Health Insurance (or) Mediclaim insurance is a must-have for all. Considering the rate at which medical costs are rising, it is very important to have sufficient medical insurance coverage. The medical inflation in India is increasing at a significant rate almost 12-15 per cent every year. Therefore, it is critical to have an adequate health cover, it is even more important for senior citizens.

Absence of health insurance can wipe out your savings. Having sufficient coverage will safeguard you and your dependents from getting into financial crisis during hospitalization or critical illnesses’ treatments or accidents.

Besides medical coverage, health insurance plans can provide Tax benefits to you. The premium paid towards medical insurance is tax deductible under section 80D of the Income Tax Act, 1961.

You can claim tax deductions, provided you are paying the premium on a mediclaim policy which is in the name of

- Yourself (and / or)

- Your Spouse (and / or)

- Your Parents (Parents need not be dependent on you) (and / or)

- Dependent Children

Section 80D | Health Insurance Tax Benefits | Budget 2018 Proposals

In the union budget 2018, the government of India has proposed the below changes with respect to deductions available on Health Insurance and/or towards Medical treatment ;

- Health Insurance & Senior Citizens : In Budget 2018, it has been proposed to raise the maximum tax deduction limit for senior citizens under Section 80D of the Indian Income Tax Act 1961. The current limit of tax deduction allowed for FY 2017-18 for senior citizens is Rs. 30,000 which will be increased to Rs 50,000, from FY 2018-19 (AY 2019-20) onwards.

- Under Section 80D an assessee, being an individual or a Hindu undivided family, can claim a deduction in respect of payments towards annual premium on health insurance policy, or preventive health check-up / medical expenditure in respect of Senior citizen (above 60 years of age).

- As of FY 2017-18, only Very Senior Citizens (who are above 80 years of age), can claim a deduction of up to Rs 30,000 incurred towards medical expenditure, in case they don’t have health insurance. The Budget 2018 has increased this to Rs 50,000 and also allowed the same flexibility to senior citizens. Even individuals who pay premiums for their dependent senior citizens parents can claim the additional deduction on health insurance premium (or) medical expenditure

- Single premium Health Insurance policy / Multi-year Mediclaim policy :

- In case of single premium health insurance policies having cover of more than one year, it is proposed that the deduction shall be allowed on proportionate basis for the number of years for which health insurance cover is provided, subject to the specified monetary limit.

Tax deduction of Health Insurance Premium (Section 80d)

Below table has the list of quantum of tax deductions applicable on health insurance premiums. The below limits are applicable for Financial Year 2017-2018 (or) Assessment Year (2018-2019).

Budget 2018-19 & Revised limits u/s Section 80D for FY 2018-19

Health insurance premium paid for Self, Spouse or dependent children is tax deductible upto Rs 25,000. If any one of the persons specified is a senior citizen and Mediclaim Insurance premium is paid for such senior citizen then the deduction amount will be Rs. 50,000 from FY 2018-19 (AY 2019-20).

The below revised limits are applicable for Financial Year 2018-2019 (or) Assessment Year (2019-2020) u/s 80D.

Medical Insurance Premium & Section 80D | Examples

Let us understand the above scenarios with couple of examples..

Example 1 : Mr Reddy (35 years) has employer’s mediclaim coverage. He pays Rs 15,000 as premium. The coverage is applicable for Mr & Mrs Reddy and their son. He has also included his parents (father 55 years & mother 52 years) under his employer’s medical insurance scheme. For parents coverage he pays Rs 20,000. He has also incurred Rs 8,000 for preventive health check-ups towards his family. He wants to know how much he can claim as total tax deduction under Section 80d?

Since no one in the family has attained 60 years of age, Mr Reddy can claim a tax deduction of Rs 40,000 (Rs 15,000 + Rs 20,000 + Rs 5000).

Example 2 : Mr Saxena (45 years) is a self-employed person. He has taken Health insurance plan and pays a premium of Rs 26,000. He also pays Rs 61,000 towards his parents’ medical treatment ( his Father’s age is 72 years & mother’s age is 68 years). What is the total tax deduction application in his case?

Mr Saxena can claim a total tax deduction of Rs 75,000 only (Rs 25,000 + Rs 50,000).

Preventive Health checkup & Section 80D | Example

Preventive health checkup (Medical checkups) expenses to the extent of Rs 5,000/- can be claimed as tax deductions. Remember, this is not over and above the individual limits as explained above.

Example – Mr Mehta (65 years) has a mediclaim policy and paid Rs 55,000 as premium . He also spent Rs 6,000 towards health check-up. He wants to know what is the total tax deductible amount?

