The residential status of taxpayers plays a key role in determining the scope of taxable income (Indian Income / Foreign Income) for a financial year in India and there by the tax payable.

The residential status of an individual is based on the duration for which he/she is present in India. There are 3 types of Residential status.

- Resident & Ordinarily Resident (ROR)

- Resident But not Ordinarily Resident (RNOR)

- Non –Resident Indian (NRI)

According to a Ministry of External Affairs report, there are around 31 million NRIs and PIOs (Person of Indian Origin) residing outside India as of December 2018.

Budget 2020 has proposed two significant changes with respect to calculation of NRI Residential Status and Taxability of Income of NRI.

In this post, let us understand – What the new NRI Residency Status rules proposed in Budget 2020? What are the latest NRI Taxation rules in India for FY 2020-21 (AY 2021-22)? How to determine NRI Status as per the new rules in India?

Latest NRI Residential Status & Income Taxation Rules | Budget 2020-21

Budget 2020 has proposed two new rules with respect to NRIs residency status and Taxation, which are as below;

- Firstly, to be categorized as a non-resident, an Indian now has to stay abroad for minimum 245 days a year, against 182 previously (FY 2019-20). In other words, an Indian national, to claim the non-resident status, can’t stay in India for 120 days or more in a financial year.

- Secondly, a non-resident Indian, who is not taxed in the foreign country, will become taxable in India. The government said it is introducing this provision to prevent tax abuse.

Let us now understand these two amendments in detail.

1) Changes with respect to Residency Status of NRIs for FY 2020-21

As per the Budget 2020, an individual has to meet either of the below (new) eligibility criteria to become Non-Resident India;

- He/She is in India for less than 120 days during the financial year. That means, if you stay abroad for minimum 245 days in previous year (financial year) then your residential status becomes NRI for taxation purposes. (OR)

- If you have stayed in India for less than 365 days during the 4 years preceding the previous financial year AND less than 60 days in the previous financial year.

Example 1 : If you stay for say 260 days abroad for FY 2020-21, then for AY 2021-22 your residential status would be NRI.

Example 2 : If you stay for say 125 days in India then you need to meet the second condition to become NRI. That is, you should have stayed for less than 60 days in FY 2020-21 AND less than 365 days during 4 financial years before the FY 2020-21 in India.

Latest NRI Status Online Calculator for FY 2020-21 / AY 2021-22

You can use the below online residential status check calculator, which is as per the Budget 2020 proposals..

Kindly keep the below points in mind while entering the no of days in the above calculator:

- Previous Year is period of 12 months from 1st April to 31st March. Number of days stay in India is to be counted during this period.

- Both the Day of Arrival into India and the Day of Departure from India are counted as the days of stay in India (i.e. 2 days stay in India).

- Dates stamped on Passport are normally considered as proof of dates of departure from and arrival in India.

- Keep track of no. of days in India from year to year and check the same before making the next trip to India. It is advisable to maintain a chart for the number of days stay in the current and in the preceding seven (7) previous years.

2) Budget (2020) Amendments with respect to Taxability of NRI Income for AY 2021-22

Below is the proposed amendment in Budget 2020 which will affect taxability of NRI Income;

