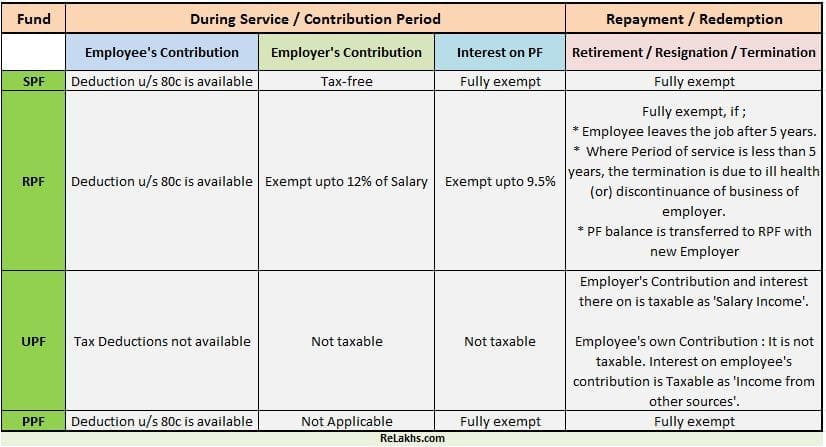

There are different types of Provident Funds (PFs) which can be used by an individual for investment and saving purposes. The Balance of Provident Fund account (PF A/c) consists of amount invested by employee (you), amount invested by your employer and interest received on the amount invested.

The rules related to subscription, withdrawal, and taxability of Provident Fund (PF) vary depending on the type of Provident Fund. Taxability of provident fund is much more complex because of separate conditions of taxability.

In this post, let us understand the types of Provident Funds and their Tax implications.

Types of Provident Funds : Tax Implications & Key Points

- Statutory Provident Fund (SPF / GPF)

- These are maintained by Government, Semi Govt bodies, Railways, Universities, Local Authorities etc.,

- The contributions made by the employer are exempted from income taxes in the year in which contributions are made.

- The contributions made by the employee can be claimed as tax deductions under section 80c.

- Interest amount credited during the financial year is not treated as income and hence it is exempted from income tax.

- The redemption amount at the time of retirement is exempted from tax.

- If an employee terminates the PF account, the withdrawal amount too is exempted from taxes.

- Recognized Provident Fund (RPF)

- Any establishment (business entity) which employs 20 or more employees can join RPF. Most of the individuals (who are salaried) generally contribute to this type of Provident Fund. This is one of the popular types of Employees Provident Funds (EPF). (Organizations which employ less than 20 employees can also join RPF if the employer and employees want to do so)

- The business entity can either join the Govt. scheme set up by the PF Commissioner (or) the employer himself can manage the scheme by creating a PF Trust. All Recognized Provident Fund Schemes must be approved by The Commissioner of Income Tax (CIT).

- Employer’s contribution in excess of 12% of salary is treated as income of the employee and is taxable. In excess of 12%, the contributions are taxable in the year of contribution.

- Tax Deduction u/s. 80C is available for amount invested by the employee (up to Rs 1.5 Lakh in a Financial Year).

- Interest amount earned (up to 9.5% interest rate) on PF balance (employee’s + employer’s contributions) is tax free. In excess of 9.5%, the interest on contributions is taxable as ‘salary’ in the year in which it is accrued.

- Accumulated funds redeemed by the employee at the time of retirement / resignation are exempt from tax if he/she continues the service for 5 years or more.

- Unrecognized Provident Fund (UPF)

- These are not recognized by Commissioner of Income Tax.

- Employer’s contribution is not treated as income in the year of investment and hence not taxable in that specific year. So, it is tax free in the year of contribution.

- Tax deduction under section 80c is not available on Employees contributions.

- Interest earned is not treated as income in the year it is credited and hence not taxable in the year of accrual.

- At the time of redemption / retirement, the employer’s contributions and interest thereon is treated as ‘salary income’ and chargeable to tax. However, employee’s contribution is not chargeable to tax. Interest on Employees contribution will be charged under income from other sources.

- Public Provident Fund (PPF)

- Under PPF any individual from public, whether is in employment or not may contribute to this fund.

- The minimum contribution is Rs. 500 p.a. & maximum is Rs 1.5 Lakh Rs. p.a. The amount is repayable after 15 years.

- PPF can serve as an excellent retirement planning / savings tool, for those who do not come under any pension scheme.

- The PPF offers tax benefit under section 8OC and the interest earned is also exempt from tax. All the eligible withdrawals are exempted from taxes.

