The National Savings Schemes (NSSs) are one of the very popular saving schemes in India. These are regulated by the Ministry of Finance. They offer complete security of investment combined with attractive returns.

These schemes also act as instruments of financial inclusion especially in the geographically inaccessible areas due to their implementation primarily through the Post Offices, which have reach far and wide.

It is estimated that nearly $137 billion or over Rs. 9 lakh crore are tied up in small savings schemes.

Some of the very popular schemes which fall under NSS are as below

- PPF (Public Provident Fund)

- Sukanya Samriddhi Scheme

- Monthly Income Scheme (Monthly Income Account)

- Senior Citizen Savings Scheme

- KVP (Kisan Vikas Patra)

- NSC (National Savings Certificate)

- Time Deposits &

- Recurring Deposits

Small Saving Schemes Interest Rates & New norms w.e.f. April 2016

Let’s have a look at what are the changes that have been implemented regarding Small saving Schemes’ interest rates;

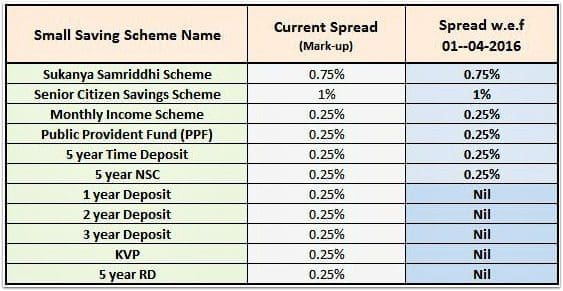

- As per the current norms, the interest rates of these small saving schemes are linked to the yield of government bonds of comparable maturity (with a small mark-up) and are revised once a year. Mark-up here refers to ‘Spread’.

For example : The interest rate on PPF has a mark-up of 25 basis points over and above the G-Sec rate (Govt Bonds rate). So, if comparable maturity G-sec rate is say 8.5% then the interest rate on PPF will be determined as 8.75%. (One Basis Point is equivalent to 0.01%)

- The government has decided to revise Small Saving Schemes Interest Rates on a Quarterly basis.

- The saving schemes like Sukanya Samriddhi, Senior Citizen Savings Scheme and Monthly Income Scheme enjoy ‘spreads’ over the G-sec rate of comparable maturity viz., of 75 basis points (0.75%), 100 bps (1%) and 25 bps respectively. These mark-ups / spreads have been left untouched by the Government.

- Similarly the spread of 25 basis pointss that long term instruments, such as the 5 yr Term Deposit, 5 year National Saving Certificates (NSC) and Public Provident Fund (PPF) currently enjoy over G-Sec of comparable maturity, have been left untouched.

- The 25 bps (0.25%) spread that 1 year, 2 year and 3 year Term Deposits, KVPs and 5 yr Recurring Deposits have over comparable tenure Government securities, shall stand removed w.e.f. April 1, 2016 to make them closer in interest rates to the similar instruments offered by the banking sector.

- The interest rates on a 10 year National Saving Certificate (discontinued since 20-12-2015), 5 year National Saving Certificate and Kisan Vikas Patra is compounded on half-yearly basis. This shall be done on an annual basis from 1st April, 2016.

- Premature closure of PPF accounts shall be permitted in genuine cases, such as cases of serious ailment, higher education of children etc,. This shall be permitted with a penalty of 1% reduction in interest payable on the whole deposit and only for the accounts having completed five years from the date of opening. (Read : ‘PPF Account pre-mature closure – latest rules, eligibility & amount calculation‘)

Latest Post Office Small Saving Schemes Interest rates FY 2018-19 (January to March 2019)

Due to the increase in interest rates in the economy by the RBI, it was expected that the government would increase interest rates on small savings schemes as well. But, the Govt has kept the rates unchanged in the second quarter of FY 2018-19.

However, the rates of interest on various small savings schemes for the third quarter of financial year 2018-19 (Oct -Dec 2018) have been increased.

For the last quarter of FY 2018-19 (Jan to Mar), the interest rate on 1 year Fixed Deposit and 3 year term deposit has been decreased. The rates for all other Small Savings Schemes have been kept unchanged.

The rates of interest applicable on various small savings schemes for the quarter from Jan to Mar 2019 effective from 1.01.2019 would be as below;

- The new rate of Interest on Sukanya Samriddhi Scheme (SSA ) is 8.5%.

