Investments are subject to risks. All investments carry some degree of risk. Stocks, bonds, mutual funds, real-estate properties, gold, precious metals etc., can lose value, sometimes even all their value.

However, most of us equate RISK with ‘losses’ directly. We forget the fact that it is only a probability of losing and not actually losing.

We all want to make profits on our investments. No one wants to absorb the losses. What if you actually have to incur a financial loss? There can be times where your investments turn negative value and you have to book losses and move on.

In such circumstances, is there any option to turn these losses into gains? Is it possible to maximize income by properly accounting for losses and lower your tax liability?

In this post, let’s discuss;

- What is a Capital Asset?

- What are Financial Assets & Non-financial Assets?

- What is Capital Loss? What is Capital Gain?

- What are different Heads of Income?

- How to set-off Capital losses incurred on sale of Stocks, mutual funds, property, gold etc., against the capital gains?

- How to carry forward Capital losses?

What are Capital Assets?

Capital asset typically refers to anything the individual owns for personal or investment purposes. It includes all kinds of property, movable or immovable, tangible or intangible, fixed or circulating.

Capital assets are further classified as Financial assets and non-financial assets. Financial assets are intangible and represent the monetary value of a physical item. Stocks (Shares), equity mutual funds are examples of Financial Assets.

A non-financial asset is an asset with a physical value, such as real estate, Gold ornaments, equipment, machinery etc.,

What are Capital Gains & Losses?

The profit or gain (if any) that you make on your Capital Assets when you redeem or sell them is referred to as Capital Gains.

It can be a Short Term Capital Gain (STCG) or a Long Term Capital Gain (LTCG) depending upon the ‘Period of Holding’. The tax that is applicable on these profits/gains is known as ‘Capital Gains Tax’.

Similarly, the losses (if any) that you make on your Capital Assets when you redeem or sell them is referred to as Capital losses.

It can be a Short Term Capital Loss (STCL) or a Long Term Capital Loss (LTCL) depending upon the ‘Period of Holding’.

Short Term Capital Gain/Loss – (STCG / STCL)

If financial assets like Stocks & Equity mutual funds are held for less than 12 months then an investor will make either Short Term Capital Gain (or) Short Term Capital Loss on that investment.

If a non-financial assets and some Financial assets like Debt Mutual Funds, Gold ETFs etc., are held for less than 36 month, investor will make either Short Term Capital Gain (or) Short Term Capital Loss on that investment.

Long term Capital Gain/Loss – (LTCG / LTCL)

If a financial asset is held for more than 12 months then that asset is treated as Long Term Capital Asset. And the investor will make either Long Term Capital Gain (or) Long Term Capital Loss on that investment.

If a non-financial asset is held for more than 36 months then an investor will make either Long Term Capital Gain (or) Long Term Capital Loss on that investment.

With effective from FY 2017-18 / AY 2018-19, the Holding period for Long term capital gains for all immovable properties has been reduced to 2 years from 3 years.

How to set off Capital Losses?

You as a taxpayer can earn income from salary, house property (rental income), business or profession, capital gains, income from other sources (like interest on FD/RD) etc.,

There cannot be a loss from salary and income from other sources. However, you could suffer losses under other heads of income such as loss from house property, business loss and capital loss.

So, is it possible to set-off capital losses against all these ‘heads of income’>

No. We can not set-off capital losses against the below heads of income;

- Income from Salary

- Income from Business or Profession.

- Income from house property (rental income and not capital gains on sale of property)

- Other sources of income.

For example : If you make a loss on stock investment, you can not set-off this capital loss against your income from salary.

The capital losses can be set-off against capital gains only.

For example : If you make capital loss on stock investment, you can set-off this loss against capital gains on sale of property (if any).

” Long Term Capital Loss can be set off only against Long Term Capital Gains.”

” Short Term Capital Losses are allowed to be set off against both Long Term Gains and Short Term Gains.”

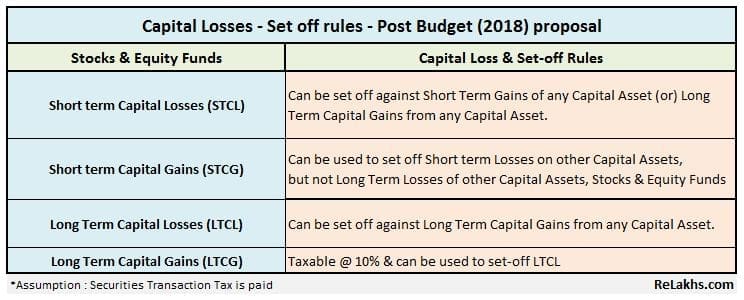

How to set-off Capital Losses on Stocks & Equity Mutual Funds AY 2024-25 / FY 2023-24?

Below table has the details on capital loss set-off rules on sale of Stocks, Equity Mutual Fund Schemes, listed Debentures & Bonds;

For example : If you had made a short term capital loss on Stocks and have a Long term capital gain on Sale of House property in a Financial Year, you can set-off losses on Stock investment against gains on Property.

How to Set-off capital losses on Non-Equity mutual funds & Non-Financial Assets?

