The health insurance plan has become a necessity these days considering the medical inflation. Without a health plan, it is tough to afford the medical expenses. A single hospitalization can create a big hole in your financial kitty. Since it is the need of the hour, this does not mean the decision of buying the health insurance policy should be taken in haste or blindly following your insurance agent.

Let’s discuss the most vital factors which one should consider evaluating them before purchasing a health plan and making a prudent buying decision.

Evaluate these 11 Vital Factors before buying the Best Health Insurance Plan

1. Plan Benefits

Indemnity based health plans offer multiple benefits which include Pre hospitalization charges, Post Hospitalization charges, inpatient hospitalization benefit, day care procedures, domiciliary treatment, maternity benefit, etc. It is imperative to understand all the benefits and look for plans which offer you such base policy benefits plus additional benefits like free health check-ups on renewal, free ambulance services, etc.

2. Sum Assured

Opt for the appropriate amount of health cover or sum assured considering the skyrocketing medical health care costs, the kind of city you live in as metro cities hospitalization costs is more as compared to non-metro locations, check on the room rents and other hospitalization costs, surgery cost, treatment of severe illnesses cost,your budget (as the higher sum assured means higher premium),etc. Taking a holistic view will enable you to opt for the right Sum Assured.

3. Type of Plan

It is imperative to decide on which kind of insurance plan you are looking for. Is it for your own individual self, your family or your parents. There are individual and family floater plans which are offered by almost every insurer selling health plans.It is important to decide on the plan basis your family structure, current health status, any existing diseases, etc.If you have a nuclear family where you and your spouse are in an age bracket of up to 40 years, then getting your family including kids can be covered under a single umbrella plan. In case, you have some medical illnesses or at an advanced age, then it is suggested to go for an individual plan and get your family insured under the different health plan.

(You may like reading : ‘Best Family Floater Health Insurance Plans – Checklist & Comparison’)

4. Co Payment Clause

When you make a claim in your policy, as per the pre-agreed amount or percentage, you have to bear the cost of the claim amount. Some insurers offering you health insurance plans will have a mandatory co-pay clause wherein you are bound to bear the defined percentage of the claim amount on each and every claim. It applies to every claim you file in a policy period.

For Example, if the co-pay clause says 10% to be borne by you so for Rs 100 as a claim amount, your insurer will pay Rs 90, and you have to pay Rs 10 in such scenario.

The health plans with higher co-payment will have lower premiums as the risk, and money is shared between the insured and the insurer whereas plans with no co-payment clause will have higher premiums as the insurer is taking the risk to bear entire amount of the claim.

Read and analyze the co-payment clause of the insurer and decide that in the case of claim will you be able to shed the defined percentage of the agreed claim amount, else it is always suggested to go for plans without a Co-pay Clause.

Source: HDFC Health Assure Plan Brochure

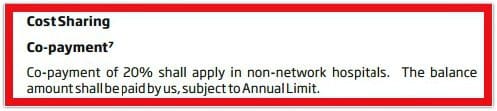

5. Sublimits

Sublimit is a monetary restriction or limiting the upper range for an expense during a claim in a health plan. To put a vigilant eye on the genuineness of the expense, the insurers put a sublimit on certain charges where there is scope of inflating the charges, like insurer may apply sub-limits for room rent charges, doctors consultation fees , ambulance charges , ICU charges etc., which may be restricted to 1% or 2% of the sum assured. Also, some plans have a sublimit on certain surgeries, where the claim is paid maximum to 50% of the Sum Assured.

For example, if your health cover Sum assured is Rs 5 lakh, and your insurer has put a capping on Room rent expenses to 1% of SA per day. Then any expense exceeding Rs 5,000 for room rent will be borne by you.

It is important to check on the sub-limits with a magnifying lens rather regretting at the time of claim. Go for plans with lower sub limits and offering the same benefits.![]()

Source: HDFC Health Assure Plan Brochure

6. Waiting Periods

To wait is the most boring task and to wait to get a benefit is all the more annoying. Health insurance plans waiting period is the prohibited time period where in you cannot claim for any benefits under your plan during that time frame and the insurer will not accept any claim. Different insurers have different waiting periods for different benefits. Most common ones are

- Initial Waiting Period: Where in post taking a policy there is a waiting period clause ranging from 30 to 90 days (as per different insurers). Any claim against your health insurance policy will not be admissible except for the hospitalization expenses due to an unforeseen accident. Such waiting period refrains the person from taking undue advantage from their health insurance as people might take the health insurance immediately post being diagnosed with any illness or disease.

