The Reserve Bank of India (RBI) has released the nineteenth volume of its annual statistical publication, ‘Handbook of Statistics on the Indian Economy – 2017‘ on 15th sep, 2017. Through this publication, the Reserve Bank has been providing time series data on various economic and financial indicators for the Indian economy.

You can find lot of useful data related to;

- Macro Economic indicators

- Money & Banking

- Financial Markets

- Public Finances

- Trade & Balance of payments

- Socio & Economic indicators and so on..

Based on this statistical data, I have been collating and publishing (since 2014) some important / interesting points and trends related to Personal Finances like – Financial Savings of Households, total investments in bank deposits, investments in shares & mutual funds, information on total bank loans, performance of Share markets, Inflation data, NRI deposits etc.,

Before discussing the facts & figures, let us understand – what are households savings, Financial Assets and Physical Assets?

Households’ Savings correspond to the total income saved by households during a certain period of time. Savings and investments in banks, stock markets, Post office schemes, company deposits etc., are considered as Financial Assets / Financial Savings. Investments in properties (real estate), gold, silver etc., are Physical Savings / Physical Assets.

Indian Households Savings, Liabilities & Investment patterns (2016-17)

Financial Assets Vs Physical Assets – Which are our preferred Assets?

- From 1990 to 2000, Indian households preferred to invest in Financial assets to Physical assets.

- From 2000 to 2007, more savings were routed to Physical assets.

- Interestingly in 2007/08, more investments were made in Financial assets. This shows that retails/small investors participated in stock markets when their valuations were at peak. The markets eventually crashed in 2008.

- From 2008 to till 2015, we preferred physical savings to financial savings.

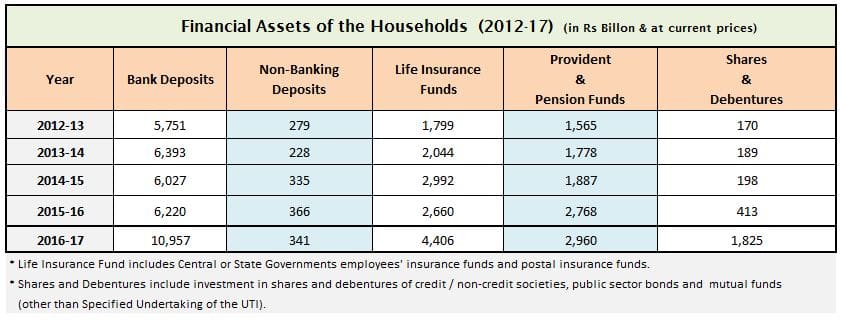

- The Financial Savings during 2014-15, 2015-16 & 2016-17 were Rs 12,826 billion, Rs 15,142 billion and Rs 18,204 billion. There has been a steep increase of around 20% when compared to financial savings of 2015-16.

- The savings in Physical Assets were Rs 14,650 billion, Rs 14,164 billion, & Rs 15,908 billion during 2012-13, 2013-14 and 2014-15 respectively. The data for 2015-16 was Rs 14,951 billion were invested in physical assets.

- The above data clearly indicates that there has been a gradual increase in financial savings rate over the last few years.

Financial Assets (Savings) of the Households (2012-2017)

Financial Liabilities of Indian Households:

- Around Rs 3,470 billion were taken as Loans and advances from the Banks during 2015-16. This figure is around Rs 4,419 for the FY 2016-17.

- Loans taken from other Financial institutions (NBFCs) during 2015-16 & 2016-17 were Rs 837 billion and Rs 1,321 billion respectively.

- The total financial liabilities of the households have increased from Rs 4,317 billion (in 2015-16) to Rs 5,747 billion (in 2016-17).

Bank Fixed Deposits Data : The below table gives you an idea about the total outstanding amount (as on Mar 2017) saved in Bank Term Deposits based on the tenure of the deposits. Term deposits with 1 to 2 year duration were the most preferred ones, followed by the Five year term deposits (these can be tax saving FDs). (Read : ‘Avoid making long-term investments in FDs / RDs / Traditional life insurance plans.‘)

NRI deposits :

- 2015-16 Data : The total outstanding NRI deposits were Rs 8,419 billion, out of which NRE deposits, FCNR and NRO deposits were around Rs 4,740 billion, Rs 3,005 billion & Rs 672 billion respectively. (NRE – Non-resident (external) Rupee accounts, FCNR – Foreign currency non-resident & NRO – Non-Resident Ordinary Rupee Accounts)

- 2016-17 Figures : The total outstanding NRI deposits were Rs 7,577 billion, out of which NRE deposits, FCNR and NRO deposits were around Rs 5,395 billion, Rs 1,361 billion & Rs 820 billion respectively.