Since he is a senior citizen, the medical insurance premium to the extent of Rs 50,000 can be claimed as tax deduction under Section 80D. Even though he incurred Rs 61,000 ( Rs 55 k + 6k) as expenses, he can claim tax deduction to the extent of Rs 50,000 only.

Multi-year Health Insurance policy & Section 80D | Example

If you prefer to pay insurance premiums for multiple years in one year itself (you may get discount on premium rates), the deduction shall be allowed proportionately over the years for which the benefit of health insurance is available (subject to the overall monetary limit).

For example : Mr Rahul (30 years) wants to buy a mediclaim cover for self. He finds out that the premium rate is Rs 20,000 per policy year. However, the same plan is available at the rate of Rs 38,000 p.a. for two policy years (a discount of Rs 2,000). So, he buys a multi-year plan and pays the two years premium in one financial year itself. He wants to know what is the total tax deductible amount?

As per the current rules (FY 2017-18), you are only allowed to claim a deduction in the first year that too up to Rs 25,000 only. As per proposals in the 2018 Budget, Rahul would be able to claim the total premium paid, proportionately, over the 2-year period, which would mean a tax deduction of Rs 19,000 p.a. in both the financial years.

Standard Deduction in-lieu of Medical Allowance – Budget 2018

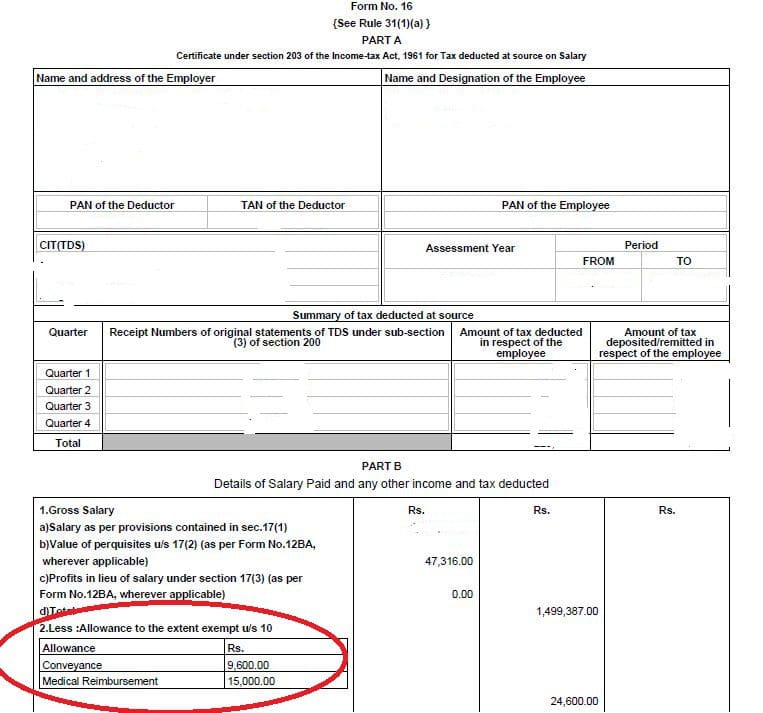

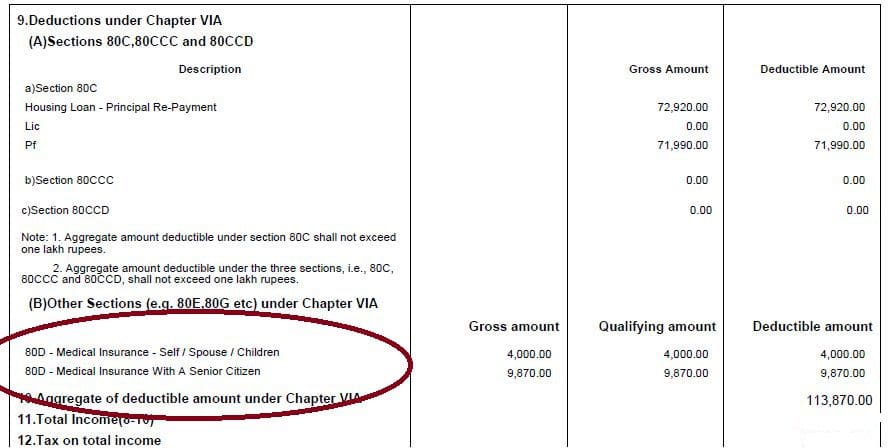

Currently (FY 2017-18), you can get medical allowance of upto Rs 15,000 as an exempted income from your Gross salary. To claim this, you need to submit medical bills to your employer and get the allowance benefit. The medical reimbursement allowance is exempted under Section 10 of the Income Tax Act.