- Pre existing Conditions: There are waiting periods ranging from 2 years to 4 years in the health plans regarding the medical condition which you had before taking the plan.

- Maternity Benefit: The waiting period to get child birth related expenses covered ranges from 9 months to 48 months.

It is imperative to check and opt the health plans offering minimal waiting periods.

Snapshot of Pre existing Disease waiting period with below insurer’s (Max Bupa / Royal Sundaram / HDFC Ergo) under their specific health plans:

7. No Claim Bonus

Bonus word really makes us all happy!! There is a provision of No Claim Bonus in most of the health plans. No claim Bonus suggests that the insurer will provide the bonus in your health plan which will increase the sum assured (without charging extra) or reduce the premium (without changing the sum assured) in an event of a claim free year with the insurer at the time of renewal. Different insurers have a different quantum of this bonus amount. Mentioning few for the reference.

Go for a health plan offering a maximum range of No claim bonus. So before you make a purchase read the section mentioning about the No Claim Bonus and reap the maximum benefits. The intent of this benefit by the insurer is to manage avoidable and small claims on the part of insured in return of No Claim Bonus.

8. List of Network Hospitals

Insurers offer cashless hospitalization in case you get admitted to any one of the listed network hospitals. Before buying a health plan, it is important to look for the list of network hospitals and also check that the nearest hospitals in your area which are offering best of health care facilities are part of the list of your intended insurer or not.

In the case of Planned hospitalization, distance from your home to the hospital may not matter, but in the event of emergencies, it would be sensible to go to the nearest hospital and on the top if it is in the list of a network hospital, it will enable the cashless hospitalization process also. You may check on the insurer’s list of hospitals on their website. Below snapshot suggests the list of Network Hospitals for Max Bupa in Delhi.

Source: Max Bupa’s website

9. Plan Renewability

Renewability of the health insurance plan is another vital factor to be considered before buying a health plan. Discourage plans with limited renewability as limited renewability will be stretched for some years and post that as your age advances it will become difficult to get the health plans as per your choice and premium will also be higher. Also, if you are planning to add your parents under a health plan, then you must opt for lifetime renewability plans only.

Health plans with lifetime renewability clause will be beneficial in the long run which provides renewing the health plan for a longer number of years. Below is the snapshot of individual insurers renewability feature offering Lifetime option.

10. Claims Settlement Ratio / Incurred Claims Ratio

Claim settlement is the ultimate goal of taking a health policy. A good claim settlement ratio (No. of claims paid/ no. of claims received) suggests a good picture of a health insurer in terms of settling the claims. Many of the companies might be offering fancy health plans but if they have a poor claim settlement ratio, then you might face problems in getting your claims settled.

Snapshot of Claim Ratio of various insurers:

(For more details on Latest Incurred Claims Ratios, kindly read : “Claims Ratios of Best Health Insurance Companies in India“)

11. Plan Pricing

Now comes the final determinant which will create an actual influence on the buying decision of health plan to the great extent and that is the PREMIUM of the health plan. Pricing is dependent on various factors such as the age of the insured, type of the plan, benefits, add-ons, health condition, etc. It is better to compare the health plans, premiums before deciding on the final one.

An important point to remember here is that premium is one of the vital factors, but not the only factor. For getting the lowest priced health plan don’t forgo on the benefits and other important features.

Below is the premium specification by different insurers for their specific Medical Insurance Plans for an individual aged 35 years, living in Noida, earning 5 to 7 lakhs p.a.

Various online comparison portals will enable you to compare premiums of health plans of multiple insurers. Take out time for comparison and action appropriately.

Conclusion : These factors need to be check on and understood well to get rid of the claim hassles at the last moment. It is imperative to spend a little time before on gathering information on the vital aspects associated with the health plan and buying the best health insurance plan, rather suffering later.

Its better to be safe than sorry!

About the Author

This guest post has been prepared by Sonia Nagpal, Sr VP (Sales) of Suggestinsurance.com.

