Every year, IRDA (Insurance Regulatory & Development Authority) publishes Incurred Claims Ratio (ICR) data in its annual report. ICR is one of important factors that you can consider when buying a health insurance plan.

What is Incurred Claims Ratio (ICR)?

Incurred Claims Ratio is nothing but the total value of all claims paid by the health insurance company divided by the total amount of premium they collected in the same period. Incurred Claims Ratio indicates the company’s ability to pay the claims.

As an example a 60% incurred claims ratio means that for every Rs 1000 of premium earned in a given accounting period, Rs 600 is paid back in the form of benefits (claims). Incurred Claim ratio is the ratio of the claims settled to the premium received.

So, how to analyze the ICR data? Whether a Non-life Insurance company which has say ICR of 110% is better than a company which has incurred claims ratio of say 85%?? Let us now understand this point.

If ICR is greater than 100%, it means that the company has given more money away as claims than what it has collected as premium. This is not good for the company.

If ICR is less than 100% say in the range of 60% to 90%, it means that the health insurance company has given lesser amount as claims than what it has collected. It means that they are making profits.

If ICR is very low say less than 40%, it means that either the company is charging higher premium rates than its peers and making huge profits (or) it has a good pool of low-risk (may be youngsters) profile individuals as clients (or even both).

Hence it is better to be with an insurance company which has neither high nor low incurred claim ratio. I believe that the ideal ratio (percentage) range can be anywhere between 60% to 90%.

The main difference between Incurred Claims Ratio and Claim Settlement ratio is – Incurred Claim ratio is the ratio of the claims settled to the premium received. Claim Settlement Ratio (CSR) is the ratio of claims approved to total claims made (received). The higher the CSR the better. Same is not the case with ICR.

Non-Life Insurance companies provide products under various segments like Motor, Health, Home, Personal Accident, Travel, Marine and other types of Insurances. In this post, we are analyzing the ICR details of Health Insurance vertical only. Also, note that Health insurance plans are primarily offered by Non-life insurers and also by stand-alone health insurance providers.

Non-life Health Insurance Business in India 2016-17

- The public sector General Insurers had collected a total premium of around Rs 19,227 cr during 2016-17, representing a market share of 63% (in Health insurance business).

- The Private sector General insurers had collected a total premium of around Rs 5,632 cr in 2016-17, which is around 19% of the total market share.

- Stand-alone Health insurance companies had collected a total premium of around Rs 5,532 cr, indicating a market share of 18%. The market share of stand-alone health insurers is gradually increasing in the last 5 years.

- The annual growth rate of ‘premium collection’ is around 24%.

- During the year 2016-17, the total PAT (Profit After Tax) of General and Health insurance industry was Rs 845 crore as against a profit of Rs 3,238 crore in 2015-16.

- The public sector companies reported a loss after tax of Rs 2,551 crore against a PAT of Rs 1,499 crore in

2015-16. (New India & National reported profits, whereas Oriental & United India reported losses.) - The private sector insurers reported a PAT of Rs 2,763 crore against a PAT of Rs 1,333 crore in 2015-16 and specialized insurers have reported Rs 606 crore PAT against a PAT of Rs 583 crore in 2015-16.

- Among the eighteen private general insurance companies, while fifteen companies reported PAT,

the remaining three companies incurred losses after tax during 2016-17. - The three insurers which reported losses after tax were Bharti AXA, Kotak Mahindra and Liberty Videocon.

- Among the eighteen private general insurance companies, while fifteen companies reported PAT,

- Whereas, the standalone health insurers reported Rs 27 crore PAT against a loss after tax of Rs 192 crore in

2015-16.- Out of six standalone health insurers, three have reported loss after tax and three have reported PAT during the year 2016-17.

- The three standalone health insurer which reported PAT during the year 2016-17 were Apollo Munich, Religare and Star Health. Apollo Munich, Religare and Star Health reported PAT of Rs 132 crore, Rs 2 crore and Rs 118 crore respectively during the year 2016-17.