If you have submitted medical bills (to your employer) towards medical allowance and also paid premium towards your mediclaim (health insurance) then both of them will be listed in your Form-16 under different sections as shown below (click on the images to open them in new browser window).

From FY 2018-19, a standard deduction of Rs 40,000 in lieu of travel, medical expense reimbursement and other allowances has been proposed for salaried employees and pensioners. To claim this standard deduction, there is no need to submit medical bills to your employer.

As per proposal, irrespective of amount of taxable salary the assessee will be entitled to get a deduction of Rs.40,000 or taxable salary, whichever is less. Thus suppose if a person has worked for few days (or) months and his salary was just Rs 40,000 for a previous year, then he will be entitled to deduction equal to salary being the same amount. If his salary is less, say Rs 30,000 the deduction shall be restricted to Rs 30,000. If salary exceeds amount of Rs 40,000, the deduction shall be restricted to Rs 40,000.

Important points on Medical insurance policies & Tax benefits

- You can claim tax deductions on mediclaim plans provided by your employer or on policies taken by you (independent of your employment). The tax deduction is applicable on both health insurance and mediclaim policies.

- Premium amount can not be paid in cash. Mode of payment can be anything (through credit card, net banking etc.,) except cash payment.

- You can take medical insurance policy on your dependent children and claim tax deductions too. If they are aged above 18 years and employed then they can not be covered. Male children if not employed then they can be covered upto 25 years. Whereas, female children can be covered until she gets married (only if she is unemployed).

- If you are paying health insurance premiums of your in-laws then you can not claim tax deductions. However your spouse can pay the premiums from her taxable income and get the tax benefits.

- If you are paying medical insurance premiums on behalf of your sister or brother then you can not claim tax deductions.

- Only premium amount can be claimed as a tax deduction. Do not include the service tax amount.

- If you have bought a life insurance policy with a Critical Illness rider then Tax deductions on premiums paid towards critical illness rider can be claimed under Section 80D.

A word of Advice : Kindly note that having a health insurance plan is not the end of your ‘medical insurance’ planning. In fact, it is your first-line of defense only. Considering the ever-increasing medical treatment expenses in India, you have to plan for a mediclaim /family floater + a Super top up plan + an Emergency fund for unforeseen consequences. Don’t depend entirely on health insurance plan alone!

Continue reading :

- Difference Between Individual (Personal) & Employer based Health Insurance Plans – Pros & Cons

- Latest Health Insurance Incurred Claims Ratio 2016-17 | IRDA Annual Report | Top Health Insurance Companies 2018

- 11 vital factors to consider when choosing the Best Health Insurance Plan!

- Best Health Insurance Comparison Websites / Portals

- Should NRIs buy Health Insurance in India?

- Income Tax Deductions List FY 2018-19 | List of important Income Tax Exemptions for AY 2019-20

(Image courtesy of digitalart at FreeDigitalPhotos.net) (Post published on : 27-February-2018)

Join our channels

Hello Sreekant,

One of my colleague has paid an amount of Rs.68,669.76 on 24th April 17 towards Apollo Munich Health insurance for a period from 24th April 17 to 23rd April 19 & he has claimed Rs.25,000/- for the income tax for FY 17-18 under Sec 80D. Since the period of insurance is till 23rd April 19, is the same paid amount can be considered for FY 18-19? Does the premium paid is towards the period of the insurance or the year of Payment??

Dear Ramakrishnan,

Its the year of payment which matters for tax benefit claim..

However from FY 2018-19 (if you have taken a multiyear policy and paid premium in FY 2018-19)..

In case of single premium health insurance policies having cover of more than one year, it has been proposed that the deduction shall be allowed on proportionate basis for the number of years for which health insurance cover is provided, subject to the specified monetary limit.

Hey Sreekanth, thanks for sharing such a great post on health insurance tax benefits.

Dear Mr. Sreekanth,

I have to renew my health insurance (SyndArogya Family Floater Health Insurance Policy) soon. I would like to pay the premium using my wife’s credit card (for reward points) and later repay the dues to the card by cheque.

My query is, Will I still be eligible to claim rebate under Section 80D under my returns? Or will my wife only be allowed to claim the rebate? Please clarify.

Dear Pawan,

I am not sure on this!

To keep it simple! Isn’t it better to pay the premium through your cheque and claim tax benefit.

