In India, we have very few instruments where the interest income is exempt from tax. One of them is the PF (Provident Fund) and the other investment option is Tax Free bonds.

Most of the other interest yielding instruments like bank deposits, company fixed deposits, NSC, Post Office Monthly Income Scheme, Sr. Citizen Savings Scheme, 7.75% GoI Bonds etc., can attract tax on interest income.

The Reserve Bank of India (RBI) has recently released its fifth bi-monthly rate review of financial year 2019-20. Though the key interest rates have been kept unchanged, the RBI has been cutting the rates since February 2019.

There have been five consecutive rate cuts from RBI – in February, April, June & August of calendar year 2019. Also, the central bank has indicated that there is a possibility of further rate cuts in the near future. This signals a further downtrend in bank deposit and lending rates in India.

In this scenario, most of the banks and corporates may also reduce the interest rates on their deposits schemes, Bonds, NCD Public Issues etc.,

This has been inducing many investors (especially HNIs) to look out for better fixed income products which can give decent tax-adjusted fixed rate of return.

The current (Dec 2019) average interest rates offered by popular banks on long-term deposits is around 6.5%. As interest income is taxable, the effective tax adjusted return works out to 4.55% only (for an individual who is in 30% income tax slab) and 5.2% (for an individual in 20% slab rate).

Post-tax returns = Pre-Tax returns * { (100-Tax Rate) / 100 }

As per the prevailing Bond Yields, Tax Free Bonds can give yields (tax free returns) in the rage of 5.5% to 6%. Though the TFBs current yields are lower when compared to yields a few years back, TFBs are still a good long-term tax-free investment option, especially for individuals who are in highest income tax slab bracket.

In this post, let us understand – What are Tax Free Bonds & their Features? What are the important factors to consider when invest in Tax Free Bonds? How to buy Best Tax Free Bonds in India for 2020 & beyond?….

What are Tax Free Bonds?

A bond is a Fixed Income security (debt investment) in which an investor loans money to an entity (typically corporate or governmental / PSUs) which borrows the funds for a defined period (tenure) of time at a variable or fixed interest rate (coupon rate).

Those bonds which are exempt from taxation on the ‘interest income’ under the Income Tax Act, 1961 are called Tax-free bonds. These are usually issued by government-backed entities with long tenures of 10, 15 and 20 years .

Several state-run companies, like NHAI, PFC, NABARD, HUDCO, IRFC etc., had earlier raised Rs 30,000 crore through tax-free bonds in FY12, Rs 25,000 crore in FY13, Rs 50,000 crore in FY14 and around Rs 40,000 cr in 2016.

These funds are utilized to fund infrastructure projects. There has been no new bond issuance since FY 2016-17. As these Bonds are listed on Stock Exchanges, one can invest in them through Demat account from Secondary Market. (Kindly note that Govt has not notified for any fresh Public Issue of TFBs in 2019-20.)

Factors to consider when investing in Tax Free Bonds

Below are the main factors that need to considered when buying Tax Free bonds from Secondary Market;

- Coupon Rate

- Current Yield

- Current Yield to Maturity

- Bond Series Maturity Date

- Traded Volume (Liquidity factor)

- Credit Rating of Bonds

- Current Economic and Interest rate scenario

Let me explain these factors by taking an example.

