Income tax in India for NRIs (Non-Resident Indian) is moderately different when compared to the residents. Everyone is aware of the basic rule that NRIs who are earning income in India are subjected to tax payments.

The source of income can be anything be it from rent, fixed deposits, savings accounts, investments, etc. an NRI earning income in India must pay the tax. Any individual (below 60 years of age) whose income is more than Rs. 2,50,000 is required to pay the tax.

For the current financial year i.e. 2020-2021, the minimum tax that will be levied is 10% of the income earned in this particular financial year. This specific rate will increase with an increase in income. Paying tax is mandatory for every citizen whoever falls into the taxable criterion.

If your status is ‘NRI,’ your income which is earned or accrued in India is taxable in India.

Related Article : Residential Status online calculator – NRI or Resident? | NRI Taxation rules

Can NRIs claim tax deductions from Income earned in India? What are the best tax saving options for NRIs in India?

On a par with residents, NRIs are also allowed to claim certain tax benefits and deductions on the investments made in India. Let’s discuss…

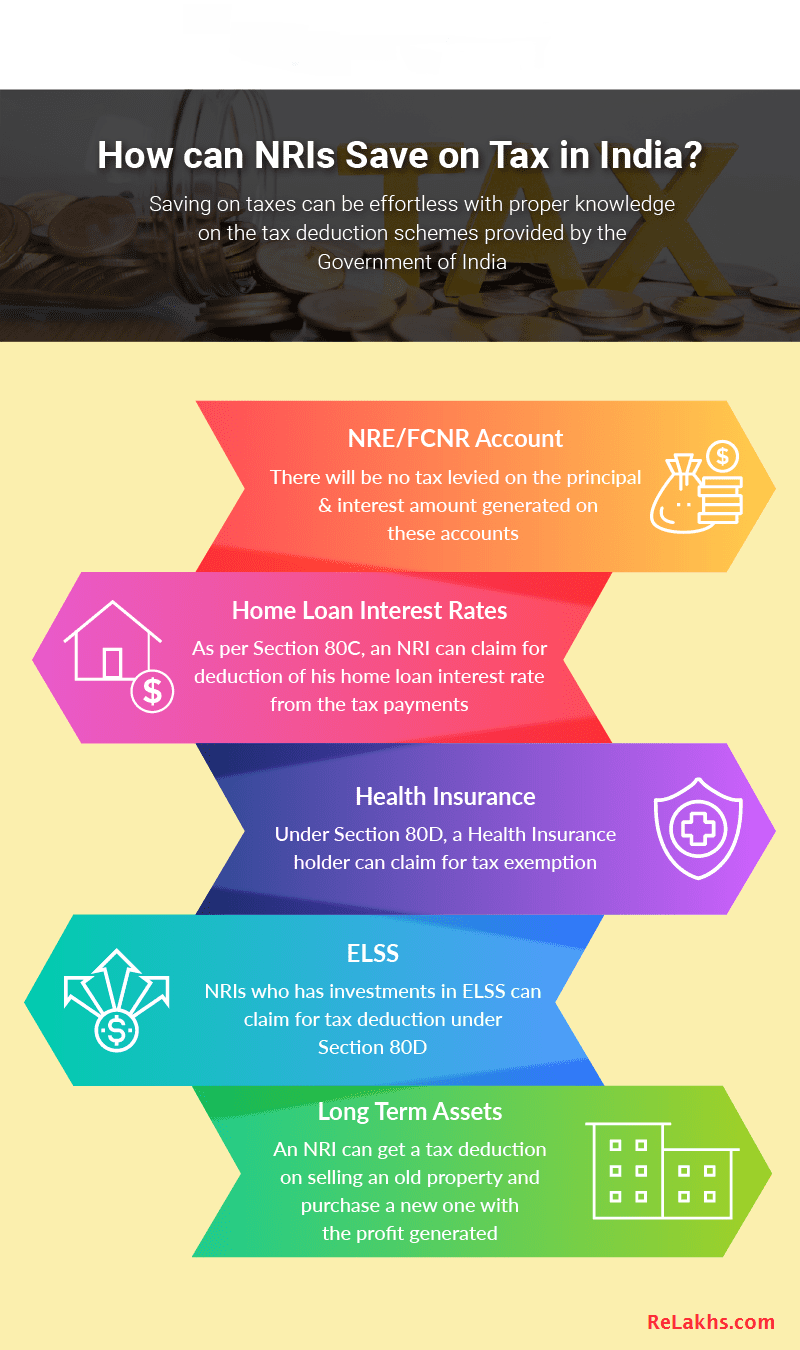

How NRIs can save on Tax in India? | NRI Tax Saving options FY 2023-2024

Maintain an NRE or FCNR Account

Non-Resident Indians are not supposed to maintain a savings account in India as per the Foreign Exchange Management Act (FEMA) rules. They can open an NRE (Non-Resident External) account in order to deposit their money earned in foreign countries.

The utmost benefit of an NRE account is, the interest earned on this account is tax-free. Instead of maintaining a normal savings account which can levy penalties, NRIs can maintain an NRE account and avail the free repatriation and tax-free benefits. There are various types of NRE accounts like Savings, deposits, etc.