- The public sector companies reported a loss after tax of Rs 2,551 crore against a PAT of Rs 1,499 crore in

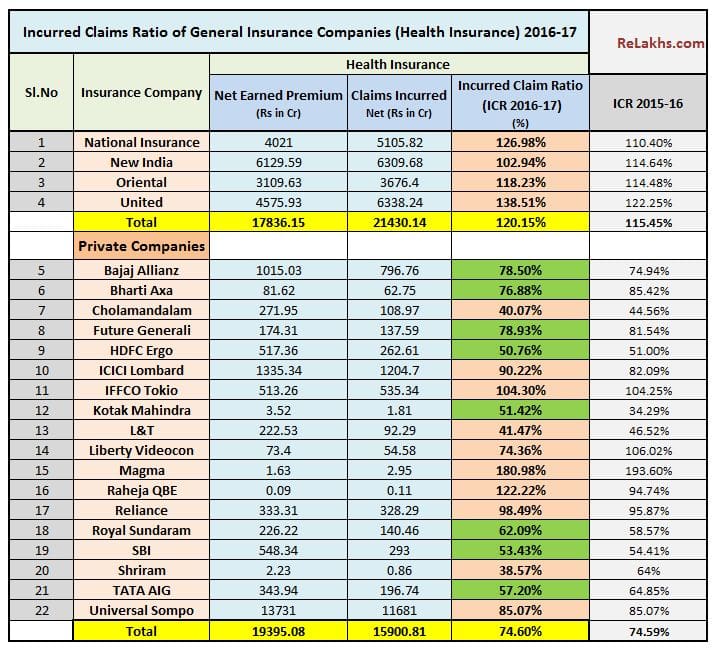

Latest Health Insurance Incurred Claims Ratio 2016-17

- The overall Incurred Claims Ratio of public sector insurer for Health insurance vertical is 120% in 2016-17. This clearly a not a good sign. May be, this is one of the reasons why PSU insurers have increased their premium rates significantly in the last couple of years.

- The overall Incurred Claims Ratio of private sector insurer for is 74% in 2016-17, which is almost same a in 2015-16.

- Whereas, the stand-alone health insurers have a low ICR of around 56%.

Let’s now look at insurer-wise latest health insurance incurred claims ratio 2016-17 details;

Below are the details of Stand-alone Health Insurers’ incurred claims ratio during 2016-17;

- The incurred claims ratio of all four public sector General Insurance companies was more than 100% in 2016-17 as well.

- The incurred claims ratio of the Private Sector non-life insurance companies (health insurance vertical) was 74% during 2016-17 which is same as that of he previous year figure.

- The incurred claims ratio of the stand-alone Health Insurance companies was 56% during 2016-17 which is lesser than the previous year ratio of 58%.

- You can notice that all of the Public sector non-life insurance companies like National Insurance, New India, Oriental & United have Incurred Claim Ratios of more than 100%.

- As far as Private General Insurance companies are concerned, the ones which have reasonable and are close to total average ICR (avg ICR of all Pvt companies is 74.59%) have been highlighted in GREEN. You may prefer buying health insurance policies from these companies.

- All the stand-alone ones or the specialized health insurance companies (except Aditya Birla) like Apollo Munich, Max Bupa, Religare & Star Health have good Incurred Claims Ratio which is around 60%. So, these can be preferred to other ones when buying a mediclaim or family floater health insurance plans.

Top 10 Best Health Insurance Companies based on Incurred Claims Ratio 2016-17

I have analyzed and short-listed the best non-life & stand-alone health insurance companies based on the latest Incurred Claims ratio data.

Actually, Claim Settlement Ratio can be a better indicator than ICR for shortlisting best health insurance companies. But IRDA does not publish CSR details for Health Insurance in its annual report. The CSR details are available in respective company websites.

Below table gives you an idea on aging of claims, settled through both TPA (Third Party Administrator) and In-house;

How to buy best Health Insurance plan/policy?

When it comes to health insurance, there is no one-size fits-all plan that you can rely on. Medical Insurance is a contract based policy with legal jargon thrown in. Besides this, a Health Insurance policy has medical terminologies. Of the numerous medical insurance plans in the market, you may find that each one is unique in some way or the other, with its own benefits and limitations.