Related article :

Income Tax Deductions List FY 2018-19 | List of important Income Tax Exemptions for AY 2019-20

Hi Sreekanth,

I have availed mediclaim policy for my in laws (both are senior citizens) Rs. 36000/-. To my surprise this time, my employer did not give me tax rebate for this policy stating that this exemption is not applicable for Parents in law and only

for parents.

I did some research on net whereby it seems to be correct.

My wife is also working and is a tax payee, my query is can my wife claim rebate under 80d for the policy premium being paid by me since it is for her parents.

Kindly advise

Dear Sumit,

If you are paying health insurance premiums of your in-laws then you can not claim tax deductions. However your spouse can pay the premiums from her taxable income and get the tax benefits.

“Tax deductions on payments towards health insurance can be claimed under Section 80D of the Income Tax Act. This deduction is available on premiums paid towards policies for self, spouse and dependent children. However, it does not extend to a health policy for the in-laws. You could consider asking your spouse to pay for premiums on this policy, which insures their parents to claim the tax deduction.”

Hi Sreekanth,

I have purchased health insurance policy for 2 years which is amount of RS 20000 ,can I claim tax benefit in single year?

Thanks,

Shahnawaz

Dear shahnawaz,

You can claim in single year only (the Financial year in which you have paid the premium).

Is it Medical reimbursement claim in Health Insurance Policy, taxable ? please let me know.

Dear Mallik,

Medical reimbursement of over Rs 15,000 is taxable in the hands of an employee. So the excess amount reimbursed to you shall be included in your salary income for calculating tax.

There is no express provisions on taxability of proceeds received in case of a health insurance policy. However, there is a prevailing view that the claim settlement received by you may not to be treated as taxable, being a reimbursement of medical expenses incurred by you.

(Kindly note that with effective from FY 2018-19, a standard deduction of Rs 40,000 in lieu of travel and medical allowances has been proposed for salaried employees and pensioners.)

Related article : Rs 40,000 Standard Deduction from FY 2018-19 | Does it really benefit the Salaried?

WHAT IS THE DIFFERENCE BETWEEN OF EMPLOYER MEDICAL HEALTH SCHEME ( IN THIS SCHEME EMPLOYEE GETS CASHLESS TREATMENT DURING SERVICE & POST RETIREMENT) HERE ON RETIREMENT ONE MONTH BASIC PAY PLUS DA DEDUCTED ON RETIREMENT AND MEDICAL HEALTH INSURANCE SCHEME . PLEASE CLARIFY IN DETAIL ,IN BOTH CASES INCOME TAX REBATE IS AVAILABLE ON DEDUCTED AMOUNTS.

Dear VIPAN,

Employer provided coverage can be a group cover.

Whereas, one can take a stand-alone mediclaim to cover self and/or family members.

The premiums paid to both can be claimed as tax deduction u/s 80d, subject to threshold limits.

Related article : Difference Between Individual (Personal) & Employer based Health Insurance Plans – Pros & Cons

I have 83 years mother in my parental house at another location. I am sending her monthly money towards day to day expenses plus medicines. Can I claim 50000/- under 80D towards these expenses. I did not bother to collect Medicine purchase receipts so I don’t have any.

Dear swami,

You can claim up to Rs 50k toward medical expenditure incurred on your very Sr citizen mother. But, the bills need to be maintained I believe..

These bills can be towards medical checkups and treatments.

Dear sir

I am a senior citizen 67 Years old. I incur about Rs.4000 for my diabetic medicines every month.I have doctor prescriptions and medicine purchase bills. Can I claim Tax rebate Under section 80D.I donot have any Health Insurance policy.

Pl answer

Regards

Vishwanath.M.N

Dear Vishwanath ji,

The Income Tax Act does not define medical expenditure. Chartered Accountant Naveen Wadhwa, DGM, Taxmann.com says, “Deduction for medical expenditure was introduced by the Finance Act, 2015 for super senior citizens (aged 80 years and above). It was further extended to senior citizens (aged 60 years and above) in Budget 2018 who were usually not covered under any health insurance policy.

Though medical expenditure is not defined anywhere in the Act, but going by the motive, medical expenditure should cover every medical expense whether or not these expenditure are covered under any health insurance policy. Therefore, you can say that expenses such as consultation fees, medicines, hearing aids and so on can be claimed as deduction.”

You may kindly go through this Economic Times article…

I am 63 years old retired person with no disease.I want to take one medical policy which will cover my medical and hospitalisation expenses up to 1.00 lakh in a year.Request you to suggest better options.Thanks

Dear Anil ji,

You may kindly go through below articles ;

* Health insurance Plans for Parents or Senior Citizens

* 11 vital factors to consider when choosing the Best Health Insurance Plan!