(SPF, RPF & UPF are types of Employees Provident Funds – EPF ) (Photo Credit : rediff.com)

You may read other EPF related articles;

- Tax Implications of EPF, PPF & NPS Withdrawals (Full / Partial) & Maturity proceeds

- All you need to know about EPFO’s Universal Account Number (UAN)

- How to transfer your EPF funds online through OTCP & UAN Member Portal?

- How is interest calculated on EPF Account – Components & Illustration?

- How to track in-operative EPF account through EPFO’s online Helpdesk?

- EPFO SMS Service – Get your EPF A/c Balance as SMS

Join our channels

Kindly guide, as to whether the exemption under 80C is available for the amount recovered against advance GPF withdrawal.

Is epfo monthly pension taxable? If so why tds is not done in it?

Dear Ashok,

Yes, monthly EPS pension is taxable under the head ‘salary’. The projected pension amount in that FY can be below basic exemption limit..

“If pension is received through a nationalized bank, TDS provisions are applicable as is the case with salary income. However, TDS is not deducted on family pension as it does not come under the ambit of section 192 of the income tax act.”

Hi,

Under which section of ITR, we need to report for the PPF interest earned…Is it under -> Statutory provident fund received ( 10- (11) )

Please advise.

Dear KAPIL,

Yes (assuming you are referring to exempt income).

Related article : EPF Interest Income & Withdrawals | Tax Implications | Is EPF Interest taxable?

Got help for my exam..

Thanks

Super Explanation. Thank you Mr. Sreekanth Reddy.

An employee retires and receive full n final GPF.In same FY he claims for rebate u/s 80c of IT, on subscriptions of same year,which he actually got refunded/finally paid.Is he entitled to do so?or IT be calculated ignoring such amount so called saving.

Dear LCChaurasia..I believe that in such a scenario, one can claim tax deductions on the contributions.

Sir,GPFcontribution has been paid to contributor and now his PF bal.is zero & a/c closed.even then his claim for show that subs.under I.T.sec80c is as per rule?Pl.quote IT Rule,if any exist.

Dear LCChaurasia..The account might have been closed but the contributions were done during the FY right??

Hi Sreekanth,

My father was a state govt employee and he got retired in 2013. and now he is getting pension every month of rs. 14000.

My question is,

1. is he eligible to take loan against his pension fund for my brothers marriage? if YES, how can he apply for it and what are the terms and conditions for it?

2. Is there a way to check whether his GPF account has some balance?

3. Is there a way to check whats his pension fund balance?

Thanks

Dear LD,

1 – I believe that it is not allowed.

2 – Let me know the State name. You may type respective state name + check GPF balance online and can visit applicable links on Google.

If a person start his job at 56years, then at the time of retirement amount withdrawn from RPF is taxable or not?

Thanks

Dear GAGANDEEP..I believe that it is tax free if the period of service is minimum 5 years.

Hi Sreekanth,

Thank you for all the informative posts. I really like reading all your posts.

My query is , Can I open PPF account for my wife (house wife) ? so we can save total 3 lakhs in 2 ppf account (mine and my wife) or it will restrict upto 1.5 lakhs all total. Please confirm.

Thank You!!

Dear bhupendra,

An individual can claim up to Rs 1.5 Lakh only as tax deduction u/s 80c.

You can not claim Rs 3 Lakh as deduction.

Thanks for the response Sreekanth. so I can open PPF account for my wife and invest 1.5 Lakh/yr in it apart from the PPF account that I have (also keeping 1.5 Lakhs in it). I don’t want to claim but I just want saving for future.

Please confirm.

Thank you once again.

Dear bhupendra,

May I know the reason for choosing PPF? Have you made any other investments?

Let me know your financial goals??

I am thinking PPF for long term goals (retirement plan) considering its good return.

I got to know about your site recently and started planning for life /non-life insurances. Recently I have taken life insurance and a health insurance plan.

can you please help in finding short term plans with good returns ?

Thanks for all the information in your site. It helped me a lot.

Dear Bhupendra,

For long-term goals, you may allocate higher portion of your savings to equity or equity oriented mutual funds. PPF is a good savings product but do not invest your entire savings in this product alone.

Kindly read my articles;

Retirement planning calculator.

Best Equity funds.

Monthly Income MFs.

Thank you for inputs Sreekanth !!

Good Information Given By You It is very useful for common man.

Thank you Arun. Keep visiting!

Nicely summarized.

Thanks Ravi and keep visiting!