The Foreign Currency Non-Resident (FCNR) account is a term deposit account which can be maintained by NRIs. Instead of getting a regular fixed deposit account, NRIs can get an FCNR account or NRE deposit account. An FCNR account can be maintained in major foreign currencies. Both these accounts are tax-free on the principal amount and interest rate.

Related Latest Article : Under the new tax regime, all popular tax saving options are not available w.e.f FY 2020-21 / AY 2021-22. Read more at : Income Tax Deductions List FY 2023-24 | Under Old & New Tax Regimes

Interest on a Home Loan

If an NRI owns a house or property back in India and gets some rent from it, then he is supposed to pay the tax according to the tax slab. One way NRIs can reclaim the tax paid on rents is if the property is under a loan. Like the Indian residents, NRIs are also eligible to claim refunds if the property is under a home/property loan.

- Under Section 80C, an NRI can claim up to Rs.1.5 Lakhs (p.a.) on the principal amount on a residential property home loan.

- As per Section 24, the deduction is available for the repayment of interest on home loans up to 200,000 p.a. This deduction is available under the head ‘Income from house property’.

- NRIs are allowed to claim 30% standard deduction on rental Income.

So, NRIs who own a house in India and paying interest on the home loan can claim for the refund.

(NRIs can also claim Life Insurance Premium Payment and investments in NPS as tax deductions u/s 80c. However, they are not allowed to open new PPF accounts and can not invest in Post office Small Saving Schemes.)

Health Insurance

NRIs who are having health insurance back in India can avail deduction under Section 80D. The maximum deduction that can be availed is Rs.50,000/- in the case of senior citizens and Rs.25,000/- on self-insured or family (spouse, children).

An NRI who has health insurance can avail deduction up to Rs.75,000 including ‘resident‘ senior citizen parents, self-insurance or health insurance for kids or spouse. An additional Rs.5000 can also be deducted from the taxable amount if there are any health check-ups taken.

But, note that deductions under Section 80DD, Section 80DDB and Section 80U are not available for NRIs.

Deduction under Section 80E

Under this Section, NRIs can claim a deduction of interest paid on an education loan. This loan may have been taken for higher education for the NRI, or NRI’s spouse or children or for a student for whom the NRI is a legal guardian. There is no limit on the amount which can be claimed as a deduction under this Section. The deduction is available for a maximum of 8 years or till the interest is paid, whichever is earlier. The deduction is not available on the principal repayment of the loan.

ELSS (Equity Linked Savings Scheme)

Currently, the most favored option to save tax is ELSS which is the abbreviation of Equity Linked Savings Scheme. It is a mutual fund scheme with a lock-in period of 3 years. This is the only mutual fund scheme that is available for tax deductions under Section 80C of Income-tax Act, 1961. It is applicable to NRIs as well.

NRIs who invest in ELSS can claim for deduction up to 1.5 Lakhs per annum.

The returns gained on ELSS can be high and the lock-in period is less which makes it a most preferable option to other conventional fixed deposits and investment schemes.

Related article : ‘Best ELSS Tax Saving Mutual Fund Schemes to invest in 2019-20 & beyond‘

NRIs can also invest in NPS Scheme now.

Long term Assets

An NRI house owner who is planning to purchase a new house by selling the old house can avail the benefits of Section 54 i.e. can claim tax exemption as he is not selling the property for profits rather purchase a new property. The seller of the house should purchase a new house within two years of the sale or 3 years in the case of an under-construction property. Under such cases, he/she can claim for exemption. One thing to be noted is the capital gain should be equal or less than the new investment to claim for tax exemption.

For example, Mr. Ravi is selling his property for Rs.30,00,000 and the new property that is being purchased is Rs.27,00,000. In such a case, the new property value is less than the sale value which concludes that the profit he gained Rs.3,00,000 is the taxable amount.

If the new property is more or equal to the old property sale amount then there would not be any tax to be paid.

Related article : ‘How to save Capital Gains Tax on Sale of Land / House Property?‘

It is not a difficult task to save on tax. There are a good number of ways provided by the Indian government that will help an NRI save in a significant amount on taxes. An NRI just requires detailed knowledge of the taxation rules in India.

NRIs who are planning to invest their money in India should not only find out the best investment options that offer good ROI (Return on Investment) but also have a comprehensive awareness of the taxes that will be levied along with approaches that can help in saving money on tax.

This is a guest post by Nikitha of mymoneysouq.com

Author Bio:

Nikitha is working as a senior analyst at MyMoneySouq. It is the leading website in UAE for comparison of personal loans, credit cards, home loans, term insurance etc., in the UAE region.

Continue reading :

- Latest NRI Gift Tax Rules 2019-20 | Gifts to NRIs can be Taxable now!

- Income Tax Deductions List FY 2023-24 | Under Old & New Tax Regimes

- Mutual Funds Taxation Rules FY 2023-24 (AY 2024-25) | Capital Gains Tax Rates Chart

- Do I need to file my Income Tax Return?

- What is Double Taxation Avoidance Agreement (DTAA)? | Is Income earned outside India Taxable?

- Should NRIs buy Health Insurance in India?

Kindly note that ReLakhs.com is not associated with MyMoneySouq. This is a guest post and NOT a sponsored one. We have not received any monetary benefit for publishing this article. The content of this post is intended for general information / educational purposes only.

(Post published on : 29-July-2019) (Post last updated on : 23-Sep-2023)

Join our channels