SuggestInsurance.com is the online identity for IRDAI approved insurance broker – S B Insurance Brokers Pvt. Ltd. SuggestInsurance.com offers quotes from leading insurance companies and let the customer explore the insurance plans, get their details, view and study brochure and other documents, compare the features and benefits of these plans side by side and then take a prudent decision.

(Kindly note that Relakhs.com is not associated with SuggestInsurance.com. This post is for information purposes only. This is a guest post and NOT a sponsored one. We have not received any monetary benefit for publishing this article.)

(Image courtesy of fantasista at FreeDigitalPhotos.net) (Post Published Date : 02-May-2015)

Join our channels

1. Which is better for health insurance – specialist health insurers or general insurers? And Why?

2, Where can we find the latest important below ratios for each insurer? Even IRDA report does not have all these. I could not find the claim settlement ratio also in the IRDA report !!

1. CSR

2. Persistency ratio

Hi,

Personally, I am comfortable to buy a health insurance from a Pvt insurer, given my perception on better service quality.

You may find the required information @ respective Insurer’s websites

No it is not, at least in many of them. And, even if we ask them they are hesitant to share. Many of us may be aware of the ratios and factors to consider while buying. But, these are not available, accessible and often different websites have different contradicting info.

PolicyBazaar also just keen to sell some random policy which is good in their own perspective (of their some junior call center agent). This is a very sad state of affairs of buying health insurance.

Excellent info – this and all the other articles. Very thankful.

I am currently living abroad and my wife and kid are foreign nationals with OCI status. They have recently moved back to India but I will still be abroad for an year or two. I will be visiting India for every 3-4 months for a stay of about 2 weeks.

Do indian health insurance companies in India provide health insurance for NRIs, Foreign nationals and OCIs etc?

My wife may start working in India soon and she will get health insurance cover from her employer. Do you still recommend having additional health insurance?

Do you recommend family floater or separate ones?

I was told public sector ones are usually good in settling claims and private ones make life difficult during claim settlement. Is that so?

Also, settlement is better when we approach through employer compared to when we approaching as an individual. Is that so? It will be good to include CSR and CIR separately for these segments.

Thank you again for your help.

Hi,

1 – Kindly read :

Should NRIs buy Health Insurance in India?

2 – Yes, not advisable to depend entirely on employer provided cover alone.

Read :

* Difference Between Individual (Personal) & Employer based Health Insurance Plans – Pros & Cons

* Latest Health Insurance Incurred Claims Ratio 2017-18 | Best Health Insurance Companies List

* Top Up Health Insurance Plans – Super Top Up Health Insurance Plans – Details & Benefits

Personally, I prefer opting insurance cover with a Pvt insurer..

Hi Sreekanth,

I am 29 years old unmarried… I want to take a health insurance plan… I am single now, and I would like to take a policy in which I can add my wife and kids (post marriage) in the future… My parents do not need my help as they have cover under Central Govt. Health Scheme under Indian Army… So i just need a health policy for me and in which I can add my future family in a few years… Is it possible? Please suggest…

Dear Bishwadeep,

Yes, you can take a mediclaim policy now and can add members to it and can make it a Family floater plan.

Kindly go through this link..click here..

Thanks a lot Sreekanth… Appreciate your prompt guidance!!!

Dear Srikanth,

I am working and residing at Middle East with my family.Presently I am having a family floater health Insurance with United India Insurance for 3 lakh and to up of another 5 lakh since 2013.

My question are:

1) Can I continue the insurance with this public sector company or shall I use potability option and move it to Cigna TTK insurance Pro health protect plus for 10 Lakhs.My united India premium renewal is in September every year.

2) I would like to take critical illness cover for 15 lakhs for myself Aged 43 and my wife aged 39 from Apollo Munich Optima Vital.I don’t have any family history of critical illness .I don’t have any pre existing diseases.

Regards,

Anil

Dear ANIL,

1 – If you are dissatisfied with them you may consider Porting your policy.

2 – Ok.

Kindly read:

Best portals to compare health insurance plans.

Best Super Top up plans.

Dear Srikath,

Thank you for your reply.

Please advise me whether I have to go for Critical illness cover from a different company as mentioned below or go for a second health insurance.

Regards,

Anil

Dear Anil,

If your family does not have any history of CI, may be you can think of buying a Super Top up plan with very high cover.

