. Why do you want to buy a life insurance policy through hdfc security? Try buying a termplan directly, online.

Hi Sreekanth,

Thank you for your reply.

Yes, I will go for online term policy by comparing LIC, HDFC life and ICICI pro etc.

1. Can you suggest which one is best from these?

2. In online term insurance policy do i need to mention all endownment policy details if i buy term insurance before surrender?

3. If I surrender the policies first, do i need to mention these policy details in application form of term insurance?

Thanks and Regards,

Deepali

Dear Deepali,

1 – All three are good, you may choose any one out of them. Kindly go through my article on Best term plans.

2 – Yes

3 – Not required.

You have done a good thing in bringing out the real yield on this endowment plan.

In my opinion, IRDA should not allow any kind of life Insurance product other than Term Plans. Endowment, money back and on top of them ULIP – all these rip off gullible investors. But they are aggressively promoted by agents and banks without being honest about real returns and the gargantuan expenses (in the case of ULIPs).

S.K

Dear S.K.

Thank you for sharing your views. Let there be all types of plans. Advisors/agents should clearly explain the pros & cons of products to investors/clients. For this to happen, they should be trained well. IRDA can streamline the commission structure 🙂

Form investors side, he/she has to do some homework before buying an insurance product. Many investors (who are well educated) do not even know what type of insurance are they buying, what is the sum assured….Let us hope this will change. From my side, I am doing my bit by providing unbiased information here.

HELLO SIR,

I AM AN LIC AND GIC AGENT I REALLY AGREE TO YOUR COMMENT ABOVE AND I DO FEEL EVERY TIME WE SHOULD KNOW ABOUT FINANCIAL PLANNING BECAUSE JUST LOOKING FOR COMMISSION ONLY IS NOT SATISFACTORY. CAN YOU SUGGEST ANY SHORT TERM FINANCIAL PLANNING COURSES FOR AGENTS.

WE REALLY CARE FOR OUR CLIENTS

THANK YOU

Dear SARIKA,

I believe that more than academics the intentions of Advisors/agents are important.

Knowledge can be acquired in many ways.

If you are interested in doing CFP (Certified Financial Planner) course, you may visit fpsbindia.org website to know more details.

You may also reach me through the Contact page of this blog.

Thank you..

Will surely contact you

I feel that is one of the so much important info for

me. And i’m satisfied studying your article. But want too stgatement oon few general things, The website style is ideal, the articles is truly great : D.

Juust right process, cheers

Hi Sreekanth,

Could you advise me about returns in SBI life insurance smart performer plan. PPT is five years (50000 per year) and policy term is for ten years.

Thanks a lot.

Suresh.

Dear Suresh,

SBI Life’s Smart Performer plan has been withdrawn. It is a ULIP (Unit Linked Plan) with an option of single or limited premium payment. The returns are dependent on the type of FUND that you have choosen. You can check the current NAV (Net Asset Value) and analyze the current returns.

Under this plan, Death benefit would be “higher of Sum Assured or Fund Value. The minimum death benefit would be 105% of premiums paid.

Maturity Benefit is : The fund value as on maturity date or as per guaranteed NAV will be provided to you.

(Smart Performer is a NAV based plan wherein there is minimum guaranteed NAV which is equivalent to 5% more than highest NAV achieved recorded in the first 7 years from the launch of product)