Capital asset typically refers to anything an individual owns for personal or investment purposes. It includes all kinds of property, movable or immovable, tangible intangible, fixed or circulating.

Capital assets are further classified as Financial assets and non-financial assets. Financial assets are intangible and represent the monetary value of a physical item. Stocks (Shares) and equity mutual funds are examples of Financial Assets.

A non-financial asset is an asset with a physical value, such as real estate, gold ornaments, equipment, machinery etc.,

The profit or gain (if any) that you make on your Capital Assets when you redeem or sell them is referred to as Capital Gains.

It can be a Short Term Capital Gain (STCG) or a Long Term Capital Gain (LTCG) depending upon the ‘Period of Holding’. The tax that is applicable on these profits/gains is known as ‘Capital Gains Tax’.

For example : If you redeem your equity mutual fund units within 1 year of your investment, after making a profit, then the profit will be considered as Short Term Capital Gain. You need to pay STCG tax @ 15%.

Related Article : Different Asset classes have different Tax implications – How Returns are taxed?

Besides the capital gains, you can also derive income from salary, pension, interest income on bank deposits, business or profession etc.,

Every Financial Year, you need to declare all such gains and incomes and then have to pay applicable taxes accordingly.

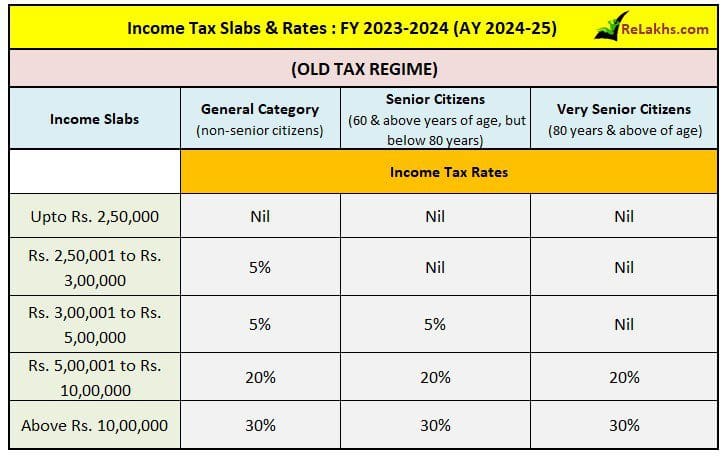

We are all aware on the availability of Basic Exemption Limit of Rs 2.5 lakh, Rs 3 lakh for Senior Citizens and Rs 5 lakh for very Senior Citizens (80+years) under the old tax regime. So, if you have salary income of say Rs 5 lakh, your income of up to Rs 2.5 lakh is not taxable.

When it comes to the New Tax Regime, one cannot claim all major tax deductions and the basic exemption limit is Rs 3 lakhs for all category of individuals.

What if you have made only Short Term Capital Gains and you do not have any other sources of income in a Financial Year? Can you still adjust Basic Exemption Limit against STCG? Do you have to pay Capital Gains tax even if your total income is less than 2.5 Lakh?

Another scenario can be – What if you have STCG, salary income and also made some tax saving investments (applicable mostly under the old tax regime)? How to calculate Short Term Capital Gains tax? What is the correct method of adjusting STCG against Basic Exemption Limit and save some tax? Can you claim 80c Tax Deduction against any STCG income? – Let’s discuss

How to save Income Tax by adjusting Short Term Capital Gains against the Basic Exemption Limit for FY 2023-24?

The tax rates on your salary or business income and Capital Gains are not uniform. For example : Your business income is taxable at applicable tax slab rates. Whereas, say your STCG on sale of Equity Funds is taxable @ 15%.

So, for calculation of tax payable on salary income and capital gains, you need to bifurcate the claiming process of incomes against Basic Exemption limit. Let’s now understand the rules related to this.

(For the sake of simplicity, we have considered the scenarios under the old tax regime. If you are opting for new tax regime, consider the basic exemption limit as Rs 3 lakhs and may ignore the tax saving provision explained in some of the below scenarios.)