We do not know how the future is going to be and the medical profile, so this suggestion is based on your present day inputs.

Kindly note that in CI, a lump sum amount is paid if any of the mentioned CI is diagnosed, its not the case with regular health insurance policy.

Hi,

I’m 34 have LIC Health Plus taken in 2008, now I’m married.

Want to take Health Insurance for my wife.

Having decided to go for Apollo Munich Health Insurance, i have one unclear definition, that it says 1 year insurance plan and 2 year insurance plan.

Does this mean that if I go for the Health Insurance for 1 year plan, I can exhausted or utilize the entire sum assured for one year and if i go for 2 year insurance plan, i can utilize the entire sum assured for two years at stretch.

Please clarify me

Thanks

Dear Karthik,

In multi-year policies, Policyholders don’t have to renew the insurance contract each year as they receive a policy certificate for a maximum of 2 or 3 years cover.

Yes, you can utilize it for 2 years.

HAi sreekanth,

i am suffering from psoriasis for past years, recently in the 2015 year Novartis pharmacital company released medine in injection form which is giving excellent results against this skin problem. but the main problem is one vial itself costing 25,000/- which insurance company can give mediclaim for this type of skin problem. kindly help me sir. presently my age 33

Dear satish,

If you are salaried, you may claim medical allowance by producing bills to your employer.

Also, as it is an pre-existing illness, insurance can be available only after waiting period say 2 to 4 years..

Hi,

I’ve LIC Health Plus taken in January-2009 for 2 lakhs with premium of Rs 6,000 yearly till age 65.

The features in them are incomparable to others (as you know, it gives hospitalisation bed charges for per day basis)

I want to go for a big better facilities, i have zeroed in for Apollo Munich as most of my relatives have got better treatment there and having observed that an Apollo Hospital has its own Health insurance plans. I’m planning to buy one.

I’ll be get married shortly.

I have read about floater plans with their cheap premium and their big cons they hide and so decided to go for individual plan for me and my future extended family.

Question here is..

1) Where to retain LIC Health Plus

2) Keep LIC Health Plus along with new one as the earlier is of lesser premium.

3) Can both Health Insurance polices be used, for maximum benefits

Thanks

Dear karthik,

1 – You may retain it.

3 – You may buy individual policies for self & spouse (in future) if you are not comfortable with floater plans. You may also consider buying a Super top up plan which can be useful.

Read:

Family floater health insurance plans.

Best Super Top up health plans.

Evaluate these 11 Vital Factors before buying the Best Health Insurance Plan

after reading this now i am confuse with so many terms.my personal request is please send a details comparison between top mediclaim plans .so it will be very easier for me to choose the best one.

otherwise please send your choice.

HAI SREEKANTH ,CAN I KNOW IF ITS POSSIBLE TO TAKE A TOP UP COVER OF 10 LACS ALONG WITH 5 LAC INSURANCE IN RED CARPET SENIOR CITIZEN POLICY FOR MY FATHER AGE 67

Dear RAMESH,

I believe that it is possible. Kindly check with STAR insurance too.

Also, Super Top-up policy can be more beneficial.

Kindly read: What are Super Top up health insurance plans?

Very Informative Page1

Sir,

One question

If the claim ratio is > 100% ( I see many in the table published in this blog), how these companies make money?

Dear Srinivas..They make profits from other non-life insurance verticals like Motor, Fire, Home etc,

Instead they just stick to other non life insurance verticals, where they are making money.

In that case, why offer the health insurance plans?

Is there a IRDA regulation to offer life insurance as well?

dear sree

thank you very much for updated usefull details .

and please suggest me which is the best health insurence .

I am 34 years old ,wife 29,Son 4 years having employer insurance 5 lacs with no preexisting illness. I am ok with longer waiting period for preexisting diseases. Which family health insurance suits me best?

Dear Samir,

Kindly go through below articles, can be useful to you;

Best Family Floater Health Insurance plans.

Best Portals to compare Health plans.

Hey Sonia, I think pricing plays a major role, and one has to compare the features before signing up. One should be aware of every feature offered, and should do a homework whether or not, he wants them. This way, he can sort out the best and cheapest option. 🙂

Thanks Mitesh for reading the article. I agree with your viewpoint as well.

Regards

Sonia