Capital asset typically refers to anything an individual owns for personal or investment purposes. It includes all kinds of property, movable or immovable, tangible intangible, fixed or circulating.

Capital assets are further classified as Financial assets and non-financial assets. Financial assets are intangible and represent the monetary value of a physical item. Stocks (Shares) and equity mutual funds are examples of Financial Assets.

A non-financial asset is an asset with a physical value, such as real estate, Gold ornaments, equipment, machinery etc.,

The profit or gain (if any) that you make on your Capital Assets when you redeem or sell them is referred to as Capital Gains.

It can be a Short Term Capital Gain (STCG) or a Long-Term Capital Gain (LTCG) depending upon the ‘Period of Holding’. The tax that is applicable on these profits/gains is known as ‘Capital Gains Tax’.

For example : If you sell your property after 2 yeas of your investment, after making a profit, then the profit will be considered as Long Term Capital Gain. You need to pay LTCG tax @ 20% with indexation benefit.

Related Article : Different Asset classes have different Tax implications – How Returns are taxed?

Besides the capital gains, you can also derive income from salary, pension, interest income on bank deposits, business or profession etc.,

Every Financial Year, you need to declare all such gains and incomes and then have to pay applicable taxes accordingly.

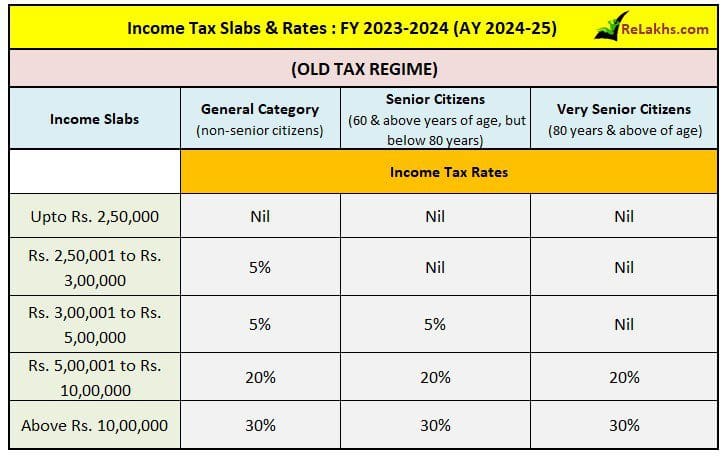

We are all aware on the availability of Basic Exemption Limit of Rs 2.5 lakh, Rs 3 lakh for Senior Citizens and Rs 5 lakh for very Senior Citizens (80+years) under the old tax regime. So, if you have salary income of say Rs 5 lakh, your income of up to Rs 2.5 lakh is not taxable.

When it comes to the New Tax Regime, one cannot claim all major tax deductions and the basic exemption limit is Rs 3 lakhs for all category of individuals.

What if you have made only Long Term Capital Gains and you do not have any other sources of income in a Financial Year? Can you still adjust Basic Exemption Limit against LTCG? Do you have to pay Capital Gains tax even if your total income is less than 2.5 Lakh?

Another scenario can be – What if you have LTCG, salary income and also made some tax saving investments FY 2023-24? How to calculate Long Term Capital Gains tax? What is the correct method of adjusting LTCG against Basic Exemption Limit and save some taxes? Can you claim 80c Tax Deduction against LTCG? – Let’s discuss

How to adjust Long Term Capital Gains against the Basic Exemption Limit in FY 2023-24?

The tax rates on your salary or business income and Capital Gains are not uniform. For example : Your salary income is taxable at applicable tax slab rates. Whereas, say your LTCG on sale of property is taxable @ 20% (with indexation).

So, for calculation of tax payable on salary income and capital gains, you need to bifurcate the claiming process of incomes against Basic Exemption limit. Let’s now understand the rules related to this.

(For the sake of simplicity, we have considered the scenarios under the old tax regime. If you are opting for new tax regime, consider the basic exemption limit as Rs 3 lakhs and may ignore the tax saving provision explained in some of the below scenarios.)

Rules related to adjustment of LTCG against Income Tax Basic Exemption Limit

- The basic exemption limit of Rs. 2,50,000 is applicable on your total income (including the Capital gains).

- If the total income including the LTCG is below the basic exemption limit, then there will be no tax liability.

- A resident individual can adjust the LTCG but such adjustment is possible only after making adjustment of other income. In other words, first income other than LTCG is to be adjusted against the exemption limit and then the remaining limit (if any) can be adjusted against LTCG.

- No tax deduction under sections 80C to 80U is allowed from long-term capital gains.