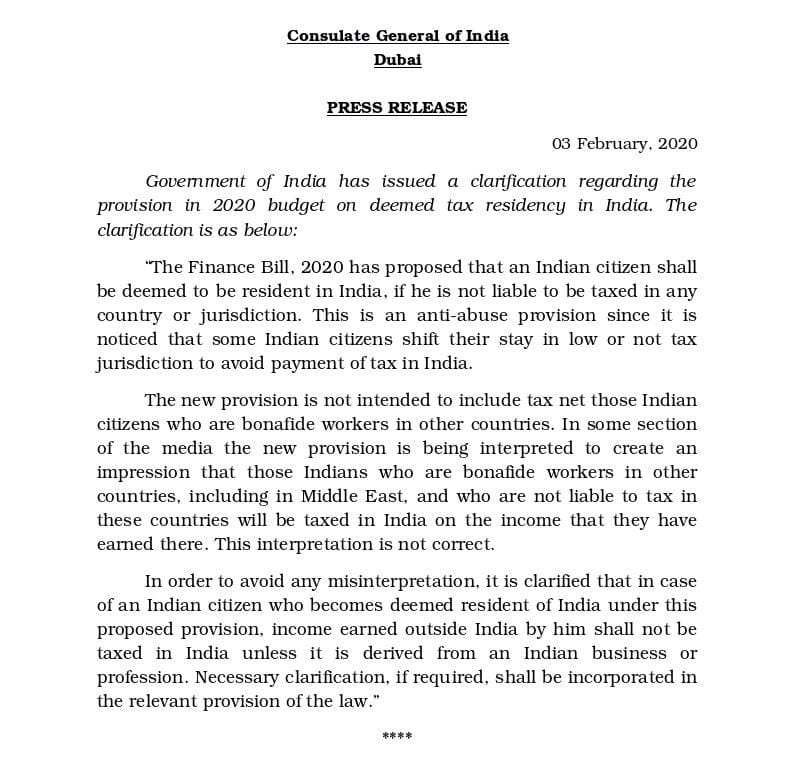

“An individual, being a citizen of India, shall be deemed to be resident in India in any previous year, if he is not liable to tax in any other country or territory by reason of his domicile or residence or any other criteria of similar nature”

This proposed new rule has created quite a confusion among the NRI fraternity.

Wrong Interpretation of the new rule:

It states that If any person who is citizen of India and not liable to tax in any other country or territory by any specified reason then he/she will be treated as resident of India despite of his residency status NRI or whatever. It is important to note that once he becomes resident under this clause his/her global income will be taxed in India.

Example : Let’s say you are an NRI employed in UAE, your income earned in UAE is tax-free and you are not liable to pay any taxes there. Now, as per this rule, as you are not paying taxes in UAE, your global income will be taxable in India.

Correct Interpretation of the new rule :

The CBDT/Govt has been quick enough to clarify on this confusing proposal.

“Genuine NRIs need not worry, because the aim of the legislature is to catch people who are evading the tax net. What matters is the tax incidence and not the tax rate in a foreign country,”

Since the tax exemption on salary in countries like say, UAE, is conferred by the law of that country, it will not be taxable in India.

So, whose NRIs’ income will be taxed as per the new rule? What happens to Indian citizens who live in countries where there is no tax on individual incomes?

Scenario 1: An HNI businessmen whose Residential status is NRI, resides in different countries in a Financial Year, thus making him a non-tax resident of any country. So, his global income is neither taxable in those countries nor in India. To remove this ‘tax arbitrage’ (loophole), the Govt now wants to tax such NRIs’ global income. (This new rule can have a negative impact on ‘Seafarers’ profession.)

Scenario 2 : An HNI businessmen whose Residential Status is NRI, resides and does business in Dubai, his global income is tax-free in Dubai and such income is also not taxable in India (he/she will not be deemed to be resident in India just because he/she is not liable to be taxed in Dubai).

Note that an NRI’s Indian income continues to be taxable in India. This income can be – interest on your bank fixed deposits, rents received from property, profit/loss from shares etc.,

Also, there can be situations where in your income may be liable to tax in foreign country as well as in India. To avoid such double taxation or to get relief from double tax, you need to check if India has any tax treaty with that nation or not. The concept of ‘Double Taxation Avoidance Agreement’ comes into picture.

Continue reading :

- How NRIs can save on Tax in India? | NRI Tax Saving options

- Latest NRI Gift Tax Rules 2019-2020 | Gifts to NRIs can be Taxable now!

- Should NRIs buy Health Insurance in India?

- New Income Tax Slab Rates Vs Old Tax Regime | Which one is better?

(This post is intended for general information purposes only. We strongly recommend you to consult an expert for your taxation/legal matters.) (Post first published on : 07-February-2020)

Join our channels

Dear Sreekanth,

I am an NRI since year 2012 and at present in India from last few months (due to covid). I think I won’t be able to go abroad until Mar 2021. If there is no relaxation approved by India govt, my tax residency for FY2020-21 is going to be RONR. My questions are

1) Do I need to convert my NRE account to Ordinary savings account? My present stay in India is temporary only and I will definitely go back to abroad.

2) Under RONR status do I need to pay Indian income tax on interest earnings from NRE FDs?

Dear Vinod,

Under RNOR status, you can maintain your NRE accounts and interest is still exempted from tax.

You may kindly consult a CA as well..

I have been made to understand that once u return to India you can not continue NRE account and FD. All have to be converted to resident account and FDs and become taxable. Otherwise it is FATCA violation. Please clarify.