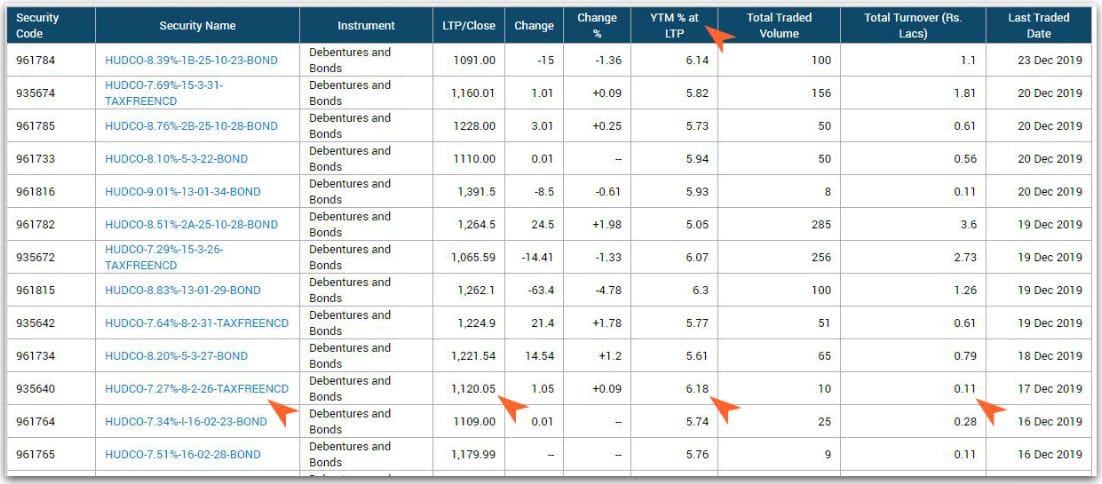

HUDCO (Housing & Urban Development Corporation) had issued Tax Free Bonds in FY 2015-16.

Coupon Rate, Yield to Maturity & Liquidity

- In one of the Public Issue Series (2016) it offered 7.27% as coupon rate with a tenure of 10 years (maturity date 08-02-2026). The Face Value of a bond is Rs 1,000.

- So, if you had invested Rs 1,000 in 2016 IPO, you would have been receiving Rs 72.7 per year as tax-free interest income till 2026.

- At the time of Public Issue, Yield of these bonds was 7.27% (same as coupon rate).

- If you are planning to buy these bonds now from secondary market, the trading price of these bonds wont be Rs 1,000 (Face value). Due to many factors (like demand & supply, interest rate cycle etc.,), these bond prices fluctuate (increase/decrease).

- You can notice that HUDCO 7.27% (2026) Bond series has last traded price as Rs 1,120.

- If an investor has bought these bonds at Rs 1,120, he/she will get interest amount Rs 72.7 per year (coupon rate is calculated on Face value and not on secondary market purchase price) till maturity (2026).

- In this case the current yield of this investment is 6.49% (Interest amount (Rs 72.7) divided by Rs 1,120).

- As interest amount is received over many years, current yield of bonds may not be the best thing to look at. The Yield to Maturity (YTM) could be the best way to calculate the returns on Bond investments.

- YTM reflects the total return an investor receives by holding the bond until it matures. A bond’s yield to maturity, or YTM, reflects all of the interest payments from the time of purchase until maturity, including interest earned on interest (in present value terms).

- If you notice, the YTM on these Bond Series is around 6.18%. Note that these interest payments are tax-free whereas the interest amount received on bank deposits is taxable. As you are now purchasing from secondary market, yield depends only upon your buying price. HIGHER the YTM, the better is return on your investment.

- Liquidity (ease to sell/buy) can be the major disadvantage when it comes to TFBs. You can notice that HUDCO 7.27% bonds which were worth of just Rs 11,000 got traded on 17th Dec, 2019. So, advisable to pick Bond Series with large Issue size and where turnover has been decent in the recent past.

- Also, it is prudent to invest in 2 or 3 Bond Series, which are from different Issuers, in case, you are investing large lump-sum amount in TFBs.

The other important factors that you need to check are Credit Rating and interest rate scenario.

Credit Rating & Interest Rate Scenario

Most of these Tax Free Bonds are issued by govt backed entities with decent Credit Rating. These ratings can be AAA (good rating), AA+, AA & AA-. But note that credit rating is dynamic factor and it can change in the future (down-grading).

