PPF and NSC are the most popular long-term saving instruments in India. The amount invested in these instruments is eligible for deduction up to Rs 150,000 under section 80C along with other eligible investments.

The Govt. of India has recently revised investment rules relating to the investments by the Non-Resident Indians (NRIs) in the select Small Savings Schemes – PPF (Public Provident Fund) and NSC (National Savings Certificates).

As per the new amendment done to PPF Act, “account holders of the Public Provident Fund (PPF) account shall be deemed to be closed the day their residential status changes to NRI.”

Latest update (23-Feb-2018) : The Govt’s notification dated 3-Oct-2017, regarding closure of PPF accounts held by NRI has now been put on hold. The Govt has issued a latest notification on this as below. So, NRIs who currently hold PPF accounts can continue their investments in PPF accounts until further notice (if any). As per the new notification it has been simply been put on hold.

A separate notification has also been issued in respect of the National Savings Certificate (NSC), which states that an NSC is deemed to be encashed on the day when holder becomes an NRI.

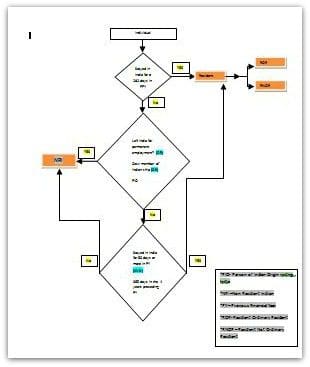

Who is considered as an NRI? – A person is considered resident in India, if he is in the country for 182 days (or) 60 days in a year and 365 days in each of the preceding four years as per Income Tax Act. When a person doesn’t satisfy both these conditions, he/she is termed as NRI.

Below is the Flow chart to know if you are an NRI or Resident. (Kindly click on the image to download the flowchart.)

(Related Article : ‘How to know your Residential Status? Online Residential Status Calculator‘)

If your Residential status is NRI and you have made investments in PPF and/or NSCs then you need to be aware of the below revised rules.

Latest NSC & PPF rules for NRIs

NRI investments in PPF

- Existing rule : NRIs cannot open a new PPF account in India. However, they were allowed to keep contributing to their existing PPF accounts as per a 2003 notification. This was for the PPF account they opened prior to becoming NRIs.

- New rule : “If a resident who opened an account under this scheme subsequently becomes a non-resident during the currency of the maturity period, the account shall be deemed to be closed with effect from the day he/she becomes a non-resident. Interest with effect from that date will be paid at the rate applicable to the post office savings account up to the last day of the month preceding the one in which the account is actually closed.”

- When you become a Non-resident Indian, your PPF account would be deemed closed.

- From the date you become NRI, your PPF would not earn the regular interest rate (current prevailing interest rate on PPF is 7.8%). Do note that the deposits earn regular interest rate till you turn NRI.

- Subsequently, until you actually close the account, your PPF deposits would earn the interest rate of post office saving account only. The current interest rate of PO savings account is 4%.

- For example : Let’s say as a Resident Indian you have have been contributing to PPF scheme. Your residential status has been recently changed to NRI in October 2017. As per the latest PPF Act amendment, your PPF a/c is deemed to be closed in Oct 2017 and your PPF a/c earns 4% as rate of interest on the total accumulation, until the time you actually close the account. (Read : ‘Latest Post office Small Savings Schemes Interest rates for FY 2017-18‘)

Below circular clearly states that this new amendment is not applicable retrospectively. (My sincere thanks to one of my blog readers, Mr Kesavan, for emailing me this circular.)

NRI investments in NSCs

- Existing rule : NRIs can not invest in any of the Small Saving Schemes like NSCs, KVP, SSA etc., However they were allowed to continue with their existing investments in NSCs till the maturity date.

- New rule : It is deemed to be encashed on the day the holder becomes an NRI. Until the time you actually encash NSC certificate, the accumulated money will earn interest at a lower rate, as applicable to Post office Savings Account (which is currently 4% p.a.).

How an NRI can close PPF account?

In case, you are in a foreign country and would like to close your PPF account now, below is the procedure to withdraw funds from PPF account ;

- You need to complete PPF withdrawal form (Form C) and arrange for your KYC Documents (like copy of ID & address proof, cancelled cheque etc.,).

- Along with the above documents, you need to enclose an authorization letter stating that you are allowing your person (relative/friend) to submit the withdrawal forms on your behalf. Post all these documents to your representative.

- Your person has to visit the bank where you have NRE/NRO account. They have to get all the documents attested by the bank official (especially the authority letter). He/she can also get these documents attested by a gazette officer.

- After attestation is done, then your representative can visit the PSU bank for PPF withdrawal.