Dear Mr Agarwal,

Partially correct, as there is an option (if eligible) like ‘RNOR’….

Dear Mr Reddy, Please clarify if the NRE FDs are taxable during RNOR status or not?

Dear Mr Agarwal,

As RNOR, you can continue to enjoy tax free status of your existing deposit held in foreign currency ( like in FCNR). In case you are holding the funds in INR ( like in NRE FD), your interest earning will become taxable as per individual slabs, in-spite of you being RNOR

Kindly go through this forum thread…

Dear Sreekanth, thank you for your information.

I’m currently staying in India for the past five years after I returned back from NewZealand. I am a NewZealand citizen & currently holding an OCI card. I haven’t updated my NRE account with the bank yet. With this new rule I’ll update to the resident status to the bank and convert to the SB account. I lived in NewZealand for the past 10 years.

I want to know what happens to my case as I didn’t updated my NRE account since beginning. Thank you.

Hi Sreekanth,

Thanks for providing all the details and educating us about the same.

I am currently an Indian Resident and will be moving to Singapore for my new job. I have no plans of coming back to India for at least 2 years.

Need your help/advice on what should I be doing with my saving accounts and investments currently held in India. My queries are as below, I would appreciate if you could briefly

advise me on the same.

–> I am currently investing in mutual funds through my Axis saving bank account (SIP) and planning to continue these investments. Could you please advice what

should be the type of the account to continue these investments (NRE/NRO). No plans to sell them for at least 7-10 years.

–> I also have 2 DEMAT Accounts with shares in them and have no plans of selling them as of now. Should I need to close these accounts and open a new one to transfer these shares?

–> I also have 2 saving bank accounts on my name which I use for my loan EMIs. What should be the type for these accounts as my EMIs will continue after I move abroad. Please note both these accounts are

joint accounts with my brother (NRI status).

–> Also do I need to update my KYC details with each and every fund house before moving abroad or there is a centralized way to do this?

Thanks,

Paritosh Maithil

Dear PARITOSH,

1 – Once your residential status is NRI, you need to update all your Financial Service / Product providers. NRIs can invest on repatriable or non-repatriable basis using funds from the NRE or NRO accounts respectively. So, its your choice. You need to get FATCA compliance. Some MF houses may not offer schemes for investments by nris.

2 – Need to update your Residential status to NRI. As an NRI you cannot continue to operate your regular demat account. Your existing demat account, which holds shares that you purchased while you were a resident Indian, will have to be closed and you would need to transfer the shares to an NRO demat account.

3 – The repayment of loan through equated monthly instalments can be made either through the NRO account or through the NRE account.

4 – You can get your cKYC done .

Read :

* FATCA Compliance Requirements & Impact on Your Mutual Fund Investments

* What is new cKYC? How to get Central KYC done?

Thank you Sreekanth for a prompt reply.

Dear Mr. Reddy. I am working in Kazakhstan on a 28/28 basis. So I am out of India more than 190 days including travel days. My salary is taxed in Kazakhstan and remitted to NRE account in India.

2 questions –

1. Since I am tax resident of Kazakhstan do I automatically become NRI or does the new 245 day rule apply.

2. If I am deemed resident of India and my global income is not taxed in India, will I still be allowed to operate the NRE account.

Dear Ranvir,

You got to stay minimum 245 days out of India, to be an NRI.

(OR)

If you have stayed in India for less than 365 days during the 4 years preceding the previous financial year AND less than 60 days in the previous financial year.

If you are not meeting any of these conditions then your residential status can be Resident Indian and can not operated NRE account.

In that case you need to check if you can claim benefits under DTAA rules as your salary is being taxed in Kazakhstan .

I believe we (India) has DTAA agreement with them. Suggest you to take help of a CA who deals with NRI taxation matters.

Thanks for the clarification and advice

Dear Sreekanth

CBDT has clarified that outside income of genuine workers will not be taxed in India if any one becomes resident as per new rules.

Will interest on NRE deposits be taxed as per new budget if I stay more than 120 days in India

Dear Viswanathan,

If anybody becomes Resident Indian, then his global income will be taxed in India subject to DTAA rules.

If Residential status is RI, can not maintain NRE deposits..

A seaman should always have the previlege of having NRI status as they live half of the year away from their family.

Dear Prashant ..Yes, this new tax proposal is a bit harsh/tough on Seafarer..let’s see if the govt relaxes this proposal for genuine cases..

Who is forcing you…