Adjustment of LTCG against the basic exemption limit – Illustrations

Scenario 1 : Basic Exemption Limit | Example:

Mr. Kapoor (resident and age 25 years) is a salaried employee earning a salary of Rs. 1,94,000 per annum. Apart from salary income, he has earned interest on fixed deposit of Rs 6,000. He does not have any other income. What will be his tax liability for the assessment year 2023-24 under the old tax regime?

For resident individual of age of below 60 years, the basic exemption limit is Rs. 2,50,000. In this case the taxable income of Mr. Kapoor is Rs. 2,00,000 (Rs. 1,94,000 + Rs. 6,000), which is below the basic exemption limit of Rs. 2,50,000, hence, his tax liability will be nil.

Scenario 2 : LTCG, no other income & Exemption Limit | Example:

Mr. Reddy (resident and age 61 years) is a retired person with no income. He has earned LTCG of Rs 3,50,000 on sale of Gold. He does not have any other sources of income. Can he claim Exemption limit on this LTCG and save on Tax?

Yes, he can adjust basic exemption limit of Rs 3 lakh from Rs 3.5 lakh LTCG. He has to pay LTCG tax @20% on Rs 50,000 only.

Scenario 3 : Salary Income, LTCG & Income Tax Exemption Limit | Example :

Smt Suvarna (resident and age 65 years) gets a Pension income of Rs 60,000 and has made an LTCG on sale of property to the tune of Rs 3.5 lakh. What is the correct method to calculate tax liability?

- She has to first adjust her Pension income against Basic Exemption limit.

- The basic exemption limit in this case is Rs. 3,00,000, after adjustment of pension income of Rs. 60,000 from the exemption limit of Rs. 3,00,000 the balance limit available will come to Rs. 2,40,000. The balance of Rs. 2,40,000 will be adjusted against LTCG.

- The remaining limit is Rs 2.4 lakh can be adjusted towards LTCG of Rs 3.5 lakh. Hence, the LTCG tax of 20% is payable on Rs 1.1 lakh only and not on entire Rs 3.5 lakh.

Scenario 4 : LTCG, Tax Saving investment & Basic Exemption Limit | Example :

Mr Shetty (resident and age 40 years) has made an LTCG on sale of Debt Mutual Funds (units bought prior to 01-Apr-2023) to the tune of Rs 3.5 lakh. He has invested Rs 1.25 lakh in ELSS Mutual Fund. Can he claim tax deduction u/s 80c from Capital Gains? What is the correct method to calculate tax liability?

“Capital gains from transfer of units of “specified mutual fund schemes” acquired on or after 1st April 2023 are treated as short term capital gains taxable at applicable slab rates as provided above irrespective of the period of holding of such mutual fund units. A specified MF (pure debt fund) is a fund where not more than 35% of its total proceeds are invested in the equity shares.”

No tax deduction under sections 80C allowed from long-term capital gains. However, he can claim basic exemption of Rs. 2,50,000 and has to pay LTCG on the remaining Rs. 1,00,000 (Rs 3.5 lakh – Rs 2.5 lakh) @ 20%.

Had he bought non-equity oriented units (specified fund) after 01-Apr-2023 then gains are treated as short term capital gains only, irrespective of the holding period.

Scenario 5 : Salary Income, LTCG, Tax Saving investment & Basic Exemption Limit | Example :

Miss Sharmila (resident and age 25 years) earned a salary income of Rs 3 lakh, has made an LTCG on sale of Property to the tune of Rs 5 lakh. She has invested Rs 75,000 in Tax Saving Fixed Deposit. Can she claim tax deduction u/s 80c?

- She can claim Rs 75,000 tax deduction from Salary income. So, her net taxable income becomes Rs 2,25,000 (Rs 3,00,000 – Rs 75,000).

- This income of Rs 2.25 lakh is less than basic exemption limit of Rs 2.5.

- Now since her Total Taxable Income (excluding LTCG) is less than Rs 2.50 Lakh, LTCG would be reduced by the differential amount remaining after claiming the total income under the basic exemption limit (i.e. Rs 25,000 = Rs. 2.50 lakh – Rs 2.25 lakh).

- Thus total LTCG taxable will be only Rs 4.75 Lakh and not Rs 5 Lakh.

(If Miss Sharmila follows the new tax regime, then she cannot claim tax deductions u/s 80c and hence the entire income is liable to taxation.)