Rules related to adjustment of STCG against Income Tax Basic Exemption Limit

- The basic exemption limit of Rs. 2,50,000 is applicable on your total income (including the Capital gains).

- If the total income including the STCG is below the basic exemption limit, then there will be no tax liability for a Resident Indian.

- A resident individual can adjust the STCG but such adjustment is possible only after making adjustment of other income.

- In other words, first income other than any STCG is to be adjusted against the exemption limit and

- Then the remaining limit (if any) can be adjusted against STCG derived on Sale of Property, Gold, Debt Funds etc (except Shares/Equity Mutual Funds) and

- Then the remaining exemption limit (if any) can be adjusted against STCG from Equity Mutual Funds and Shares (STCG covered under Section 111A).

“Capital gains from transfer of units of “specified mutual fund schemes” acquired on or after 1st April 2023 are treated as short term capital gains taxable at applicable slab rates as provided above irrespective of the period of holding of such mutual fund units. A specified MF (pure debt fund) is a fund where not more than 35% of its total proceeds are invested in the equity shares.”

- A Non-resident individuals / HUF, can adjust STCG against Basic Exemption limit, other than the STCG covered under Section 111A.

- For example : If an NRI makes STCG on Sale of property, Gold and Debt Funds, he/she can adjust such STCG against Exemption limit.

- In case, STCG is from Equity oriented Mutual Funds or Shares (Stocks), which are covered under section 111A then he/she can not adjust STCG against Exemption limit.

- Tax deduction under sections 80C to 80U is allowed from short-term capital gains other than covered under section 111A.

- For example : If you have got STCG on sale of property and invested in a tax saving FD then you can claim tax deduction u/s 80c from STCG.

- In case you have got STCG on sale of Equity mutual fund units and has also invested in PPF then you can not claim tax deduction u/s 80c from STCG.

Adjustment of STCG against the basic exemption limit FY 2023-24 | Illustrations

Scenario 1 : Basic Exemption Limit | Example:

Mr. Kapoor (resident and age 25 years) is a salaried employee earning a salary of Rs. 1,94,000 per annum. Apart from salary income, he has earned interest on NCD bond of Rs 6,000. He does not have any other income. What will be his tax liability for the assessment year 2024-25?

For resident individual of age of below 60 years, the basic exemption limit is Rs. 2,50,000 (under the old tax regime). In this case the taxable income of Mr. Kapoor is Rs. 2,00,000 (Rs. 1,94,000 + Rs. 6,000), which is below the basic exemption limit of Rs. 2,50,000, hence, his tax liability will be nil.

Scenario 2 : STCG, no other income & Exemption Limit | Example:

Mr. Reddy (resident and age 61 years) is a retired person with no income. He has earned STCG of Rs 3,50,000 on sale of Gold. He does not have any other sources of income. Can he claim Exemption limit on this STCG and save on Tax?

Yes, he can adjust basic exemption limit of Rs 3 lakh from Rs 3.5 lakh STCG. He has to pay STCG tax at applicable tax slab rate on Rs 50,000 only.

Scenario 3 : STCG u/s 111A, no other income & Exemption Limit | Example:

Miss Sunitha (resident and age 61 years) is a retired person with no income. She has earned STCG of Rs 3,50,000 on sale of Shares. She does not have any other sources of income. Can she claim Exemption limit on this STCG and save on Tax?

As she is a Resident Indian, she can adjust the STCG covered u/s 111A as well against the Exemption limit. So, she can adjust basic exemption limit of Rs 3 lakh from Rs 3.5 lakh STCG. Se has to pay STCG tax rate @ 15% on Rs 50,000 only.

Scenario 4 : NRI, STCG u/s 111A, Pension income & Exemption Limit | Example:

Mr Hussain (non-resident and age 65 years) earns STCG of Rs 2,20,000 on sale of Shares and also gets a Pension of Rs 5,000 pm. He does not have any other sources of income. Can he claim Exemption limit on this STCG and save on Tax?