* Best Health Insurance Comparison Websites / Portals

Kindly note that features of each plan may vary, suggest you to kindly go through them in detail..

Hi Sreekanth,

I paid the premium for the Cancer Cover policy of my Wife, who is a housewife but has interest and dividend income (below taxable limits). We file the return for my wife, though she does not have income exceeding the taxable limit. My query is can I claim deduction u/s 80D (subject to maximum limit) towards the premium paid by me for my wife??

Dear Ketan..Yes, you can claim tax deduction in your ITR.

Hi Sree,

Please help me in term of new income tax rule

1.) If the central government abolish the Medical reimbursement (Allowance) + conveyance Allowance from income tax and they have given 40000/- exemption in place of this.

My question is if 40000/- has been exempted (including conveyance allowances) then employee can avail car lease ? because in last financial year there were norms that those employee who will avail car lease than we (company) cant give the conveyance allowances but in this Financial year government has given by default in this case employee can get such perquisite ? please clear the concept.

Dear Harinath,

I am not sure about the link between Standard deduction of Rs 40,000 and Car lease perquisite. Suggest you to kindly consult a CA.

Related article : Rs 40,000 Standard Deduction from FY 2018-19 | Does it really benefit the Salaried?

Dear Mr. Reddy,

Myself Ravindra jain aged 65 years have paid a premium of Rs. 31705.00 towards family Medicare plan UIIC. Can I claim additional deduction of Rs. 18295.00 towards medical expenses incurred by me for general medical treatment u/s 80 D plus additional Rs. 5000.00 towards PHC check ups. i. e total Rs. 55000/=.

Dear Ravindra ji,

Yes, you can claim up to Rs 55k as mentioned above.

Really valuable website.

Hello Sreekanth,

Please clarify my following doubt.

Does 80D claim for Medical expenditure/bills will be there in FY 2018-19 also or will it be removed because of standard deduction of Rs 40000. Can one claim both i.e. standard deduction of Rs 40000 and actual medical expenditure (what will be the max limit).

Like in FY 2017-18, one can claim upto Rs 15000 as medical expenditure under sec 80D.

Dear Rahul,

Medical allowance (submission of bills to employer) is different to tax deduction u/s 80D.

Mediccal allowance of up to Rs 15,000 can be claimed by submitting bills to employer. This is applicable for FY 2017-18.

From FY 2018-19, medical allowance will be replaced by Standard deduction. No need to submit medical bills.

I am holder of mediclaim policy. I pay mediclaim premium through cheque only. I have receipt from oriental insurance with stamp and indication of my cheque number. I have provided my bank statement also which clearly show that against that specific cheque number, amount is deducted from my account. But I am asked for providing special certificate which indicates that this premium is paid through cheque and entitled for tax deduction under section 80D.

As far as my understanding, it is sufficient if receipt indicates that it is paid through cheque for getting tax benefits. Please suggest.

Dear Tushar,

Yes, your understanding is correct.

What is special certificate? Is this being asked by your employer?

In case, they do not consider your premium payment as valid, you can claim it u/s 80d when filing your income tax return.

Plz suggest me best way to buy Health Insurance means mode of buying i.e. From directly Insurance company or from any agent or from any website like coverfox, policybazar. Also give your valuable reviews on Max Bupa Health Companion Refill & Apollo Munich Optoma Restore.

Also inform impact while claims if office of insurance company or agent not available in your city.

Thanks a lot

Dear ANAND,

Advisable to go through the respective plan features, premium rates and Plan exclusions and then kindly take decision.

You may go through below articles, can be useful ;

Important factors that need to be considered when buying a health insurance plan

Best portals to compare medical insurance plans

Today an agent may be with you or insurer branch may be available in your location but what is the guarantee of they being available in the future.

So, I dont think this is a major factor while taking the final decision.

Plan Features, hospital network, policy exclusions, copay clause, premium rates etc can be given higher importance.

I am a Senior Citizen holding a group health insurance cover of IBA for retired bank employees with an annual premium of Rs 33000.This policy covers only hospitalization expenses.My regular medical expenses for domiciliary treatments are not covered by this policy.Can I claim deduction under 80D for the balance eligible amount of Rs 17000 supported by Consultation and Medical bills

Dear Prasad ji,

For senior citizens above the age of 60 years, who are not eligible to take health insurance, deduction is allowed for Rs 50,000 towards medical expenditure.

As you have an health cover, I dont think you can claim the deduction for Rs 17k.

Dear Reddy

Medical expenditure means Can it be Medicine purchase bills only with priscription or should it be hospitalisation.It is not very clear.