Scenario 6 : NRI, Pension Income, LTCG & Basic Exemption Limit | Example :

Mr. Sharan (age 67 years and non-resident) is a retired person earning a monthly pension of Rs. 5,000 from Indian employer. He purchased a piece of land in Delhi in December, 2012 and sold the same in April, 2023. Taxable LTCG amounted to Rs. 2,20,000. Apart from pension income and gain on sale of land he is not having any other income. What will be his tax liability for the assessment year 2024-25 under old tax regime?

” A Non-resident can get the benefit of the basic exemption limit of Rs. 2,50,000 from his/her total income. But note that Non-Resident Indians cannot adjust basic exemption limit against Long Term Capital Gains.”

Mr. Sharan can adjust the pension income against the basic exemption limit but the remaining exemption limit cannot be adjusted against LTCG on sale of land.

The basic exemption limit in this case is Rs. 2,50,000, and the same will be adjusted against pension income of Rs. 60,000. The balance limit of Rs. 1,90,000 (i.e., Rs. 2,50,000 less Rs. 60,000) cannot be adjusted against LTCG. Hence, in this case Mr. Sharan has to pay tax @ 20% (plus health & education cess @ 4%) on LTCG of Rs. 2,20,000. Thus, the tax liability will come to Rs. 45,760.

I hope you find this post informative and useful, cheers!

Continue reading :

- How to adjust Short Term Capital Gains against the Basic Exemption Limit? | Tax Rules & Examples

- How to set-off Capital Losses on Mutual Funds, Stocks, Property, Gold, Bonds & Debentures?

- List of all Popular Investment Options in India – Features & Snapshot

- Income Tax Deductions List FY 2023-24 | Under Old & New Tax Regimes

(Post first published on : 18-July-2019) (Post last updated on: 26-Sep-2023)

Join our channels

Hello Sree,

Great to see your blog just by chance … so nicely explained. Congratulations.

Can we adjust LTCG upon sale of equity (or equity MF) from our basic exemption limit ALSO after taking exemption of Rs 1 lakh u/s. 10 (38)?

Best wishes.

Dear Mr Garg,

To be frank there is no much clarity on this (suggest you to kindly consult a CA).

In my opinion, Rs 1 lakh need to be included in the adjustment and it is not over and above..

Dear Sreekanth,

Need clarity on the following points :

* Switching from the closed scheme within same fund house will attract LTCG Tax

* Switching from the closed scheme within same fund house but a different type of fund will attract LTCG e.g.Tax saver to another debt or equity fund

* HDFC long term advantage is a closed scheme. Is it advisable to remain in this fund anymore? If no then which is the best scheme in HDFC to switch.

Dear Shyam,

I believe that in case of ELSS & close ended schemes, switch is not possible before the lock in period.

“A close-ended fund or scheme has a stipulated maturity period e.g. 3-5 years. The fund is open for subscription only during a specified period at the time of launch of the scheme. Investors can invest in the scheme at the time of the new fund offer and thereafter they can buy or sell the

units of the scheme on the stock exchanges where the units are listed. In order to provide an exit route to the investors, some close-ended funds give an option of selling back the units to the mutual fund through periodic repurchase at NAV related prices. SEBI Regulations stipulate that at least one of the two exit routes is provided to the investor i.e. either repurchase facility or through listing on stock exchanges. ”

Related article : Mutual Funds Taxation Rules FY 2019-20 (AY 2020-21) | Capital Gains Tax Rates Chart

Hi Sree,

Have not yet received a response to my questions. I have invested in this scheme 6 years back so Maturity period is already over.

Should I stay invested in Long term Advantage as a scheme is already closed and No fund Manager is there.

Switching from one fund to another in the same house will not attract LTCG?

And the link which you have provided is nowhere giving reference of switching impact on LTCG from the closed scheme.

Thanks.

Dear Shyam,

HDFC Mutual Fund has decided to discontinue accepting subscriptions via fresh subscriptions / additional purchases / switch-ins / systematic investments under HDFC Long Term Advantage Fund with effect from May 16, 2018.

Switching units of mutual fund within the same scheme from Growth Plan to Dividend Plan and vice-versa is subject to capital gains tax.

Switching units across schemes within an AMC also attracts capital gains tax.

Kindly let me know if you have invested in any other MF schemes?

Dear Sri sir,

I have sold out a residential plot and dont want to pay long term capital gain of 2 lakh then is it possible to adjust with a new flat purchase ? or could be adjust with indexation slab ?

Dear Indrajeet,

You may kindly go through this article @ How to save Capital Gains Tax on Sale of Land / House Property?

Scenario 4 and 5 is very helpful for the young and middle age Salaried individuals. Thanks Sree.

Keep visiting Relakhs.com! Cheers!