- For non-resident individual irrespective of the age, the basic exemption limit is Rs. 2,50,000. Further, a non-resident individual cannot adjust the basic exemption limit against STCG covered under section 111A.

- In other words, Mr. Hussain can adjust the pension income against the basic exemption limit but the remaining exemption limit cannot be adjusted against STCG on sale of shares.

- The basic exemption limit in this case is Rs. 2,50,000, and the same will be adjusted against pension income of Rs. 60,000. The balance limit of Rs. 1,90,000 (i.e., Rs. 2,50,000 less Rs. 60,000) cannot be adjusted against STCG covered under section 111A. Hence, in this case, Mr Hussain has to pay tax @ 15% on STCG of Rs. 2,20,000.

Scenario 5 : STCG, STCG u/s 111A, Pension Income & Exemption Limit | Example:

Mr. Krunal (age 59 years and resident) is a retired person earning a monthly pension of Rs. 5,000. He purchased shares of SBI Ltd. in April, 2023 and sold the same in August, 2023 (sold in Bombay Stock Exchange and STT is levied). Taxable STCG amounted to Rs. 1,20,000. Apart from pension income, gain on sale of shares, he has also made STCG on sale of property of amount Rs 1 lakh. What will be his tax liability for the year 2024-25?

- Kindly note that Krunal has STCG covered under 111A (Sale of shares) and STCG other than covered u/s 111A (sale of property).

- He has to first adjust Rs 60000 pension income against Rs 2.5 lakh limit. So, the exemption limit comes down to Rs 1.9 lakh.

- He can then claim STCG on sale of property. The exemption limit comes down to Rs 90000 (Rs 1.9 lakh – Rs 1 lakh).

- The STCG from sale of shares of Rs 1.2 lakh can be adjusted to the extent of Rs 90,000 only. So, he has to pay tax @ 15% on the remaining STCG of Rs 30,000 (Rs 1.2 lakh – Rs 90,000).

- In case, Krunal is an NRI then he can not adjust STCG from sale of Shares against the basic Exemption limit.

Scenario 6 : STCG other than u/s 111A, Tax Saving Investment & Exemption Limit | Example:

Mr. Kapoor (age 57 years and resident) is a retired person. He purchased a piece of land worth Rs. 8,84,000 in March, 2023 and sold the same in Sept, 2023 for Rs. 12,84,000. Apart from gain on sale of land he is not having any other income. He deposited Rs. 1,00,000 in Public Provident Fund (PPF) and Rs.50,000 in NSC . He wants to claim deduction under section 80C on account of Rs. 1,50,000 deposited in PPF and NSC. Can he do so?

Deduction under section 80C to 80U can be claimed on short-term capital gains other than STCG covered under section 111A. In this case, the gain is on sale of land and, hence, is not covered under section 111A. Hence, Mr. Kapoor can claim deduction under section 80C of Rs. 1,50,000 from STCG of Rs. 4,00,000. His taxable income will be Rs 2.5 lakh.

(If Mr Kapoor follows the new tax regime then he cannot claim tax deductions u/s 80c and hence the entire STCG of Rs 4 lakhs is liable to taxation.)

Scenario 7 : STCG u/s 111A, Tax Saving Investment & Exemption Limit | Example:

Mr. Babbar (age 57 years and resident) is a self-employed person. He purchased equity shares of SBI Ltd. in Feb, 2023 and sold the same in Sep, 2023. Taxable STCG amounted to Rs. 2,20,000. Apart from gain on sale of shares he is not having any other income. He deposited Rs. 1,50,000 in Public Provident Fund (PPF). He wants to claim deduction under section 80C on account of Rs. 1,50,000 deposited in PPF. Can he do so?

In this case, the STCG of Rs. 2,20,000 arising on account of sale of shares is STCG covered under section 111A and, hence, Mr. Babbar cannot claim any deduction under section 80C to 80U from such gain.

Considering the above provisions, Mr. Kapoor cannot claim deduction of Rs. 1,50,000 under section 80C from the STCG of Rs. 2,20,000. The taxable income will be Rs 2.2 lakh.