The Incurred Claim Ratio (or) Claim Settlement Ratio can help you in shortlisting the best health insurance companies but you have to do a lot of research to identify the right and best health insurance plan which suits your requirements. You have to make a comparison of health insurance plans offered by multiple companies. This is where I believe that health insurance comparison websites could be beneficial.

Kindly note that having a health insurance plan is not the end of your ‘medical insurance’ planning. In fact, it is your first-line of defense only. Considering the ever-increasing medical treatment expenses in India, you have to plan for a mediclaim /family floater + a Super top up plan + an Emergency fund for unforeseen consequences. Don’t depend entirely on health insurance plan alone!

Continue reading :

- Best Health Insurance Comparison Websites / Portals

- 11 vital factors to consider when choosing the Best Health Insurance Plan!

- Difference Between Individual (Personal) & Employer based Health Insurance Plans – Pros & Cons

- Should NRIs buy Health Insurance in India?

- Medical Insurance Premium : Tax Benefits (under Section 80D)

(Image courtesy of fantasista at FreeDigitalPhotos.net) (Post published on : 08-January-2018)

Join our channels

I am a senior citizen of 65 years…I have no major disease ..I want to take health insurance…..I am confused about which health insurance will be suitable for me.. please recommend the best health

insurance for me and remove my confusion..thank you

Mrudula Jani

TAKE A plan which will give you value for money, offer you yearly health check up ( free), no increase in premium if the medical report is adverse with exception to age bracket premium. No claim bonus yearly upto 150% if available, cashless treatment, number of hospitals in India / your locality.

sir we have one policy for your plan is senior citizen red carpet and we do cover all illness after 30 days and your premium same for life long we never change your premium

Dear REDDY,

Thanks for the wonderful Article.

I want to buy a floater family (me+spouse+2 children ) health insurance plan. I am thinking about three companies New India Assurance, ICICI Lombard & HDFC ERGO. Can you suggest which should be the better option ?

Dear Rahul,

Advisable to go through the respective plan features, premium rates and Plan exclusions and then kindly take decision.

You may go through below articles, can be useful ;

Family floater health insurance plans

Important factors that need to be considered when buying a health insurance plan

Best portals to compare medical insurance plans

Dear Sreekanth,

Thank you for the extensive analysis. Really gives a insights on many factors.

I am looking for senrior Citz health insurance and I already went through the blogs you have given for Sr Citz insurance.

I would like to ask your suggestion of choice between Max Bupa and Bajaj Allianz.

Considering premium cost of floater plans (4-5 Lakhs) being very competitive it really makes hard to take a final decision.

The above Table shows the ICR lower for Max Bupa than Baja Allianz. Can I consider this as the major factor as other things things including CSR are almost similar for both.

Dear Laxminarayan,

Companies wise both are doing well.

Is premium of Max bupa plan on the higher side?

Go for a plan that suits your requirements the best.

Kindly read :

11 vital factors to consider when choosing the Best Health Insurance Plan!

No Bajaj allianz is on the higher side compared to Max Bupa.

objective of insurance is the claim guarantee in an event. Claim ratios are best indicators. Bajaj Allianz is good, however, look at other available ones like RELIGARE who offer you medical test every year free, No claim bonus upto 150%, claim ratios are good. choice upto you.

Hi Sreekanth,

My wife and I have L&T, now HDFC Ergo health insurance. We have subscribed to L&T since 2 years now.

ICR of 50.76 is not that bad either. What do you suggest should we switch to different insurance or stick to this?

Dear Zubin,

If you are happy with the product features and meets your requirements, you may stick to it.

Portability is one new feature. You can switch your policies with same or better features with less price to other better performing companies , wherein your OBJECT OF INSURANCEE is SAFE, SECURE, DEPENDABLE, Refer to claim settlement ratios yearly. Most companies do not offer yearly medical health check up free with the lowest premium, with no claim bonus available upto 150%. Customer is king, with Portability coming in.

PF money apply health problem

Dear Ashok,

You may kindly go through below articles :

PF partial withdrawal for Medical treatment

EPF partial withdrawal options & rules