The above latest amendments will surely impact a large number of NRIs who have made investments in PPF/NSCs. The amendment indicates that such accounts may need to be closed / encashed. Once you return to India and become Resident Indians, you can open a fresh PPF account. (As of now, there is no clarity on whether these deemed to be closed accounts can be revived or not.)

So, what should NRI’s who have PPF and NSC accounts do now with their accumulated corpus? – I believe that NRIs should withdraw their funds in PFF/NSCs immediately (or during their next visit to India) and invest in other suitable/better investment avenues. As an NRI, before you consider any other investment alternative, suggest you to kindly know the current tax rules that are prevailing both in India and foreign country (especially rules related to ‘repatriation’).

Continue reading :

- List of best Investment Options

- What is FATCA compliance requirement?

- What is Double Taxation Avoidance Agreement (DTAA)? Is Income earned outside India Taxable?

(Post published on : 31-October-2017)

Join our channels

I became a non-resident Indian (NRI) in July 2017, when I migrated to the USA.

I was naturalized as a US citizen (OCI) in August 2022.

My NSCs mature in February 2023.

1) Does the 2017 Amendment apply to me? If so, how?

2) How do I encash my NSCs when they mature in February 2024? I am not in a position to visit India in the near future. I do not have a Post Office Savings account. However, I do have an NRO account.

Kindly advise.

Is an Aadhar card necesary while closing a PPF account by a Citizen of Indian Origin? Thanks for your reply.

L. Iyengar

Dear Mr Iyengar,

I believe that it is not mandatory, but you may have to submit a valid ID proof at the time of closing the account.

Dear Sir,

I am an NRI and my NSC got matured recently. I bought the NSC when I was in India. I am not returning to India soon and I want my father to encash the money on my behalf.

The post office is not cooperating and stating that I need to be present to encash the NSC. I read online that legal heir can opt for encashment upon submission of form SB84. I also read all the questions and answers in this section to see if you have already responded to similar questions before but did not find one.

Could you please help me with the encashment process.

Sincerely,

Binesh.

Dear Binesh,

I believe that SB84 form is used only in case of Death of investor for claiming the proceeds by nominee/a relative.

I also believe that you can send an authorized representative with original NSC, signed authorization letter, your bank account cancelled cheque etc., and can get the NSCs encashed.

Hii Shreekant Reddy sir

I have a PPF account from 2013 and I am not NRI, but i want to close my PPF account, sir plz tell me how to close the ppf account

Dear Pramod,

Kindly note that you can close PPF account prematurely only if your account has completed FIVE Financial Years. (This rule is not applicable in case of ‘death’ of the account holder.)

Suggest you to kindly go through this article @ PPF Account Premature Closure : Latest Rules & Eligibility Amount Calculation

Srikanth- Namsthe

My son is NRI from 2008. He opened a PPF a/c in capacity of Guardian of her daugher in 2012 with SBI. PAN Card and Aadhar card was submited at that time. The Ruling for NRIs was not in notice so the NRIs status was not disclosed at that time.Now, he wants to close this account. What shall be the treatment of Interest payable on this account. Please advise.

Regards

Dear Brij Mohan ji,

The Govt Notification (dated Oct 2017) has been kept on HOLD for now. NRIs can continue with their investments for time-being.

Suggest him to keep his PPF ac in active mode by contributing minimum amount every year till further notice or any new notification gets issued.

Confirmation from SBI

https://www.sbi.co.in/portal/web/personal-banking/public-provident-fund-ppf

Thank you dear Omkar, for sharing this link!

Hello,

I am planning to migrate from India soon expected to be in march 2018. I have a PPF account with SBI bank.

will i get my money invested back in hand if i close out the PPF account before i travel abroad by .showing the VISA .

Or is it necessary to Hold a NRE/NRO account to get the encashment. I dont have one now, i am planning to take one once i get all confirmations from my company. But is it possible to encash/withdraw the amount invested in PPF

Dear Rajesh,

I believe they will issue a cheque for the withdrawn balance and that needs to be deposited in NRE/NRO account I believe, as NRIs are not permitted to maintain regular Indian rupee savings account.

Ohkay, so does that mean I cannot encash the cheque without a NRE/NRO account??

I was thinking whether I can use this amount for my travel expenses of this gets encashed before I migrate

Dear Rajesh,

I believe that PO/Banks insist on having Savings account to withdraw the funds. I doubt encashment is allowed.

Hi Sreekanth,

This suspension looks temporary . The intention seems to be to not allow NRIs to invest in PPF . My question is if there is no new development until the first week of April, as an NRI, can I deposit new funds into my PPF account? Should I risk a new deposit given the previous directive of 4% savings rate since the date you become an NRI?

Dear OMKAR,

My suggestion would be not to make any major contributions to your PPF ac, but you may just make minimum contributions to keep it ACTIVE.

You may better off looking out for other alternative investments to PPF.