Structure of Interest Rates on Bank Deposits (2012 to 2017)

You can notice that deposit rates and lending rates have been in downward trend since 2014-15. Some of the major banks have even reduced the interest rate on saving account deposits from 4% to 3.5%. (Related Article : ‘What is MLCR?‘)

Post office Small Savings Schemes (SSS)

- Indian households’ savings in Post office time deposits and recurring deposits have increased slightly in 2016 as well.

- Since 2011-15 there has been a decline in investments in NSCs, KVP certificates and other popular schemes like Senior Citizen Savings Schemes or Monthly Income Scheme (MIS), however this trend has been reversed in 2015-16. (Read: ‘Latest Interest rates on Post office Small Savings Schemes 2017-2018‘)

- There has been a steady increase in long-term savings in Public Provident Fund scheme (PPF).

Imports of Gold & Silver

- Gold & silver to the tune of Rs 2,106 billion and Rs 276 billion were imported during FY 2014-15, Rs 2,074 billion and Rs 244 billion were imported during FY 2015-16 and around Rs 1,843 billion & Rs 123 billion were imported during FY 2016-17. Thus, we can see a steady decline in imports of Gold & Silver in India.

- The average annual price of Gold (10 gms) in 2016-17 was Rs 29,655 and silver (1 kg) was Rs 42,748.

Mutual Fund Schemes : Assets Under Management

There has been a 40% increase in AUM of Mutual Funds in India during 2016-17. (Read : ‘How to select right & best Mutual Fund Schemes?‘)

Other notable observations

- Share Market Indices: The annual average of share price index of BSE Sensex was 27,338 and Nifty was 8,421 for FY 2016-17.

- Inflation : The CPI (consumer Price Index), which is popularly known as INFLATION has gradually decreased from 10 in 2012-13 to 4.5 in 2016-17.

- CRR & Repo Rates : During 2016-17, the RBI has reduced key policy rates like Repo Rate & Statutory Liquidity ratio. It has kept the Cash Reserve Ratio unchanged. The latest rates as of 2nd August, 2017 are – CRR @ 4%, SLR @ 20%, Repo rate @ 6% and Reverse-repo rate @ 5.75%. (Read : ‘What is CRR/SLR/Repo rate?‘)

- Investments by LIC : LIC has invested around Rs 21,525 billion in Stock-exchange securities during 2016-17(an increase of around 14%).

- Home loans : HDFC has disbursed home loans to the tune of Rs 1,453 billion in FY 2016-17. The total home loans outstanding amount with HDFC is around Rs 2,994 billion.

- Rs 2000 Bank Notes : The high denomination notes of Rs 2,000 were introduced in FY 2016-17. The total value of Rs 2000 bank notes that are now in circulation is around Rs 6,570 billion.

- Electronic Payment System : The FY 2016-17 saw an uptick in the amount of money cleared through ‘paperless & retail electronic clearing systems’. Around Rs 1,32,255 billion were cleared through payment systems like like ECS, NEFT, IMPS and NACH during

Recent data does portend that a shift, albeit small, may be underway. Gold imports have been trending downwards. Additionally, with data also pointing towards greater equity participation (especially in mutual funds) by retail investors over the past few years, it does raise the question as to whether these trends are transitory or whether they are indicative of a shift in the saving pattern of households.

I hope this post is useful and informative. Do you believe that the above data indicates a shift in the saving pattern of Indian households? How do you save and invest your money? Kindly share your views and thoughts. Thank you!

(Reference : RBI’s Handbook of Statistics on the Indian Economy. 2016-17 data is based on preliminary estimates) (Post published on : 16-September-2017)

Join our channels

Really excellent job sir. Sir, is it possible to get information regarding households’s investment in chit funds alone..

Dear Lekshmi,

I doubt if there is any such comprehensive data on Chit funds available..

Really a good article Sree!

I thought the gold and silver investments are increasing but the trend is showing otherwise.

I got the clear picture of the economy now.

Surely, there is an increase in investment in stock markets especially through Mutual Funds.

This means people have now started investing instead of saving in their bank accounts.

Also, this can mean that there will be steady rise in the stock market in the near future.

Thanks for the post.

Dear Rishit,

The last few years have been really good for the equity markets, could be one of the reasons for high retail participation in equity oriented schemes/securities. Also, the returns from Small saving schemes & Bank deposits have been moving southwards, hence there is lot of increased interest in mutual funds and also in other fixed income products like NCDs, Company FDs etc.,

Nice summary Sreekanth.

I think the shift in saving pattern can be because of the reduced FD rates. You agree?

Dear Parag,

Yes, can be one of the reasons. Also, we can see a raise in savings in Post office related schemes (as PPF or Sukanya schemes offer slightly better rates than other debt avenues).

We also need to note that the real estate sector is going through a transformation and only genuine deals are happening (investments for speculation are not happening, thanks to Demonetization, GST effect & RERA Act).

Great work Sreekanth. Your summary is an easy reckoner for understanding the complex financial world.

Thank you dear Rajiv..Keep visiting ReLakhs!