These bonds generally become attractive when the interest rates in the financial system are high. The interest rates are in a downward trend now. So, the current Yields on Tax fee bonds may not be that attractive. But, keep in mind, currently, there are very few investment options that can give tax-adjusted returns of around 6%.

If RBI cuts interest rates (considering current inflation rate), the bond prices may go up further leading to further fall of YTM from the current levels.

As bonds pay a fixed interest rate, if interest rates in general fall, the existing bonds’ interest rates become more attractive, so people will bid up the price of the bond. Likewise, if interest rates rise, people will no longer prefer the lower fixed interest rate paid by a bond, and their price will fall.

(You may use this Bond Yield Calculator available at SEBI Portal. I have noticed some discrepancies in YTM calculations on NSE website.)

Best Tax Free Bonds to invest in 2020

Below are some of the best Tax Free Bonds that can be considered for investment in 2020-21;

- PFC Tax Free Bonds – N2 Series

- REC Bonds – N2 Series

- IRFC Bonds – NO Series

- NHAI – NA Series

(You can find more details on available TFBs at NSE Portal / BSE Portal.)

Tax Implications on Tax free bonds

- Is TDS applicable on Tax free bonds? – These bonds are tax free and hence not subject to TDS.

- Interest income earned on TFBs is exempted from income tax. The interest earned from these bonds does not part form of your total taxable income.

- The invested amount is not eligible for any tax deduction.

- Are Capital Gains taxes applicable on Tax free bonds? – Though the interest earned on these bonds is tax-free, any capital gain from sale in the secondary market is taxable. If you sell your Bond for a price that is more than the cost then you would have to consider this as a capital gain. Short-term capital gains from sale of tax-free bonds on exchanges are taxed at your income tax slab rate, while long-term capital gains are taxed at 10% without indexation. The indexation benefit is not available for Bonds/NCDs. (For STCG holding period is less than 12 months. For LTCG holding period should be more than 12 months)

Important points to ponder over:

- If you are in 20% or 30% income tax slabs, it makes sense to consider investing in tax free bonds as part of your Debt Portfolio (besides EPF/VPF/PPF). Provided, your investment tenure matches with bond’s maturity date, you are expected to remain in high tax slab bracket and also aiming at periodic income.

- I believe that ‘lack of liquidity’ is the biggest disadvantage of Tax-Free Bonds. Hence, invest in TFBs only if you can hold the bonds till their maturity date.

- TFBs can be a very good investment option for NRIs and HNI individuals.

- If you are an existing investor in Tax Free Bonds, you can check your current slab rate, current bond traded prices and can take a decision (if any) to book Capital Gains. (This is not advise to sell, but just letting you know the scenario.)

- If you were in say 30% IT slab when you had bought TFB at Rs 1,000 and if you are now a retiree at 10% IT slab bracket and the current bond price is say Rs 1,200 then you can make capital gains of Rs 200.

Hope you find this post informative. Have you invested in any Tax Free Bonds? Do share your views on investing in TFBs..Cheers!

Continue reading:

- List of all Popular Investment Options in India – Features & Snapshot

- Lump sum Investment options for Retirees/Senior Citizens | Where to invest my Retiral benefits to get Regular Income?

- Top 15 Best Mutual Funds to invest in 2020 & beyond | Top Performing Equity Funds

(Post first published on : 23-December-2019)

Join our channels

It’s great, company start this type of program, who give the knowledge

If I brought an infrastructure bond like PFC OR REC from secondary market which maturity year 2033, then I can shown it IT 80ccf ?

god input for investment. can I come back with that

If I had bought a tax free bond during initial public issue at say Rs. 1000 and kept it till maturity (10 years or whatever), at the end during maturity, how much will I get. The initial issue price of Rs. 1000 or any thing more? Please explain.

Dear Sriram.. The initial issue price / face value is returned to the investor on maturity date..

Can I buy these bonds in secondary market with my broker reliance securities? Or with only specific brokers

Dear Nagasahitya..Mostly yes, kindly check with your service provider..