Hi sir ,

I am an NRI , I open ppf on my wife name on her name she do not have NRI account she has joint aacount with her father . can she continue with ppf or has to close .

Dear Manish..As the account holder is not an NRI, I believe she can continue it.

Hello Sreekanth

I opened a PPF account in 1999, became NRI in 2002. Maturity was in 2014 but extended that to 2019. How will my interest be calculated.

Dear Shelly,

You will get regular PPF interest till Oct 2017, after that till the time you actually close the PPF account you will get around 4% ie prevailing savings account interest rate.

There is further letter on this subject in February 2018.from the authorities.Can you please put this on this blog.

Raghuram.

Dear Raghuramlc ..If possible, can you kindly share it to me??

I am extremely thankful to you for the expert advice which is very prompt too.

I have accessed a letter of GOI No. 5/23-1/2017/35 dt.8-1-2018 from the. Office of the Director, National Savings Institute, New Delhi-2 addresseed to Govt Business Dept., , all Nationalised banks, ICICI, axis ,HDFC, says

” The reduced rate of interest for nri ppf shall be applicable from the date of effect I.e. 3/10/2017″

This will end the confusion re retrospective nature of the notification.

With great regards

R Kesavan

Thank you so much for sharing the circular, much appreciated!

Thanks for sharing the letter details of 8th Jan 2018 letter by the Directorate National Savings Institute, MOF addressed to banks. My bank refuses to have recieved this letter. Can you share this complete letter please so that it can help many readers like me,

Thanks & Regards,

Dear Mr Khosla,

I have uploaded the complete letter in the article.

You may click here to download the same ..

.Dear Sri Srikanth Reddy,

I am posting a problem being faced by a friend in respect of PPF & NRI and seeking a solution through your very helpful blogs.

1. He Joined IT company in India in 2003 . Opened a bank account for getting salary credited and opened a PPF account in post office in Oct 2003.

2. Has been filing income tax returns in India as per rules when employed in India.

3. In 2007 joined an American company & and is in USA as NRI since March /April 2007

4. When income in India became non taxable , has not been filing I T returns in India.

has no assets in India. only has a term deposit (FD) for ₹ 4 lakhs in another bank . In this bank is having a joint SB account ( as second name joint with father)

5. has an Indian PAN card. has been keeping the ppf account alive by depositing some amount every year.

6. The 15 th and final installment in PPF has been paid in May 2017. No more deposit is payable and the maturity value is withdrawable any time after April 2019.

7. The NRI status has not been so far mentioned in the ppf or bank account. The interest accruing in PPF account has also not been shown in US income statements.

8. has no NRO account in India.Now has become citizen of USA in 2017

9. The total credit balance in the PPF account in post office at the end of FY 2016 a 2017 is

₹ 12 lakhs approximately.

10. has also been issued a AADHAR card during visit to India in 2015.This has not been linked to PAN card , PPF account and bank account.

Now planning to visit India sometime in 2018. In view of details provided above

Q1. Is it advisable to visit India after April 2019 , close the PPF account in post office using the AADHAR and PAN card , deposit the maturity proceeds in the bank where earlier salary was being credited, without referring to US citizen status

OR

Declare the US citizen status now , foreclose the PPF account in post office during any visit in 2018 itself, using the US passport and US residential proof, get the money and deposit in a NRO account which can be opened at that time.

Which route will be free of hassles ?

Q2

Once the amount becomes available

1. is it to be reflected in US income statement & how ?

2. What is the procedure involved ?

With best regards

R Kesavan

.

Dear Kesavan,

As soon as your friend became an NRI, he should have updated his residential status with at least at Bank. Maintaining regular Indian Savings account is not permissible.

So, I believe that this is the right and advisable option – “Declare the US citizen status now , foreclose the PPF account in post office during any visit in 2018 itself, using the US passport and US residential proof, get the money and deposit in a NRO account which can be opened at that time.”

Also, Aadhar is not for NRIs and there is no need to link it with PAN.

He can get the credit of withdrawal proceeds of PPF account into the NRO account. And balance in the NRO account can be repatriated abroad up to a limit of USD 1 million per financial year. Of course, he would need to follow certain procedure for such repatriation.

Hi,

Thanks Sreekanth for your blog.

I have opened ppf account in 2012 . As NRI now planning to close account to comply with new rules. Believe I need to have NRO account for money be transferred into. Also has anyone successfully closed PPF at SBI. I will be traveling this month end to India, it will help me if any one has done it.

Thanks,

Hemachandra

Dear Hemachandra,

I have recently received an email from one of my blog readers (as below) who has successfully closed NRI – PPF ac.

He has received regular PPF interest up to Sep 2017 and after that interest @ rate of PO savings ac.

Thank Sreekanth for your update. In that case I will approach SBI to transfer my savings account as NRO account first and then close PPF. Will update you if I am successful