- The new rate of Interest on PPF (Public Provident Fund) would be 8%.

- The interest rate on Senior Citizen Savings Scheme (SCSS) has been retained same at 8.7%.

- New interest rate on Kisan Vikas Patra (KVP) would be 7.7%.

- The rate of interest on 5 year National Savings Certificate (NSC) is 8%.

- New interest rate on post office MIS (Monthly Income Scheme) is 7.7%.

- The rate of interest on a 5 year Post Office RD (Recurring Deposit) would be 7.8%.

(Click on the above image to open it in a new browser window)

Latest updates :

- Govt allows all Public Sector Banks and three Private Banks (ICICI, HDFC & Axis) to accept deposits under Small Savings Schemes like National Savings Certificate (NSC), Recurring Deposits and Monthly Income Scheme (MIS).

- It has now been decided to extend the last date to link Aadhaar with Small Savings Schemes from 31 March, 2018 indefinitely, until further orders.

Continue reading :

- Why you should not invest in Fixed Deposits / RDs for long-term?

- Are you aware of this interesting fact on Bank Fixed Deposits?

- Tax Saving investment options u/s 80c : In whose name can they be invested?

- RBI hikes interest rates | RBI’s Rate hike & its Impact on the Economy & your Personal Finances

- RBI’s statistical data on Indian Households Savings & Investments (2017-18) | How & Where do we save & invest?

(Source : Min of Finance Notification) (Post first published on 29-March-2018)

Join our channels

Sreekanth sir,

I have technically resigned a state government job after serving 11 years and joined railways. It was the matter of 2014. Railways are denying the service continuity for which still I’m fighting.

May I withdraw my GPF amount which is still not transferred to railways from state government department due to service continuity reasons?

Kindly help and suggest a way.

Dear Nikhil,

I do not have the required information.

I have read that Railways may offer NPS instead of GPF going forward..

Hi sreekanth, can you help me regarding the following issue on PPF account: As on 1st April PPF account balance is 1,48,857.00 and on 3rd Jan-2018 I have credited 32,500.00 in PPF account. For the F.Y. 2017-18, I got 10,706.00 as interest. But, as per my knowledge, the accumulated interest seems to be incorrect. Can you please give your views.

Dear srinivasrao ..Kindly refer to our FB chat.

how to get maximum benefits from post office by investing????

Dear soundhu ..May I know your Financial goals and time-frame??

Hello sir,

I am looking a for morgatge loan on my house papers which is paagdi house so can I get loan on that Property. If yes in which bank can I get loan ? &what rate of interest ?

Dear Ashok,

If you have a savings account, you may kindly approach them for more details.

My jijaji tried to open joint account under the names 1st holder my younger sister(jiju wife) , 2nd holder elder sister & third holder my brother(who is mentally disabled) but after insisting by me he added my name as 4th account holder under mode of operation as ‘Anyone or survior’. after opening he tranfers huge amt. chq. bearing my brother name. recently my brother recd. these chq. from sale of land from fathers property. my father was expired before 2yrs & my husband also expire in last yr. now jiju said me don’t show any transaction on my behalf. i am paying the hospital bills of my brother & younger sister give a chq. of that amt. from joint account. cheque book is in the hands of my younger sister. i want to know that what are my rights in this account. may i demand cheque book from bank for my brothers hosp. bills. Is there another norms for this joint account. many times i visited bank i request for transaction alert messages and bank ragister for the same but still i dont receive the messages. now what should i do? if my brother dies then who claim the balance money from the account as my brother suffering from illness. i insist jiju to make fd under my brothers name but he ignore me that fd can be made in the name of 1st a/c holder & tax also paid by 1st account holder. bank also giving the same statement. can we close the joint account by transfering amt. in my brothers bank account. please give your opinion.

Dear vaishali,

May I know the type of property that has been sold? Was it an ancestral property or self-acquired property by your father?

Kindly read : What is an Ancestral property?

Whose name has been mentioned as nominee for the said bank account?

Kindly note that nominee is again just a Care-taker of these investments. He/she has to receive the asset/money from the concerned bank or financial institution and transfer/distribute that to Legal owners. All legal heirs have rights on these investments.

As the cheque that has been credited was in your brother’s name, I believe that your Jijaji may not get a claim on this amount, if you go legally.

Kindly save the bills paid by you/sister as documentary proof that you have been taking care of your brother, for future reference (if any)..