Below table has the details on capital loss set-off rules on sale of Property, Debt Mutual Funds (Non-Equity Funds), Gold ornaments, Gold ETFs (Exchange Traded Funds) & unlisted Debentures;

For Example : If you have made a Long term loss on Debt Funds and have a LTCG on Equity Funds, you can not set-off the loss, as the LTCG on Stocks/Equity funds is a non-taxable income taxable income (w.e.f 1st April, 2018).

Other Important points:

- Can I carry forward my Capital Losses to the next Financial Year? – Yes. If you can not set-off a capital loss under the same head during the same financial year, you can carry forward such losses to the next financial year and can be set-off against Capital Gains (if any) arising in the next year. A capital loss can be carried forward for 8 years from the end of the financial year in which the loss has been incurred.

- Do I need to file Income Tax Return to carry forward my Capital Losses? – A capital loss can be carried forward to the next year only if you had declared such losses in your ITR and the tax return is filed before the due date.

- How to set off Losses from Intra-day trading? – If you have incurred speculative loses by doing Intra-day trading in Stocks, they can only be set off through speculative income and can be carried forward up to four years only.

- How to set off losses on Futures & Options trading? – Intra-day trading has been defined as ‘Speculative business’ whereas F&O trading is not. Income from trading in F&O (both intraday and overnight) on all the Stock Exchanges can be considered as non-speculative business income. Speculative (Intraday trading in equity) loss can’t be offset with non-speculative (F&O) gains, but speculative gains can be offset with non-speculative losses.

- If I have a Capital Loss & Capital Gains on various investments, what is the effective way of setting-off my loss? – Kindly note that there is no standard rule that the short-term capital loss has to be first set off against short-term capital gains before being set off against long-term capital gains. So, you need to look at the applicable tax rate on various Capital Gains and try to set-off your capital loss against the capital gain which has the lowest tax rate (also, do consider your income tax slab rate).

-

If income from any source is exempt, then can loss from such source be adjusted against any other taxable income? – If income from a particular source is exempt from tax, then loss from such source cannot be set off against any other income which is chargeable to tax. For example : Agricultural income is exempt from tax, hence, if the taxpayer incurs loss from agricultural activity, then such loss cannot be adjusted against any other taxable income.

- Can I set off capital loss after receiving dividend from Stocks/Mutual fund Schemes? – To prevent tax avoidance through dividend stripping, capital loss set off is not allowed under Income Tax Act, if investment was made within 3 months of dividend record date or redemption was made within 9 months of the dividend record date.

Continue reading :

- Different Asset Classes have different Tax Implications : How Returns are taxed?

- Tax Treatment of various Financial investments

- How to save Income Tax by adjusting Long Term Capital Gains against Basic Exemption Limit?

- How to adjust Short Term Capital Gains against the Basic Exemption Limit? | Tax Rules & Examples

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net) (Post published on 23-January-2017)

Join our channels

I have a LTCG on debt mutual funds (A) and LTCL on equity mutual funds (B) where A > B. Can I offset these two? What will be my final tax liability after offset? Will it be 20% of (A-B) ?

Dear Varun,

” Long Term Capital Loss can be set off only against Long Term Capital Gains.” So, it is possible..

If you have a net LTCG from debt funds then, the LTCG tax rate on non-equity funds is 20% (with Indexation benefit).

Related articles :

* What is Indexation of Mutual Funds and why is it important for you?

* Cost Inflation Index FY 2020-21 / AY 2021-22

I have incurred long term capital gain on debt fund (non equity fund ) but after indexation , then there is a long term capital loss. For income tax purpose which figure is to be taken into consideration — is of gain ( without indexation) or loss (with indexation). Please clarify.

Dear Kirti Prakash,

You can opt for whichever is beneficial for you. Can set off LTCL against gains..

Thanks for the prompt reply. I have still doubt because loss is after indexation but before indexation it is profit. So whether I can set off LTCL after indexation from the debt fund ( non equity ) against profit from LTCG (Equity ). Please explain it in detail.

Dear KIRTI PRAKASH ,

Its the NET loss (after indexation calculation)that can be carried forward, so you can …

Dear Sir,

Whereas you have explained nicely the setoff of losses during the current year what about carry forward and adjustement of brough forward losses? Can you kindly explain with examples under different scenarios after 2018 when new law has come? Thanks.

Dear RP,

ITR forms like ITR-2 and ITR-3 forms have been amended and updated to accommodate the changes, according to CBDT. You need to disclose the aggregate LTCG or LTCL in the specified columns and spaces provided in these ITR forms.

Dear Sir,

Isn’t the section and rules mentioned by you for equity shares whether short term or long term applicable only if stt is paid? eg if sells equity listed shares offmarket stt would not be paid how would the rules & definitions or category change? Can you kindly elaborate? Thanks.

Dear RP,

Yes, the above set off rules (for Equity oriented securities) are applicable if STT is paid.

Regarding off market transactions and tax implications, you may kindly consult a CA.

Dear Sreekanth,

I am an investor and trade in equity & F&O.

I understand that for turnover less than 2cr, the gain should be shown as 6% of this turnover to avoid tax audit.

1. I wanted to know that for checking applicability of tax audit, what does the “turnover” comprise of – Intra-day and F&O?

2. So, if have 50% of Intra-day turnover as profit but only 1% in F&O, the combined profit of Intraday and F&O should be 6% ? Or does it need to be atleast 6% in each?

Thanks for your time!

Regards.

Dear Mr Garg,

Suggest you to kindly consult a CA.