I hope you find this post informative and useful, cheers!

Continue reading :

- Income Tax Deductions List FY 2023-24 | Under Old & New Tax Regimes

- How to save Income Tax by adjusting Long Term Capital Gains against Basic Exemption Limit?

- How to set-off Capital Losses on Mutual Funds, Stocks, Property, Gold, Bonds & Debentures?

- Latest TDS Rates AY 2024-25 | TDS Rate Table for FY 2023-24

(Post first published on : 19-July-2019) (Post last updated on : 25-Sep-2023)

Join our channels

Hello sir

If my salary income is 565000 after 50k standard deduction and STCG under 111 A is 40k

Investment under 80c is 50k then can you please tell what will be my tax liability .

Thanks in advance..

Dear Abhinav,

Suggest you to use the tax calculator provided at e-filing portal.

Hello sir

If my salary income is 565000 after 50k standard deduction and STCG under 111 A is 40k

Investment under 80c is 50k then can you please tell what will be my tax liability .

Thanks in advance..

Hi Sreekanth,

Could you please help answer my questions below as per my details?

Age = 45

Interest Income = Rs.425000/-,

PPF Investment = 150000/-

Medical Prem. = 18000/-

Taxable Income = Rs. 257000/-

STCG on sale of Equity Mutual Funds= Rs. 30000.

How does rebate under section 87A work under this scenario?

Do I need to pay 15% STCG as my taxable income is above 2.5 lakhs? If yes, can i make additional tax saving investment (such as NPS) to bring my taxable income below 2.5 lakhs and save tax on STCG?

Thanks in advance.

Dear Sandeep,

The threshold limit us/ 87A is Rs 12,500 for FY 2020-21 / AY 2021-22. This means that if the total tax payable is lower than Rs 12,500, then that amount will be the rebate under section 87A.

Only Individual Assesses earning net taxable income up to Rs 5 lakhs are eligible to enjoy tax rebate u/s 87A.

The Tax Assessee is first required to add all incomes i.e. salary, house income, capital gains, business or profession income and income from other sources and then deduct the eligible tax deduction amounts u/s 80C to 80U and under section 24(b) (Home Loan Interest) to come up with the net taxable income. (If you opt for new tax regime then you can not claim income tax deductions u/s 80c, 80d etc.,)

Yes, you can bring down your taxable income by making additional investment. But, advisable not to pick an investment option just to avoid some taxes. Pick a product only if it meets your financial goal(s), risk profile and time-frame.

Related article : Why you should think beyond TAX when investing!

Age-35 years

Salary Income = Rs.300000/-, Tax Saving under section 80c = 150000/-. Taxable Income = Rs. 150000/- (3L – 1.5L). STCG covered under Sec 111A= Rs. 100000.

Is Tax Liability = NIL ? or,

15% Tax on STCG has to be paid by him?

Dear NB,

The tax liability would be NIL.

You can also try the calculation yourself at incometaxindia . gov. in portal.

Hi Sreekanth ji,

in above case, does he or she still needs to file NIL tax returns?

Very nice article with valuable info explained with clear examples.

Dear Venkata,

As Capital Gains is one of the sources of income, advisable to file ITR.

Thank you

Fantastic!!! Explained nicely. Very much useful. Thanks a lot.

T.L.K. RAO

Dear Mr Rao – Thank you for the appreciation. Keep visiting ReLakhs!

My income below 2lk and I invest in shares as STCG and get 20000rs and now will I pay tax or not ……and i dont have any other income

Salary Income = Rs.300000/-, Tax Saving under section 80c = 150000/-. Taxable Income = Rs. 150000/- (3L – 1.5L). STCG covered under Sec 111A= Rs. 100000.

Is Tax Liability = NIL ? or,

15% Tax on STCG has to be paid by him?

Hi,

May I know the age of the Assessee in this scenario?

Nice article Sreekanth. The way you categorised with various scenarios, it is easy to understand. Keep it up

Thank you dear Suresh..!